Beef Wrap March 10

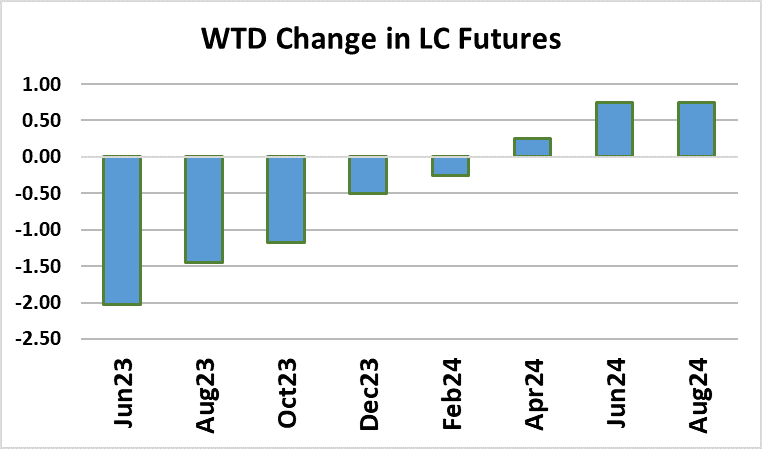

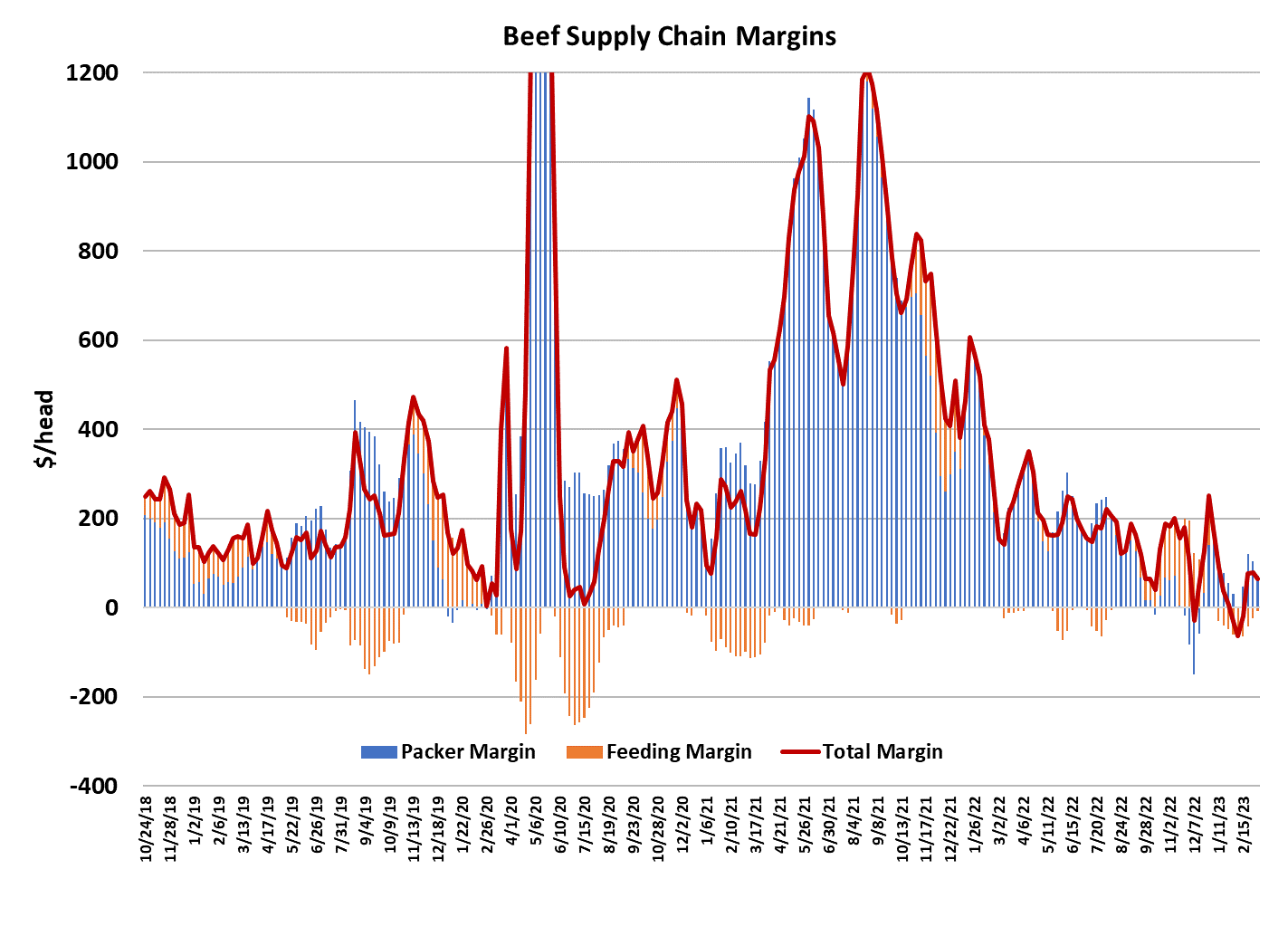

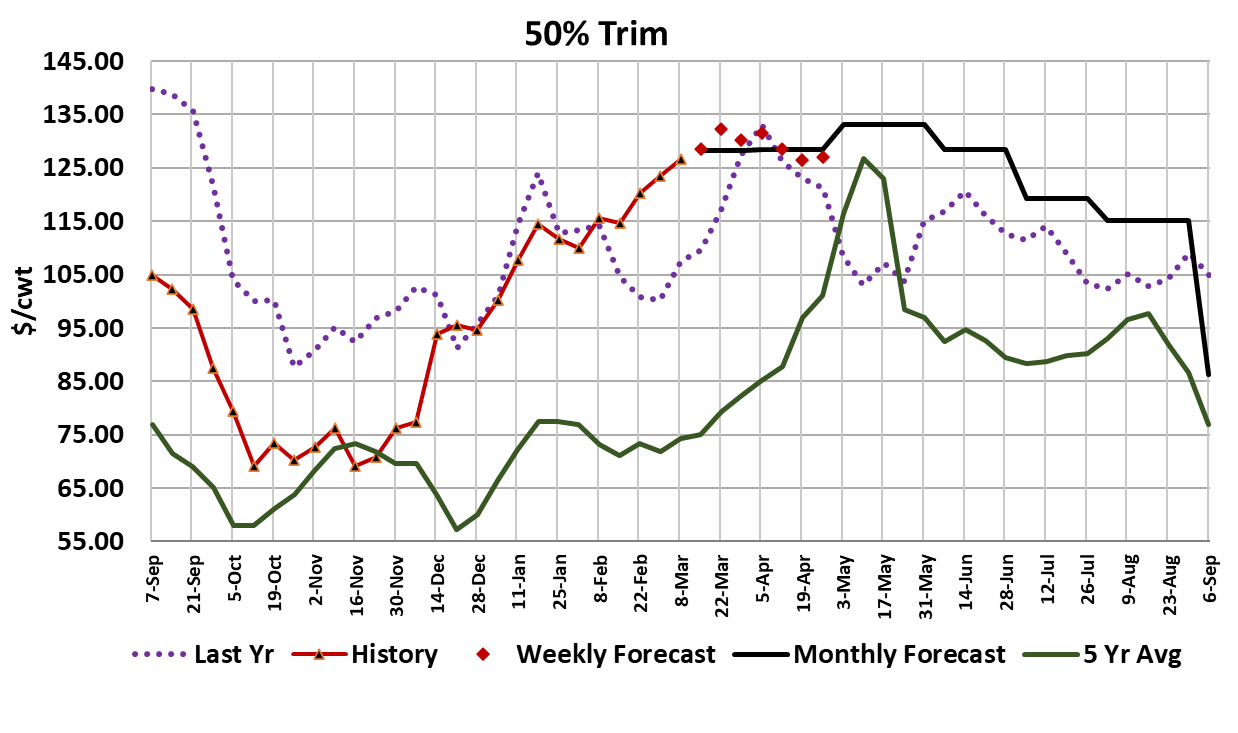

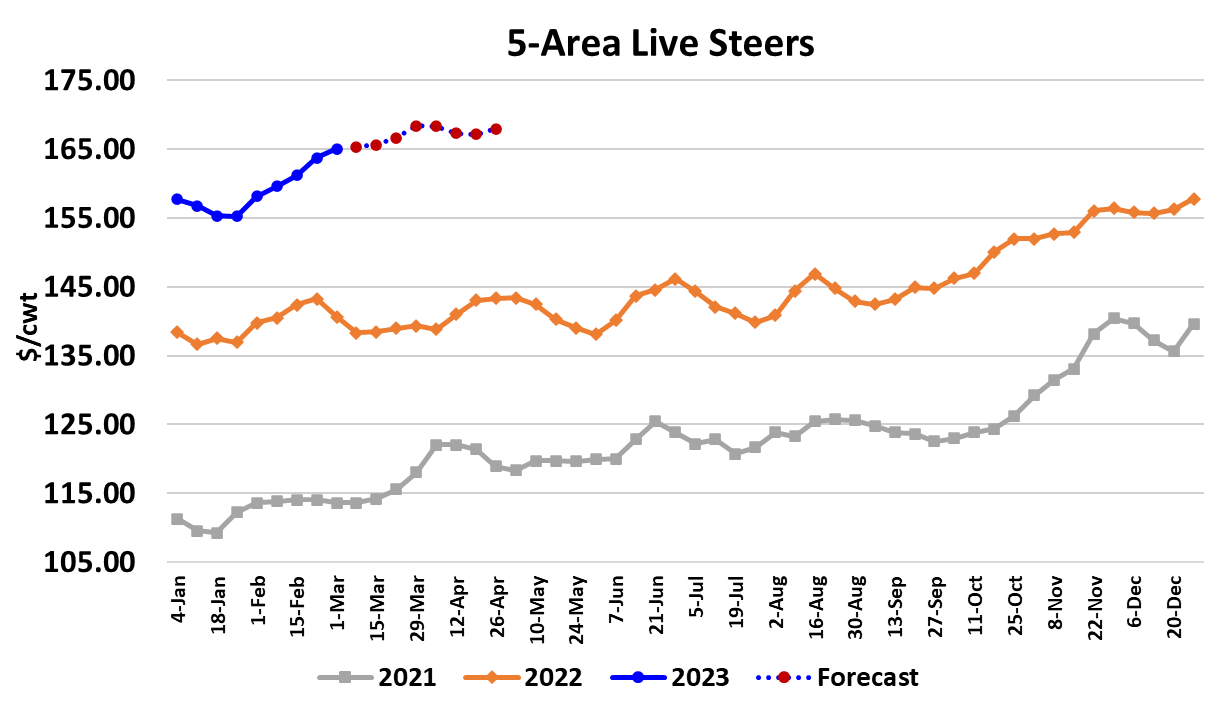

The beef market started to ease lower this week with both the Choice and Select losing about $2/cwt on a weekly average basis. That made it difficult for cattle feeders to advance the cash market so the trade this week was mostly steady at just a little over $165/cwt. Traders have become so used to seeing cash cattle prices advance that when we finally got a week where that didn’t happen, they punished the front end of the futures curve. However, while the LC futures were moving lower, the FC futures were posting impressive gains. FC gave some of the gains back late in the week, but overall we saw the FC gain significantly on the fats. The attached chart shows the premium of the Aug FC contract over the Dec LC contract. The corn market played a role in fostering this sharp increase as the May corn futures have fallen about 60 cents/bushel in the last four weeks. As corn prices fell, cattle feeders were quick to bid up the price of feeder cattle. That is all good and fine as long as corn stays at current levels or retreats, but if corn moves higher after the feeder cattle are purchased, the cattle feeder is likely to face a margin squeeze. However, once a cattle feeder locks in a high breakeven he will fight pretty hard to try and get fed cattle prices high enough to cover it. The cash feeder index finished the week near $189, which implies cash cattle prices will need to be in the mid $170s in August when those cattle finish just to break even. Steer and heifer slaughter this week registered 489k, up only 2k from the week before and still in line with what the flow model has been projecting. I’ve got next week’s fed kill coming in just a little over 500k under the assumption that packers will try to press the kill a little harder because margins were about $67/head in the black this week. If they do push the kill higher, they might end up having to pay more for cattle next week. A lot will depend on how boxed beef values behave next week. Beef prices were generally lower this week, but spring is getting closer with each passing day and that could spur some additional demand that limits how much beef prices can drop in the near term. I’m looking for the cutouts to shed another $3/cwt next week, but then stabilize and start to work higher the following week. If it works out that way, then there probably isn’t much downside risk in cash cattle prices. Carcass weights moved lower again this week, but at a less-than-seasonal rate, which suggests that maybe feedyards are losing a little of the currentness that they enjoyed earlier this year. Both the end cuts and middle meat primals moved lower this week, but neither to a big degree. The fat trim market has been moving higher for several weeks now and is solidly above last year’s level. That shouldn’t be too surprising given that steer and heifer slaughter is running about 5% below last year at present. The combined margin moved a little lower again this week, signaling some softening in demand, but so far the move hasn’t been convincing and so I’d need at least one more data point before I’d call this a demand downcycle. In order to get a strong demand downcycle I think we need to have retailers jack up their retail pricing and thus slow movement through that channel. That takes time to play out and I’m not sure enough time has passed since the sharp run-up in the cutout during February to complete the process. Easter comes on April 9 this year and is more of a pork and poultry holiday than a beef holiday, but I would expect that retailers will greet consumers in the post-Easter market with stronger retail beef prices and fewer beef features. Of course, by that time the spring grilling season will have started and the normal seasonal boost in demand might offset any consumption decline that is due to retailers raising prices. USDA gave us the official trade data for January this week and it showed total beef exports down 15.7% YOY, but to be fair, January 2022 saw some very strong exports, so the bar was set high. The weekly export data has looked a little softer lately and that makes me wonder if perhaps high US beef pricing is starting to temper international interest. Going forward, the most important feature in this market is going to be emergence of grilling season demand. High quality middle meats are likely to be in tight supply given how much the cattle herd has declined and since demand for those items continues to be very strong, we could see very high pricing on Choice middles in April and May. At the other end of the spectrum, I get the feeling that demand for the lower quality, and lower valued cuts is softening somewhat so ground beef might end up being a better bargain for the grill this spring than a ribeye steak. Next week, look for some further small declines in the cutouts and perhaps a cattle market that holds steady or even declines a little. Beyond next week I think the seasonal improvements in demand will become more evident in the market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}