Beef Wrap May 28

The cash cattle market was essentially unchanged this week, with the

average for live transactions coming in at $119.64. In the previous two

weeks, the averages were $119.73 and $119.72, so you can see that

there has been almost no movement in the cash cattle market for three

weeks now. In fact, it looks like someone is intentionally trying their

best to hold the market just below $120. There is a growing sense that

packers are simply being generous and paying $120 for cattle even

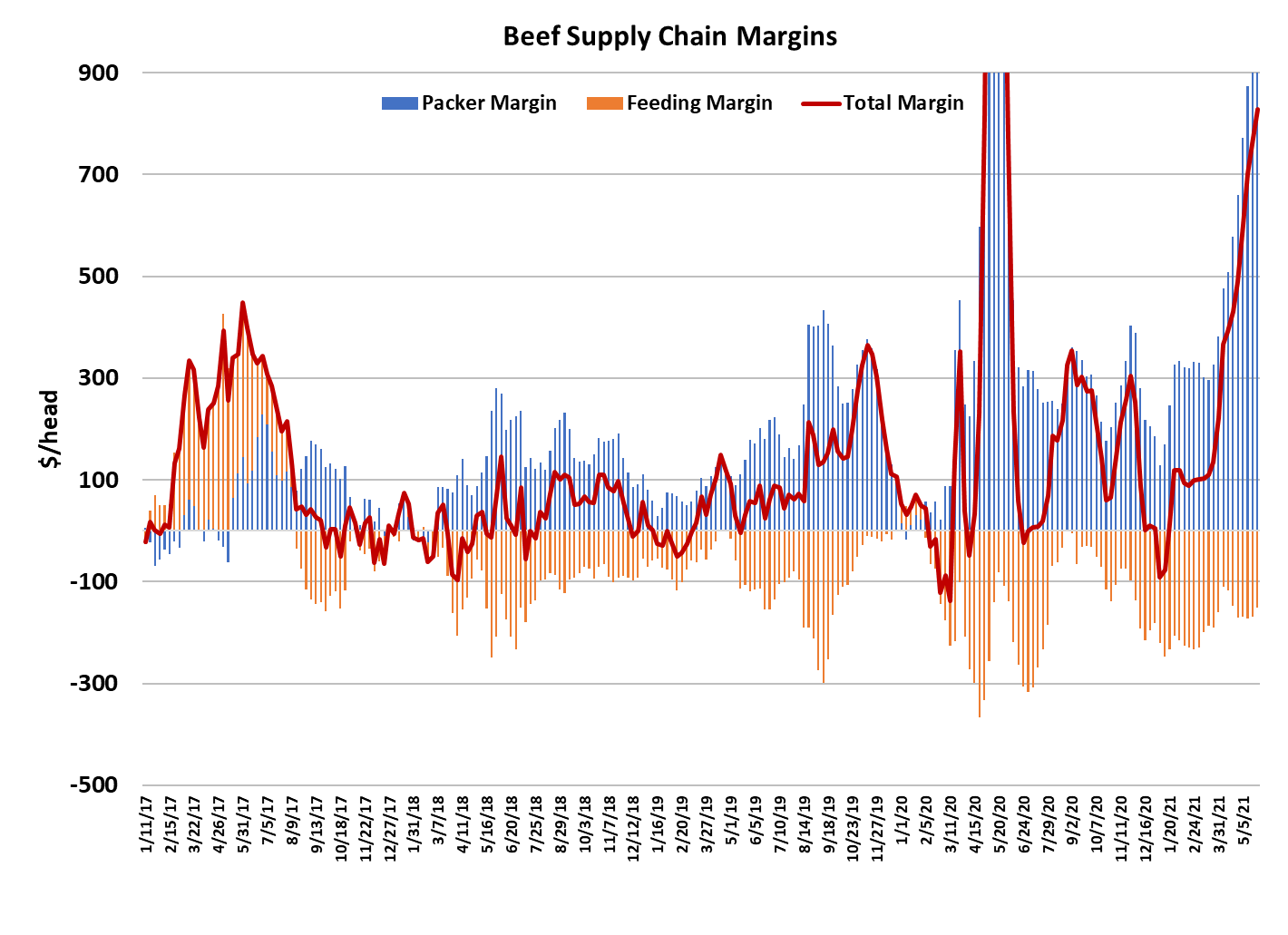

though they don’t need too. I calculate their net margin this week at

$981/head, so I guess they can afford a little generosity. Everything

points to a bottleneck at the packing plant level caused by insufficient

labor to run plants at full capacity.

As we were coming into spring, I was willing to grant packers a

$200-300 per head margin because there were some labor issues, but

the labor issues must be far more severe than I envisioned to push

margins up close to $1000/head. That was the big miss on my part and

it is why the cash cattle (and futures) haven’t followed the beef markets

higher this spring. Going forward, this means that getting the cattle

price forecast correct is going to entail correctly predicting what

happens to labor in packing plants. Will it get tighter? Will packers find

a way to entice more workers? My guess is that packers will raise

wages slowly and gauge potential workers’ reaction. It is not

reasonable to think that they can hire on new workers at a higher rate

than existing workers, so they will also need to raise wages for existing

employees. That means their cost per unit of beef produced is going to

rise. And you know who they are going to expect to cover those

increased costs—consumers and cattle producers.

Traditionally, beef plants have made big use of immigrant labor but for

the past four years the US has done everything imaginable to

discourage immigrants from coming to this country. I think that is part

of the problem also. The labor pool for packing plants to draw from has

shrunk due to the actions of the previous administration. So, wages

will be raised slowly, more workers will be hired slowly, and thus it takes

a long time for this labor issue to get resolved. Not to mention that you

just can’t hire someone off the street and expect them to properly debone a round the next day. Training is required. All of this argues for a

very slow return to normalcy and thus exceedingly large packer margins

for some time to come. It also means we shouldn’t expect too much

strength in cash cattle prices while this process is playing out.

Accordingly, I raised packer margin forecasts through the balance of

2021 and that pushed the cash cattle price forecasts lower. The beef

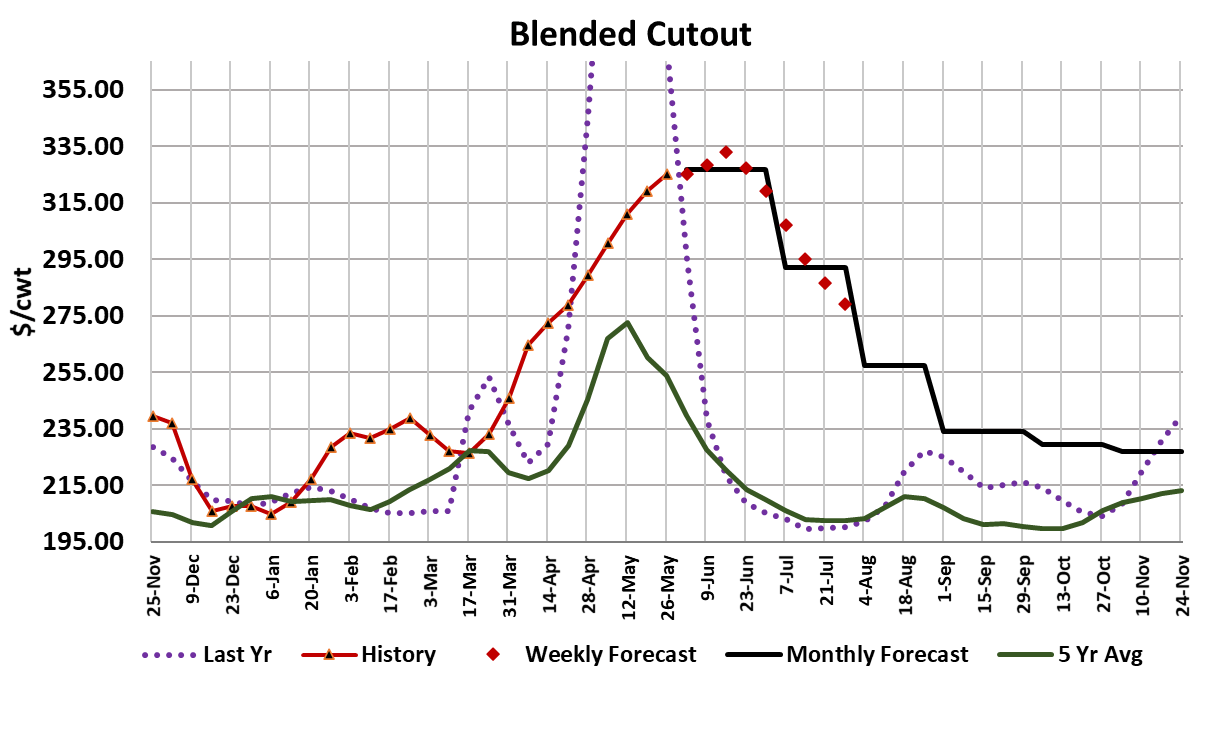

markets, on the other hand, are doing quite well. The Choice cutout

gained $6.50 on a weekly average basis and the Select was up $3.43.

I had fully expected a very strong beef market this spring, but this is well

beyond anything I could have imagined.

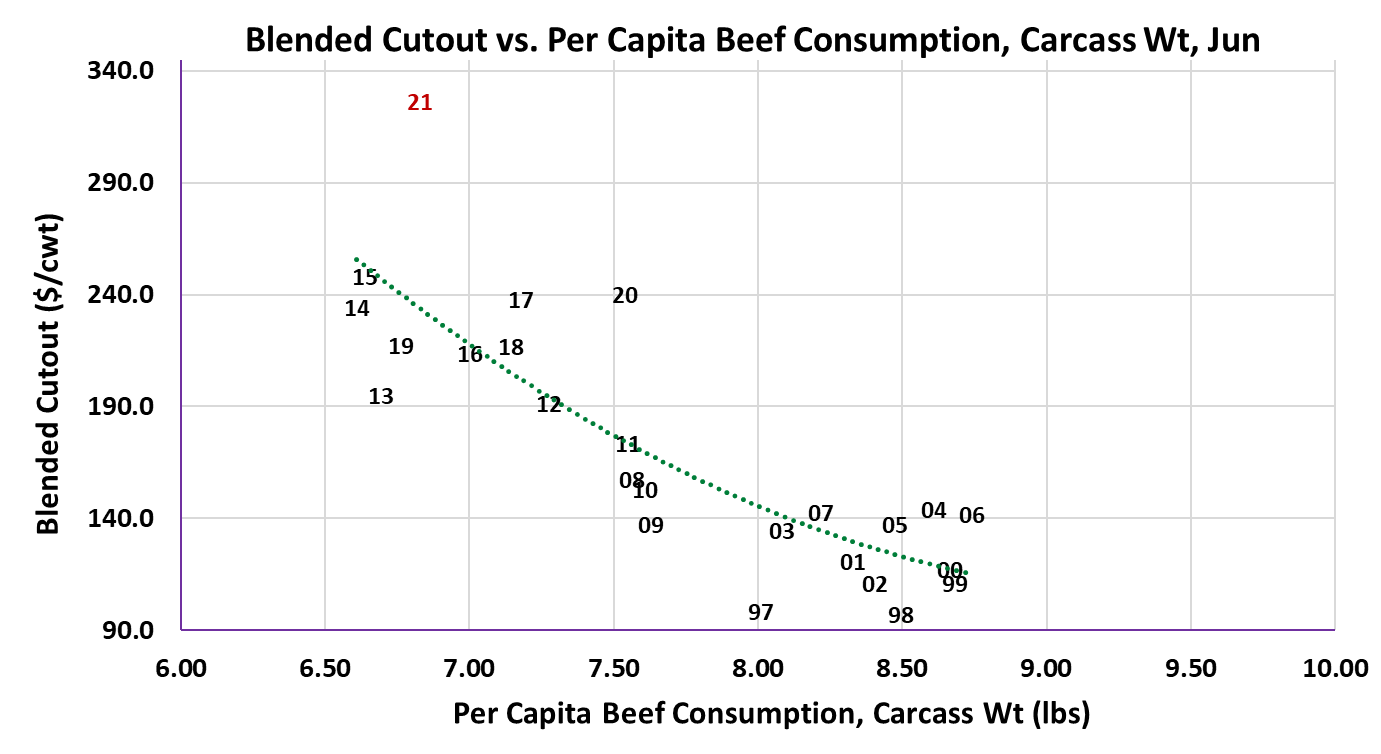

Some have suggested that retailers are still pricing their product too

low and that is causing customers to purchase more beef than they

would if retail prices adequately reflected the rapid rise in wholesale

prices. There is probably some truth to that, but how long will retailers

wait to push pricing higher? Given that nothing has been able to slow

the steady rise in beef pricing, I’m of the opinion that price just doesn’t

matter all that much to consumers right now because they are in a

celebratory mood as the pandemic fades. That, of course, won’t last,

and we will eventually get back to a situation where price does matter,

but it might be many weeks or months down the road.

Another point on this bizarre demand situation: Memorial Day doesn’t

seem to matter either. Normally, we expect demand to fall once the

holiday buying is complete, but this year there was none of that. That

tells me that whatever is driving this abnormally strong demand is far

stronger than the normal holiday effect that we see. That is pretty

important because the Memorial Day effect is one of the strongest and

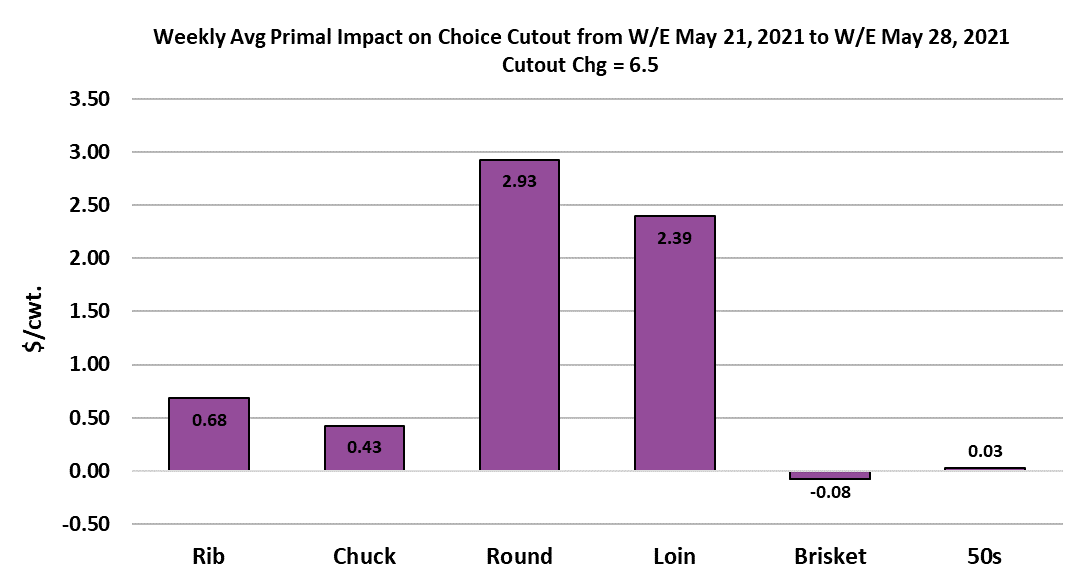

most dependable seasonal trends in animal agriculture. The chart

below indicates that this week, rounds were the biggest contributors to

the cutout’s increase and that is another really unusual aspect of this

rally—end meats have been star performers. The combined margin

chart just keeps moving higher, which is an indication that this demand

strength isn’t done yet. I pushed beef price forecasts higher again this

week and still have this nagging feeling that I’m too low. The fed kill

this week clocked in at only 501k, as packers decided to do a very light

Saturday kill. That was about 35k less than last week and keep in

mind that next week will be a short kill also. So near-term beef

availability is going to tighten up and that doesn’t seem conducive to

lower pricing in the short run.

The weather forecast for Memorial Day weekend looks pretty good

across most of the US, so its reasonable to think that retail clearance

will be good and that means retailers will be back in the market on

Tuesday looking to re-stock. Another interesting aspect to this bizarre

spring market is that high prices haven’t seemed to matter at all to the

export markets. The weekly numbers suggest that beef exports are

running along at the same pace as they were back in March, when

prices were much lower. In fact, I’m projecting May and June beef

exports to be larger than they were in March. I did some upward

revisions to the 2021 export forecast and now have them up almost

17% from last year. Next week, I’m forecasting cash cattle to trade in

the $119-120 range (hey, you can’t blame me for taking that easy one)

and the cutouts to be another $4-5 higher. Packer margins are likely

to break the $1000/head mark soon.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}