Beef Wrap March 25

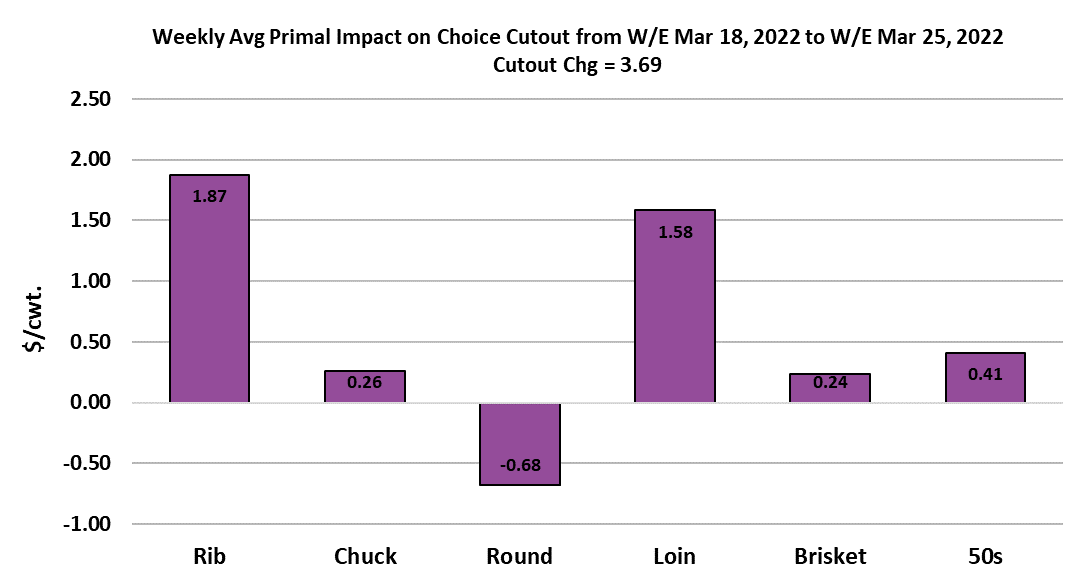

The beef cutouts continued to work higher this week, although

probably at a slower pace than most were expecting. The Choice

cutout added $3.69 while the Select was up $2.40. Cash cattle

traded mostly steady, averaging $138.96, about $0.50 above last

week’s average. Packers reloaded their cattle inventory this week,

buying the largest number of negotiated cattle in almost six weeks.

They will get access to their April formula cattle next week, so that,

combined with the big trade this week, should keep them from

needing to be too aggressive next week. They will also get some

help from today’s Cattle on Feed report, which showed February

placements up 9.3% YOY when the trade was looking for something

closer to a 6% increase. That should pressure the futures lower on

Monday and should set a bearish tone that will allow packers to

avoid paying up for cattle once again. In addition to the large

placement number, today’s report showed overall feedyard

inventories up 1.4% from last year and very close to all-time highs

Feedyards are brimming with cattle and those cattle are excessively

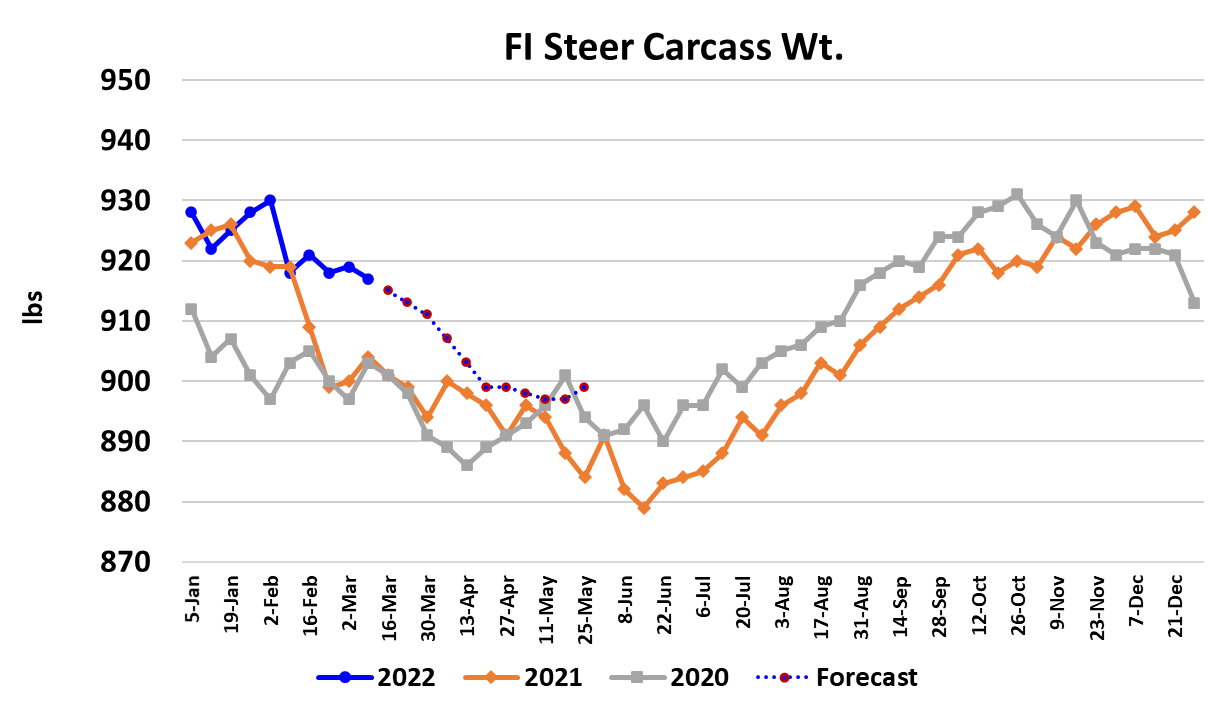

heavy. USDA reported steer weights a little lower this week, but they

are still 14 pounds heavier than last year and declining very slowly

now. Cattle feeders need to keep the animals moving out of the

feedyard and that will limit their ability to advance cash prices. This

week’s fed kill was stronger than in previous weeks, clocking in at

511k, with packers scheduling a bigger Saturday kill than expected.

That additional production may test the cutouts’ ability to remain on

an upward trajectory. So far, the upcycle in beef demand has been a

bit subdued and that might imply that consumer demand is not really

as strong as it appears. We are seeing warmer weather across the

Southern states and that should bring out some grilling demand, but

price levels at retail are very high and consumers are dealing with

high prices in a number of other sectors of the economy.

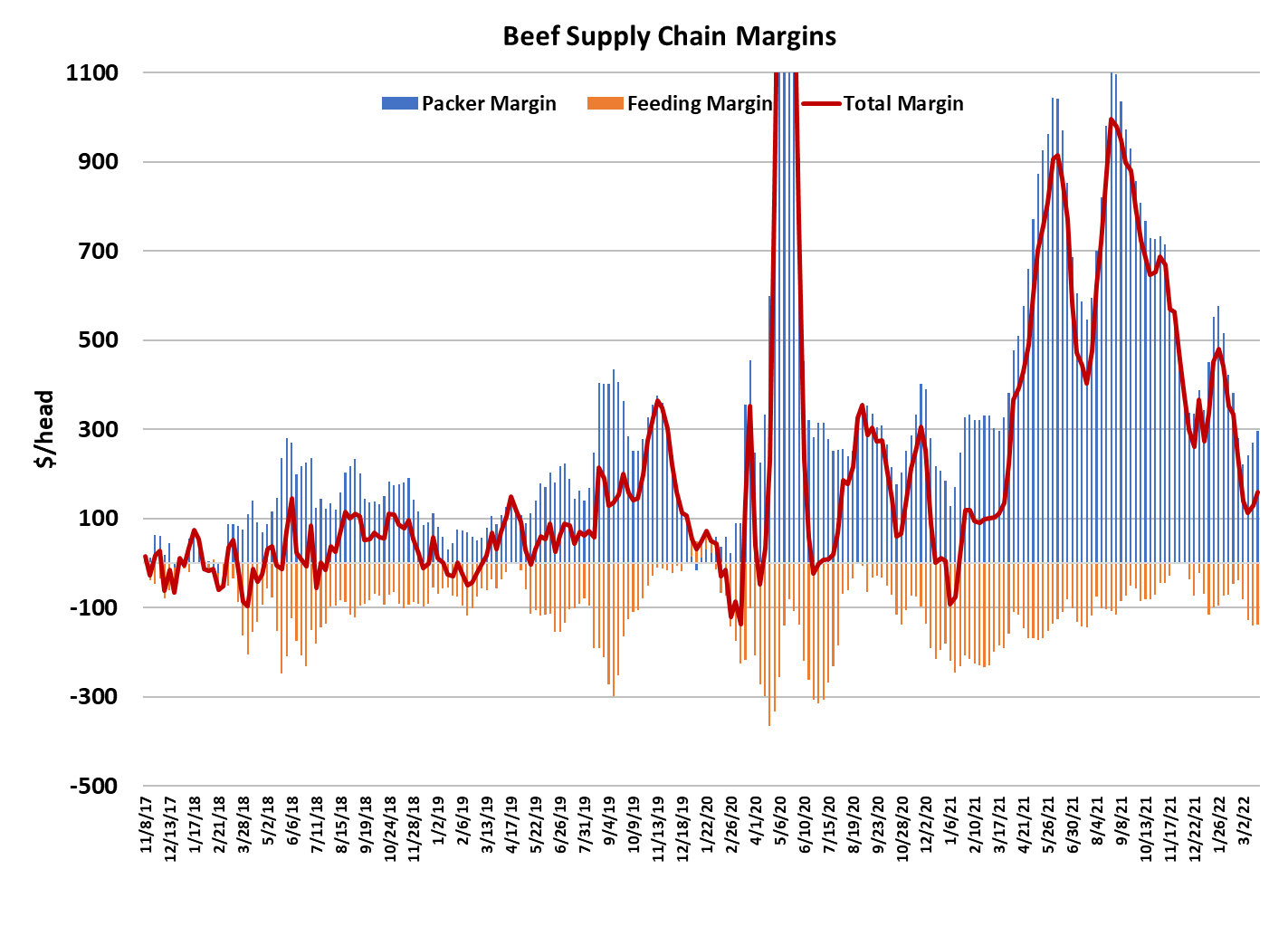

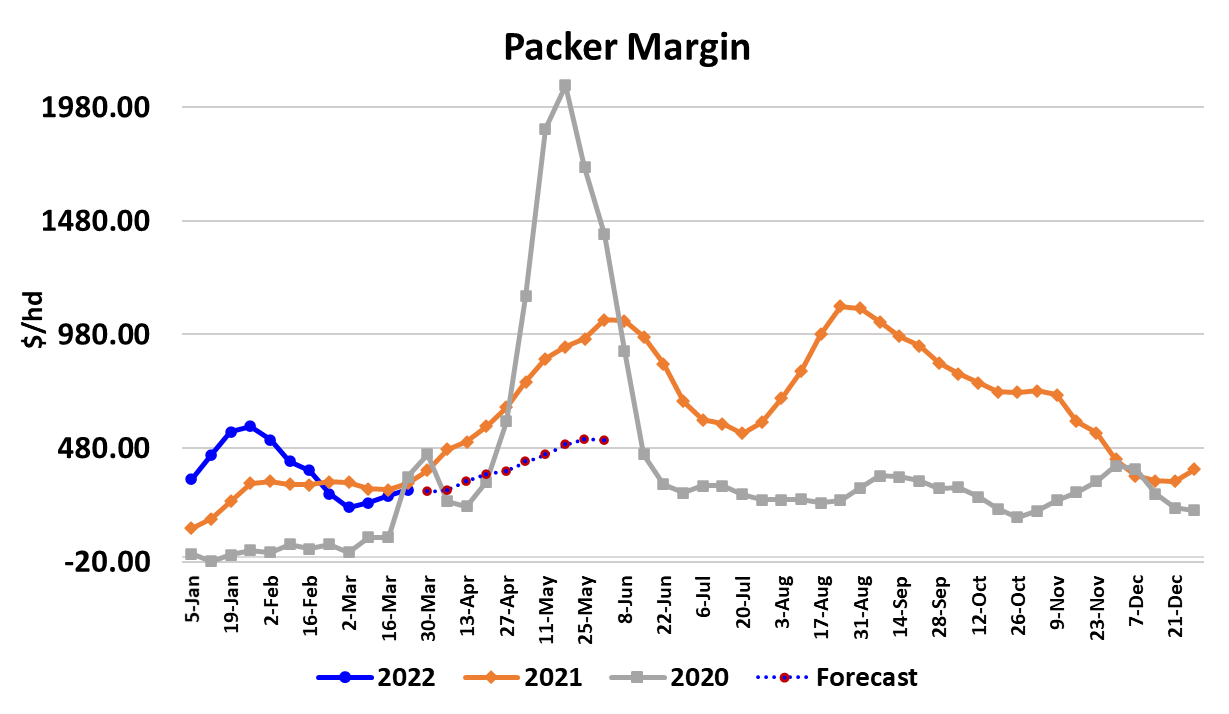

Packer margins are slowly on the mend after a soft February and I

calculate this week’s margin at $296/head, up $30 from last week.

Going forward, the margin should continue to grow since I see beef

prices appreciating faster than the cattle market over the next couple

of months. It is not unusual for packers to see some of their best

margins of the year in May and that may very well be the case again

this year. At some point, if margins grow at a good clip, then packers

may toss cattle feeders a small increase in cash cattle prices, but

that isn’t a given. Cattle feeders had been counting on a tight supply

picture this spring to improve prices, but the window of opportunity

for that is growing rather small.

By my calculation, cattle feeding margins are in the red by about

$140/head and given what they paid for feeder cattle a few months

back and the high price of corn, they would need to sell the finished

cattle for almost $150 just to break even. That doesn’t appear to be

in the cards. In fact, breakevens are projected to rise further and

could be close to $155 by Memorial Day. It looks like cattle feeders

are once again facing a long stretch of poor profitability. Grain

markets aren’t showing any signs of backing down as long as the

war in Europe is causing serious concerns about how much planting

will get done this spring in Ukraine and Russia. Sooner or later,

cattle feeders are going to face reality and start pressuring cash

feeder cattle prices lower. Deferred feeder cattle futures prices look

way too optimistic if corn pricing is going to remain near $7.50 per

bushel and fat cattle prices are going to struggle to add even a little

to current levels.

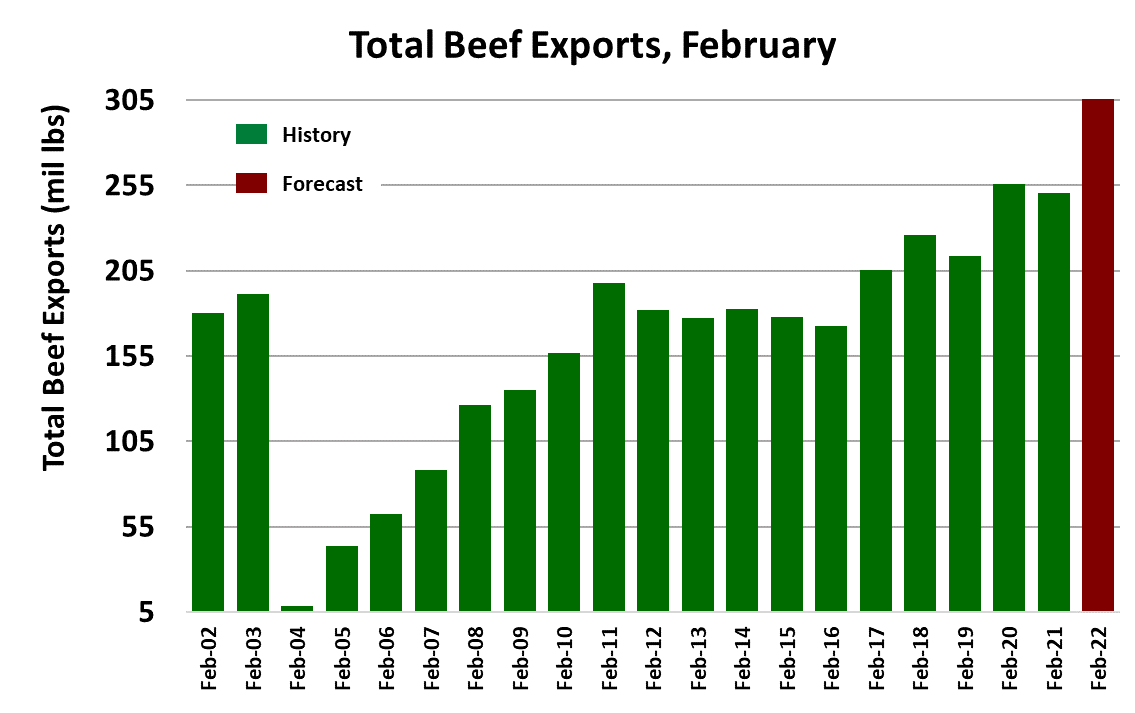

The weekly export report provided by USDA this week was a mess

because one or more entities failed to report exports over a period of

time and so USDA just dumped that entire volume into this week’s

report. I guess the one thing that we can surmise from that is that

exports have actually been better than the prior data suggested

through much of 2021. USDA will give us the official export numbers

for February on April 6. I’m expecting a little more than a 20% YOY

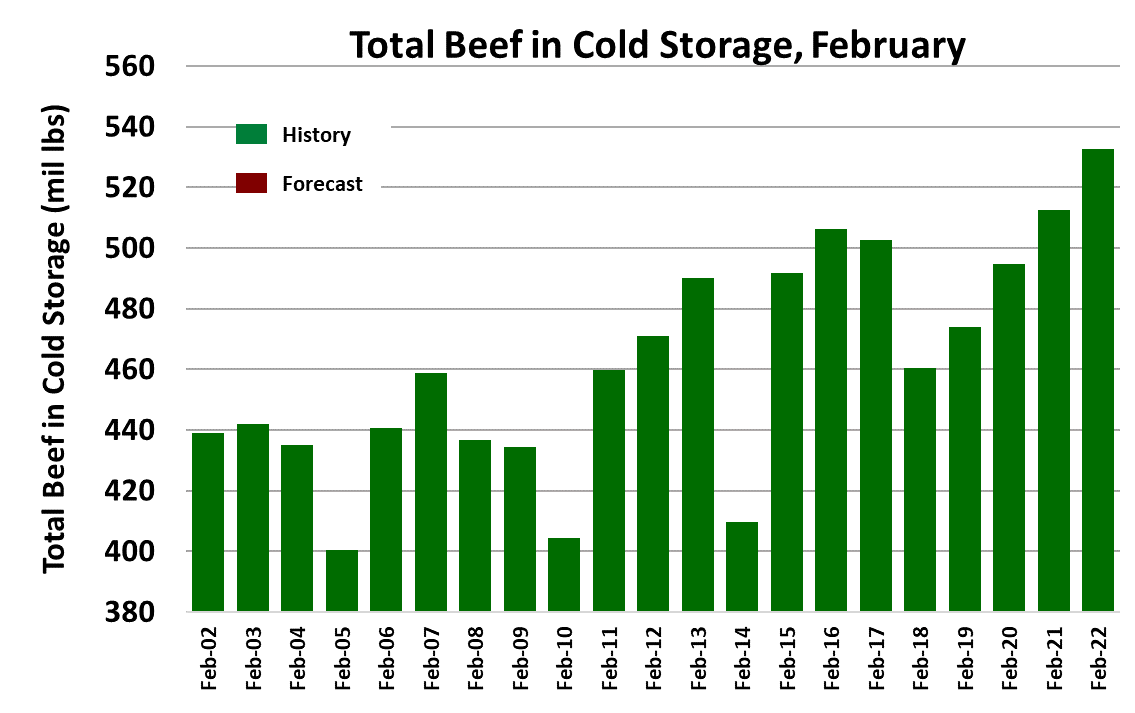

increase. USDA also released Cold Storage totals for February this

week and it showed a modest, counter-seasonal increase with most

of the increase attributable to whole muscle cuts, not boneless beef.

That may signal that foodservice has been socking away more

product than usual in anticipation of higher prices this spring and

summer.

The combined margin seems to confirm that a new demand upcycle

is underway. The fundamental forecast has the Choice cutout

peaking in the $290-295 range just ahead of Memorial Day and that

should be when the next downcycle in demand begins. Next week,

expect the market to get off on a sour note as traders react to

today’s bearish COF report. Keep an eye on the cutouts to see if

they struggle under the weight of this week’s additional production.

If they do, that could be an early sign that this demand cycle is going

to underperform what we’ve seen in the recent past.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}