Beef Wrap February 24

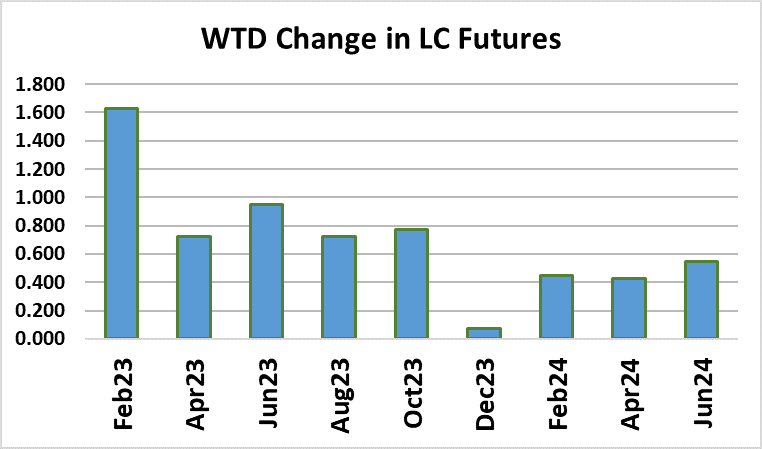

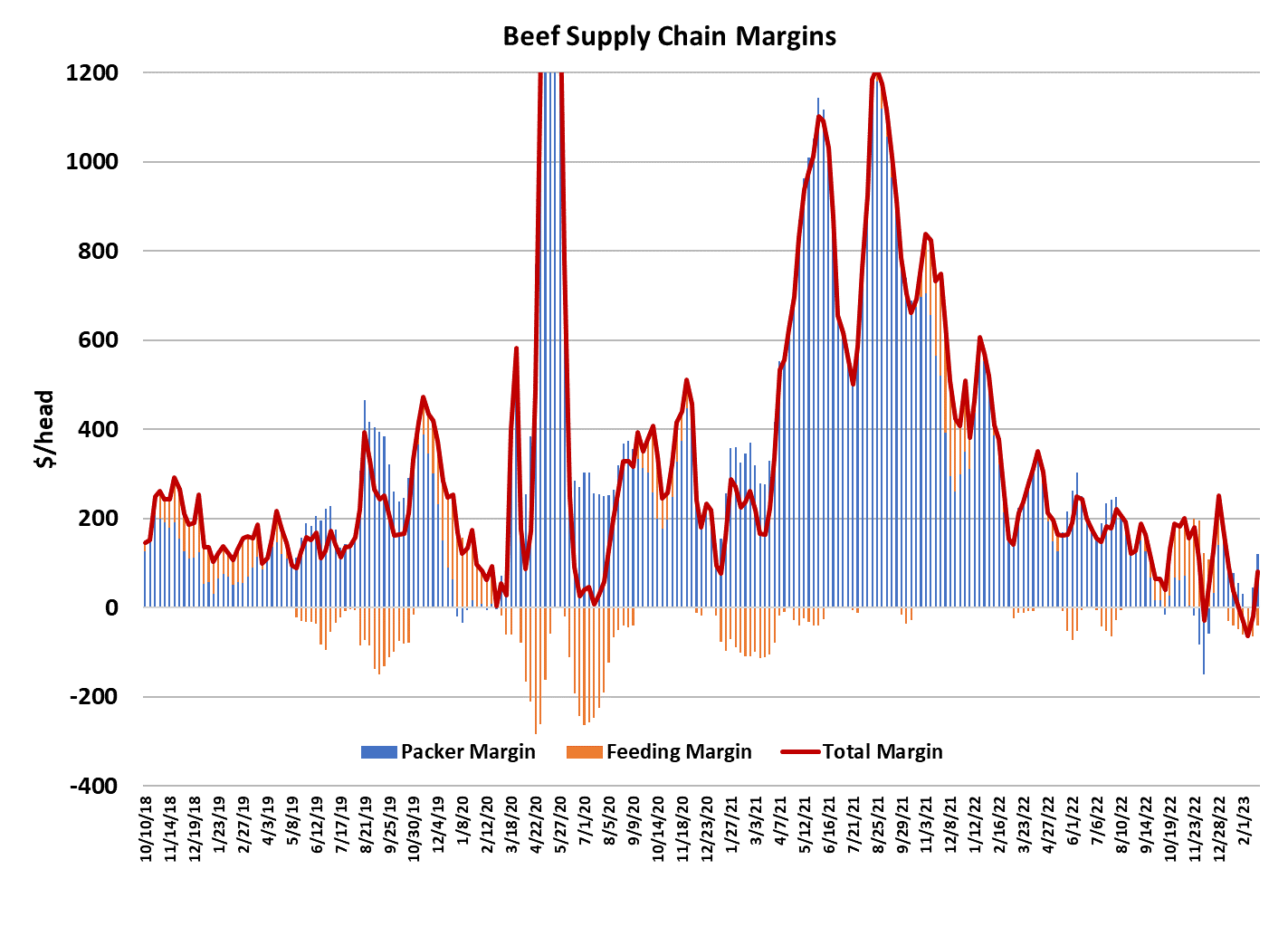

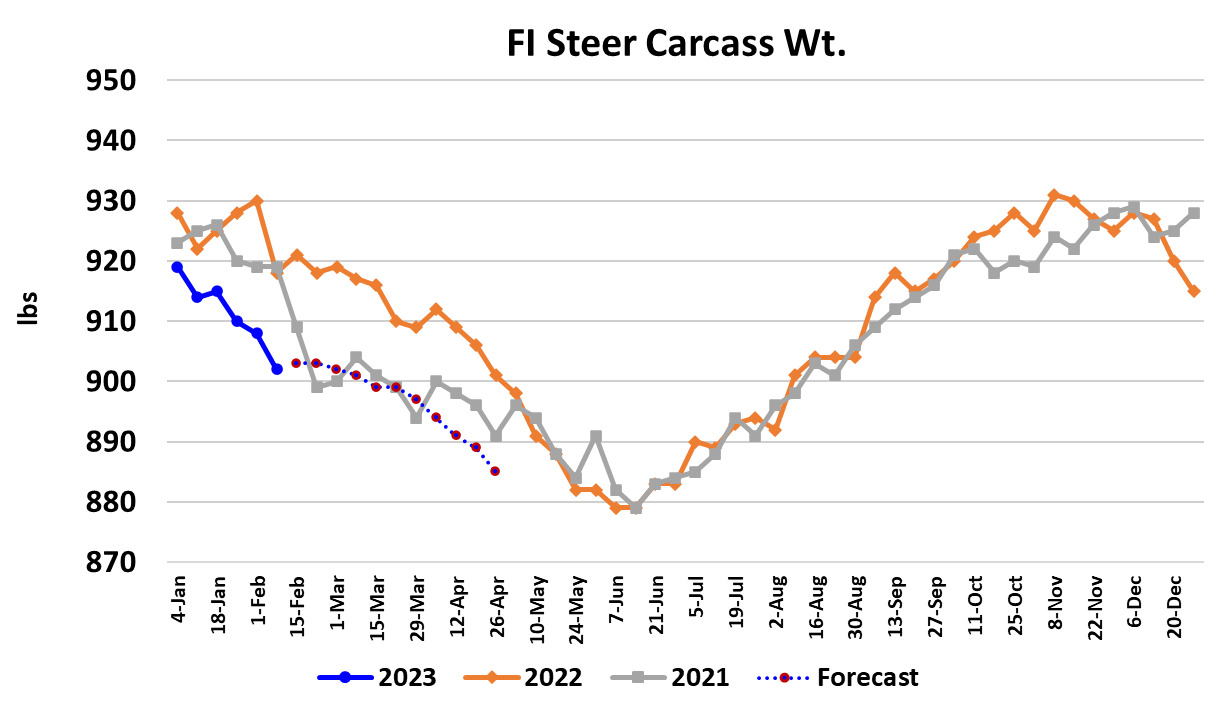

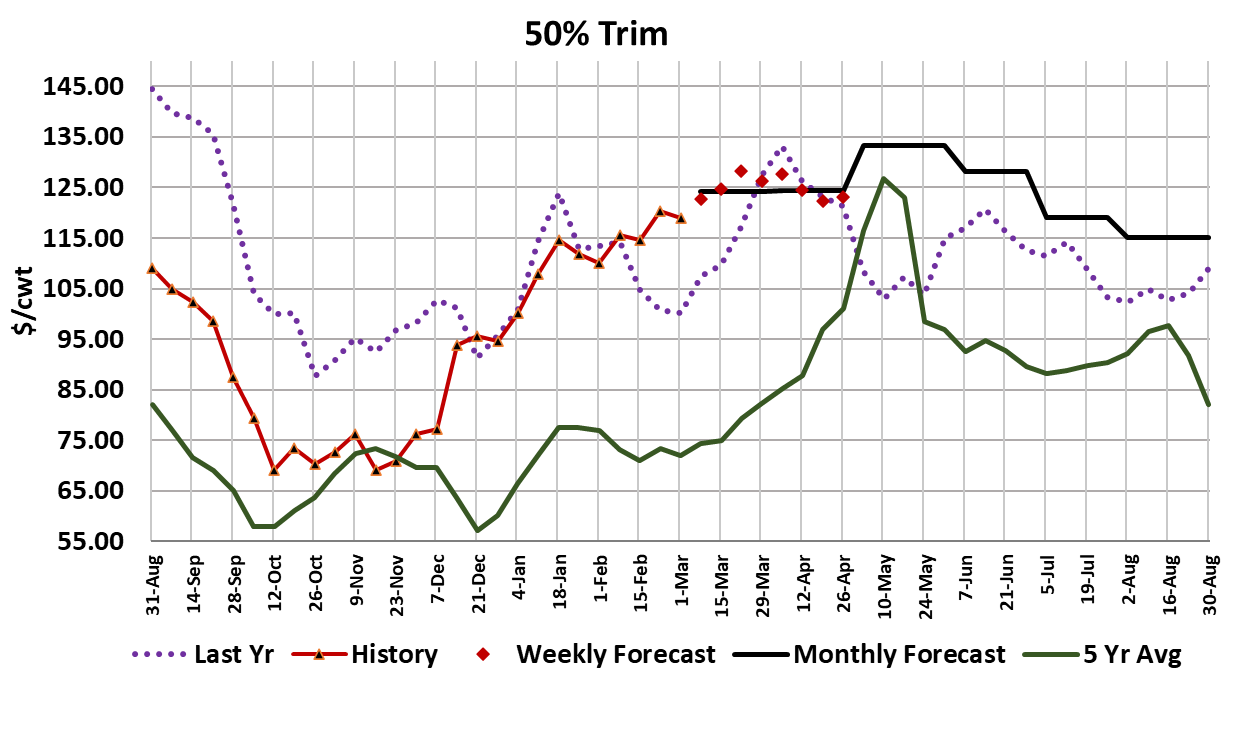

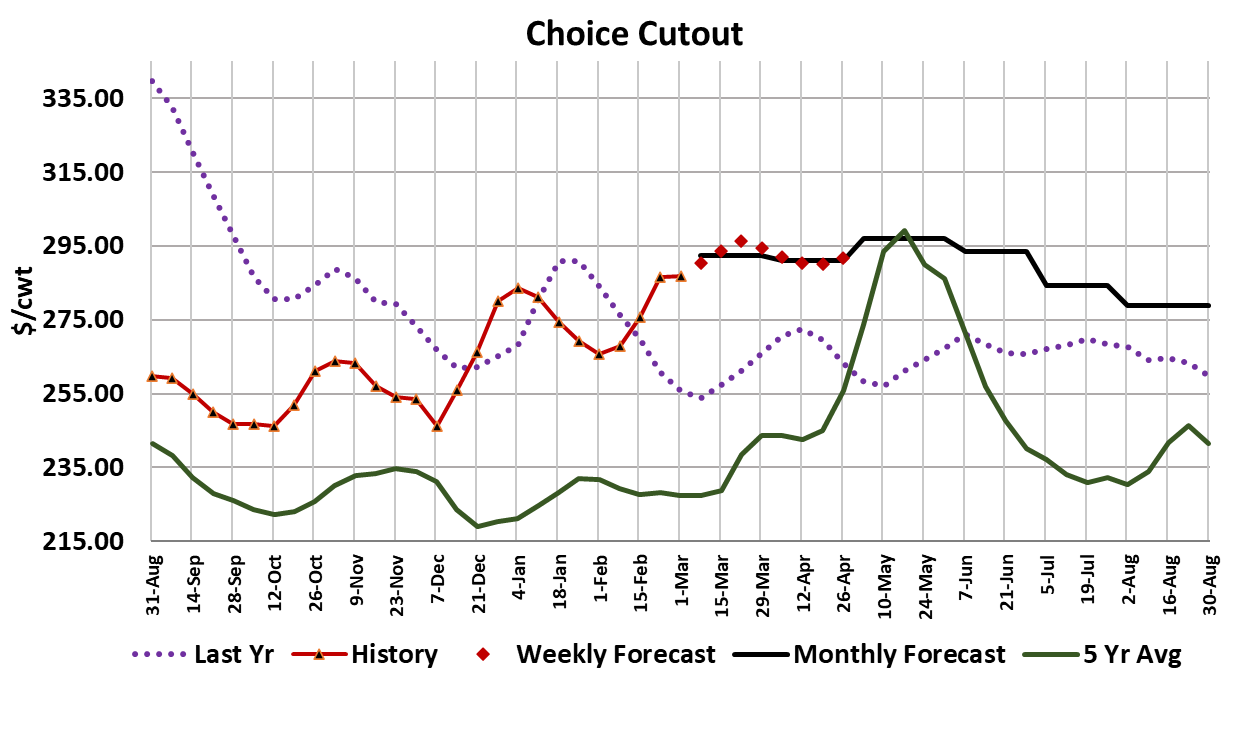

The cash cattle market continued its march higher this week, with the majority of transactions in the South registering $164, up almost $3 from the previous week’s average. The packer’s sales desk was busy raising asking prices on beef and we saw the Choice cutout increase almost $11/cwt and the Select cutout gained a little over $12/cwt. The magnitude of the increase in beef prices suggests that some buyers were caught out of position and thus were forced to pay what the packer was asking. That kind of response is typical, but often very temporary, and by the end of the week it was starting to look like buyer resistance was increasing. Retailers who were forced to pay up in a big way this week will likely get busy raising retail pricing and making a mental note not to lower that pricing again any time soon. Eventually, that will slow movement at the retail counter and thus help contain wholesale price gains. However, I don’t want to blame all of the recent price increases simply on buyers being caught flat-footed, because there is certainly a supply-side contribution as fed kills shrink and carcass weights decline. This week’s fed kill looks like it will total only 472k, down 8k from a week ago. Last year at this time fed kills were running close to 515k. So cattle availability is now much below what packers were accustomed to. That tight cattle availability is likely to persist all of the way through March and April too, so it is hard to see how cattle and beef prices decline much in the next couple of months. At the same time, some late winter weather has muddied feedyards and caused cattle to perform well below normal. Blended steer and heifer carcass weights are 18 pounds below last year and that spread has the potential to widen in the weeks to come. With animal numbers down and carcass weights declining, we now have a situation where beef production is running 7-8% below last year at this time. That is very price supportive and will likely remain that way for most of the spring. Meanwhile export demand remains healthy and may get even better as China turns more towards beef from the US after banning beef from Brazil this week due to a case of BSE in that country. The ban is likely only going to last for a few months at most, but it comes at a time when US supplies are already quite tight. This week’s surge in beef prices helped push packer margins up to $120/head, which is the best since early January. I wouldn’t expect those juicy margins to last very long however, as cattle feeders will be back next week looking for another couple dollars more in the cash cattle market. The attached chart indicates that this week’s cutout gains were distributed fairly evenly throughout the carcass, which makes me think that the supply tightness was the dominant factor. The poor feeding conditions and lighter carcass weights has been very supportive to the 50s market, with the fresh product being quoted near $122/cwt at the end of the week. Feb LC futures will expire on Tuesday and are already pointing to a $165-166 cash market next week. Since early Feb, the cash cattle market has gained over $10/cwt, once again demonstrating that the best gains in the cattle market seem to come when the nearby is in the delivery period. Apr has reluctantly followed Feb higher, but is in danger of actually being discount to the Feb when it expires in a couple of days. Thus, I’d look for the futures market to cool down a bit in March and there is a good chance that Apr will remain discount to cash throughout much of March. However, when the Apr delivery period arrives traders should be prepared for another run higher. Demand should be much better in April than February and the supply of beef won’t be all that much larger. USDA reported feedyard placements during January down 3.6% on Friday, which was a little smaller than what analysts were looking for. One has to think that we are going to see a steady string of YOY placement declines in the months to come. Next week, watch the cutouts for signs that buyer resistance is rising, but don’t expect much in the way of lower prices. Don’t neglect the weather watch either, because that has proved to be a rather potent factor here in late winter.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}