Beef Wrap June 10

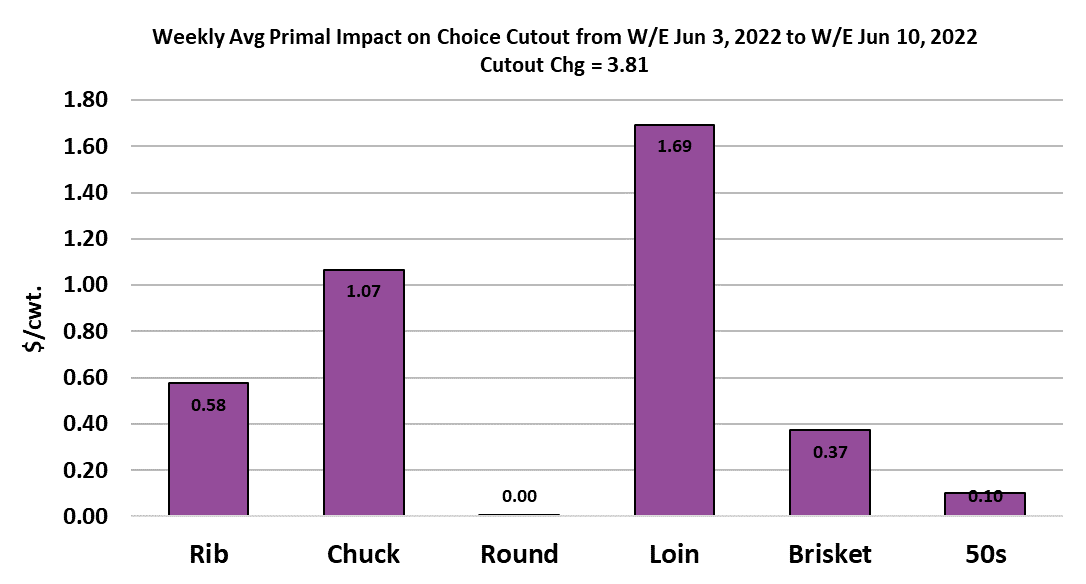

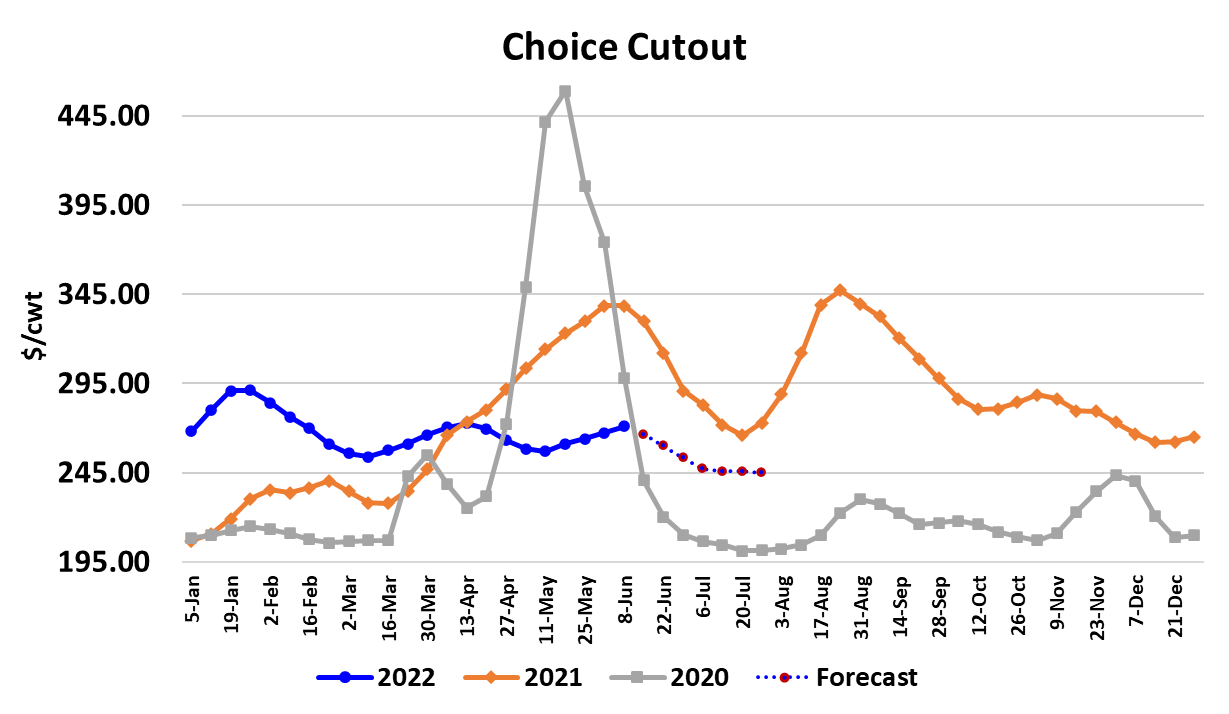

The beef cutouts continued higher this week, with the Choice gaining

$3.81/cwt and the Select up $0.41. The cutouts started to struggle

some near the end of the week and that makes me think that the early

week gains were at least partly a function of the short kill the week

before. The gains were spread pretty much across the carcass

which also supports the idea that the short kill had a hand in this

week’s gains. Cash cattle posted a surprising turn around, averaging

$140.50, which was up about $1.50 from the week before. It is not

clear to me why cattle feeders were suddenly able to extract higher

money from packers after prices moved lower in each of the past 4

weeks. Some of it might be attributable to the way cattle have been

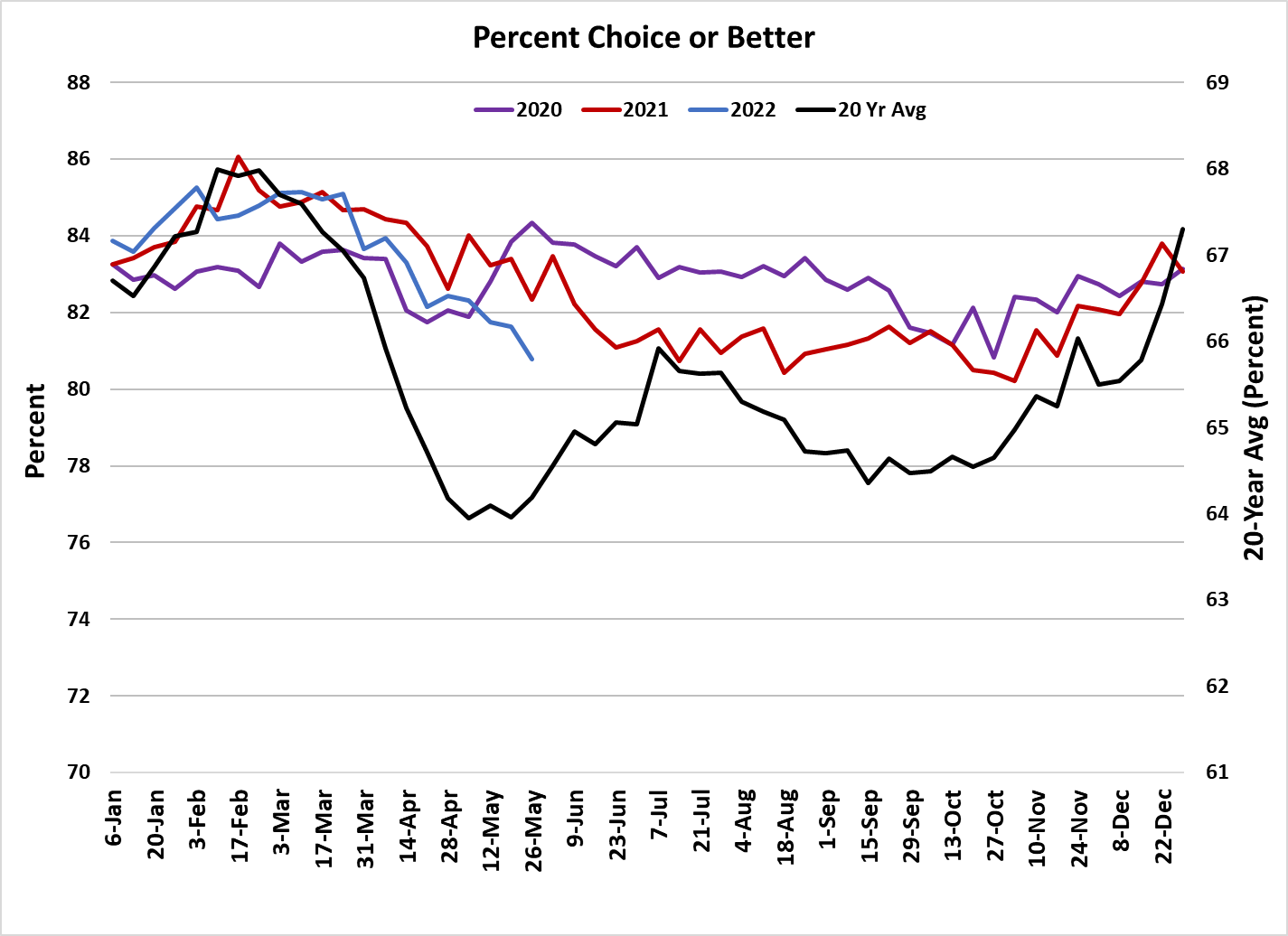

grading lately. The attached chart shows the percentage of beef

grading Choice or higher has fallen well below the levels seen in the

last couple of years.

At the same time, consumer demand for Choice product has been

increasing, so perhaps packers are having to reach more to find the

quantity of Choice-grading cattle they need and in some weeks that

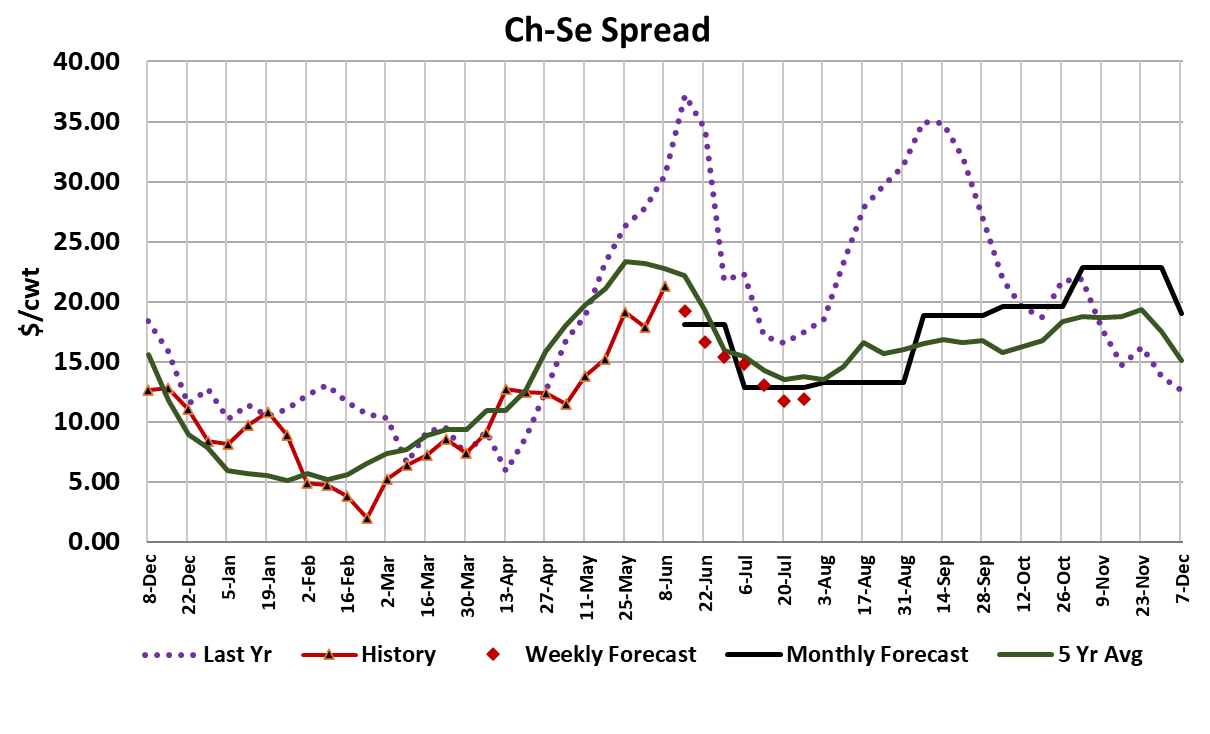

may require higher cash prices. The Choice-Select spread averaged

over $20 this week. There has been a lot of chatter from the cowboys

about how current feedyards are these days and perhaps that is also

a factor. Cattle carcass weights continue to decline well beyond

where I thought the bottom would be and the DTDS weights have

dropped like a rock over the past 4-5 weeks. Super-high corn pricing

is probably causing cattle feeders to try and get cattle marketed as

quickly as possible so that they can save some on the feed bill.

Packers have played into that hand by keeping kills relatively strong

over the past month or two. Still, the number of cattle on feed is

record large right now, so at some point I would expect cash cattle to

continue trending lower. Packers will feel a margin squeeze next

week when those more expensive cattle show up at the packing plant

and cutout values are likely to be declining.

I calculate this week’s packer margin at around $310/head, but it is

likely to fall back below $250/head next week. It appears that the

days of super lucrative packer margins are now behind us. By the

time that we get into the second half of July, packer margins could be

solidly below $200/head. I don’t think there is much risk of them

going negative this summer, but the $800+ margins that we saw in

the summers of 2020 and 2021 are clearly off the table. This week’s

fed kill came in close to expectations at 529k, up 50k from the

previous week’s holiday shortened kill. I think we can expect a

steady stream of fed kills in the 520-530k range for the next couple of

months. That isn’t a big problem right now when lingering holiday

demand from Memorial Day, Father’s Day and Independence Day is

boosting consumption, but the seasonal suggests that demand will

suffer beyond the first of July.

The combined margin moved higher again this week, indicating that

we are still in the upcycle phase of demand but I expect that we will

see the combined margin turn lower within 2-3 weeks and it could

actually happen next week. All of the demand headwinds that I’ve

discussed previously: inflation, lack of stimulus, pandemic fading,

declining equity markets, remain in place. In fact, equity markets

took another dive toward the end of this week and it is looking like

there may be a lot more downside there. When consumers see their

stock portfolios losing money week after week, they feel poorer and

reflect that in their purchasing habits. The University of Michigan

consumer confidence index was released today and it dropped to its

lowest level since the series began back in the 1950s.

That is not the type of environment that would encourage robust beef

demand. So the demand story remains the same: we are in a brief

seasonal upcycle right now, but the longer-term trend towards softer

demand remains in place and will probably carry through the end of

this year, if not beyond. It doesn’t look like futures traders want to

hear that however, because they added more premium back into the

deferred contracts this week. Maybe they aren’t thinking too hard

about demand and are just focused on an eventual tightening of the

cattle supply. That could be a huge mistake because often demand

turns out to be a bigger price determinant than supply. And even so,

there is nothing bullish about the supply side for the remainder of

2022.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}