Beef Wrap March 4

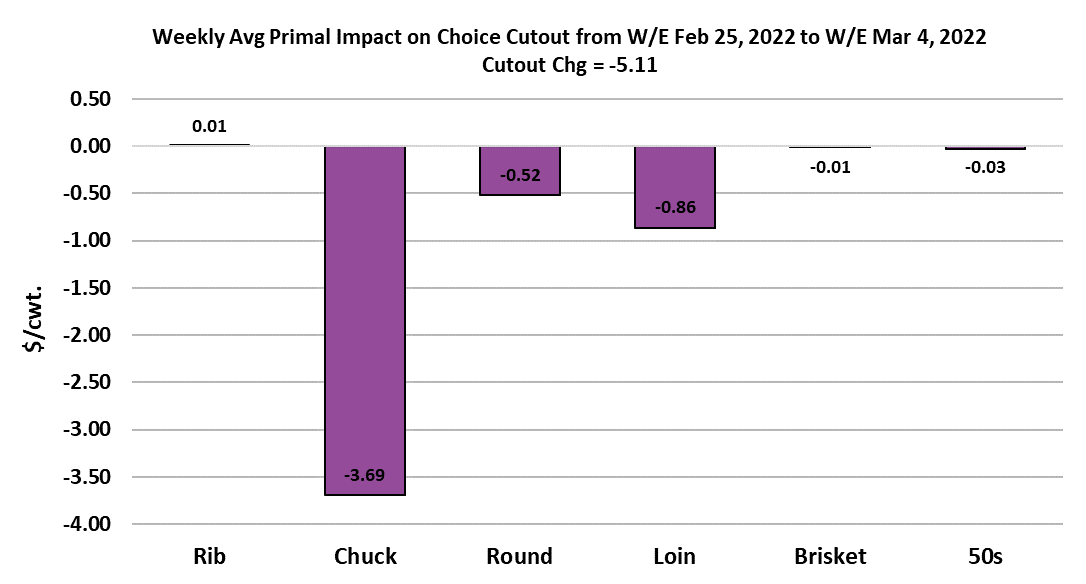

The slide in beef prices continued this week, with the Choice cutout

dropping $5.11 on a weekly average basis and the Select cutout

down $8.39. Cash cattle finally turned lower, dropping almost $3

from the week before to average $140.76. Packer margins finally

narrowed enough that packers felt the need to put some pressure on

the cash cattle market and they were helped along by the escalation

of hostilities in Ukraine, which made the market very jittery. There

has been a lot of talk about how the war in Ukraine will hurt beef

demand and while there is some truth to that, we need to recognize

that beef demand was on the decline well before this war started. In

my opinion, the end of the pandemic posed a bigger threat to beef

demand than the war. However, the war will certainly exacerbate

inflationary pressures across the economy and that will stretch

consumer’s budgets to the point where they will likely decide they

can forego that expensive steak and make do with pork chops or

chicken.

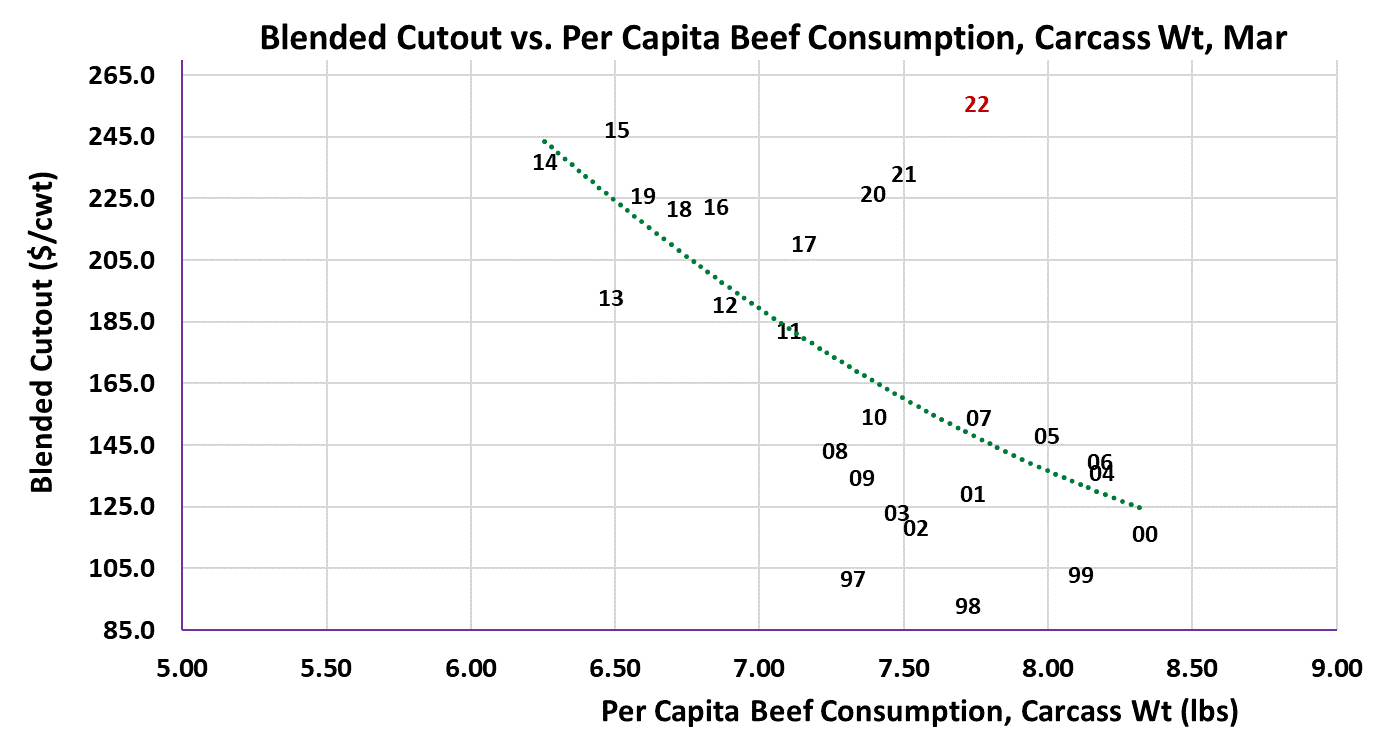

Beef is the most vulnerable protein as the demand side resets in

2022 following an epic demand year in 2021. That said, we are

beginning to see spring-like weather in the Southern US and that

should bring out some seasonal demand improvement for grilling

items over the next few weeks. My guess is that the cutouts will put

in a bottom next week and then start grinding higher as middle meat

prices begin to improve. This week it was the chucks that were the

biggest drag on the cutout. Brisket prices were lower early in the

week, but began to improve near week’s end. That may be tied to

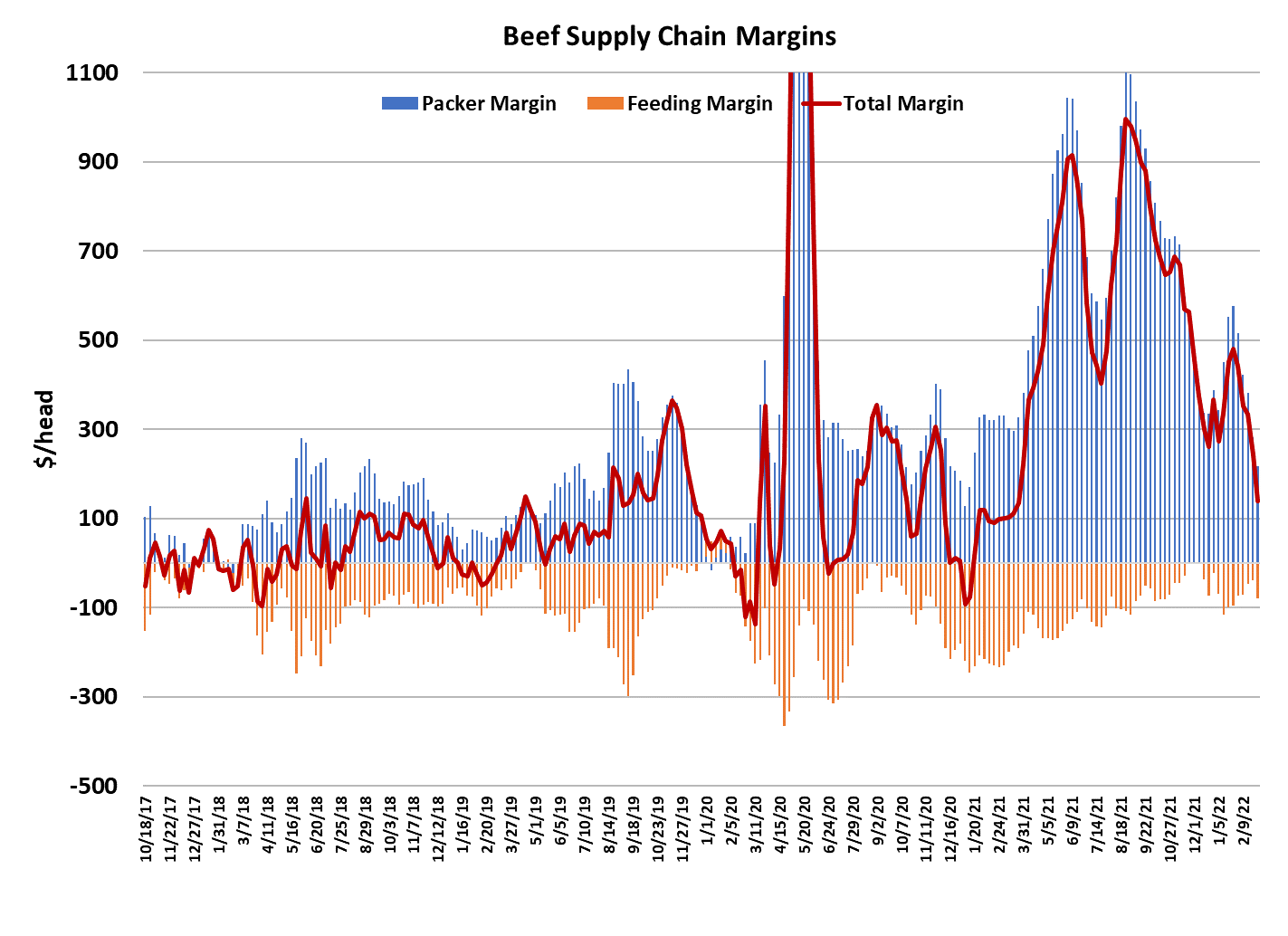

last minute buying ahead of St. Patrick’s Day. The combined margin

is still heading lower and it is clear that this next bottom will be well

below any bottom that was made during the “great demand bubble”

last year. This looks like a sign that demand is working its way back

to more-normal levels. It will be interesting to see how quick the next

upcycle develops. I expect that it will be slow to get started, but will

probably show stronger gains once we get beyond March.

I don’t expect packers to immediately begin to pay higher money for

cattle just because the cutouts bottomed and turned seasonally

higher. They will probably keep some pressure on the cash cattle

market for a couple of weeks and then let it go sideways for a while

as their margins get back on good footing. I calculate this week’s

margin at $218/head—the smallest packer margin in over a year. I

expect it will slowly grow from here, but don’t look for it expand back

out to $600-700 head like it did last spring. Cattle feeders are

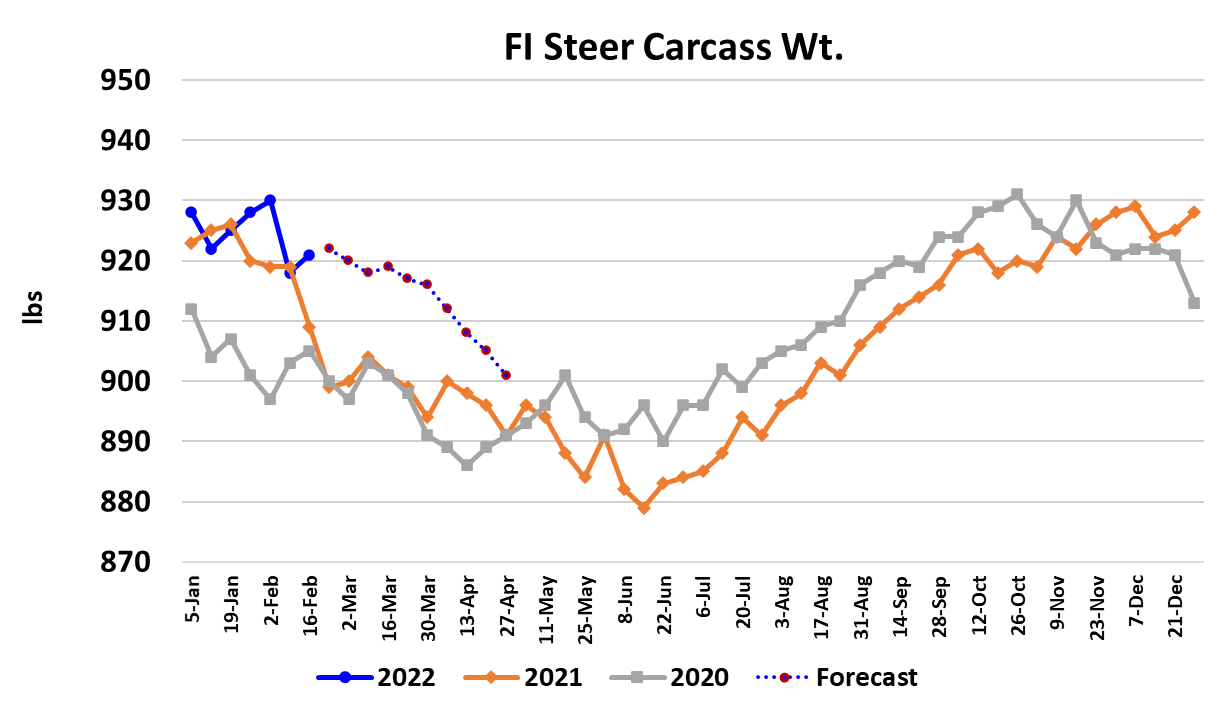

probably not in the best negotiating position right now. Steer carcass

weights were 3 pounds higher this week as they rebounded from last

week’s sharp drop and the DTDS is at very high levels. Steer

weights are now 12 pounds over last year.

I think feedyards need to move cattle and that is evidenced by the

fact that there was some cash trade today at $138, $2 back of the

weekly average. The basis to the futures has made a gigantic shift

in recent days, as Apr LC fell below $136 today. That is telling cattle

feeders that the longer they wait to sell cattle, the less they will get

for them. The futures market has done a huge reset over the last

couple of weeks. Apr has moved lower for eight trading sessions in

a row now. In those eight days, the market has wiped out almost all

of the value that Apr gained since last September. That is the way

that cattle futures trade: they grind slowly higher in an uptrend, but

when the market turns lower, the selling is swift and prices quickly

cascade lower. Needless to say, the speculators, who typically play

the long side of the market, are not happy with the events of the past

two weeks.

Those cattle feeders that had the presence of mind to hedge back in

mid-to-late February when the market was near its highs are

probably breathing a sigh of relief. This week’s fed kill came in at

509k, which was 6k above last week and pretty much right in line

with what the flow model says we should be killing in early March.

We will likely see fed kills hold in the 505-515k range for the next

several weeks. There are more cattle in feedyards right now that at

any point in the past. That alone seems pretty bearish to me. If the

beef market can muster a rally in the next couple of months, it will not

be due to tight supplies, but rather due to seasonal improvement in

beef demand. Lower pricing in the beef complex seems to be

attracting the interest of international buyers as the weekly export

numbers have looked pretty good recently. That helps, but it won’t

be enough to substantially boost the market this spring. We will get

the official export totals for January on Wednesday.

Grain markets have been highly volatile and moving higher since the

invasion of Ukraine and it looks like the world will have to do without

any grain from that region of the world for at least a few months.

That is a big problem because the S. American crop is struggling and

there is a lot of dryness in N. America as well. The cost of feed is

going to be way higher this year than last and that means cattle

feeders will do their best to push feeder cattle prices lower to

compensate. Feeder cattle futures did a huge reset lower this week

also. That won’t encourage cow-calf producers to begin expanding

their herds. Herd expansion plans will likely have to wait until 2023

or beyond. Next week, watch for early cash cattle trade at lower

money. If that happens, it is usually a sign that cattle feeders feel a

sense of urgency to move cattle and could signal a new downtrend in

the cash cattle market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}