Beef Wrap March 3

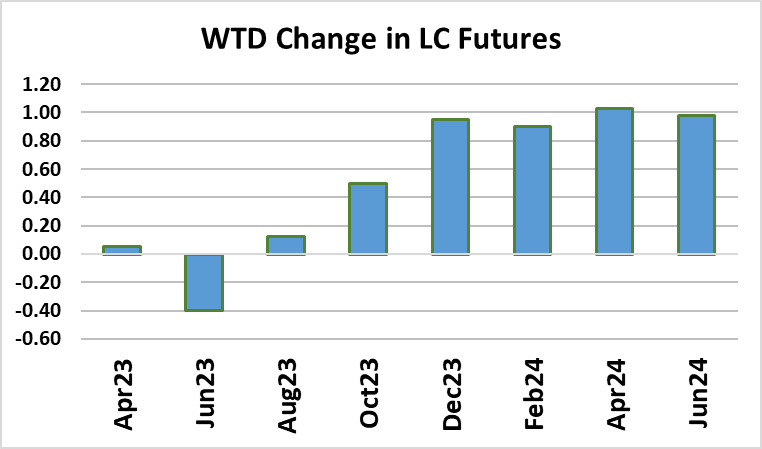

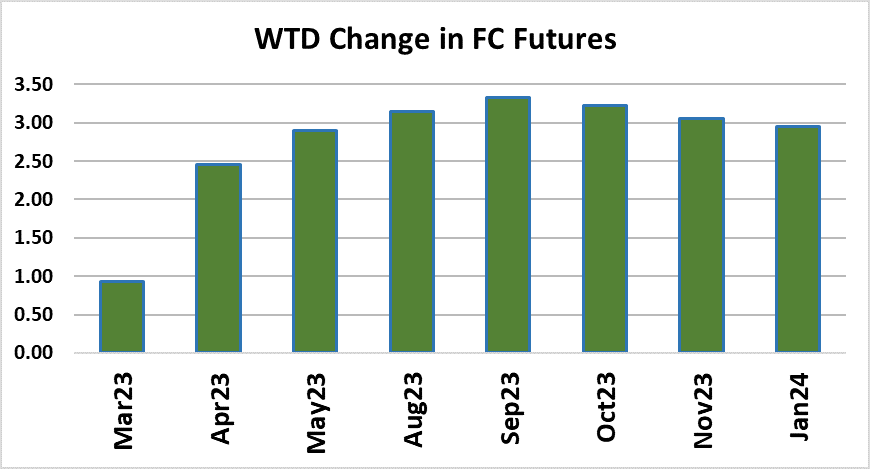

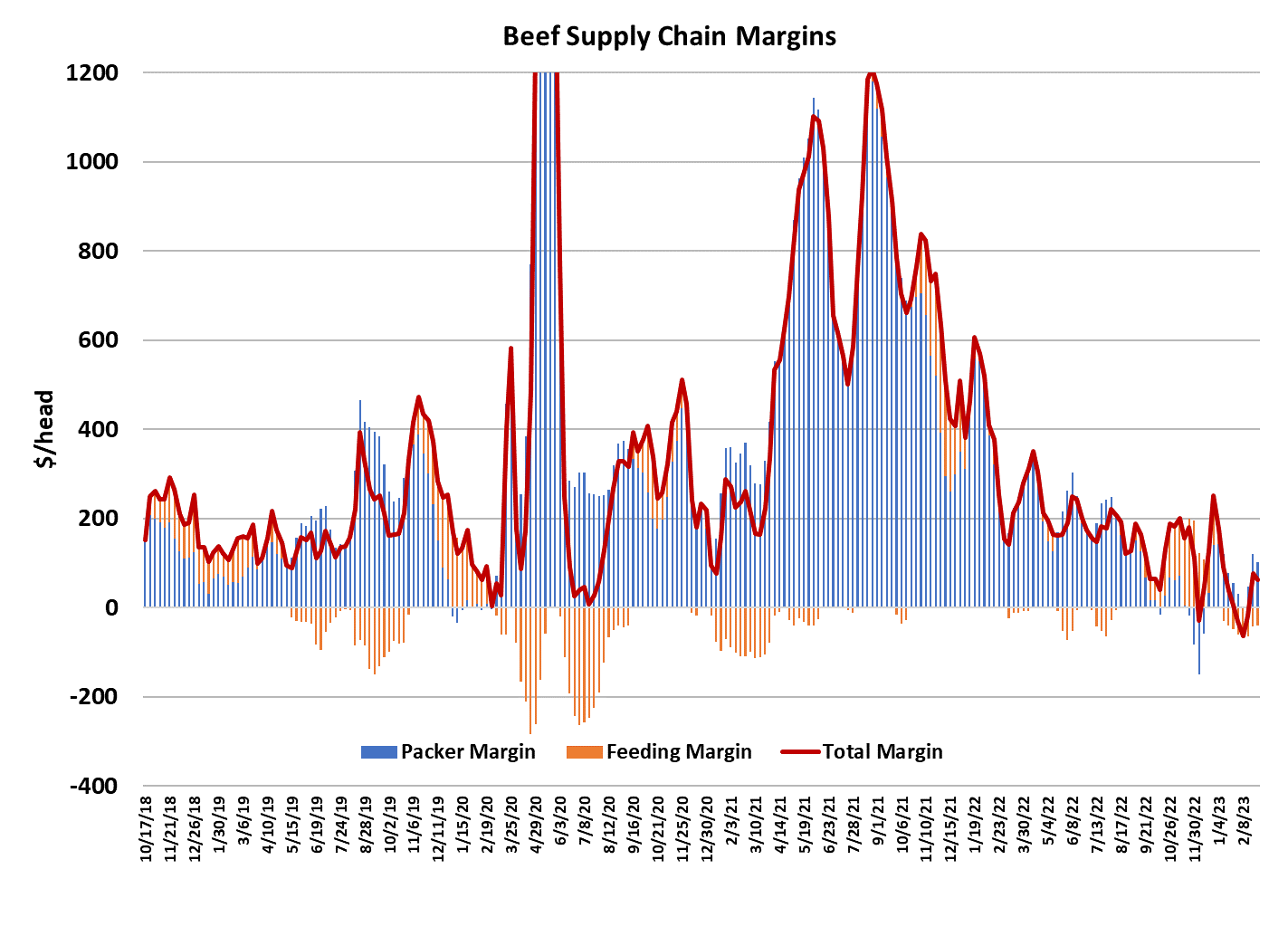

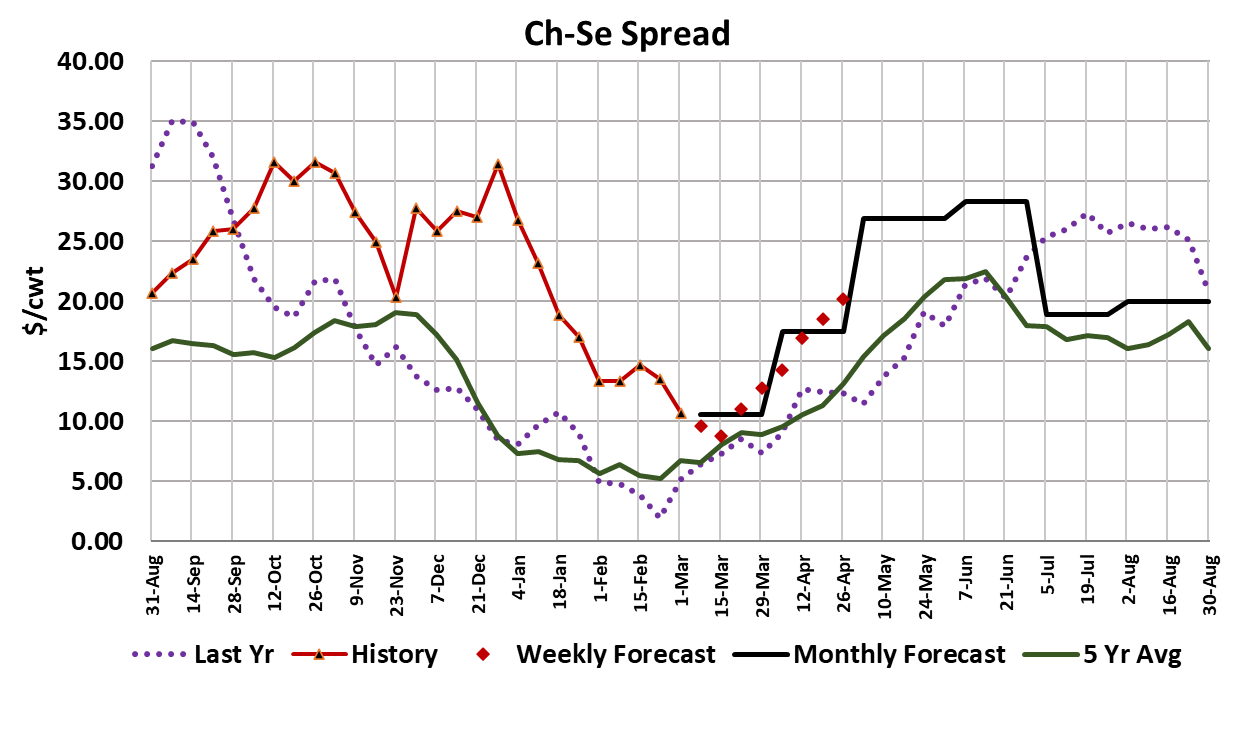

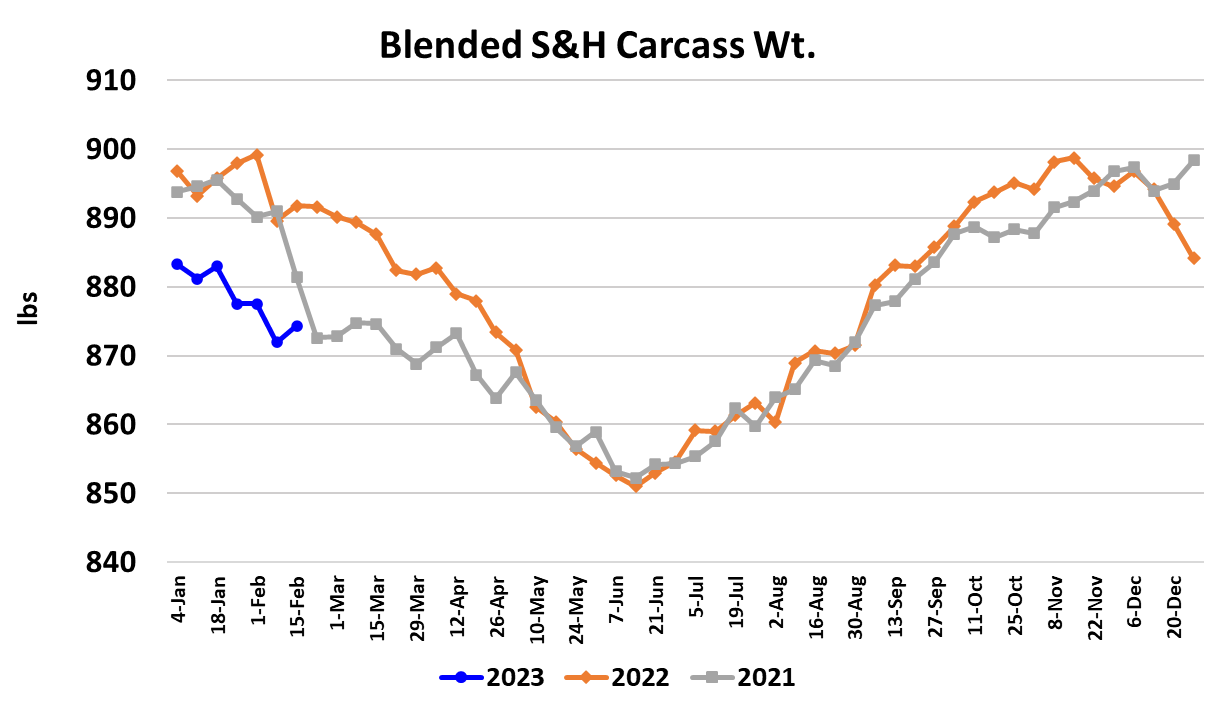

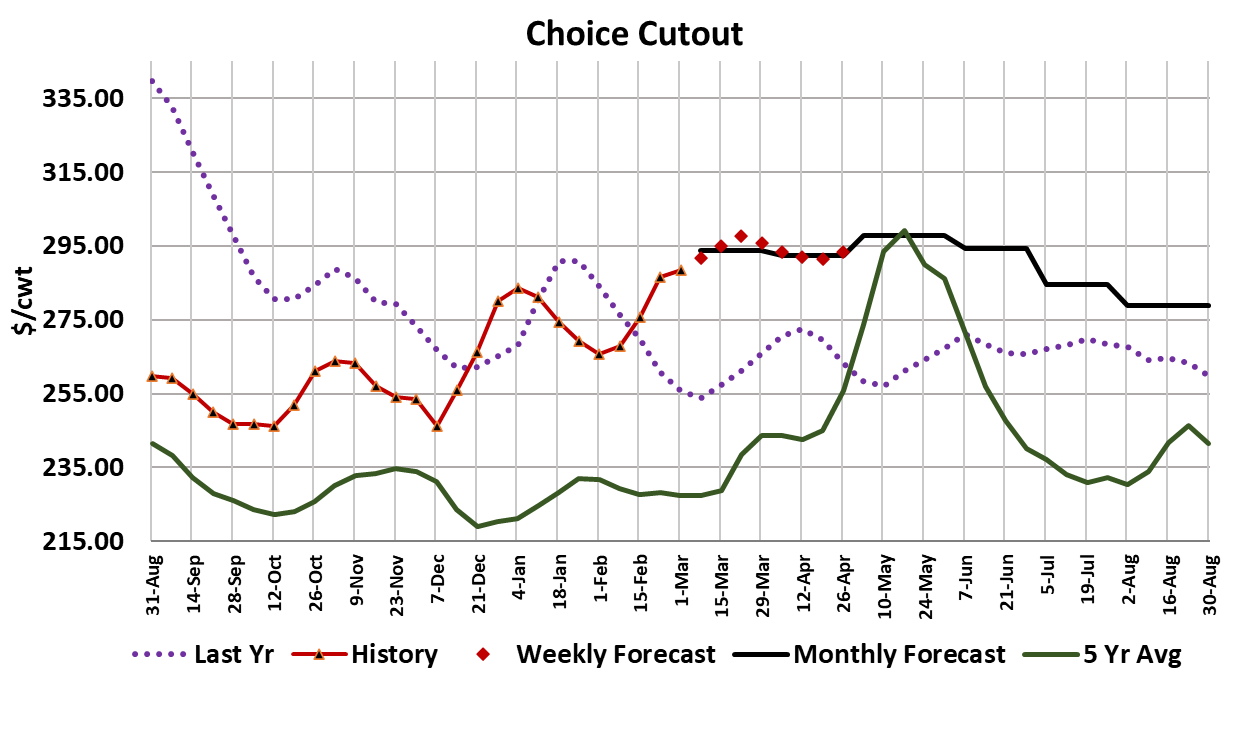

The beef market slowed down this week, with the Choice cutout only gaining $1.93/cwt on a weekly average basis and the Select cutout up $4.78. That caused the Choice-Select spread to narrow down to $10.69/cwt, which is the smallest spread in almost a year. Packers have incentive to keep trying to push the beef higher because they paid more for cash cattle again this week. When all the data is in on Monday, my best guess is that cash will be about $1.50/cwt higher than last week at something close to $165.20/cwt. Packer margins slipped about $20/head this week and now sit just over $100. Prior to the pandemic, $100/head would be considered a very good packer margin in early March. Of course, cattle feeders are eager to take a larger portion of the overall margin each week and I’m sure they will be out with higher asking prices on the cattle early next week. Packers will be telling beef buyers that they have to get more for the beef because they were forced to pay up for cattle. But the rapidly rising wholesale beef prices that we have seen over the past month or so have greatly compressed retail margins and retailers probably won’t tolerate that for long. They will begin raising their everyday retail prices and shift some of their March and April feature activity toward cheaper pork and poultry. The beef ads that they do run will not carry very “hot” pricing. This will help retailers claw back some margin, but it will also likely slow consumer off-take and that will be what puts pressure on packers and feeders to take lower money. It normally takes a few weeks or so for that process to begin to play out and it probably got started back in February, so by the middle of this month we should start to see the wholesale beef market retreat. Of course, March brings warmer weather and improving consumer demand, so that could offset some of the influence of higher retail prices. There are also millions of food stamp recipients that will have a lot less money from the government to buy food starting in March as the “emergency allocation” from the pandemic expires. I think that is going to be a pretty big deal and will likely have the most influence on demand for the lower valued items like ends and grinds. If we look closely, we can see that the combined margin ticked a little lower this week. This may be the start of another downcycle in demand. Since the middle of last year, these demand cycles have had lower highs and lower lows. I’d like to see another week of decline in the combined margin to confirm that the trend has indeed changed, but if it has, it is somewhat scary to think how low it might go on the next down leg. The supply side is likely to remain relatively tight through March and April but cattle availability should improve in May and June. The flow model tells us that fed kills during March might only be in the 480-490k range and the outlook for April is similar. This week’s fed kill is estimated at 483k, up 4k from last week. We are at the point in the cattle cycle where cattle supplies are starting to get quite low and that will be the case for another 2-3 years. Both cattle and beef prices will both need to rise in order to ration that smaller supply. Cattle feeders will need to pay more and more for feeder cattle in order to fill their pens and eventually the feeder cattle price will get high enough that it provides an incentive for cow calf producers to expand their herds. When that happens, supply will get really tight and prices will get really high. I think that herd rebuilding effort is at least a year away and maybe 2 years distant, but buyers need to be prepared for it. The current tightness in beef availability was helped along by some nasty winter weather during February in the Northern feeding region and it looks like there could be more snowfall in that area next week. Snow normally gets the cattle futures excited, so we might see further gains in the futures early next week as the weather event comes into focus. LC futures had a very strong day today, but that just mostly offset declines that occurred earlier in the week. New nearby Apr was just a hair above unchanged this week. Apr is currently trading almost dead on with the cash market, signaling that traders don’t think there is a lot more upside in the near-term cash market. Feeder cattle futures saw better gains than the LC futures this week, largely due to a sharp decline in corn futures that has played out since the middle of February. The 40-cent per bushel drop in the May corn futures during the last week of the year might be a bit overdone and in the last few days the market has been moving a little higher. Planting season is just around the corner and that almost always comes with concerns about getting the crop in the ground and a commiserate rally in the futures, so I think there are greater odds of corn moving higher from here rather than lower. Corn in the cattle feeding regions is still very expensive. USDA quoted cash corn in SW Kansas this week at $7.61/bu, which is definitely better than the $8.10/bu that was printing back in January, but still not cheap. I’ve been waiting for carcass weights to tell us something about how current feedyards are. The FI carcass weight data released this week showed steer weights moving up four pounds to 906, but they are still 15 pounds below last year. Clearly the late-winter weather has had an impact. It often takes carcass weights many weeks to get back to normal after several winter storms. The weekly export data has looked fairly good for beef, but that could change if beef pricing remains elevated. The fundamental forecast has the Choice cutout flattening out in the $290-300/cwt range over the next few weeks, mostly due to fed kills staying small. If I’m right about that, the cash cattle probably don’t have a lot of room to run higher and if the cutout starts to fall precipitously, we could see packers take cattle prices down a few notches. Next week, watch the weather in the Northern Plains, if the storm is worse than advertised, it could boost the cash cattle market again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}