Beef Wrap March 18

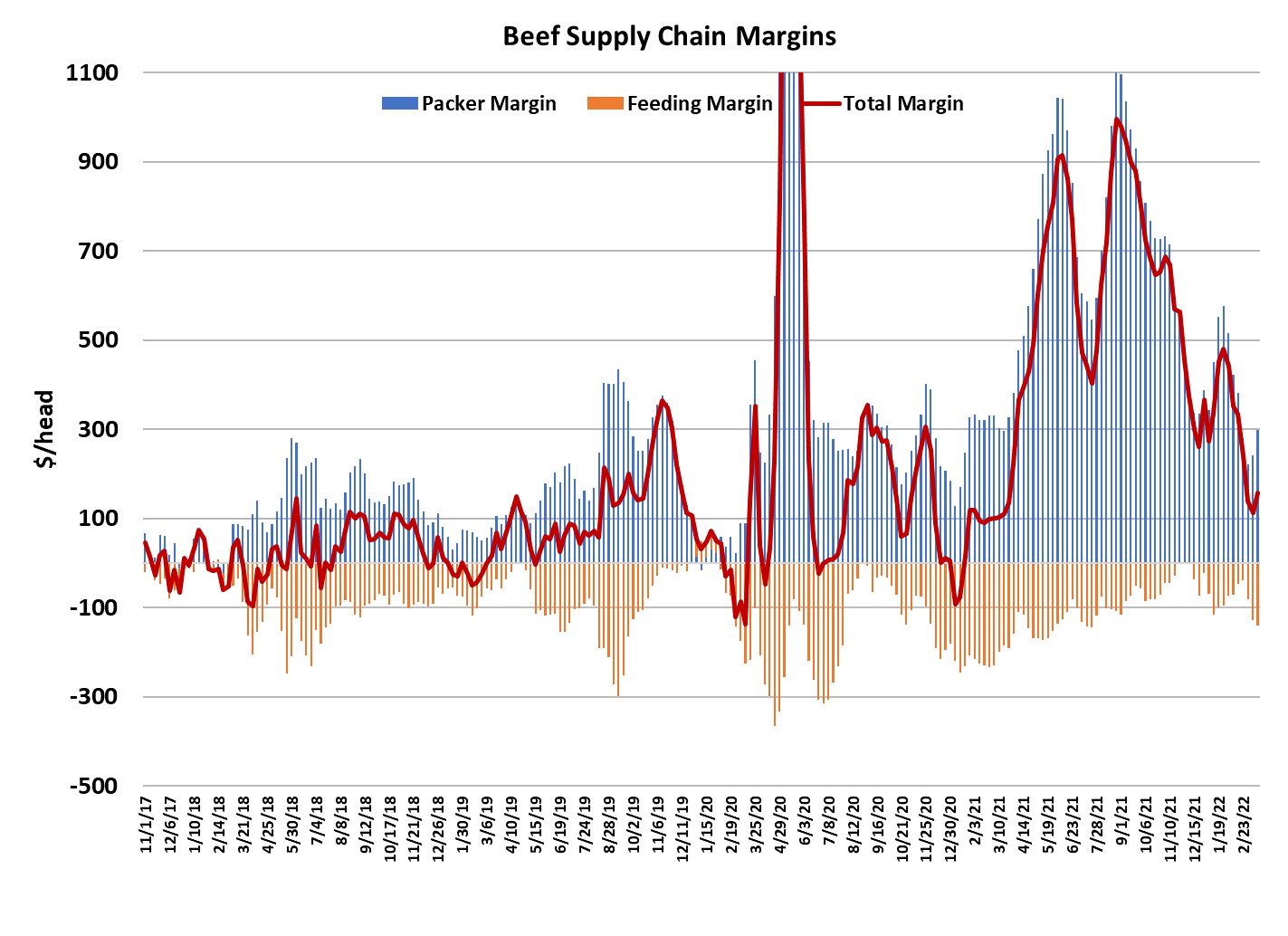

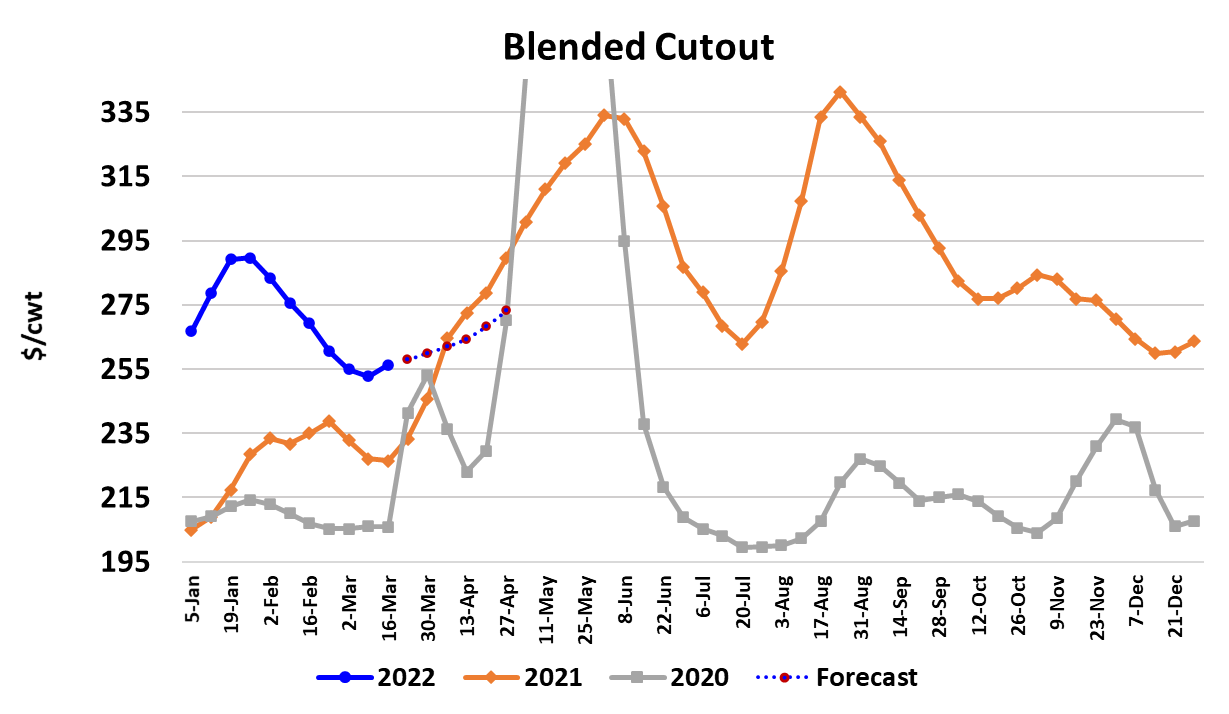

Packer margins got a little more breathing room this week as the

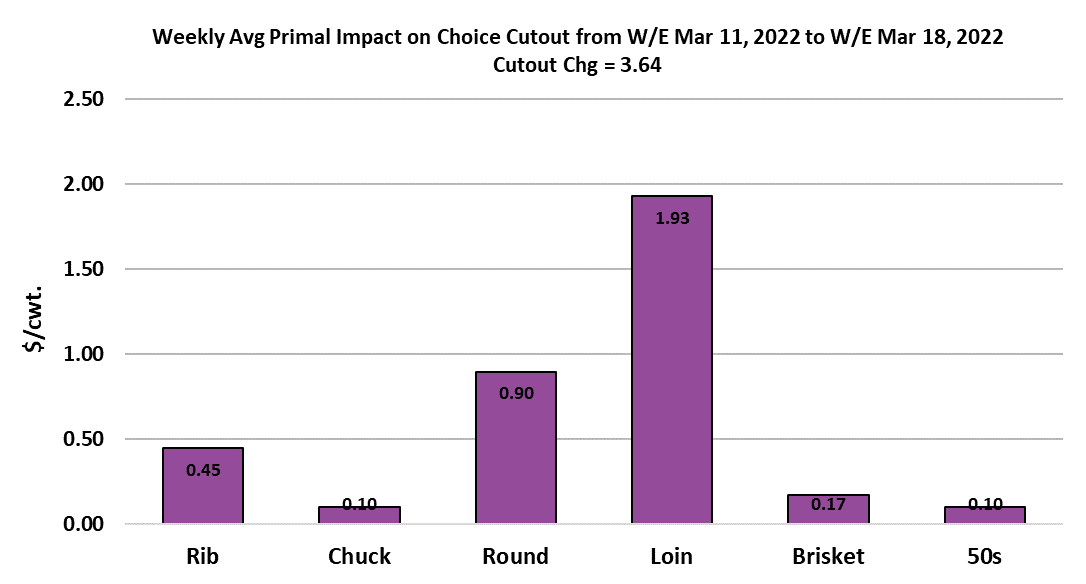

cutouts advanced while cash cattle stayed relatively flat. The Choice

cutout gained $3.64 on a weekly average basis and the Select was

up $2.79. This looks like the beginning of the usual spring rally in the

beef market. How high and how fast it goes remains to be seen, but

for now prices are finally advancing after being on the defensive

since late January. I estimate this week’s margin at $300/head, up

about $60 from last week. The margin should be even better next

week as beef prices are expected to continue higher and packers will

be killing cattle bought this week at steady money. I’m sure cattle

feeders were disappointed by the failure of cash cattle to turn higher

this week and many analysts were blaming external factors such as

the war in Ukraine for holding cattle back this week, but I suspect that

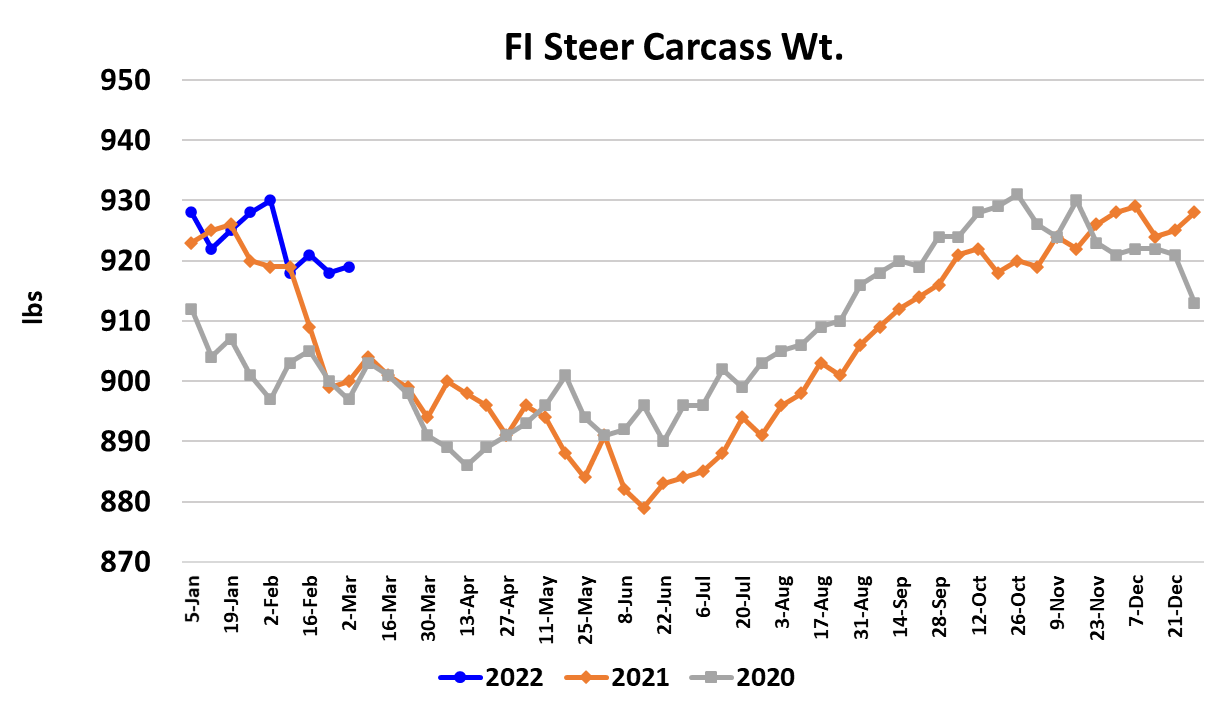

it has more to do with excellent feedyard performance this winter and

the fact that carcass weights are 16 pounds over last year.

Further, carcass weights have been steady at 919-920 pounds for

the last four weeks and this is the time of year when weights normally

drop precipitously. It leaves cattle feeders in a precarious position

where they can’t afford to hold cattle back in an effort to force

packers into raising bids. There is some risk of bunching cattle up

here in the next month or two as rather large placements from the

Oct-Dec period start to become market ready ahead of schedule

because of great weather and performance. There seems to be the

idea among market participants that market-ready supplies won’t

grow burdensome until summer, but if they are finishing ahead of

schedule, we could see the front end supply grow faster than

anticipated. This wouldn’t be much of a problem if packers were

slaughtering aggressively and thus helping to keep market-ready

supplies manageable, but packers seem to be taking a cautious

approach to kills.

They can recognize that beef demand is not robust and thus are

reluctant to push big production into the market before grilling season

demand gets its footing. This week’s fed kill amounted to only 494k,

up 2k from the week before and at least 15k below what our flow

model suggests should be slaughtered during March. The Saturday

steer and heifer slaughter was only about 35k, which is a far cry from

the 55k they were doing at this point last year when demand was

rapidly improving. So, you can see the problem facing cattle feeders.

I suspect that packers will use their leverage to keep cash cattle

relatively steady here in the high $138s over the next few weeks and

let their margins improve as boxed beef values climb. The demand

pendulum has finally swung back in a positive direction and the

combined margin confirms that the bottom is in for this cycle. I don’t

expect demand this spring to be as strong as it was last year

because there are a number of headwinds working against it.

To begin with, the retail prices that consumers see are almost 16%

over where they were last year at this time. Consumers also have to

deal with much higher energy, housing and transportation costs than

what prevailed last year. Further, covid has receded to such low

levels in the US that everyone is treating the pandemic as over.

That means they want to catch up on all of the things they missed

during the pandemic like travel and large gatherings. I suspect they

be happy to forgo an expensive beef meal in order to fill their tanks

and travel to places they were unable to visit during the pandemic.

Of course, just as I say that the pandemic has ended, there appears

yet another variant that is sweeping through Europe and it is

probably only a matter of weeks before it sweeps through North

America. That could push people back into stay-at-home mode and

thus boost beef demand, but my sense is that the population here in

the US is done with COVID whether or not COVID is done with us.

Travel will still happen, large gatherings will be held, and if that

means that the hospitals fill back up with COVID patients, well then

so be it. We have better tools now to combat COVID (vaccines and

anti-viral drugs) than we did in the early days and hopefully that will

keep the next wave from becoming a show stopper. I look for

demand to be best at the lower end of the beef spectrum this spring

and summer and that means grinds could perform better than pricey

middle meats. End meats should get support from very high lean

trimmings prices, but expensive tenders, strips and ribeyes are likely

to see demand considerably softer than last spring. Offtake into the

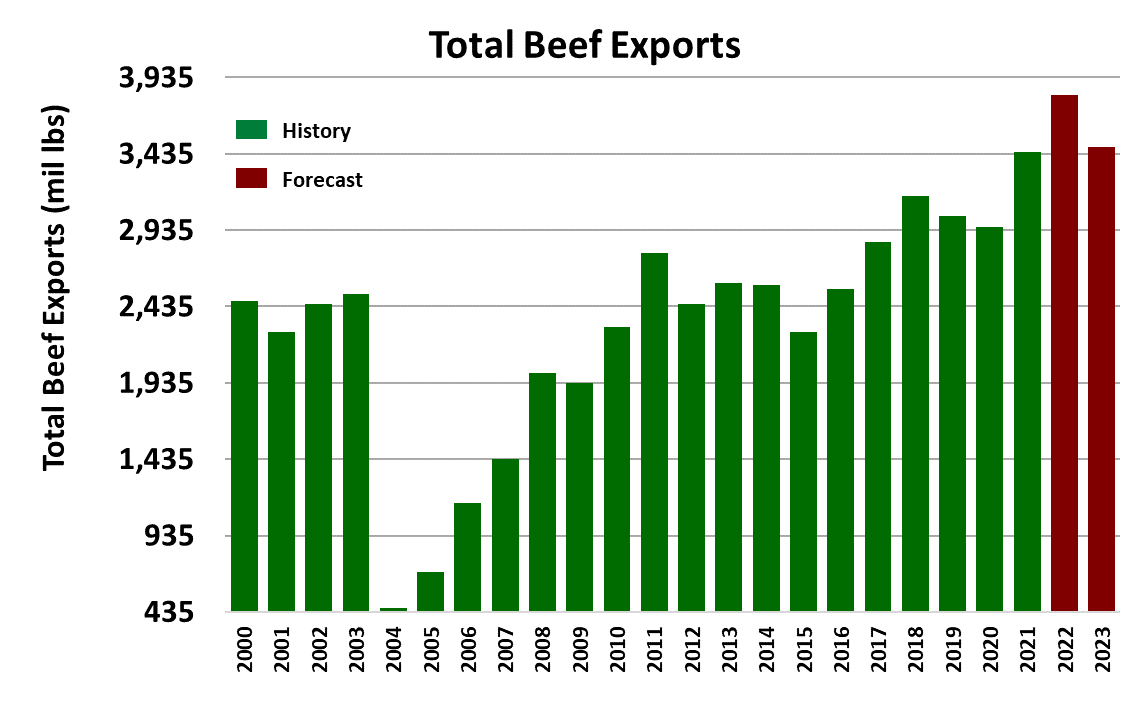

export markets is expected to remain rather good, with China being

a big customer for US beef over the next few months. I’m projecting

a 22% YOY increase in beef exports through the first half of 2022

and then volumes may track much closer to last year during the

second half of 2022. That would result in a 10-11% YOY increase in

exports in 2022 and that comes on the heels of a 17% increase last

year.

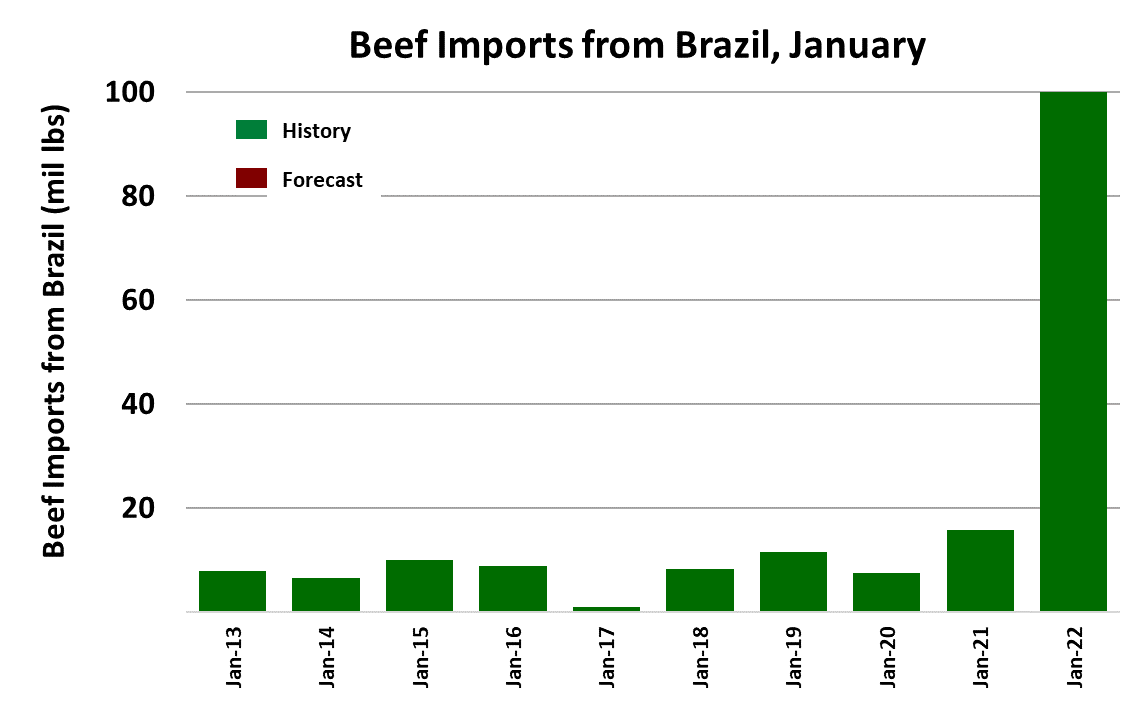

Beef imports are expected to be quite strong also and recently we

have been seeing a lot of Brazilian beef coming into the US market.

ERS data for January showed imports from Brazil at almost 100

million pounds. Last January they shipped 15 million pounds.

Mexico is also shipping more beef into the US. Volumes were up

62% YOY in January. So the strong import gains are coming from

the Americas, and not Oceania where they typically originate. Even

with the strong imports, I expect that the US will be a net beef

exporter again in 2022. Next week, watch the cutouts to see if they

can outpace this week’s rather small gains. That would be a sign

that spring demand is gaining traction. Also keep an eye on carcass

weights because those could be a leading indicator of the next

pricing problem in the fed cattle market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}