Beef Wrap July 29

The cash cattle market averaged almost $2 lower this week at

close to $139, with trades in the South as low as $135 and prices in

the North falling mostly in the $141-142 range. The cutouts were

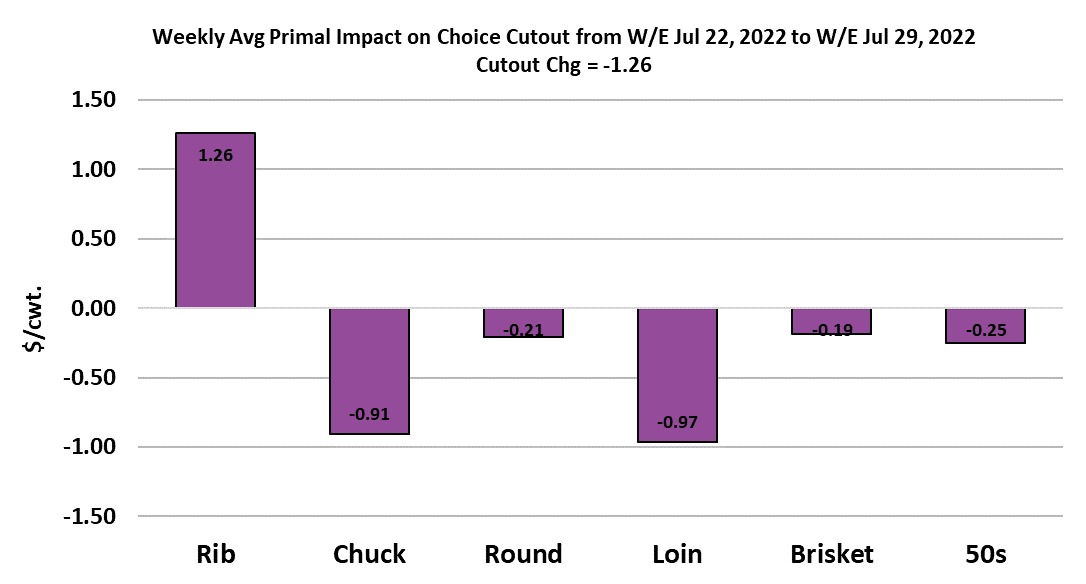

also slightly lower, with the Choice dropping $1.26/cwt on the week

and the Select down $0.42/cwt. The beef trade was a choppy mix,

with price strength evident at the beginning and end of the week,

but softer during the middle of the week. This week the ribs

provided most of the cutout’s support, while the other primals all

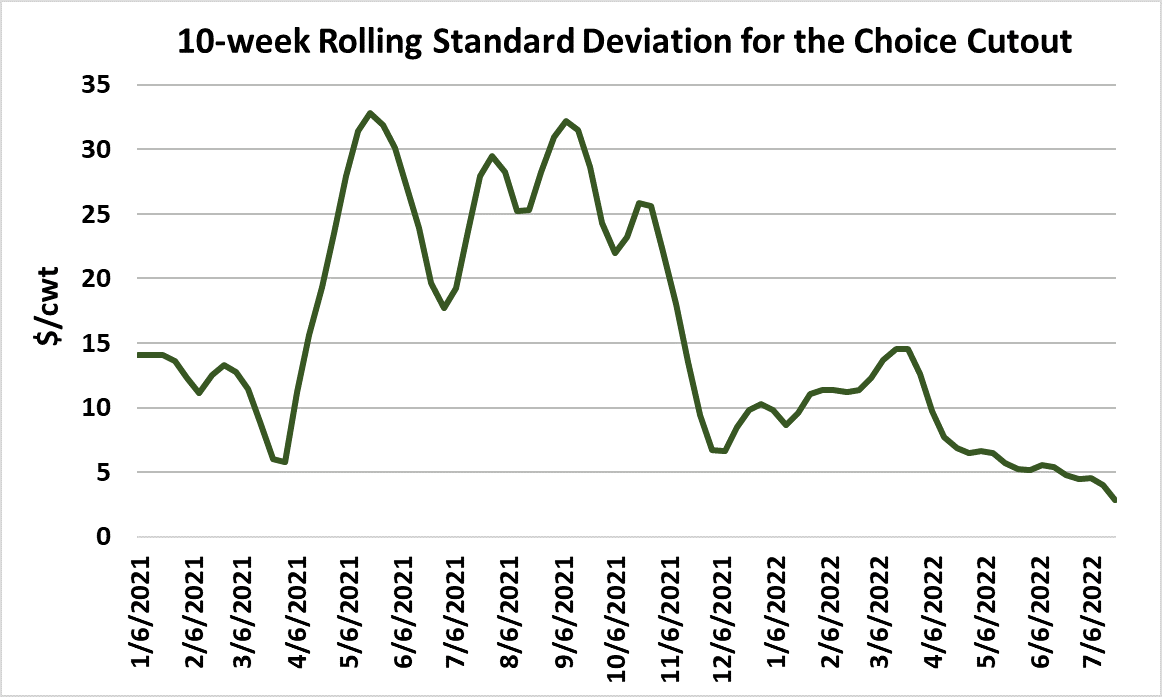

sank a little lower. One thing that I have noticed over the past few

months is that the volatility in the beef cutout has been very low.

The attached chart gives the 10-week rolling standard deviation for

the Choice cutout value since the beginning of last year. Since

about mid-March of 2022, this measure of volatility has been in

steady decline and now is at its lowest level in years.

The cutout just doesn’t seem to move much anymore. If we go

back to the middle of March, the Choice cutout averaged $266/cwt

and this week it averaged a little over $268/cwt. The highest

weekly average recorded during that stretch was $272 and the

lowest was $257. That amounts to 18 weeks where the cutout has

traded in a very narrow range. Are packers doing something

differently that has stabilized the cutout? Possibly, but I’m not sure

what that would be. If the cutout doesn’t move much, then that

suggests that cash cattle prices don’t really need to move much,

which could be one reason why open interest in live cattle futures

has dropped so much over the past couple of months. Speculators

thrive on volatility and when they can’t find it in one market, they will

switch to another. Further, the other market participants, hedgers,

don’t feel an urgency to take on hedge positions whenever prices

aren’t moving much.

It is also worth noting that retail beef prices haven’t moved much

since March either. I’m not really sure what to make of this, but it

does make me wonder if I’m going to get burned by forecasting the

Choice cutout down to $245 this fall. Maybe it will just stay in its

$255-270 range. In order to get down to a $245 Choice cutout by

October, it will be necessary to see some demand softening. The

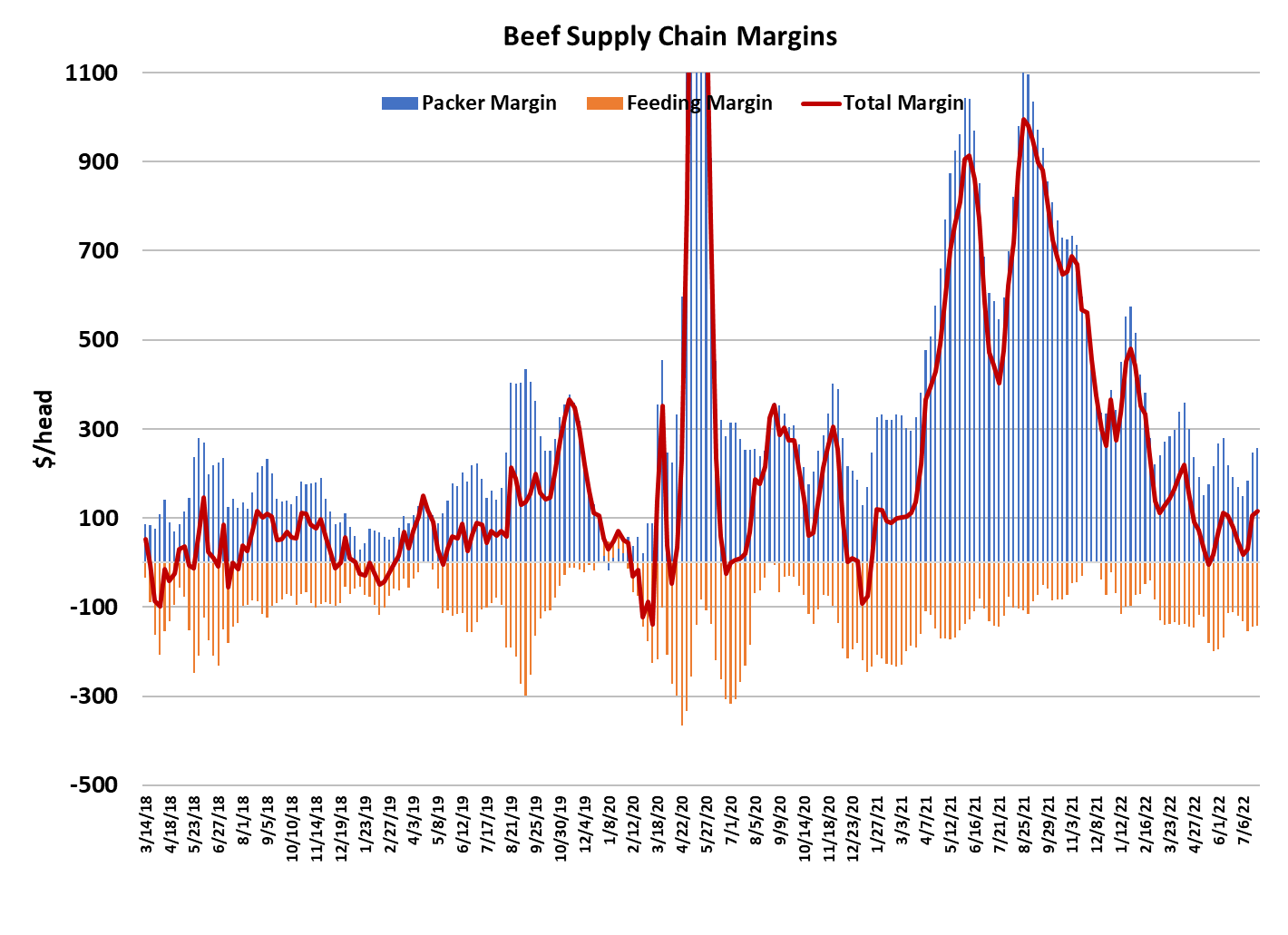

combined margin continued upward this week, but at a little slower

pace than in previous weeks. Perhaps it is ready to make a top and

turn lower. That would likely push cutout values down unless

packers cut the kill to compensate for softer demand. It is likely that

we will see some middle meat interest during the middle of August

as retailers prep for Labor Day. We may also see interest in end

meats and grinds from institutional buyers as US schools start to

re-open during August.

I have to balance those normal seasonal factors against the rather

bleak macro picture where inflation is still raging and the economy

appears to be cooling. It’s not surprising that US consumers kept

spending during the summer of 2022 since they were very eager

to travel and do things that the pandemic hindered. But now we

are moving into the waning weeks of summer and demand

continues to be strong. On the supply side of the market, this

week’s steer and heifer slaughter came in at 521k, which was a

little below the 530k that the flow model projected. This marks the

third week in a row where packers under-killed our model and that

may be playing a role in their ability to keep stepping cattle prices

lower each week.

Past placement patterns suggest that there should be sufficient

cattle available in August for 530k weekly fed kills, but whether or

not packers will keep slaughter that high is an open question.

There is more brutally hot weather in the forecast for cattle

country in the next couple of weeks and that has the potential to

slow weight gains some and perhaps slow down the loss of

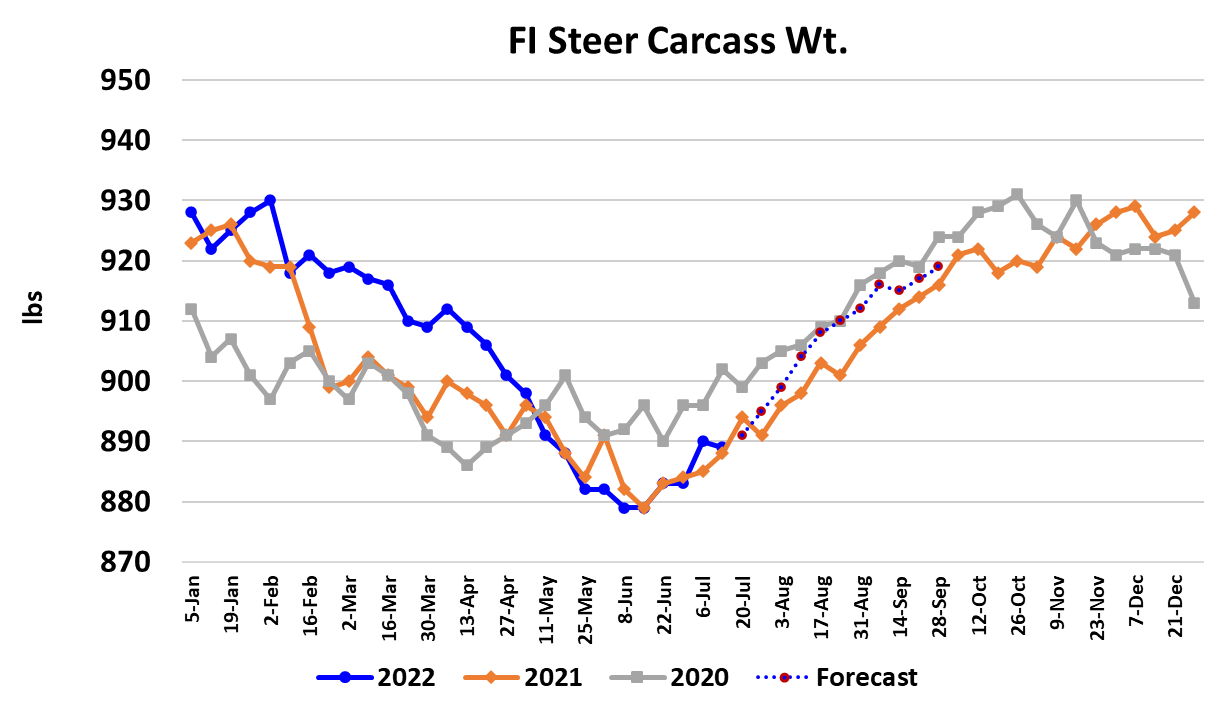

leverage by cattle feeders. Steer carcass weights were reported

down one pound this week and are now almost dead-on with last

year’s level. The seasonal uptrend in weights is expected to

continue unabated by the hot weather that is coming. Corn

prices are on the rebound now and that might help to temper

weight gains, but won’t be enough to disrupt the seasonal pattern.

For the first half of 2022, placements were almost equal to the first

six months of 2021 (actually 0.2% higher).

That seems somewhat odd for a herd that has been getting

smaller every year since 2019. It also suggests that placements

in the second half of 2022 will need to be below last year in

aggregate. Mother Nature will have a lot to say about that

though. If the drought persists in grazing areas, we will likely

continue to see a lot of feeder cattle pushed into feedyards

because there is insufficient forage for them. The beef export

data continues to look good, keeping pace with last year and still

registering strong Chinese interest in US beef. Next week, look

for some softening in middle meat prices to take a few more

dollars off of the cutouts. Cash cattle prices should also continue

to soften due to fed kills failing to meet expectations over the past

few weeks. It looks like the price action in the cattle and beef

complex has the potential to be rather boring for the next few

weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}