Beef Wrap March 24

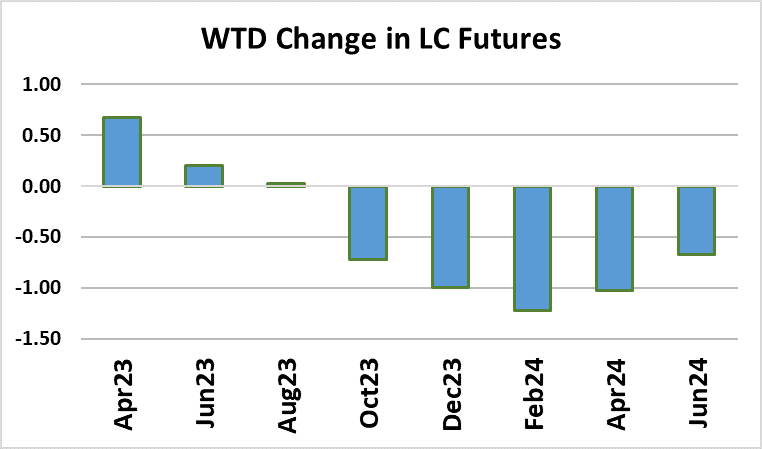

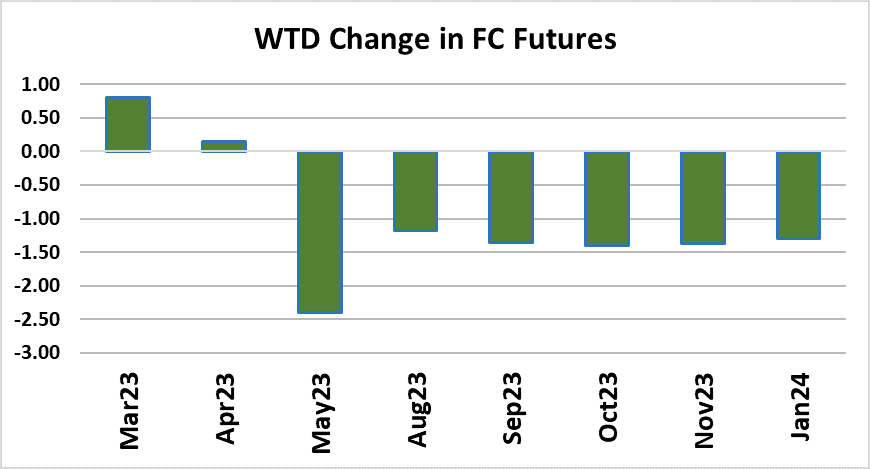

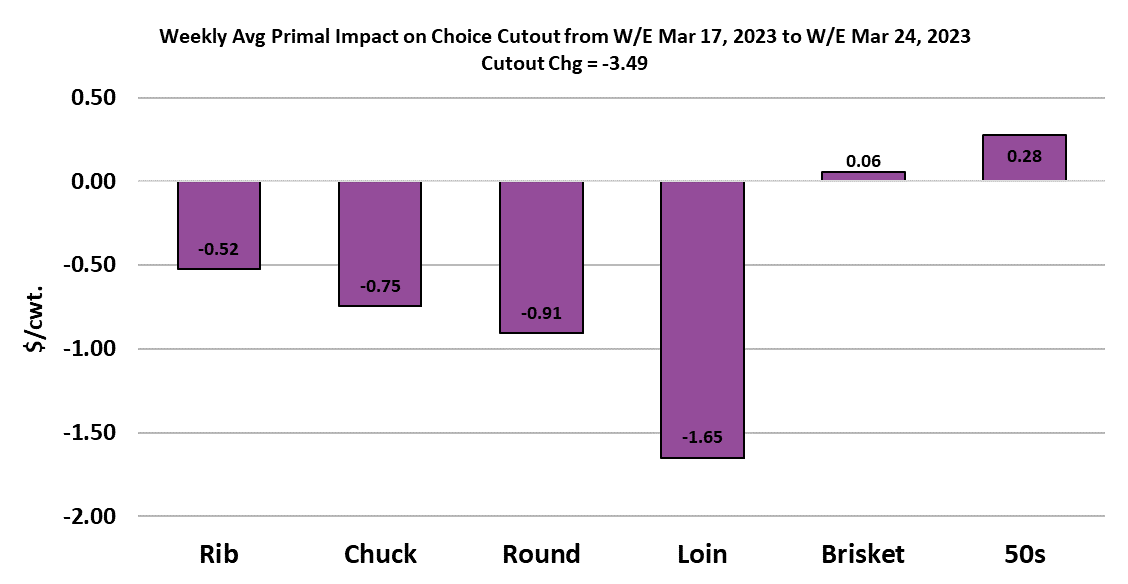

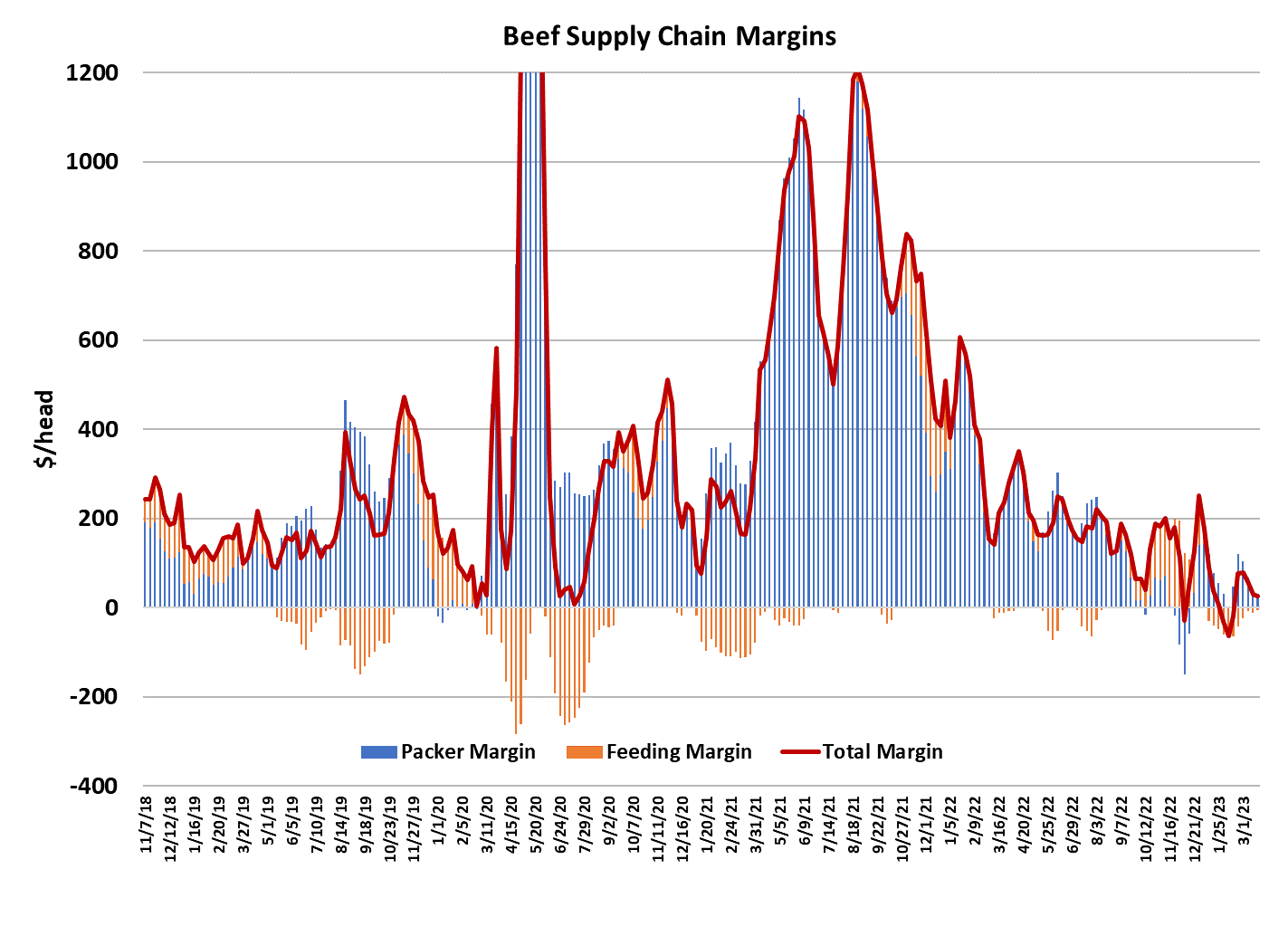

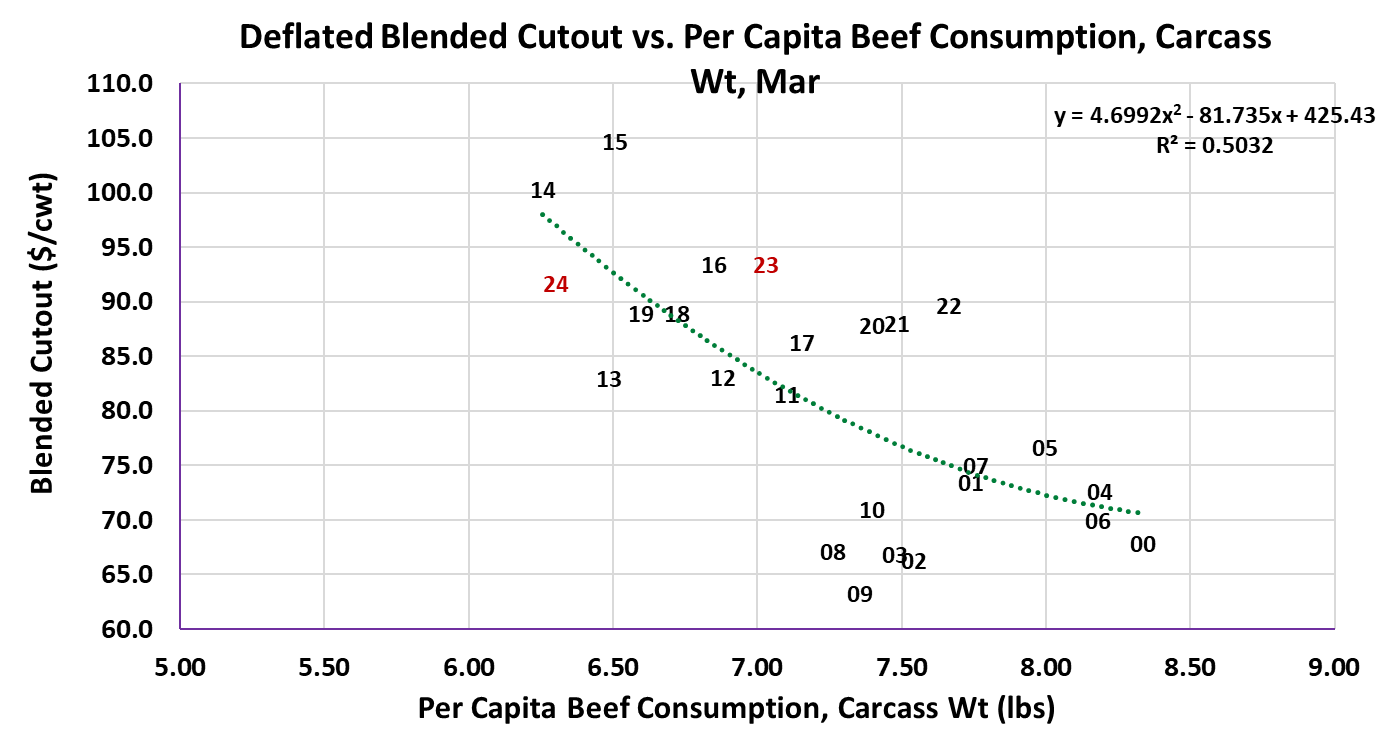

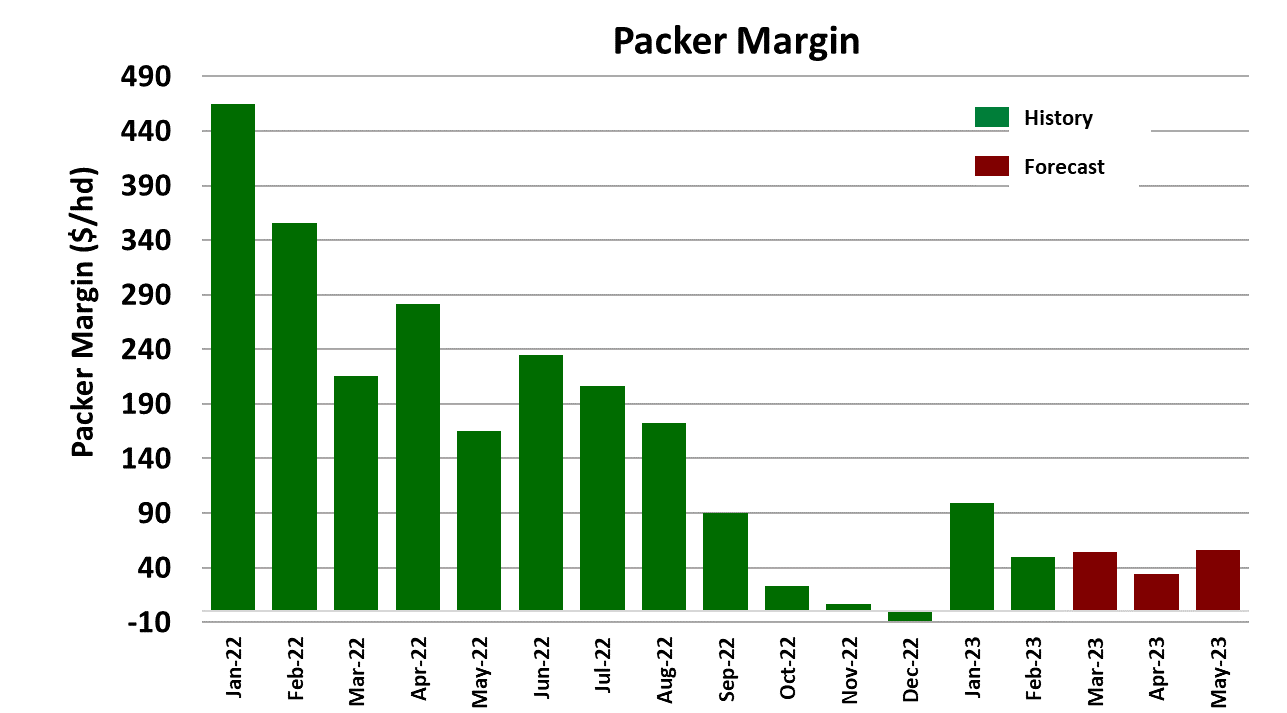

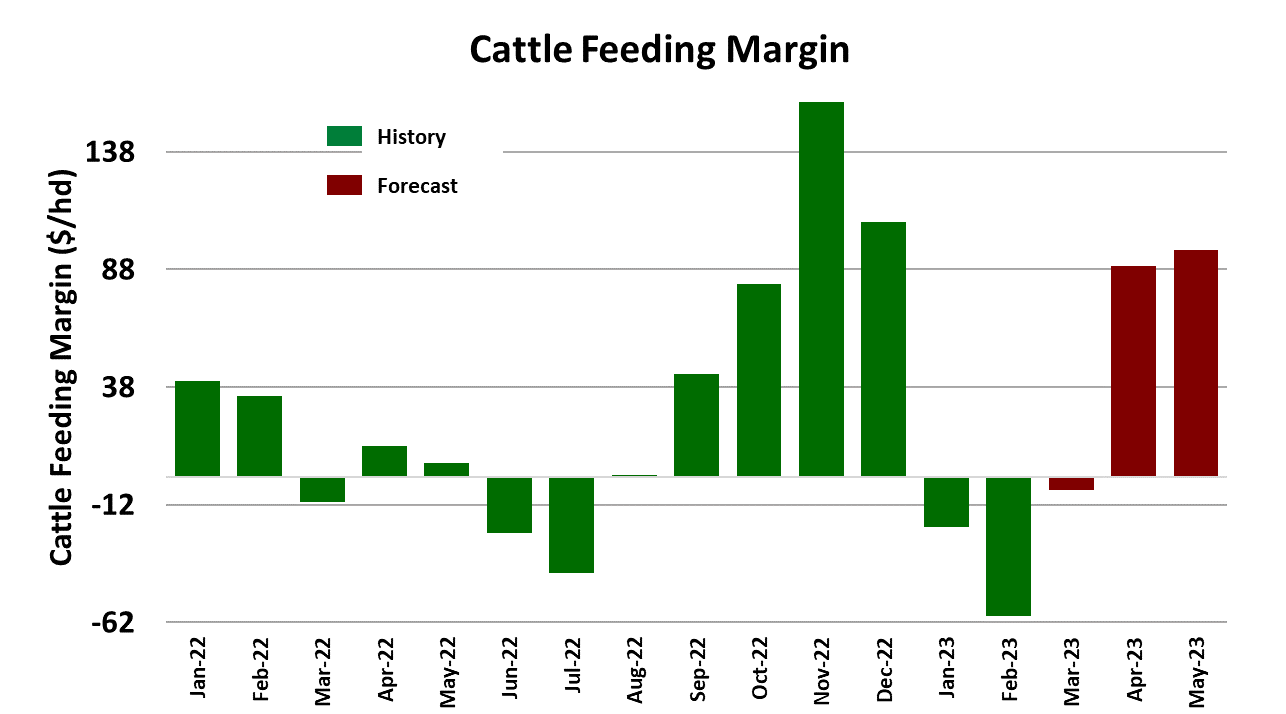

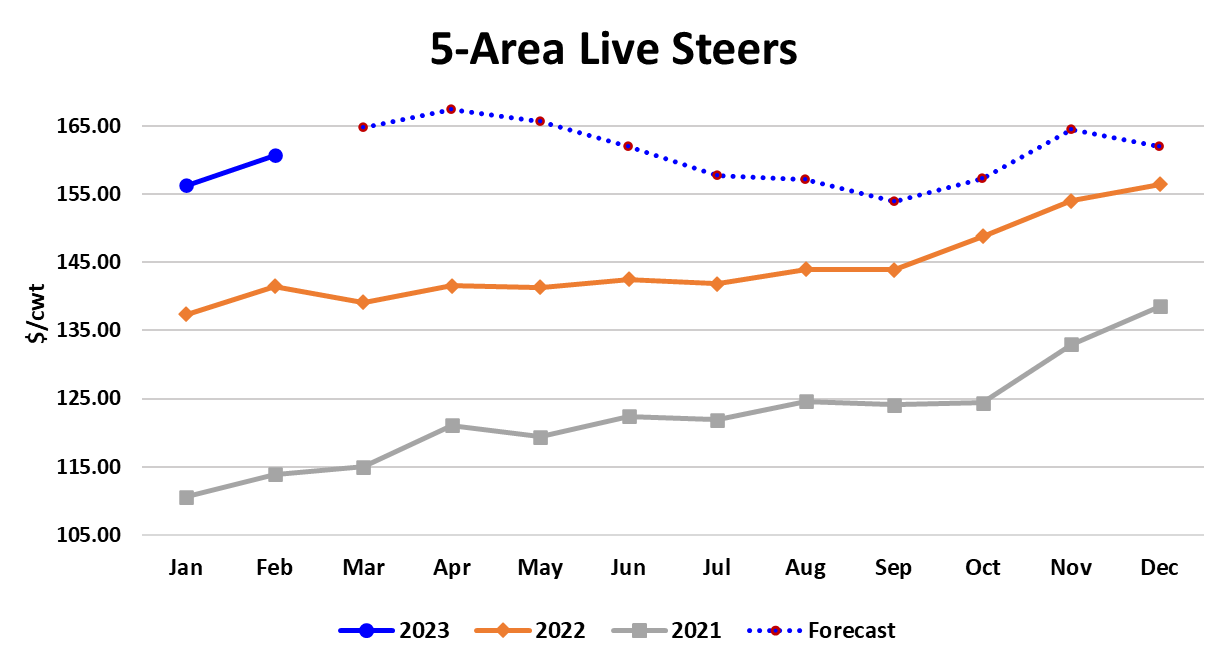

The beef cutouts continued lower this week, with the Choice losing $3.49/cwt to average close to $281 and the Select dropping 2.41/cwt to average just over $270. The weakness was spread throughout the carcass with both middle meats and end meats posting modest declines. Last week’s beef production was up about 7 million pounds from the previous week, so perhaps that explains at least part of the downward price pressure. There could also have been some consumer resistance starting to creep in as retailers begin to shy away from expensive beef items in their weekly ads. I don’t really think that will last very long at this time of year because the April is just around the corner and traditionally beef demand surges as consumers get out to enjoy the warmer weather. With Easter coming on April 9 this year, retailers are probably preparing to run strong grilling ads for the week following Easter. That product has likely already been booked, but good clearance would send retailers back the following week looking to fill in inventory gaps. So there is reason to hope that beef demand will see some improvement in coming weeks. Cattle feeders were able to add a tiny bit to cash prices this week, with the average coming in near $164.45/cwt, up about $0.25 from the week before. That was a bit of a surprise to many observers who were expecting the cash retreat further after dropping $1 the week before. Cattle availability remains tight and the flow model suggests that steer and heifer kills should track right around 490k per week from now through the end of April. This week’s fed kill registered 491k, so it was right in line with the model. However, my fear is that the industry may be setting up for another situation like we saw late last year ahead of the holidays when packers were eager for high quality middle meats and so they ramped up the kill beyond what available cattle supplies would support and it resulted in steadily increasing cash cattle prices. High quality middles are likely to be sought after this spring in the same way and, with cattle availability so tight, it could result in a similar strengthening of cash cattle prices. So far, Apr and Jun LC futures haven’t seen it that way and both are trading about $5/cwt below where my read of the fundamentals suggest they should expire. As long as the cutouts are easing, there is little reason for traders to get bullish the futures, but once the cutouts turn higher, the memories of last fall may begin to influence trader attitudes. The Choice-Select spread is expected to move from around $10/cwt this week to close to $30/cwt ahead of Memorial Day. One potential fly in the ointment for that scenario is that in the last year or so, prices in the cattle and beef complex have not followed traditional seasonal patterns very closely. We had strong price rallies in February, when the seasonal suggested that prices should be declining and we had price weakness in Sep/early Oct when the approaching holiday season should have boosted demand. So while the spring grilling season rally is normally very reliable in this market, recent history suggests there may be more risk to that occurring on schedule this year. The combined margin moved a little lower this week and clearly appears to be in a downcycle right now, so that is also concerning. I calculate packer margins this week at only +$27/head and have cattle feeding margins almost at breakeven. The breakevens for cattle feeders should ease lower in the coming weeks, reflecting the slump in feeder cattle prices back in October when these animals were placed on feed. However, within 6-8 weeks breakevens will begin to rise again and put additional pressure on cattle feeders to extract more margin from the packers. There just isn’t much margin in the system right now and the only way to improve that situation is to somehow convince consumers to pay more for beef. That could be a struggle as we move deeper into 2023. The macro picture looks dimmer by the day, with consumers hearing about bank failures and watching the resulting market turmoil push their retirement accounts lower. We know that millions of poor Americans who depend upon the food stamp program had a lot less to spend in March as the covid bump in benefits expired. That could have driven those consumers to trade down and we have seen very strong pricing lately in the trimmings market. Fat trim closed just over $140/cwt on Friday and the fresh 90s were averaging over $275/cwt. I suspect that much of the gains in fat trim are related to the fact that carcass weights are presently pretty light and when that is combined with fed kills consistently below 500k per week, it implies pretty light production of fat trim. The weekly data suggests that export markets are starting to struggle, particularly with respect to Japan and S. Korea. It looks to me like it will be very difficult for beef exports to match last year for at least the next six months. Deteriorating exports could become a headwind that limits how high the cutouts go this spring and summer. The domestic demand scatter for March is currently signaling decent demand, but a little below last year’s strong showing. The current forecast has the Choice cutout reaching a peak near $290/cwt during the middle of May, but there is probably more upside risk to that forecast than downside risk. I wouldn’t be particularly surprised to see the Choice cutout top $300 at some point this spring if the middles really heat up. Next week, watch for some modest increases in the cutout, driven by the middles as retailers prep for their post-Easter features. That should be enough to hold the cash cattle market close to steady with some potential for a small gain.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}