Beef Wrap April 1

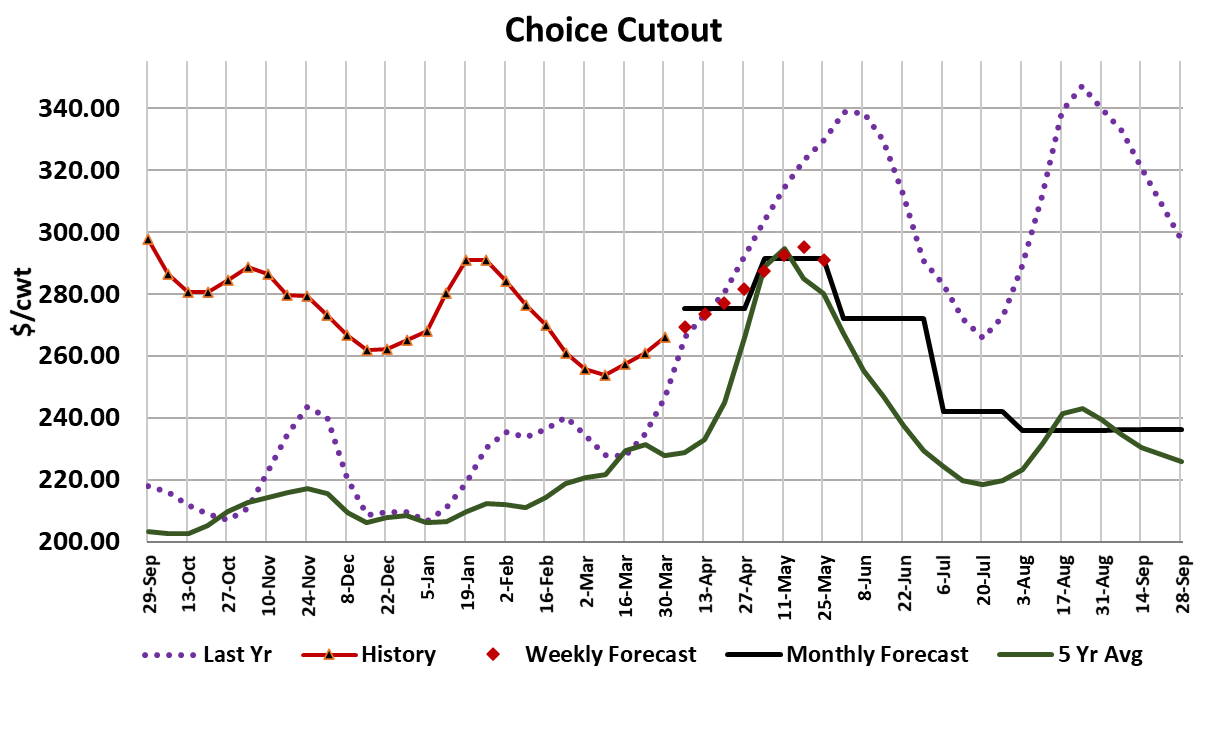

The beef markets continued higher this week, with the Choice cutout

gaining $5.06 on a weekly average basis and the Select adding

$6.22. As you might expect for this time of year, it was the middle

meat primals that led the cutout higher, but both cutouts were also

helped by soaring 50s prices. In the past two weeks, the 50s market

has gained $21/cwt and now sits at $131. It seems to me that this is

a demand-driven rally in the 50s, not a shortage of supply. Cattle

weights are quite heavy and so the carcasses should be generating a

lot of fat trim. Demand-wise, as consumers trade down from very

pricey middle meats, one of their targets is ground beef and that

means strong demand for both lean and fat trim. About 9 to 10% of a

cut-up carcass is 50% lean trimmings, so when they rally hard it really

helps boost the cutouts. I expect that fat trim prices will stay high at

least through Memorial Day and quite possibly for most of the

summer. There is almost certainly no relief coming next week given

that this week’s fed kill fell to only 490k.

That was down 15k from last week and more in line with kill levels in

two weeks prior to last week. To be fair, the flow model has pointed

to a dip in supplies during April and with cattle probably finishing

ahead of schedule, we shouldn’t be all that surprised if the light kills

came a little earlier than expected. It is probably a good thing that fed

kills are not all that big at present because my sense is that if kills

were much bigger, the cutout probably wouldn’t advance very quickly.

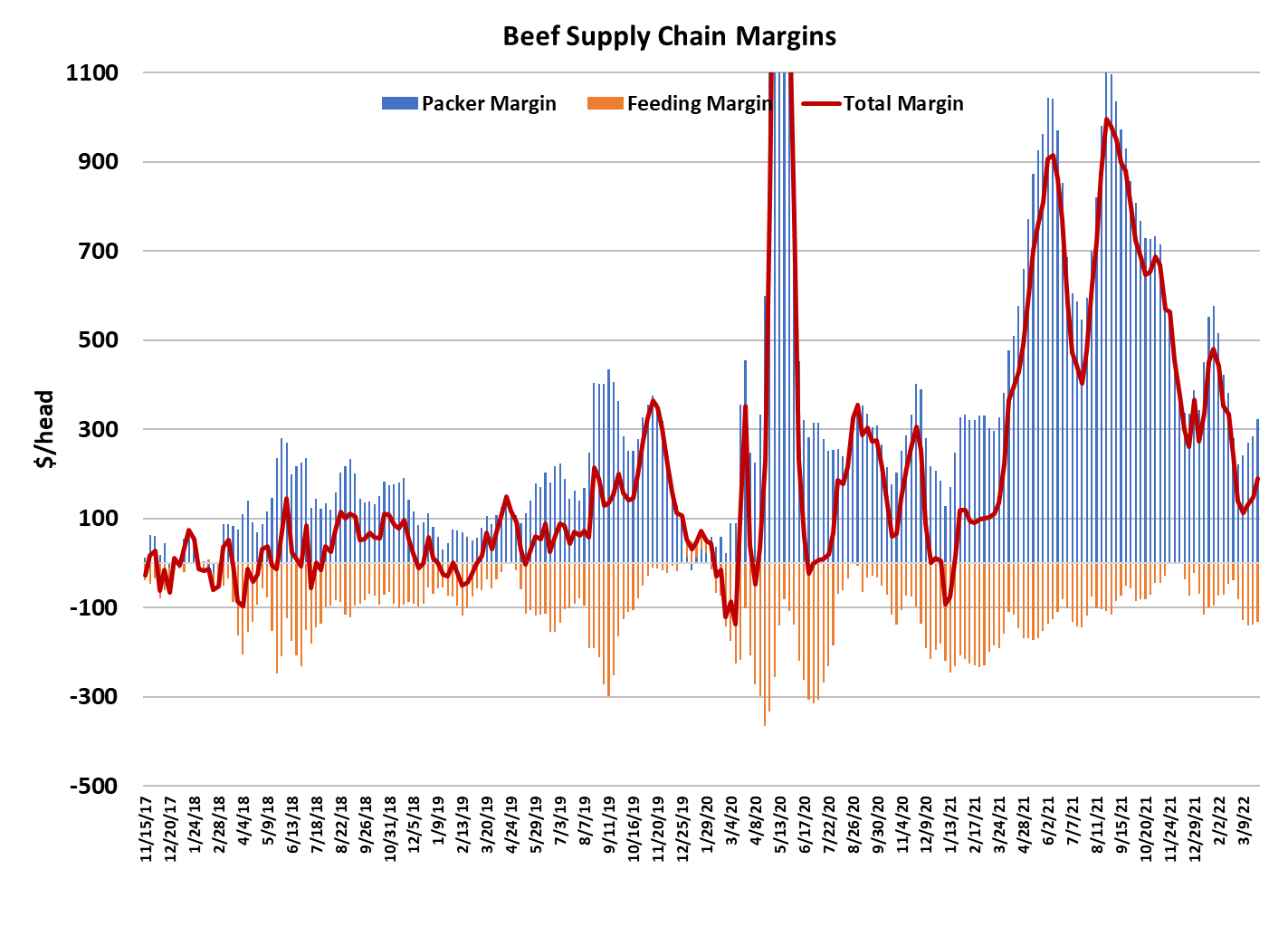

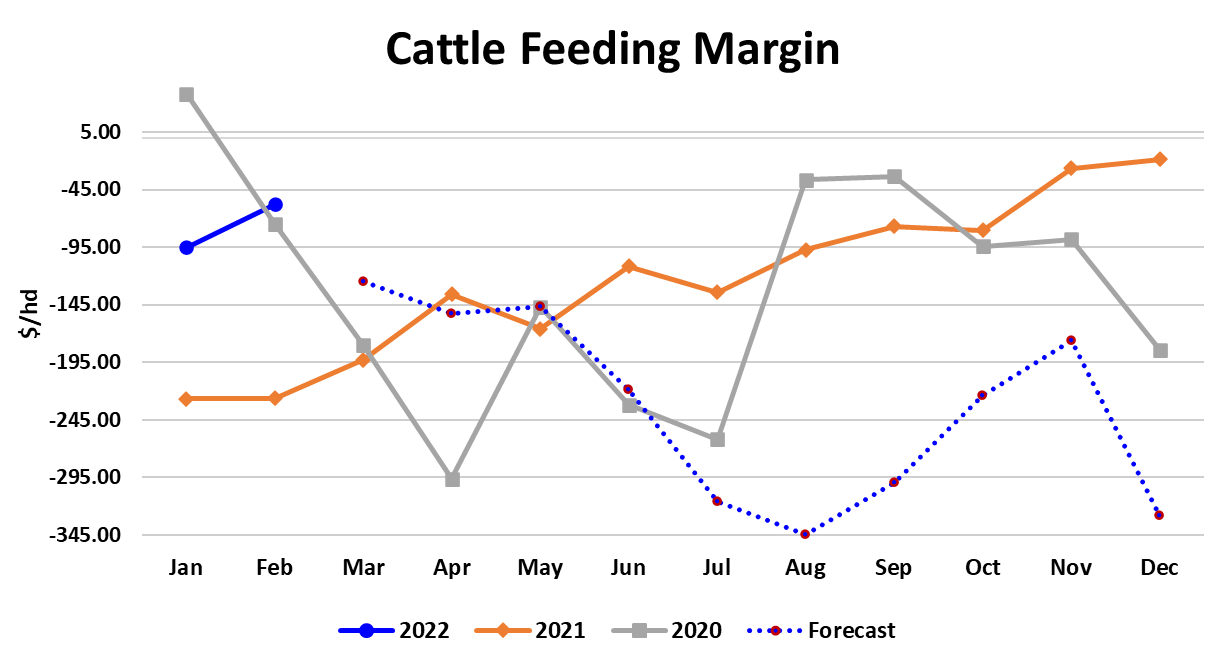

Demand is definitely in an uptrend and we can see that in the

combined margin chart and the daily demand scatters, but we are still

in the early stages of this demand cycle and it hasn’t gotten to full

steam yet. Retailers are asking consumers to pay some pretty high

prices for beef and that is likely going to be the stumbling block that

keeps this year’s spring rally well below what we saw last year. My

guess is that consumers will be a lot more interested in ground beef

than ribeyes this spring as they deal with price inflation in other areas

of the economy.

Further, the red flags are starting to go up about a potential recession

on the horizon and that is never good for beef demand. Honestly, I

think a recession is needed to cool down the inflation problem and the

red-hot labor market. But consumers are in no mood to think about

recessions right now. It is party time now that COVID infection rates

have fallen to almost zero. That is fine, but the party is going to be

expensive. Cash cattle averaged $139.36 this week, up about $0.50

from the week before. That makes it four weeks in a row that the

cash market has averaged below $140. Packers are focused on

regaining their margins and have little interest in paying up for cattle

right now. I calculate this week’s packer margin at $325/head, up $40

from last week. Cattle feeders don’t really seem to have enough

leverage to force cattle prices higher anyway.

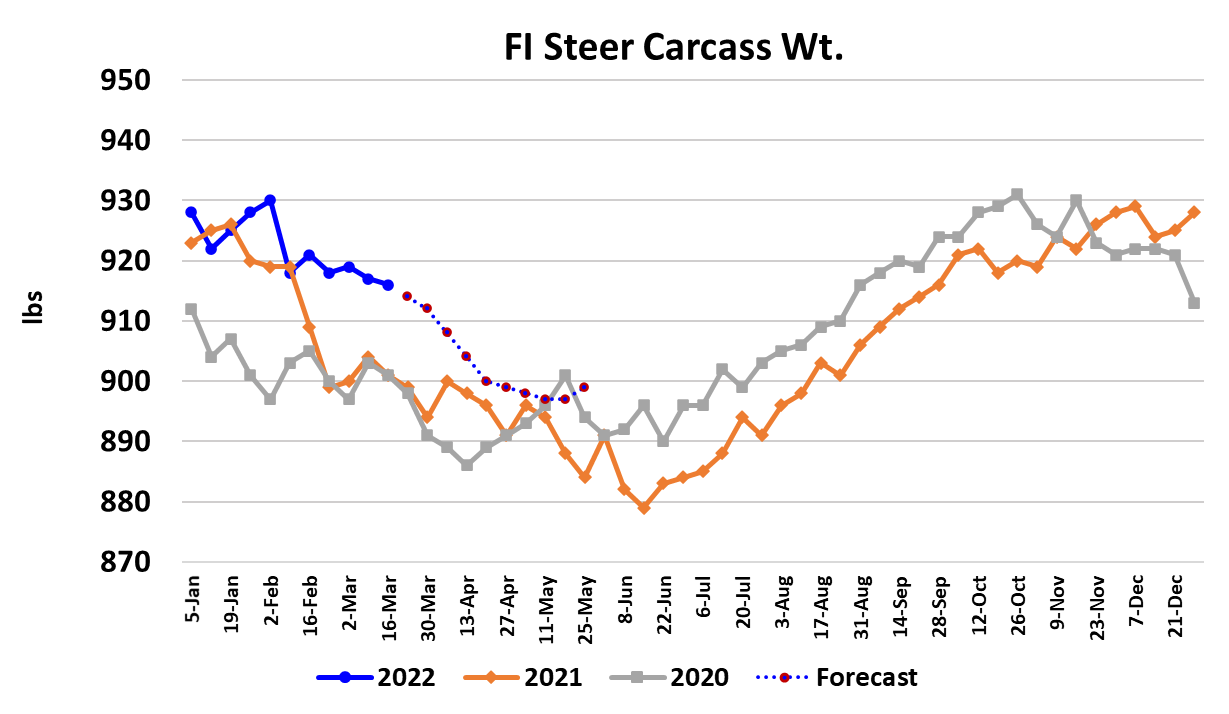

Steer weights were down only 1 pound this week and they are still

15 pounds heavier than last year. I have to believe that they need to

keep the cattle moving out of feedyards and thus can’t bargain from

a position of strength with packers right now. That situation of poor

producer leverage is likely to get worse before it gets better. The

flow model is pointing to considerably larger numbers of marketready cattle during May and June than in April. My guess is that

cash cattle prices struggle to do much better than about $142 from

now until Memorial Day. Over the same period, I’m forecasting the

Choice cutout to push towards the high $280s or low $290s, so I

suspect that packer margins will move back close to $500/head

before June 1. The risk is that cattle prices tumble between now

and then and thus packer margins exceed my forecast. Feedyards

are full of cattle and they are heavy. USDA estimated feedyard

inventories as of March 1 were 1.6% higher than last year’s recordlarge number. There is a bulge in fed cattle supplies coming in the

May/June/July period—the result of strong placements late last year

and there is no stopping that train now.

Cattle feeders seem to recognize that there is a problem on the

horizon because it looks like they really slowed down placements

during March. That is fine, but it won’t provide much supply

tightening until Sep/Oct. In the meantime, high feed costs are

expected to keep cattle feeding margins solidly in the red all

summer. USDA released its Prospective Plantings report this week

and it showed that US farmers are planning to plant a lot less corn

than expected. That is unfortunate because the war in Ukraine is

likely to greatly reduce production in that area of the world and the

hope was that US producers could make up a chunk of that lost

production. Farmers are seeing huge price increases in nearly all of

the inputs needed to grow a corn crop, with fuel and fertilizer leading

the way.

The tight corn balance sheet is likely to keep corn futures well

supported into summer and they will be very vulnerable to any

issues that might arise in getting the crop planted. Normally, when

corn prices go up cattle feeders work hard to pay less for feeder

cattle in order to compensate. So far this year however, it looks like

they haven’t done a very good job with that and are over-paying for

feeder cattle given current corn prices. That is how they ended up

facing the prospect of negative margins from now until fall. Next

week, watch the fed kill to see if packers can get it back over 500k.

The following week is Easter and that will see lighter-than-normal

production on Good Friday and the Saturday following, so they may

try to boost next week’s kill to compensate. However, if the fed kill

remains down around 490k or less, the prospects for a stronger

cattle market this spring start to get more remote.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}