Beef Wrap March 11

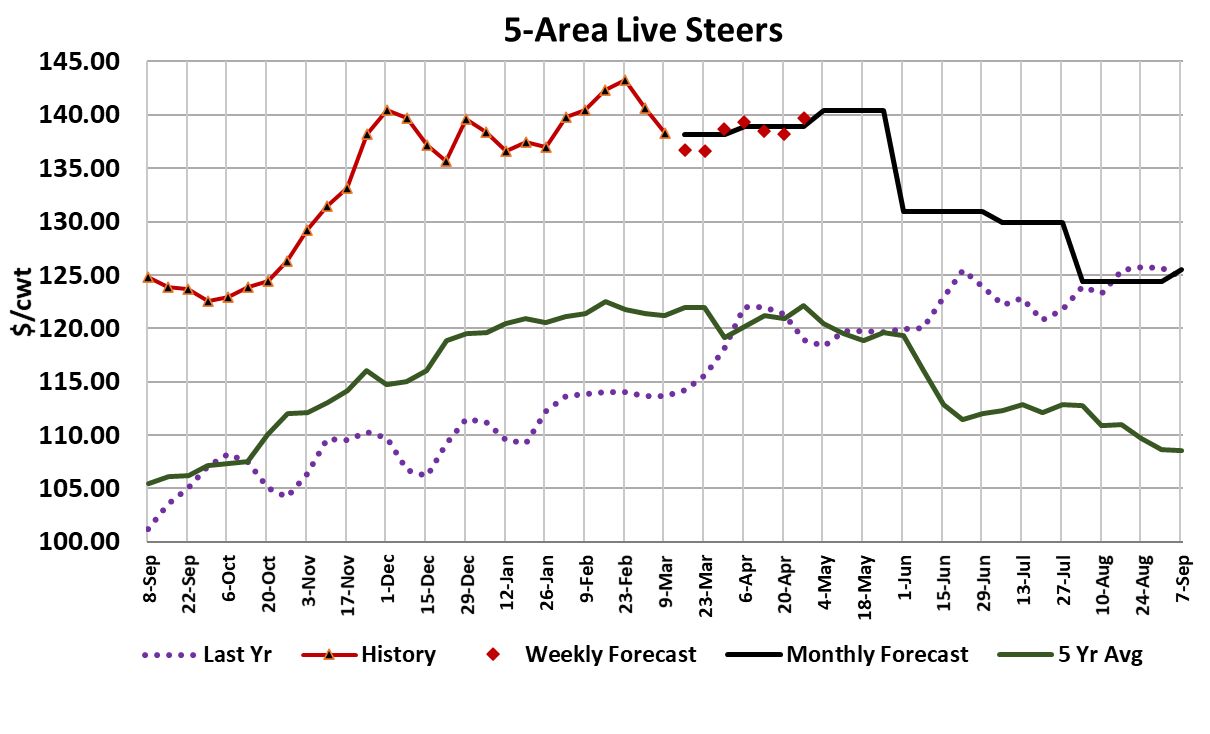

The cash cattle market moved lower again this week with the

bulk of the trade occurring at $138, down a little over $2 from last

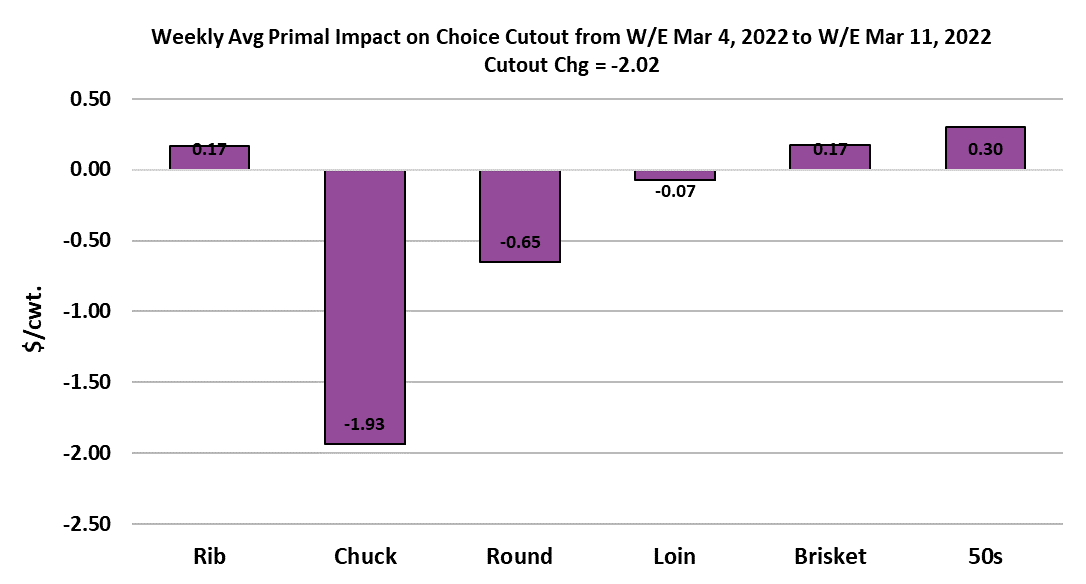

week. The cutouts also continued lower, but the decline slowed

and by the end of the week the cutouts were starting to move

higher. The Choice averaged $253.70, down $2.02, while the

Select averaged $247.29, down $3.20 from the week before.

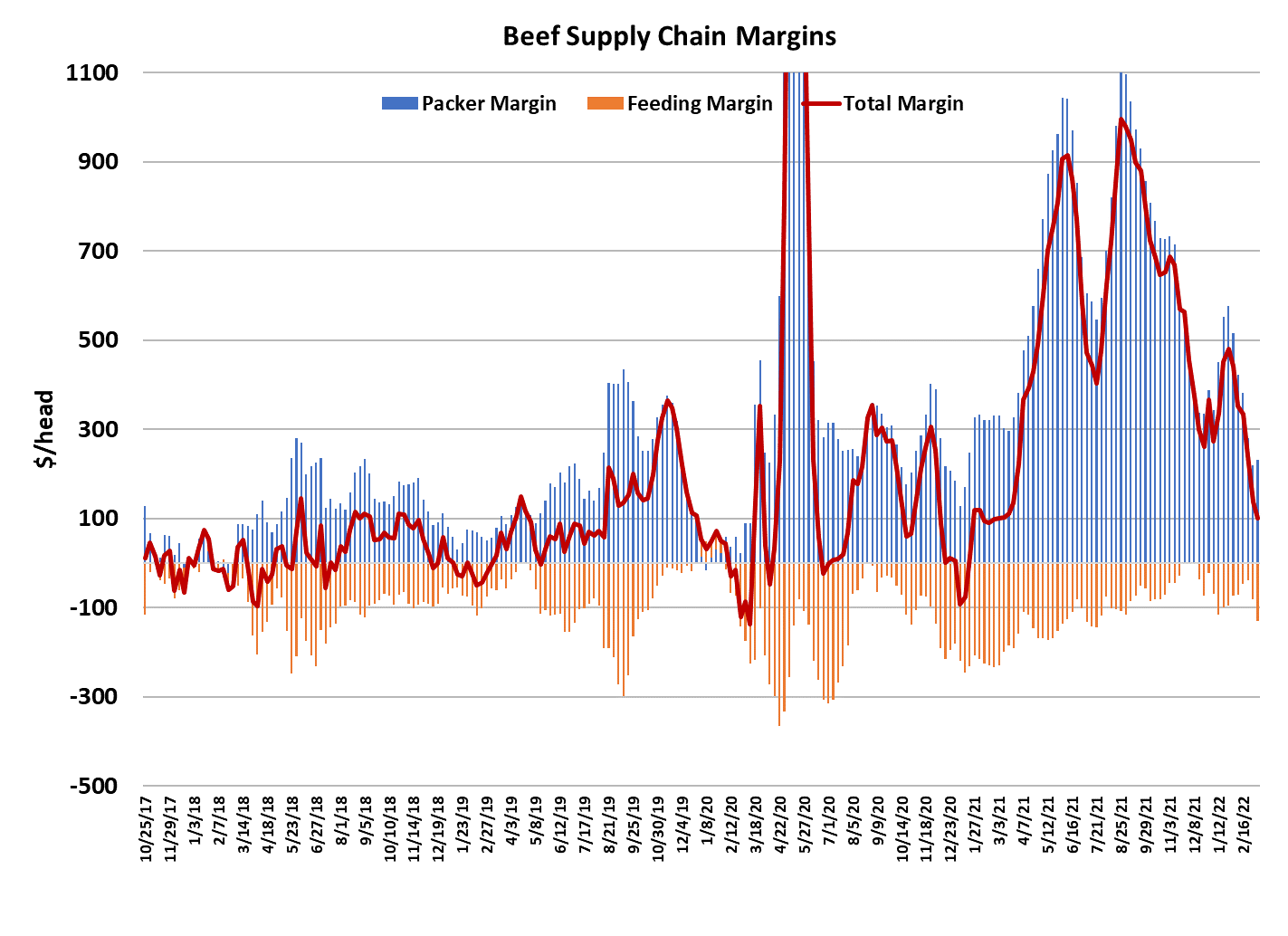

Packer margins averaged $233 per head, up slightly from the

week before. We should see some further improvement in

packer margins over the next few weeks as beef prices work

higher and cash cattle trade steady to lower. We have now

reached the point in the calendar where beef should experience

some seasonal demand strength and that should take prices for

most items higher. The move is likely to be slow and uneven at

first, but by the time April arrives, we could see bigger and more

consistent price increases.

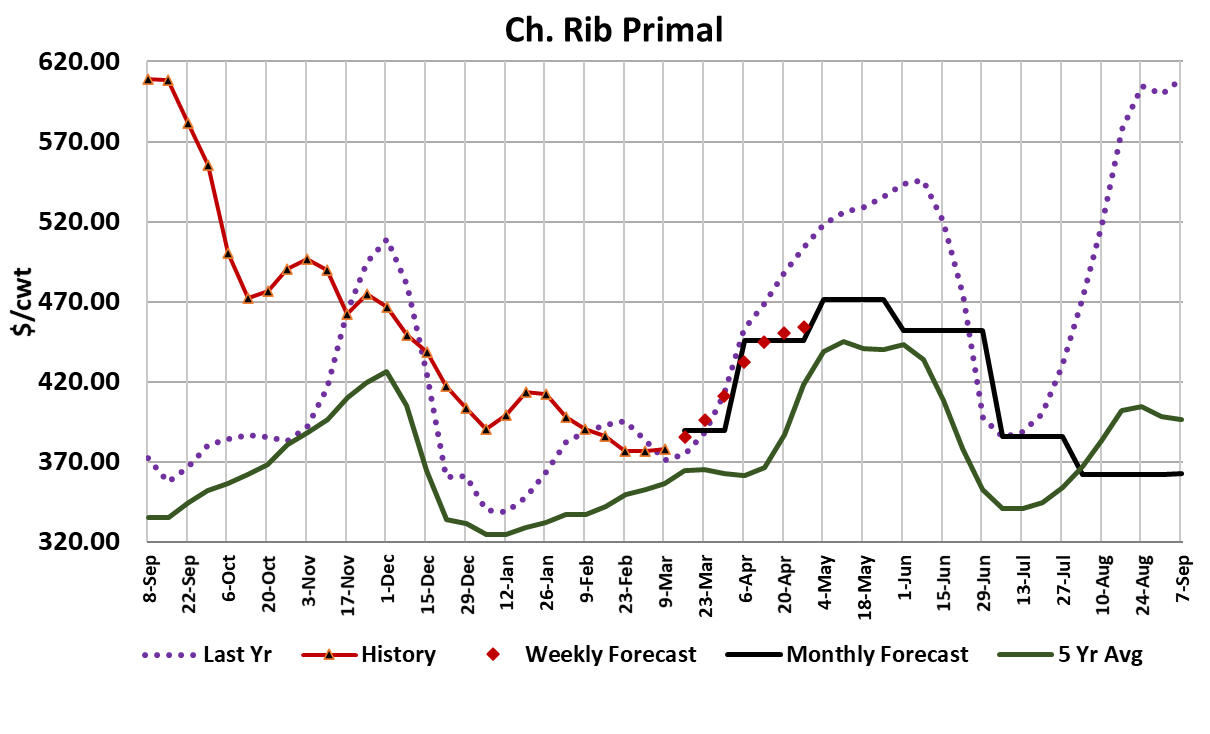

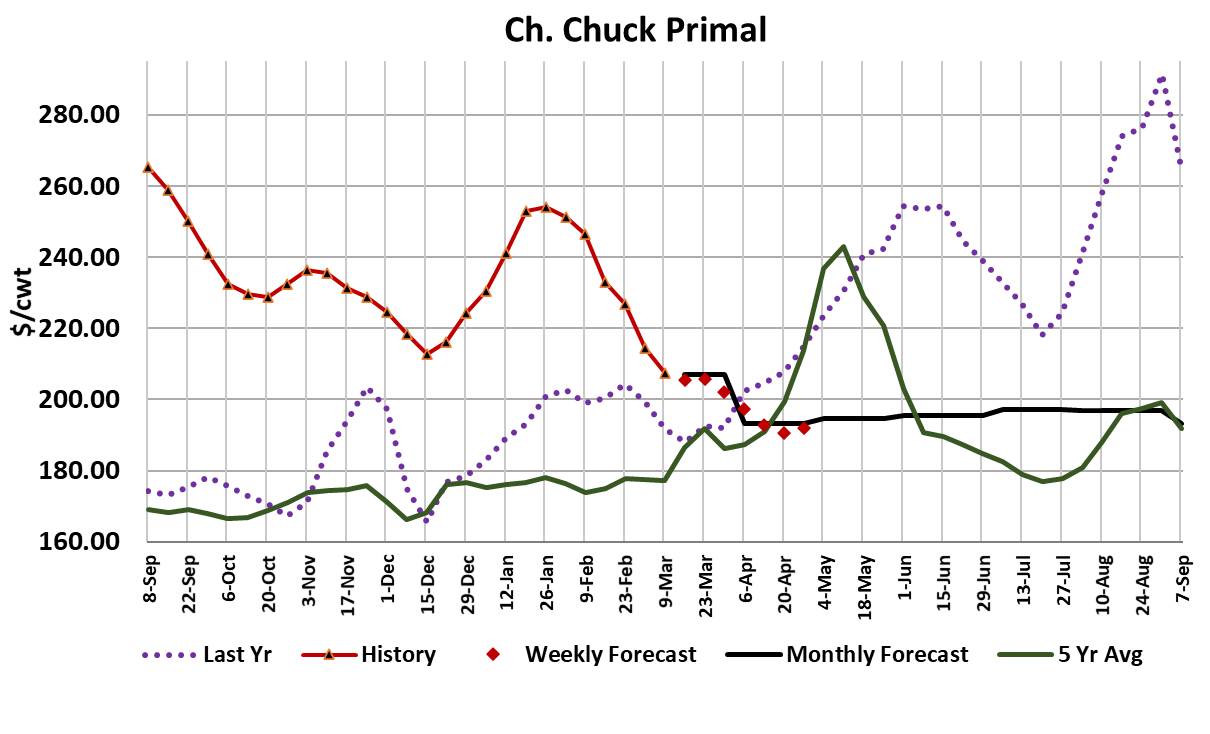

This week, it was the end meats that pulled the cutout lower while

the middle meats were steady to a little higher. The forecast has

a bit more softening in the end meats over the next month or so

before they stabilize through the summer. Very strong pricing for

lean trim should keep a floor under the ends and keep prices

from sliding too low. Fresh 90s averaged $285 this week and so

it is easy to see why a Choice shoulder clod at its current price of

$253 might not have a whole lot of further downside risk.

Ground beef should see improving demand this spring, not only

from consumers trading down, but also from consumers traveling

more and thus making more QSR visits where ground beef is a

staple. Retailers are almost sure to be buying middle cuts at the

moment in order to feature a few weeks down the road when the

weather is warmer.

It will be interesting to see how strong consumer interest is in the

middles this spring when they don’t have the benefit of stimulus

money in their bank accounts. Choice boneless ribeyes are

about $58/cwt below where they were last year at this time. I am

not anticipating middle meat prices to exceed last year’s spring

highs. The combined margin moved lower again this week, but I

expect that by next week it will be showing a bottom and perhaps

may even be a little higher. That should mark the beginning of a

new demand upcycle that should last until mid-May. This week’s

fed kill only registered 496k, down 12k from last week. It appears

that packers are seeing the labor problems in packing plants

ease a bit. They are doing bigger weekday kills and smaller

Saturday kills as a result.

Even so, this week’s fed kill was smaller than what the flow

model projected, so I don’t think it was small because of cattle

tightness, but rather because packers are attempting to help the

cutouts turn higher and stay on that trajectory.That has the

potential to back some cattle up and reduce cattle feeders’

leverage in the next few weeks. Carcass weights are already

very heavy. This week, steer weights were reported 19 pounds

over last year. It doesn’t seem like the kind of environment

where cattle feeders are going to be able to force the market

higher. It would be a small victory for them if they can just hold

the cash market steady for a couple of weeks. US beef supplies

continue to be bolstered by strong imports. USDA just reported

imports for January that were 57% stronger than last year and

that follows on the heels of a Q4 YOY increase of nearly 25%.

Strong demand has a way of attracting the supply to satisfy it.

January exports were up 17% YOY, so that helps to offset a

good portion of the import increase. I see exports remaining

relatively strong in the near-term, mostly because I expect China

to become a more aggressive buyer of US beef in the weeks

ahead. Per capita domestic availability is projected to be up

almost 3% YOY in Q1, but could be down as much as 3% in Q2.

The blended cutout is projected to average 18% stronger than

last year in Q1, but 11% lower in Q2. This reflects the fact that

the huge demand surge seen last year didn’t take hold until late

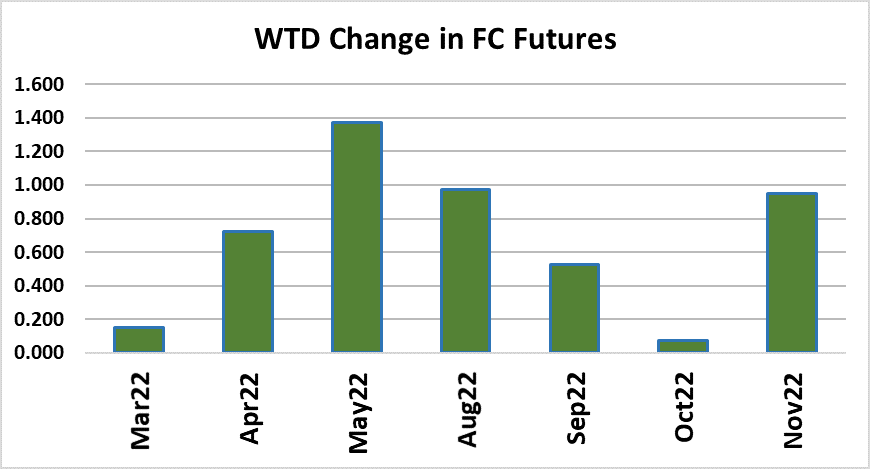

in Q1. Live cattle futures seem to have stabilized for the moment

after nearby Apr shed almost $10/cwt in the last two weeks.

Large speculators seem to be giving up on the bull story for beef

and they are exiting long positions in the front of the curve.

There is still a lot of optimism built into deferred futures and the

mis-pricing chart reflects this. Either traders believe that 2021-

style demand is going to persist forever or else they are betting

on a sharp curtailment of supply from summer onward. I don’t

think either will happen and that leads me to a price forecast well

below what the futures wants to imply. Next week, we will be

watching for continued strength in the cutouts as they try to turn

the corner and get ready to advance into grilling season.

Carcass weights are also important to watch because they are

very elevated and fed kills have been below expectations. If that

continues, it could cause the cattle market to take another leg

down prior to the spring rally.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}