Beef Wrap May 14

Cash cattle traded in the $119-120 range this week, up about

$1.50 from the week before. Strong gains in the futures early in

the week likely prompted packers to pay up, but the market sold

off hard on Thursday and that brought the higher cash trade to an

abrupt end. Packers had plenty of extra revenue to pay for cattle

this week, given that the Choice cutout added almost $10 and the

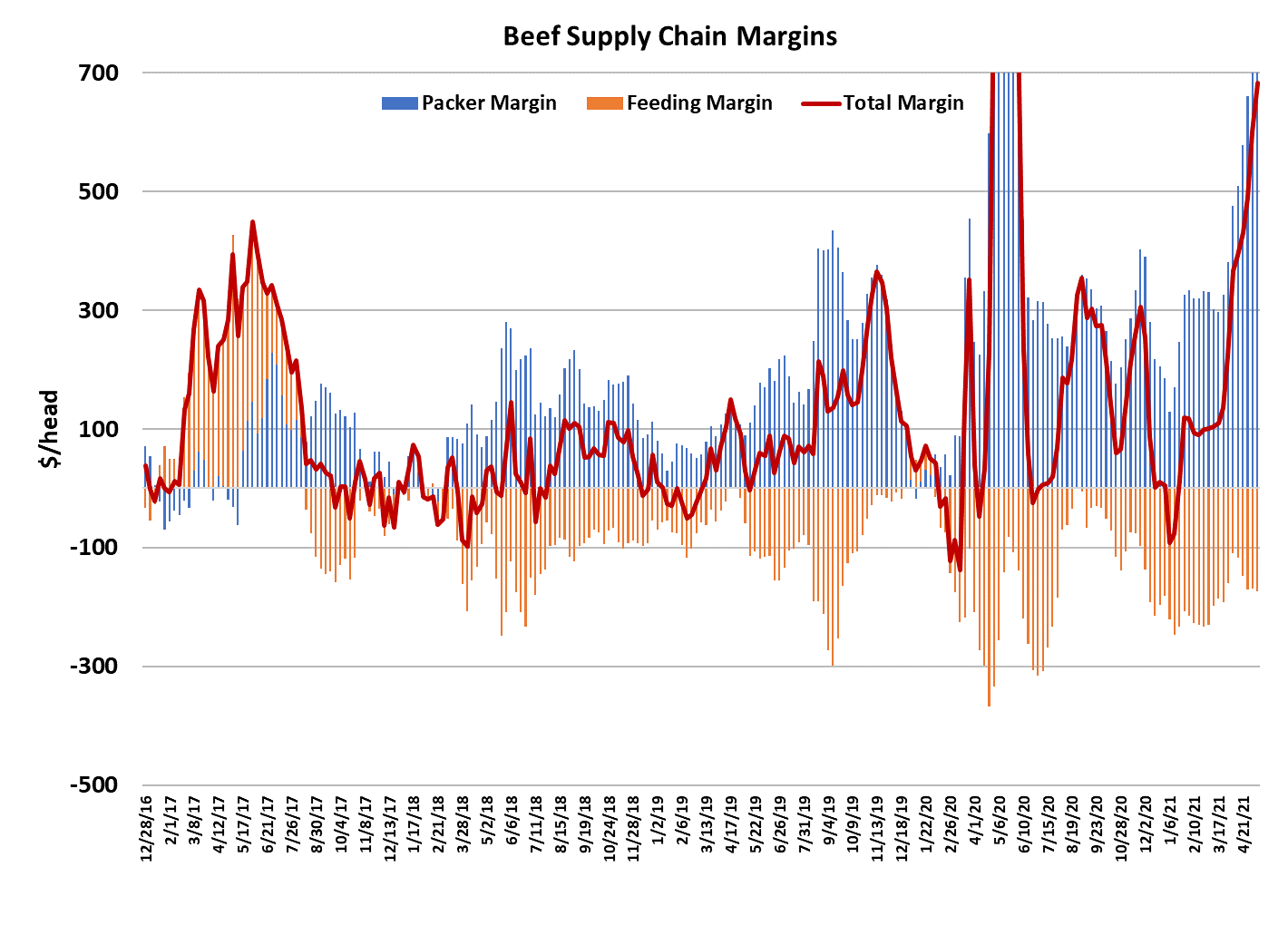

Select cutout was up $9. Of course, packer margins expanded

once again, adding almost $100/head and the margin is now

around $855/head (I recently revised the margin calculation to

reflect higher labor costs, so that is why this week’s margin

appears to be less that what was reported last week.)

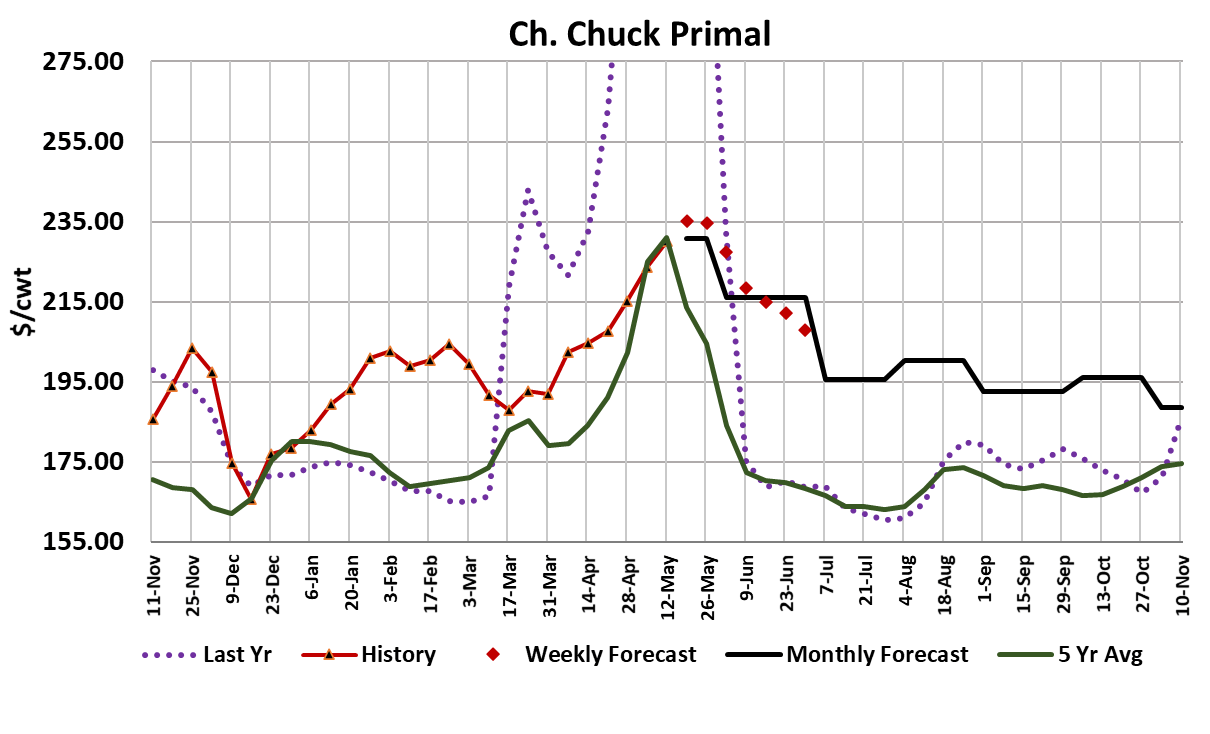

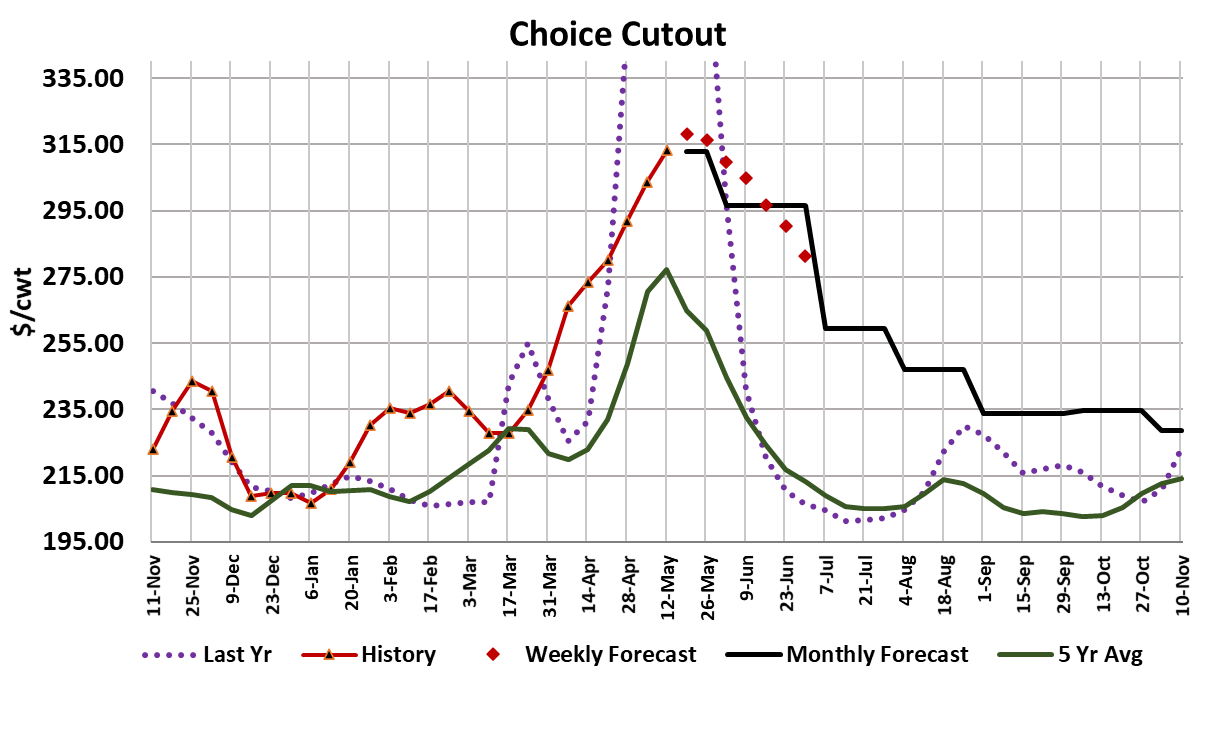

Once again, the Choice cutout exceeded my target level for a top

and forecasts had to be raised. It seems to me that we can

expect the cutout to gain again next week as the finishing touches

are put on Memorial Day buying, but that could very well be a

near-term top in the cutout. Who would have thought that chucks

and rounds would be more influential to the cutout in the second

week of May than ribs? That is exactly what happened this week.

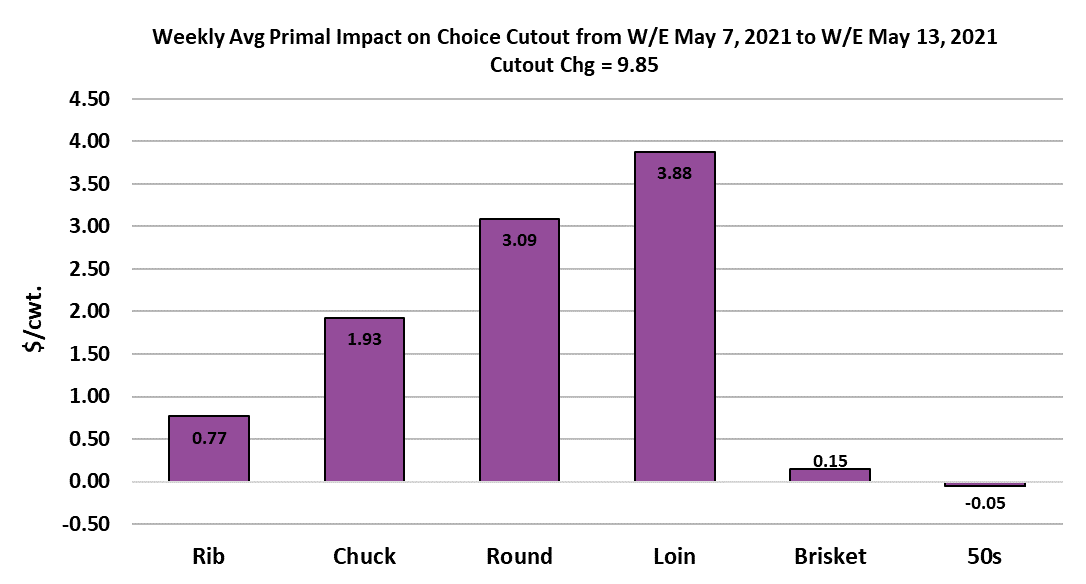

In fact, the chart below indicates that all of the primals were

higher this week, with the exception of a tiny drop in the 50s. The

uncharacteristic strength in end meats at this time of year is part

of what makes me think that a shift in consumer dietary patterns

toward more high protein diets is partly responsible for the

incredible demand strength that we’ve seen this spring. Those

consumers don’t necessarily follow the normal seasonal

consumption pattern. They are just looking for protein variety.

The combined margin chart below shows that the current demand

upcycle is still in play and by far the strongest we’ve seen outside

of the COVID-related plant shutdown period last year.

My guess is that demand will cool off some once we get to

Memorial Day, but I wouldn’t expect it to fall sharply. It is pretty

clear to me that a lot of the recent demand strength is unrelated to

the holiday and so it wouldn’t make sense to expect demand to

retrace rapidly once the holiday is behind us. Supply

considerations will also help to support prices beyond Memorial

Day. Packers are struggling to keep plants fully staffed right now

and that is not going to be a short-run phenomenon. I’m

estimating that this week’s fed kill might only be 495k. That’s

about 10-15k below what I think the supply would support and it

will probably cause some minor backing up in feedyards.

There is not much doubt that with $850/head margins, packers

would kill everything they could get their hands on if they had the

capacity to do so. So, the only conclusion that I can make is that

they don’t have enough dependable labor to run at full capacity.

It is more of a problem for cattle producers and beef buyers than

it is for packers however. This super-tight labor situation is

driving a big wedge between beef prices and cattle prices, raising

the beef price and pressuring the cattle price. To rectify the

situation, cattle feeders need to put the brakes on placements in

order to scale back on-feed inventories.

Drought is also reducing pasture availability and thus driving

more cattle into the feedyard than would otherwise be the case.

As long as cattlemen continue to place like it’s a pre-pandemic,

2019-type market instead of a labor-constrained, 2021-type

market, packer margins will stay uncharacteristically wide and

cattle prices will underperform. Cattle feeders are very fortunate

that we’ve had such strong demand this spring or else cattle

prices would be a lot lower. Given super-high feedgrain costs, I

estimate that cattle feeding margins this week were in the red to

the tune of $170/head. Persistently negative margins are the

market’s way of sending a signal to downsize. Of course, beef

buyers who are staring at a $313 Choice cutout right now don’t

think the industry should downsize at all. Very strong demand

from consumers is saying “expand”, but the labor wedge in the

packing sector is telling producers “contract”.

These mixed signals are not good for the long-run health of the

industry. In the end, consumers will pay more for beef, producers

will get paid less for cattle, and the industry will be smaller than it

would be had the labor problem not arisen. Next week, watch

the cutouts for signs that a top is forming and watch the reported

carcass weights for signs that feedyards are losing currentness

due to these unusually light May kills.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}