Beef Wrap February 25

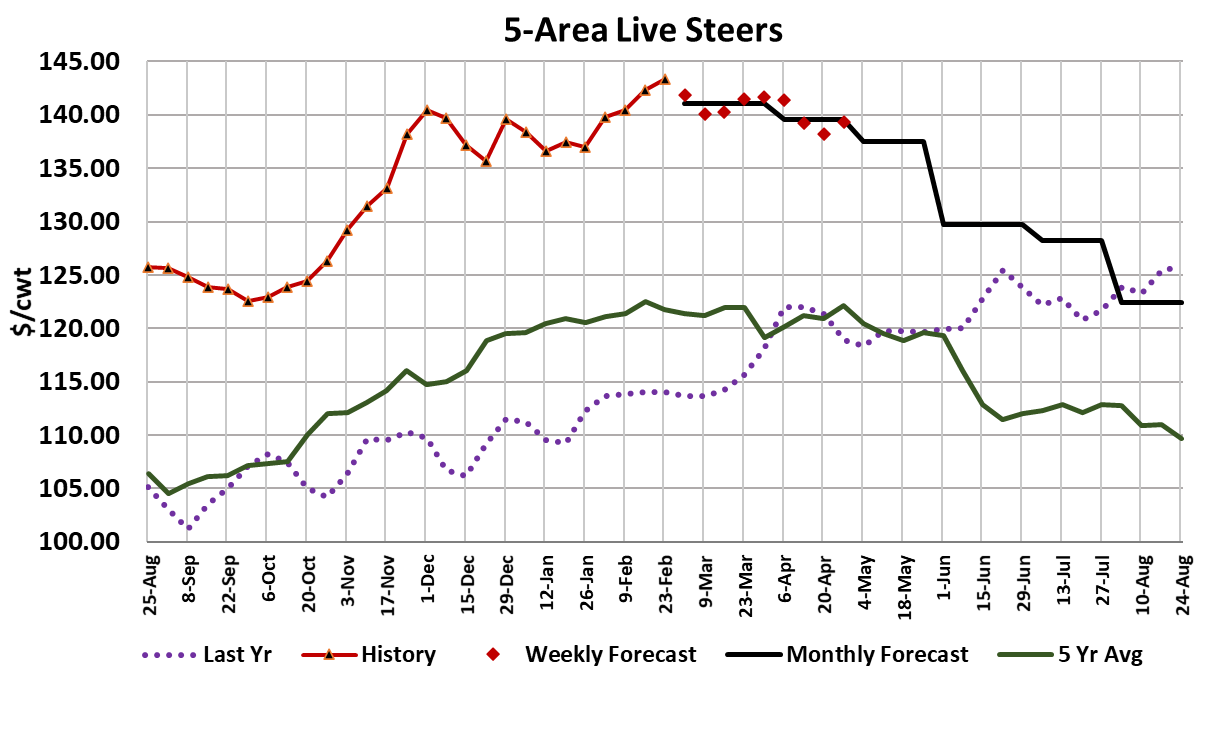

Cash cattle markets averaged about $1 higher this week, but there

was a wide range of prices reported. Early in the week, some

packers stepped up and paid as much as $145 for cash cattle, with

more sold at $144. Then following the news of Russia’s invasion of

Ukraine, the futures market fell hard and that prompted some cattle

feeders to accept $142 for their cattle. In the end, the average was

$143.40 and packers bought fewer animals than the week before.

However, on Tuesday packers will get access to their March formula

cattle, so perhaps it wasn’t a priority for them to buy a lot this week.

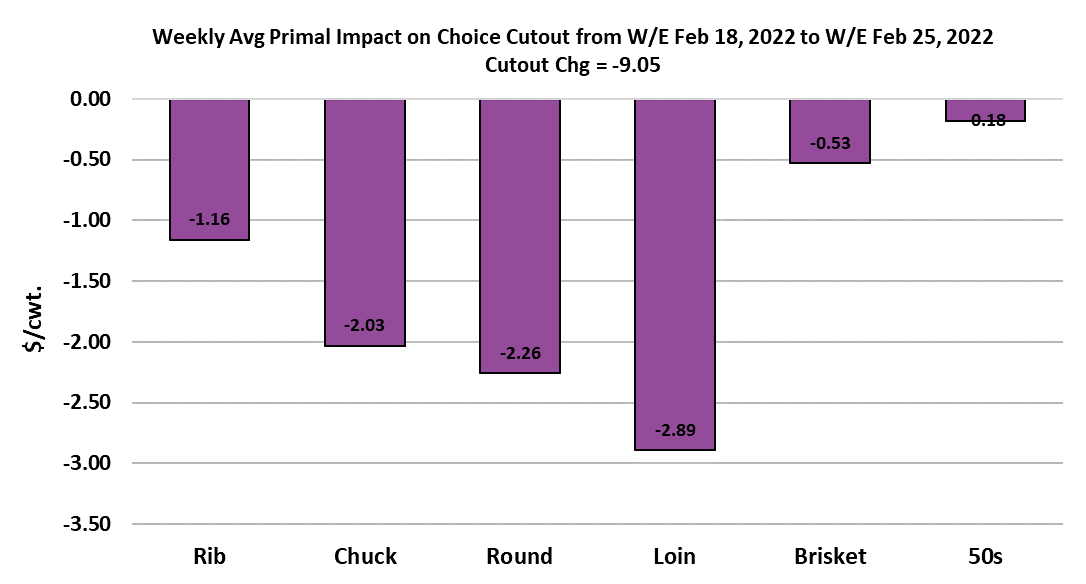

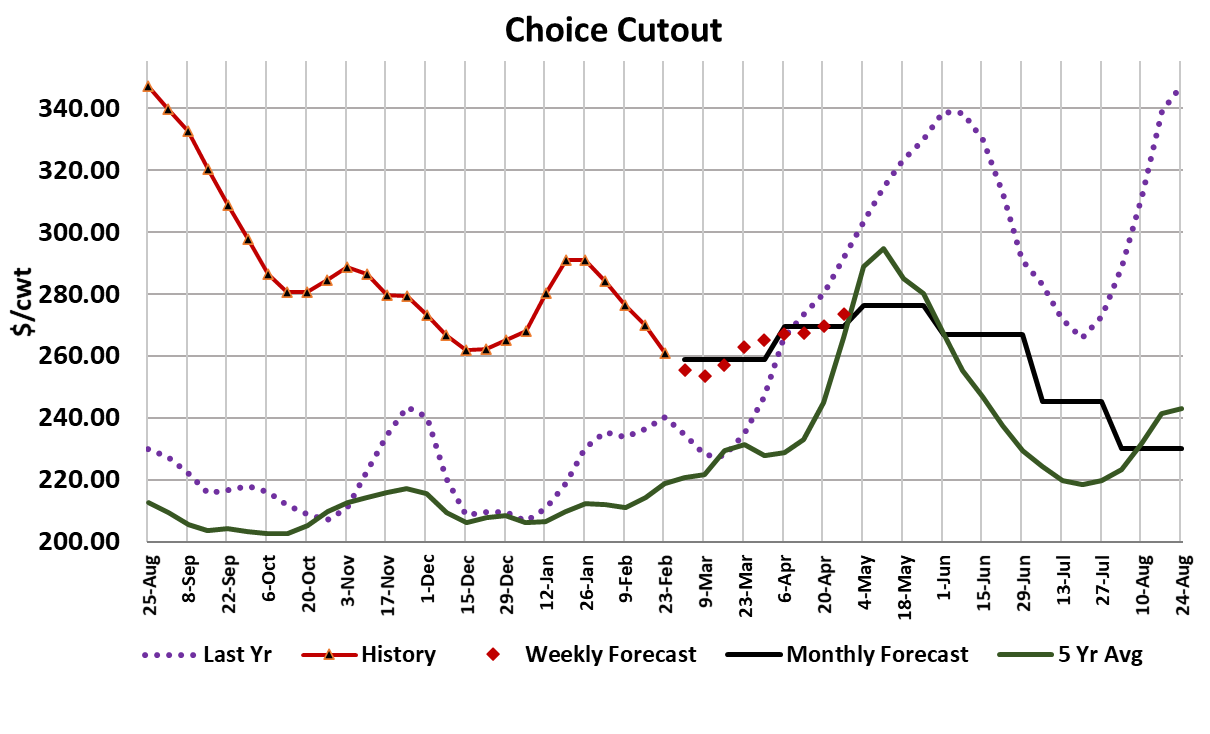

Meanwhile, the beef market just kept sliding lower. The Choice

cutout lost over $9 on a weekly average basis and the Select was

down over $7. Many observers had pegged the $260 level on the

Choice cutout as forecasted bottom for this demand cycle. However,

this afternoon the Choice cutout printed $258.

That is causing some analysts to revise their forecasts lower, myself

included, but I’ve always thought that the risk was to the downside in

this situation. February is an awful month for beef demand and if I’m

right about consumers trading down from the super-high beef prices

that they are seeing in grocery stores, then there could still be some

price erosion before the bottom is in. Next week marks the beginning

of Lent and that won’t help beef demand either. Last week, I wrote a

lot about watching the brisket primal as a proxy for consumers

moving back to a post-pandemic lifestyle that likely means softer beef

demand that what we’ve experienced for the past year. Well, the

Choice brisket primal lost $21 over the course of this week. I don’t

think that bodes well for beef demand going forward. The combined

margin is now below all of the bottoms that it made since the “great

demand bubble of 2021” started early last year. And yet, the

combined margin is still very high in a historical context so there is

plenty of room for it to move lower.

The packer part of that combined margin fell to $270/head this week,

a level that it hasn’t visited in over a year. Further, if my forecasts for

next week’s cutout are close, the next packer margin will fall below

$200/head. At some point here soon, packers are going to

vehemently resist paying more for cash cattle in the face of falling

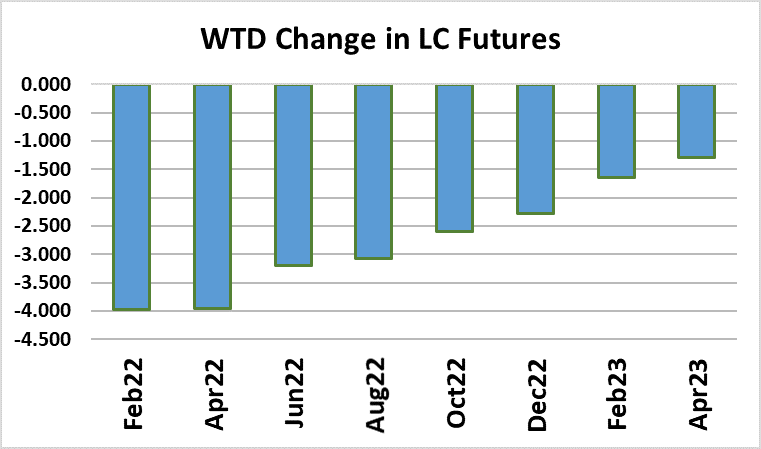

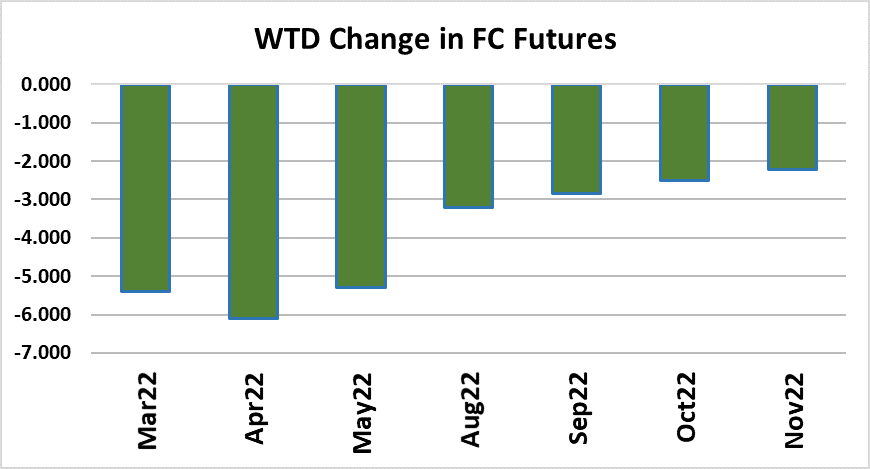

cutouts. The futures market seemed to sense that this week and we

saw a big sell-off in the front end of the futures curve. The

uncertainty created by the situation in Ukraine also created a risk-off

environment that led to selling pressure. The Apr contract finished

the week just below $142 and that is important because now Apr is

below the current cash market. For a long time prior to this week,

Apr was above cash and helping to lead it higher. Now the basis has

shifted and the market is telling cattle feeders that the longer they

hold cattle the less they will be worth.

There is already a feeling that cattle in the feedyards are not very

current, so this shift in the futures could make cattle feeders more

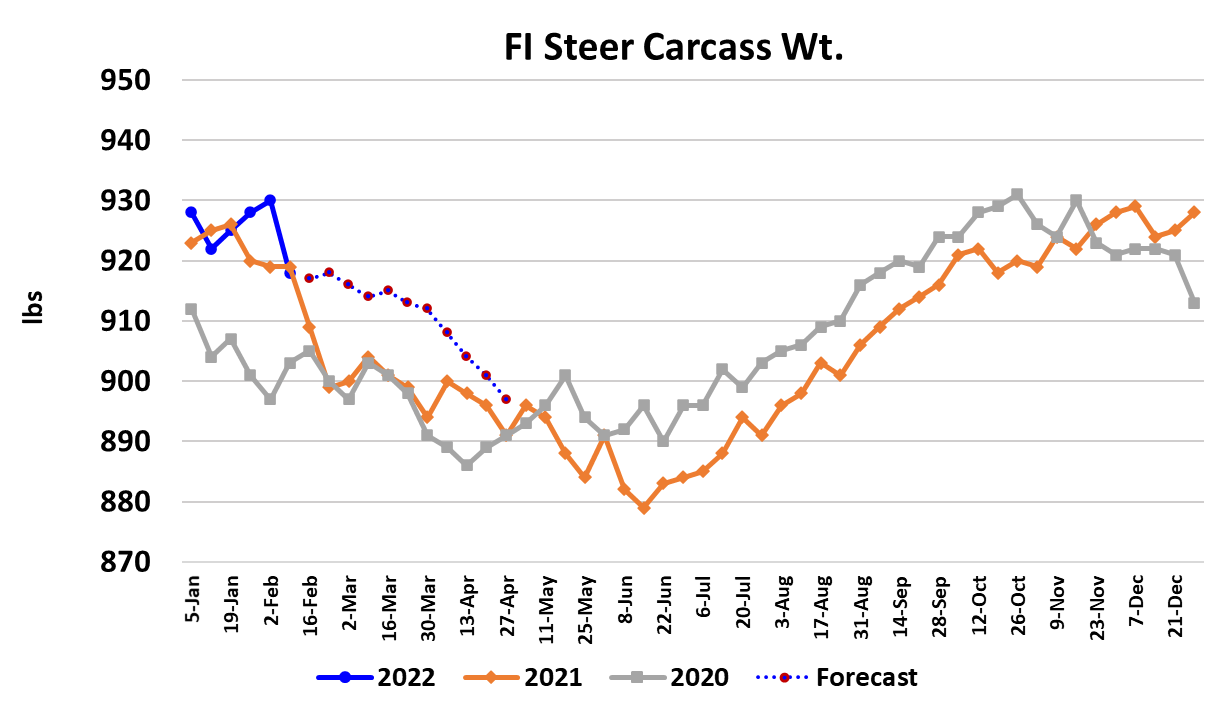

willing sellers as we move forward. Speaking of currentness, this

week’s weight data showed a whopping 12 pound decline in steer

carcass weights. That was a huge surprise, but it really just brings

weights back down to where they are almost even with last year and

last year’s weights were quite heavy. The DTDS weights are still

very elevated. There was a pretty severe cold front that moved

across cattle country this week and that may help keep weights on

the defensive, but I still think that weights will remain above last year

for at least a couple of months. The forecast for next week is warm

and mild across the midsection of the country. This week’s fed

slaughter registered 500k, down 12k from the week before. I have a

similar size kill forecasted for next week. With demand somewhat

precarious, I doubt that packers will get very aggressive with the kill.

As we move into March, the fed kill could expand a bit, perhaps into

the 510-515k per week range. Non-fed slaughter was unchanged

from the week before at 148k. So, the supply side of the market is

fairly well behaved and I wouldn’t expect any big surprises in the next

few weeks. USDA did give us a Cold Storage report this week which

showed beef stocks as of the end of January up 1.4% from last year.

That was the largest January cold storage inventory since 2017, so

end users have more of a buffer in place if spot beef prices should

start to rise. Most of the increase was in cuts, not boneless product,

and that might indicate that users like steak cutters were socking

away product during January in anticipation of the spring market. As

we move into next week, the situation in Ukraine will be top of mind

for both cash and futures market participants.

Prices for a number of commodities including crude oil shot higher

on the news of the invasion and cattle/beef traders will be working to

determine how these changes will affect consumer behavior. It looks

almost certain that gasoline prices will rise as a result of this event,

and they were already very high. That will just put more stress on

consumer budgets and leave less room for consumers pay the

extremely high beef prices that grocery stores are asking. It also

stokes fears of overall inflation in the economy, which won’t be good

for beef demand either. We can expect the stock market to be on

edge also and any big declines there won’t do any favors for beef

demand. There is not much about this new war that is going to be

positive for beef prices. Next week, watch everything—equities,

crude oil, news updates from Ukraine, brisket prices, cutouts and the

weight data. It is all going to have a bearing on the direction of cattle

and beef markets over the next few weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}