Beef Wrap March 17

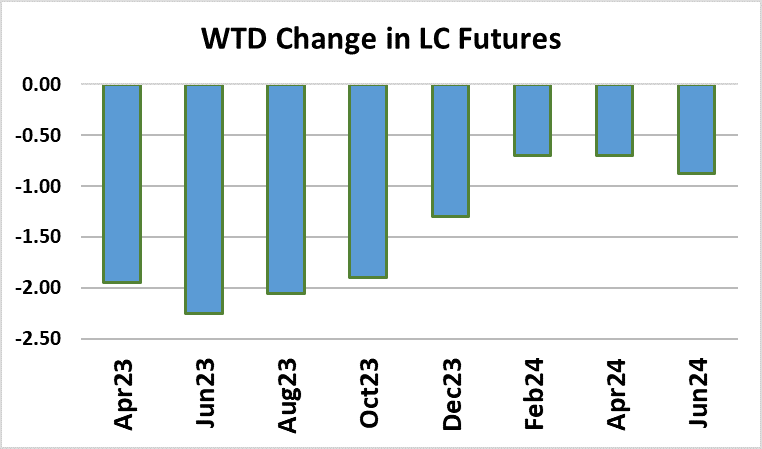

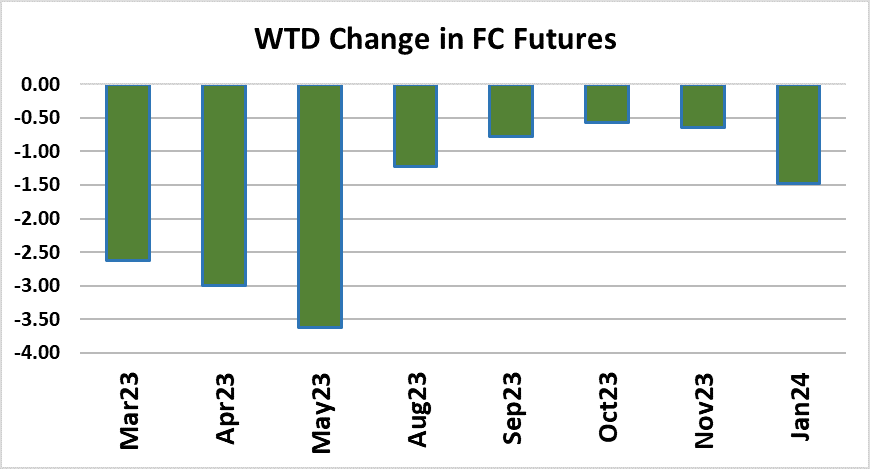

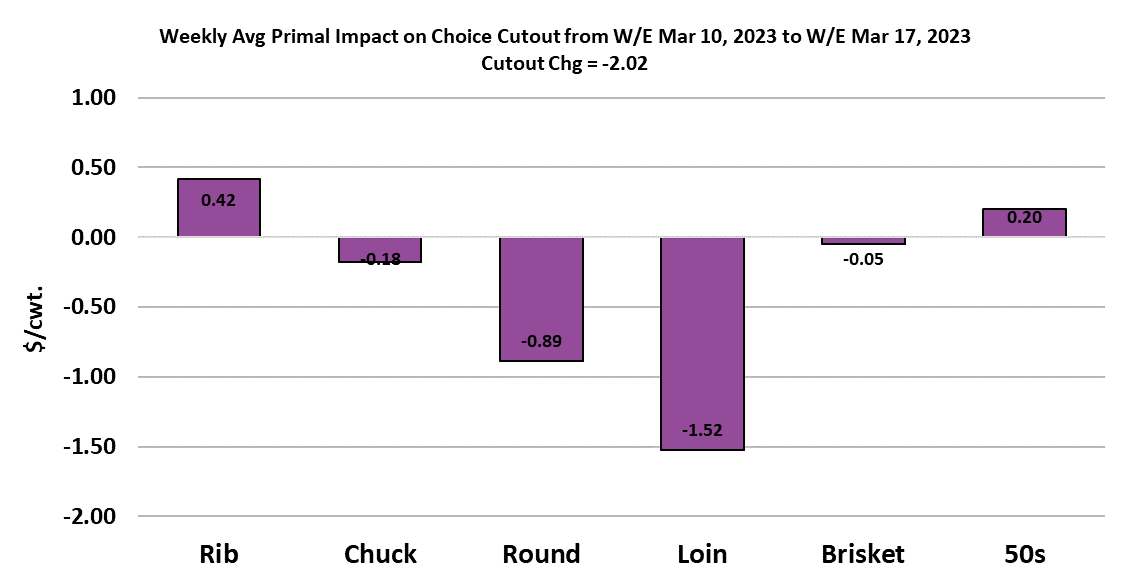

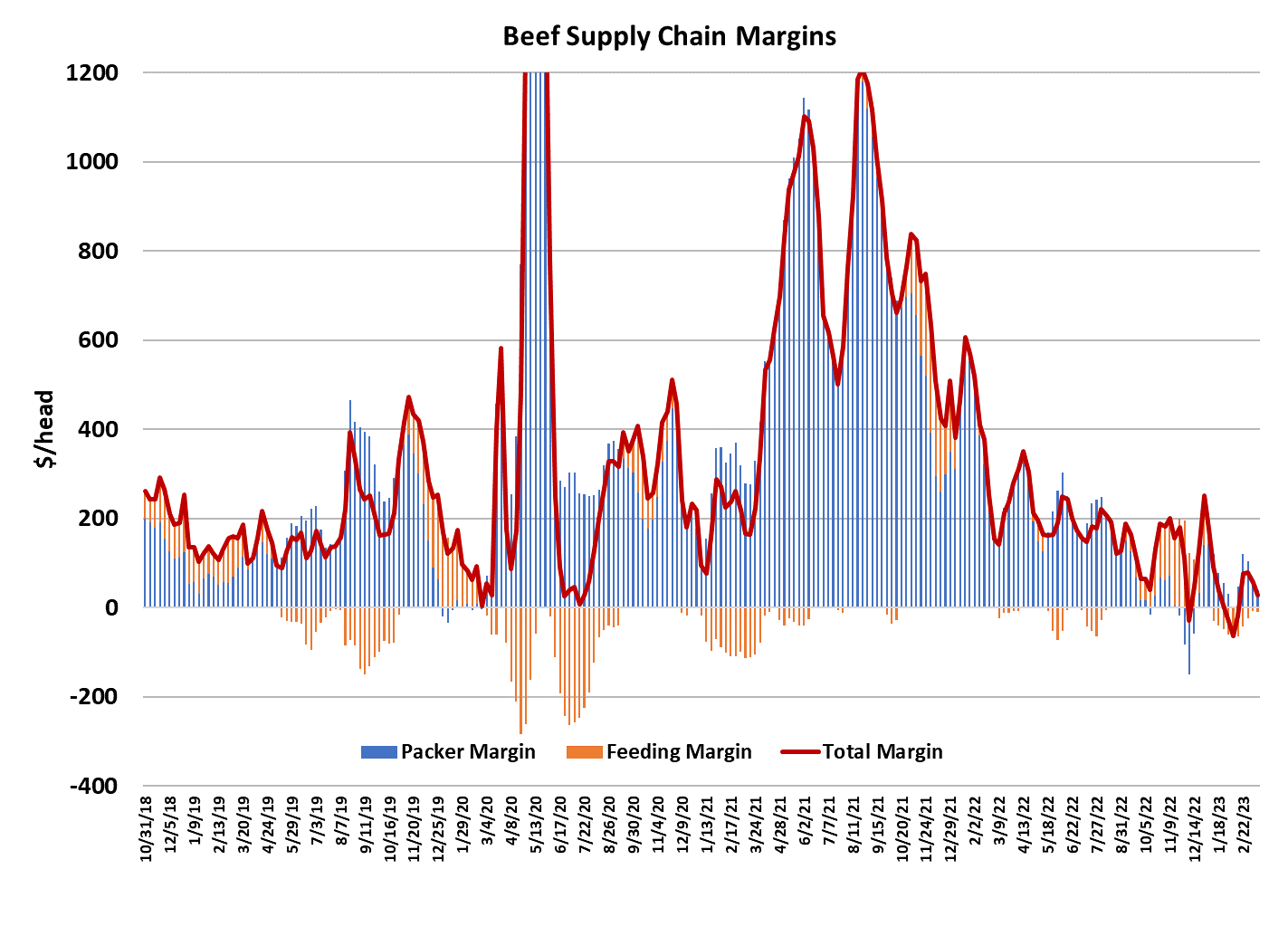

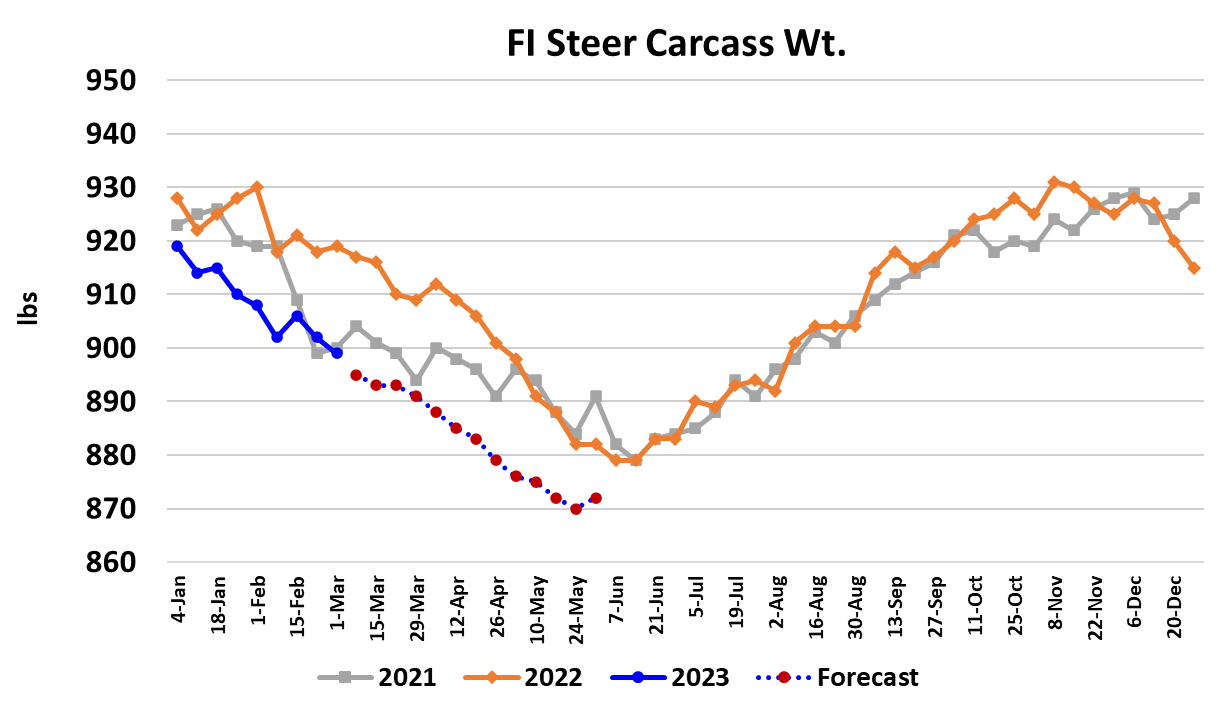

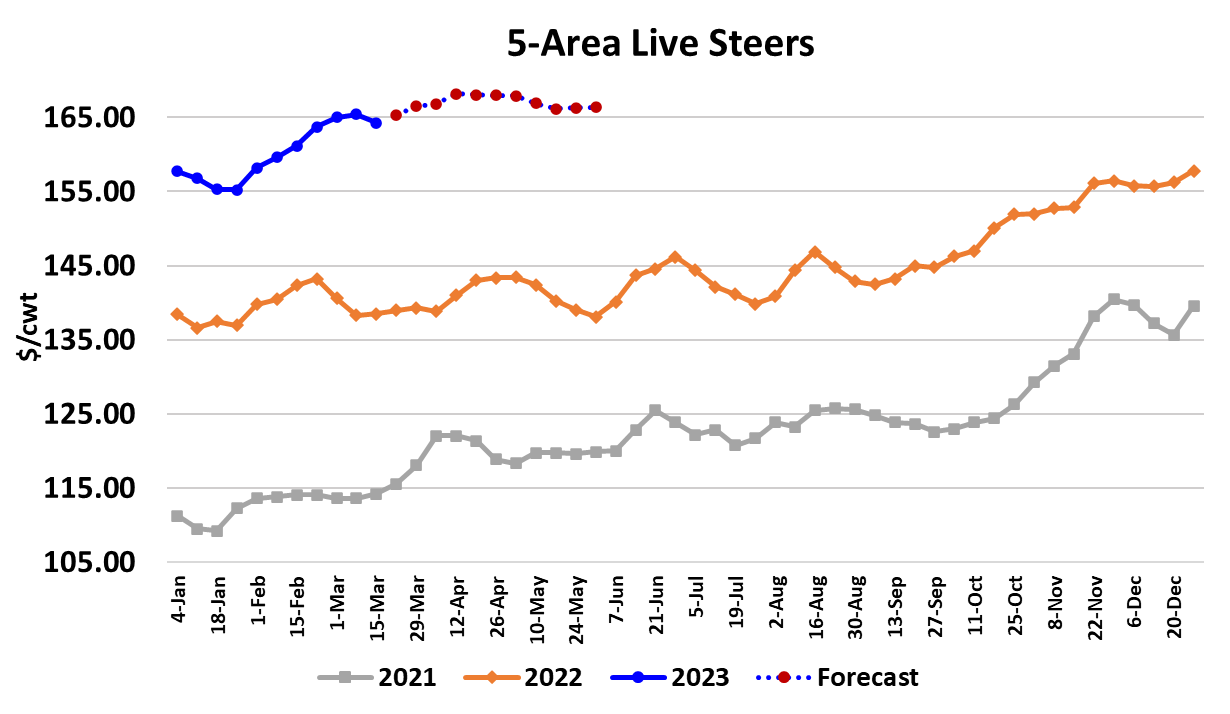

Turmoil in the outside markets had a big influence on the cattle and beef complex this week. Reports of bank failures and other banking problems drove the equity market down hard this week and that quickly spilled over into the cattle futures and then the cash cattle market. Anytime that it starts to look like the economy might struggle, market participants worry about the impact on beef demand and that usually leads to a sell-off. For the week, the first four cattle futures contracts each lost close to $2. That prompted cattle feeders who were holding short futures hedges to quickly hit the bid in the cash cattle market and then lift the profitable hedge. It didn’t take long for that initial selling to spread to all regions and by Wednesday the bulk of the cash cattle trade was done. That is in contrast to when the cash market was rising and week after week the cash trade waited until late on Friday. It looks like the average live price this week was close to $164.20/cwt, down about $1.20 from last week’s average. In the beef markets, the Choice cutout lost $2.02/cwt on a weekly average basis and the Select cutout was down $2.93/cwt. Packer margins compressed down to about $40/head from $65/head the week before. The gains and losses were a mixed bag, with the rib primal up slightly, but the loin primal down the most. The end meats were also down on the week. It is likely that some beef buyers that didn’t have immediate needs probably backed away for a few days to see how the financial market unrest was going to shake out. If there are no more surprises to come from the banking community then perhaps those beef buyers will be back in the market next week. After all, the weather is starting to warm in the southern tier states and that means consumers will soon be breaking out their grills. I’m not looking for much more downside risk in the cutout from here. Maybe down just a little more next week, but then I’d look for the cutouts to start tracking higher again. That should give packers better margins and of course cattle feeders will want their share. I have breakevens on cattle leaving the yards today at about $165/cwt, so not very far off where the cash traded this week. However, breaking even doesn’t pay the bills—profits do. So cattle feeders will be looking to return cash cattle prices to an upward trajectory next week. I’m relatively optimistic for their success since available cattle supplies will remain tight for another 6-8 weeks. Right now, I’m forecasting the Choice cutout to top around $292 in mid-May and the cash cattle market to perhaps peak at $168 in mid-April. Much will depend on the strength of consumer demand. Pork demand seems to be struggling mightily these days and I’m a bit apprehensive that could spill over into the beef market. Further, the combined margin is now tracking lower again, so we could see demand continue to weaken. So, if I’m wrong on the cattle and beef forecasts, I’m probably too high. This week’s fed cattle slaughter totaled 494k, same as the week before and just a little over what the flow model suggested. Packers really pulled back on the Friday and Saturday kill, so that could signal that they have concerns about near-term demand or worries that kills any larger would result in cash cattle prices moving higher. The flow model suggest that fed kills should stay at or below 500k through March and April and into the first half of May. Those small kills are not a problem now, but when we get to May, packers will want to increase slaughter rates in order to capitalize on stronger margins. That probably means that some cattle killed in May will actually be “borrowed” from June. Carcass weights are still coming down pretty fast, with steer weights dropping three pounds this week and the forecast looking for another four-pound decrease next week. That will continue to limit production. FI beef production this week was 513 million pounds, down from 553 million pounds in the same week last year (-7.3%). For those hoping that beef availability will increase later this year, the signs are not very encouraging. Today’s Cattle on Feed report found that February feedyard placements were down 7.2% from last year. That is the sixth YOY decrease in a row now and there is a reasonably good chance that that streak could extend through the end of 2023 and into next year. As of March 1, the nation’s feedyards hold 4.5% less cattle than they did last year at this time. So the takeaway is that the supply side will remain bullish for prices for the foreseeable future. Demand is less easily discerned and it is possible that the US economy will sink into a recession later this year and the resulting softening in beef demand might offset at least part of the price advance that might arise from tighter supplies. Winter weather continues to track across the northern feeding regions and thus limit cattle performance, but soon that risk will be off of the table. Right now, it looks like the biggest risk comes from the uncertainty in outside financial markets. If that gets worse, then it would be reasonable to look for cattle and beef prices to remain on the defensive. However, if those markets stabilize in the coming days and weeks then it is reasonable to expect buyer confidence to improve and prices to get back on the upward trajectory they were on before mess in the financial markets began. Next week, look for a steady cash cattle market and slightly weaker beef markets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}