Beef Wrap March 31

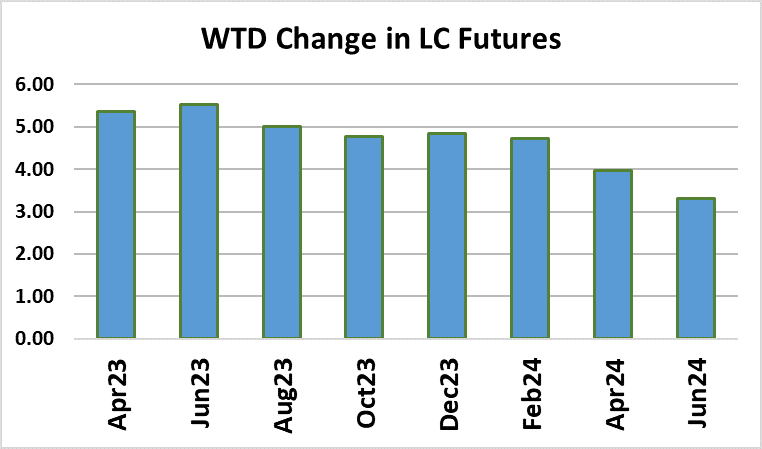

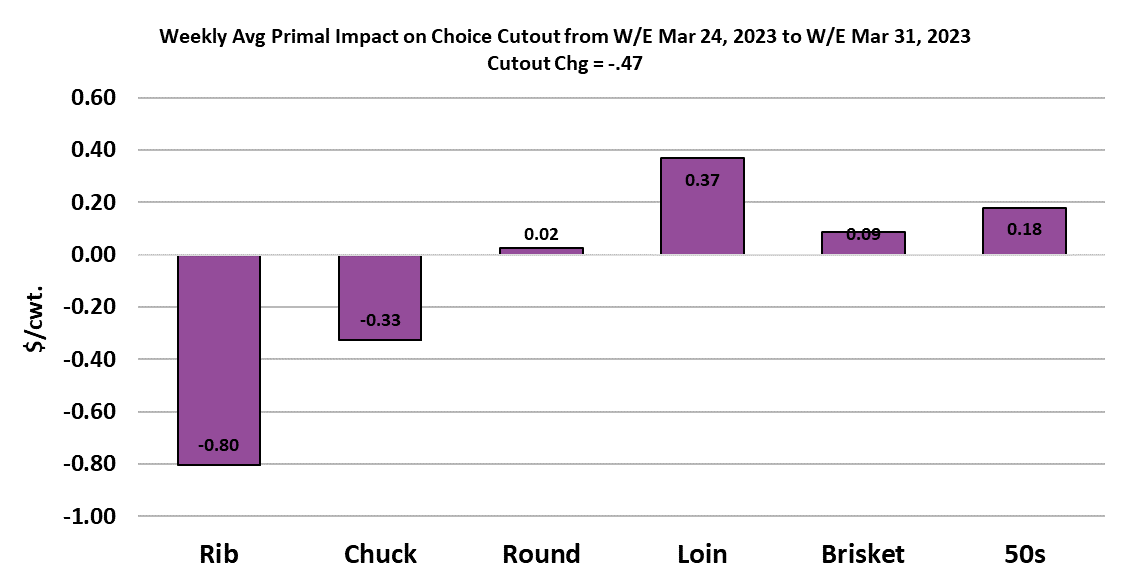

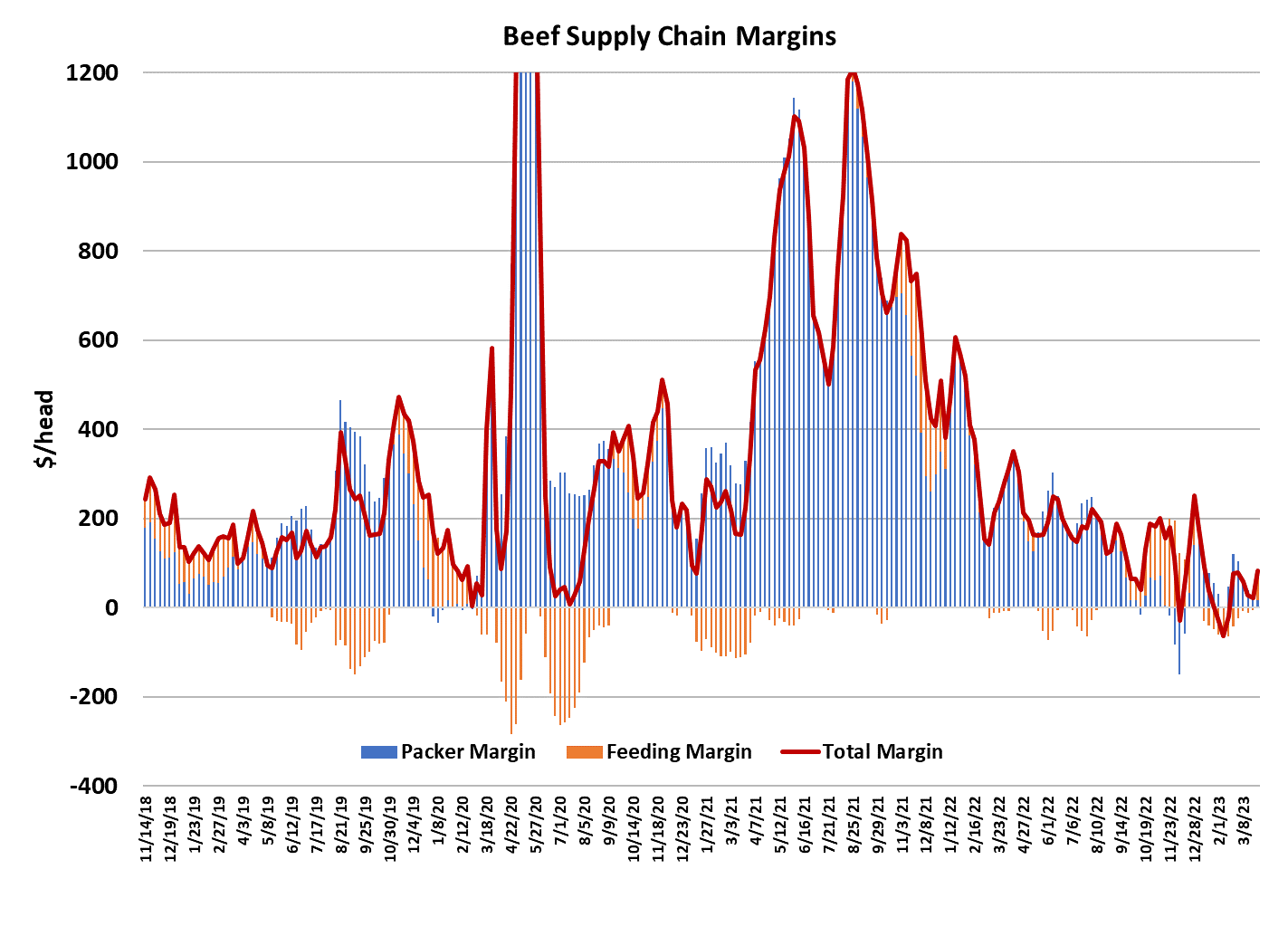

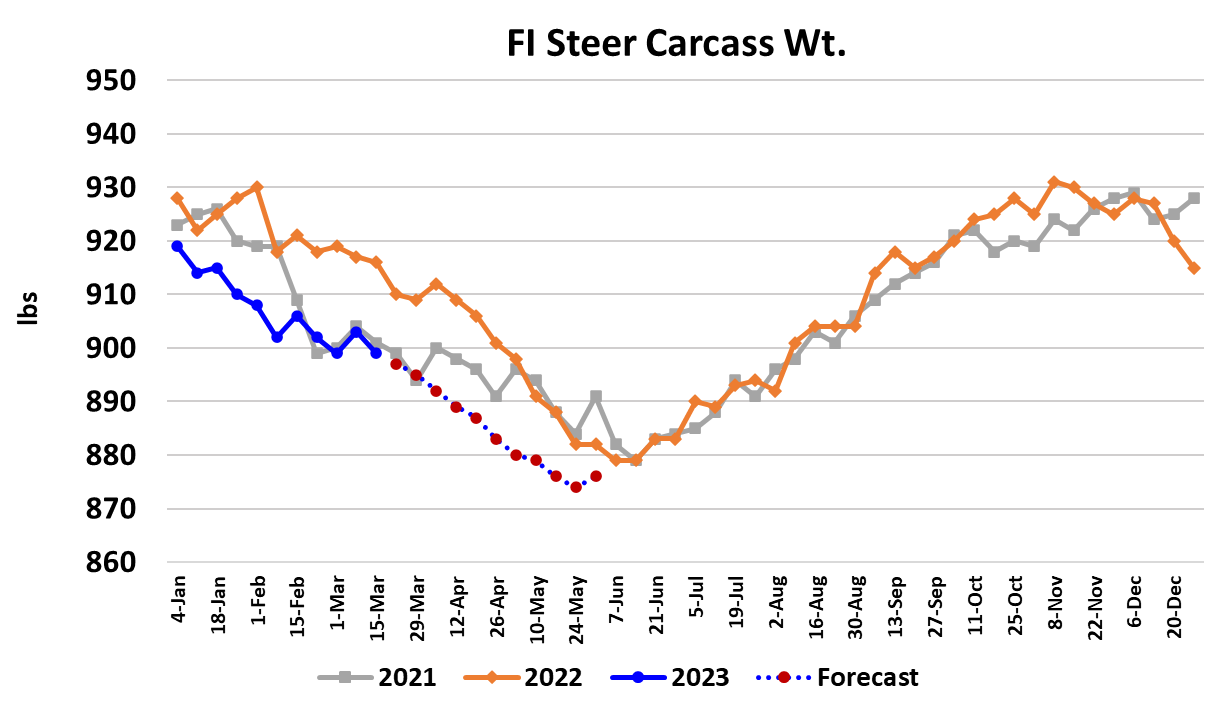

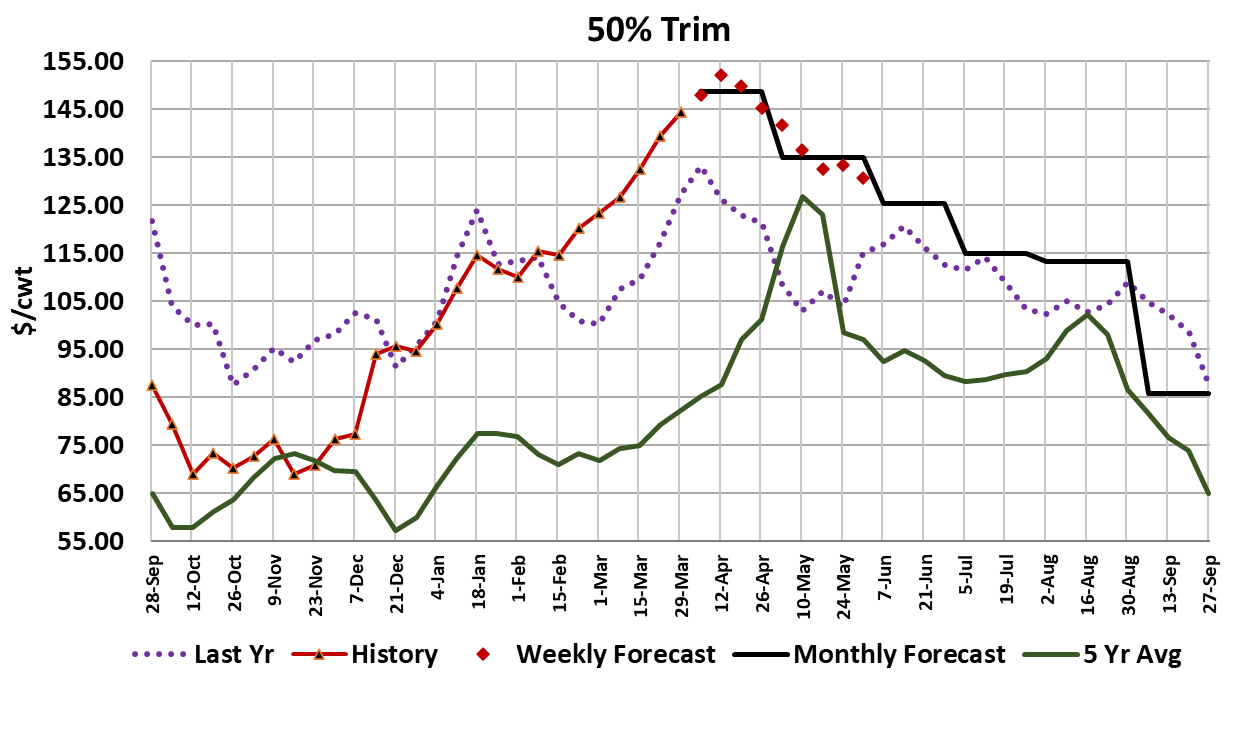

The cash cattle market lurched higher this week, adding $4.23/cwt to average $168.64/cwt. The futures market cheered this development, with the front contracts gaining over $5/cwt on the week. Exactly what spurred the sharp increase was unclear since the beef market was mostly a sideways affair and it looked like packers had adequate live inventory after the previous week’s big buy. Further, next week’s kill will be tempered a bit by a smallish kill on Good Friday and Saturday. Perhaps packers were gearing up to deliver contracted beef for the week following Easter or it might just have been good ole fashioned competition between the packers. Whatever the impetus, cattle feeders certainly welcomed the boost in prices because it moved their margin from slightly negative to +$73/head this week. The Choice cutout fell $0.47 to $280.51 on a weekly average basis and the Select cutout was down $0.96 to $269.63. Most of the decline in the beef took place before Thursday’s sharp gains in the cattle market and the packer sales desk was busy on Friday informing buyers that beef prices would be going up because they had to pay much more for cattle. That can work in the short run because there were likely some buyers that got caught short and thus had to pay up, but in a longer-run context consumer beef demand will decide prices at the wholesale level. One thing it will almost certainly do is keep retailers from lowering beef prices and could result in further increases in those consumer-facing price levels. Beef production is probably going to remain constrained for the next six weeks, so rising retail prices to slow consumption might not be such a bad thing. The problem will come in June when production expands seasonally and retailers have consumer prices set so high that offtake doesn’t keep up with production. At that point, there will probably need to be a re-think about price levels at the packer and feedlot levels. Until then however, it is full-on grilling season and consumers will likely continue to pick up beef out of the meat case without undue regard for price. Buyers have been amply warned about tight availability for high quality middles in April and May, so hopefully they have a sizeable portion of their needs covered by now. The sharp increase in cattle prices will put packer margins in the red next week unless they can rapidly escalate wholesale beef prices. The combined margin turned higher this week because the higher cattle prices affect cattle feeding margins in the current week, but don’t affect packer margins until the following week. My guess is that the combined margin will continue higher because packers will find some success in raising the cutouts next week and beyond. It was interesting that the rib primal was the biggest drag on the cutout this week. Perhaps that was just a little lull in buying ahead of Easter. The 50s market averaged close to $145/cwt this week, up about $6 from the week before. I have always considered strong pricing in fat trim to be a bullish indicator for cattle pricing because it often reflects light carcass weights and very current feedyards. Steer carcass weights dropped four pounds in this week’s data release and are now 11 pounds below last year. Lean trim prices have also been steadily rising, this week averaging about $275/cwt and $8 below this time last year. Interestingly, ground beef pricing hasn’t been all that hot, with the 81% coarse ground trading sideways to lower in recent weeks. If consumers are trading down, it isn’t evident in ground beef prices and it certainly isn’t evident in pork prices. The macro picture seems to have stabilized a bit this week as the banking crisis eased and the stock market posted decent gains. Inflation remains a problem, but it too seems to be slowly easing. That said, consumers at the lower echelons of the income pyramid are becoming increasingly distressed and are having to rely more on savings and credit to make ends meet. It probably won’t be long before those consumers are priced completely out of the beef market and have to rely on other sources of protein. For now however, it looks like the market is entering another upcycle in demand and this one should carry until Memorial Day at least. This week’s fed kill registered 510k, which was up 25k from the week before and way larger than what past placements suggested should have been available. Perhaps packers are already starting to over-kill the available supply as they search for those prized Choice middle meats. That big kill was probably a factor in packers’ aggressive behavior in the cash cattle market this week. Next week, I’m looking for the fed kill to drop back under 490k, tempered somewhat by smaller-than-normal kills on Friday and Saturday ahead of the holidays. If packers come out in the week after Easter determined to kill 500k+ steers and heifers each week, then I’m afraid that they will continue to run the cash cattle market higher because the flow model is suggesting availability of only around 480k per week until mid-May. Something tells me that packers will have a hard time constraining the fed kill to just 480-490k between Easter and mid-May. It isn’t all rainbows and unicorns in the beef market. We are starting to see evidence of export volumes softening. That will probably only get worse as the cutouts increase between now and Memorial Day. Pricewise, it probably won’t matter much as long as grilling season is in play, but as we move toward the dog days of summer I think the market will start to really miss that export business. For now however, it looks like all of the price arrows are pointed up. Next week, watch for substantive increases in the cutouts as packers jawbone beef buyers with their sad story about having to pay more for cattle. The cash cattle market probably takes a breather for the next week or two, but I wouldn’t expect it to decline much, if any.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}