Beef Wrap August 12

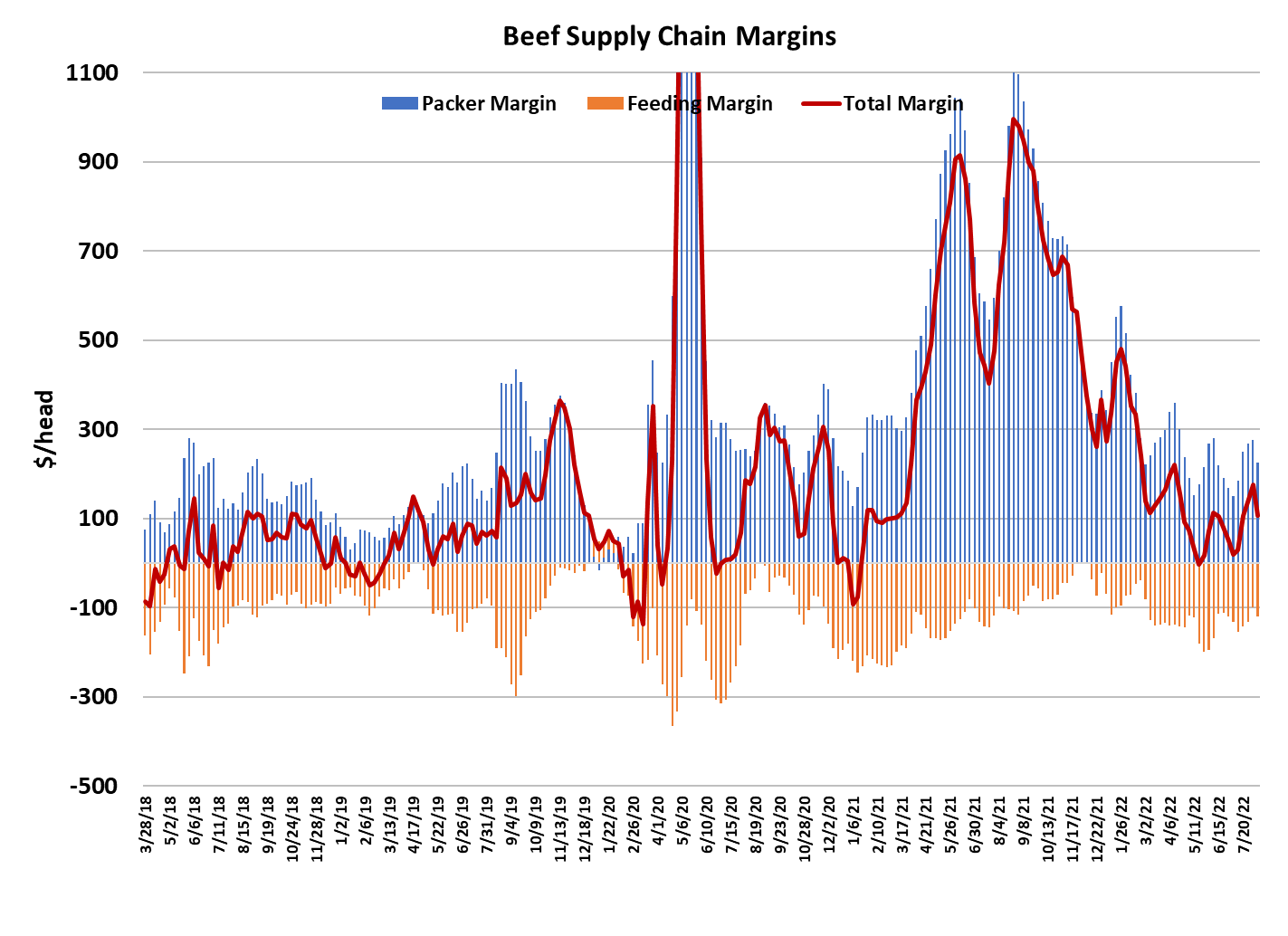

This was a week for compressing packer margins as the cutouts slid

lower and cash cattle prices surged higher. The Choice cutout lost

$3.34/cwt on a weekly average basis and the Select was down $2.82/

cwt. The cash cattle market, on the other hand, was on fire this week

with the weekly average price up $3.50/cwt from last week to

$144.34. When those more expensive cattle show up for slaughter

next week, packers will likely be merchandising the beef at prices

lower than this week and we could easily see margins fall below $180/

head. Packer margins seem to have normalized since the beginning

of May into a range between $150/cwt and $300/cwt. Even though

packers would probably consider the $150 margin to be tight, it is still

well above typical margins prior to the August, 2019 Tyson plant fire.

However, with the US cattle herd shrinking now at a pretty fast clip,

packers will find that, over the next couple of years, slaughter capacity

outstrips the available supply of cattle and that will mean further

margin compression.

At some point, it may even be necessary for packers to mothball a

plant or two in order to better align production capacity with the

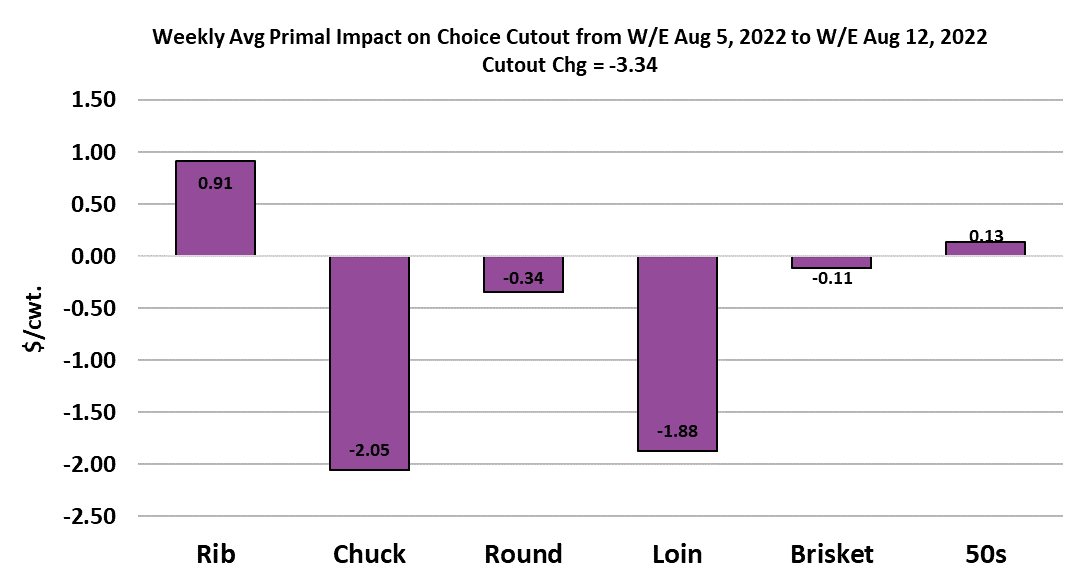

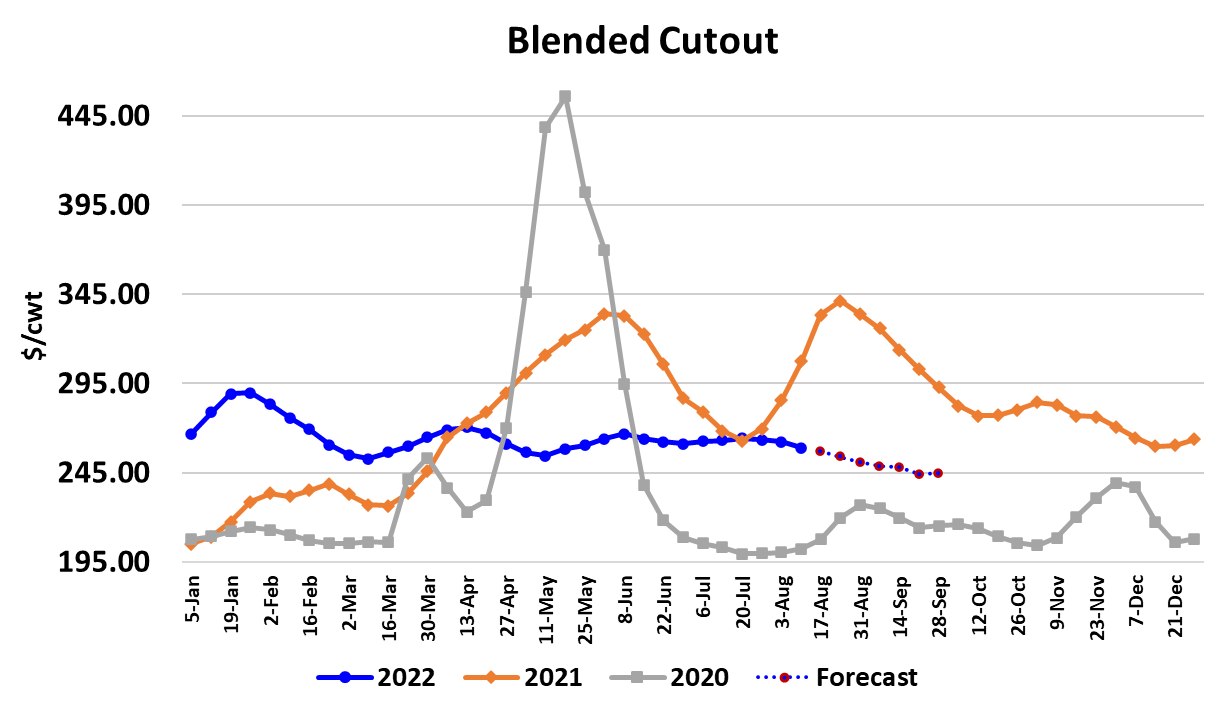

available supply of cattle. The attached chart indicates that the ribs

and fat trim provided a little support to the cutout this week, but all of

the other primals pulled lower on the cutout. The combined margin

has now turned decidedly lower and that suggests that a new demand

downcycle has finally begun. The last upcycle came in a little

stronger than I thought it would and it is possible that the current

downcycle might not be as deep as I had originally envisioned. I’ve

discussed before the amazing stability in the cutout since mid-March

where the Choice has traded in a narrow $15 range between $255 on

the low side and $270 on the high side. It is almost as though most of

the normal price seasonality has been removed. Certainly, the

amplitude of the demand cycles has been diminished from what we

saw in 2021.

I am still expecting consumer demand to fade because there are a

number of macroeconomic headwinds that consumers will be dealing

with in the coming months, but I have to admit that demand has held

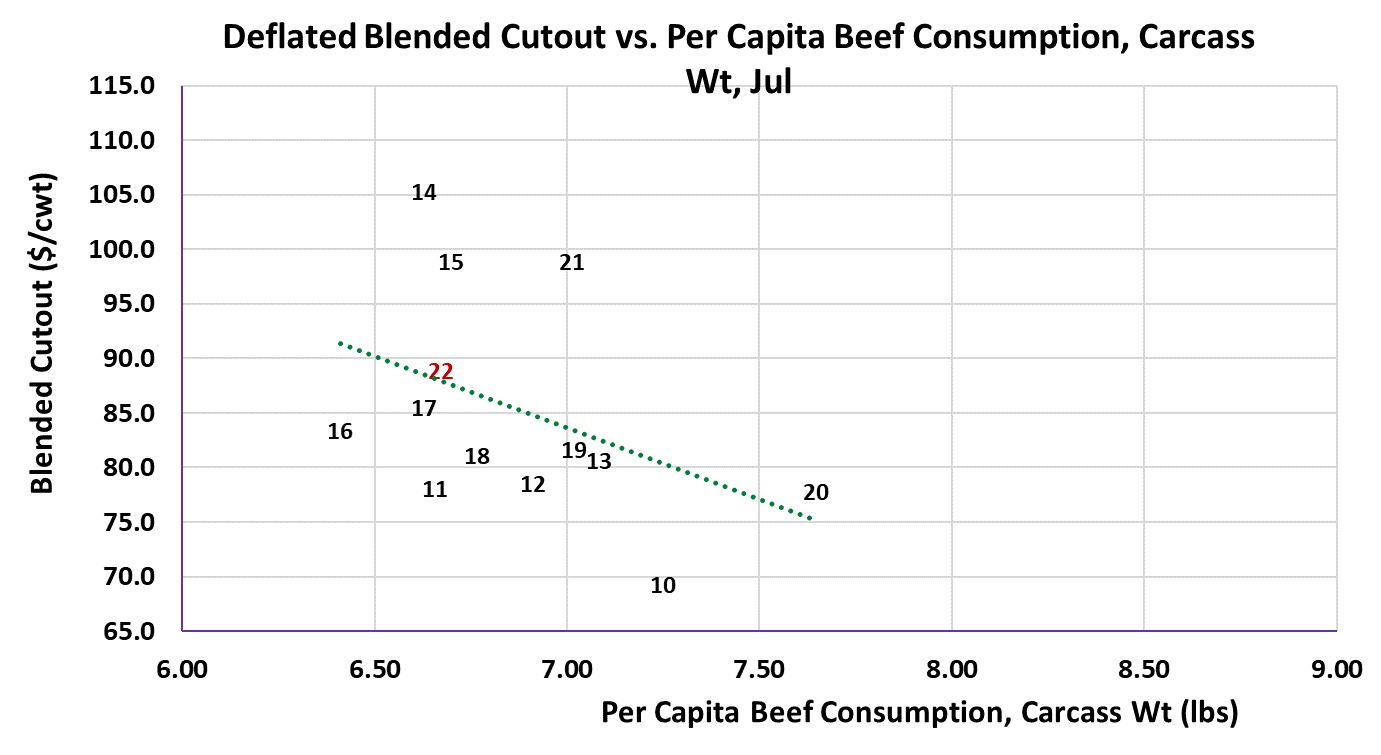

up better than expected this summer. Or has it? The attached scatter

diagram gives the deflated blended cutout verses per capita income

for the month of July. In this scatter, I’ve deflated the cutout using the

Consumer Price Index. The huge demand surge from 2021 is

evident, but the data point for 2022 is coming in much closer to the

regression line, which represents the average level of demand during

July since 2010. For years, analysts haven’t had to worry much about

price inflation in the general economy, but in the past couple of years

it has become a bigger concern. We may be forced to deflate our

price series going forward in order to avoid getting the wrong signals.

That is just something to keep in mind as we think about beef demand

going forward from here.

On the supply side of the market, this week’s steer and heifer

slaughter was estimated at just 505k, with packers doing a lighterthan-expected Saturday kill. That is well below the 520-530k per

week that the flow model suggests should be available to kill right

now. Perhaps packers are trying to boost their margins by throttling

back. Certainly, this week’s big increase in the cash cattle market

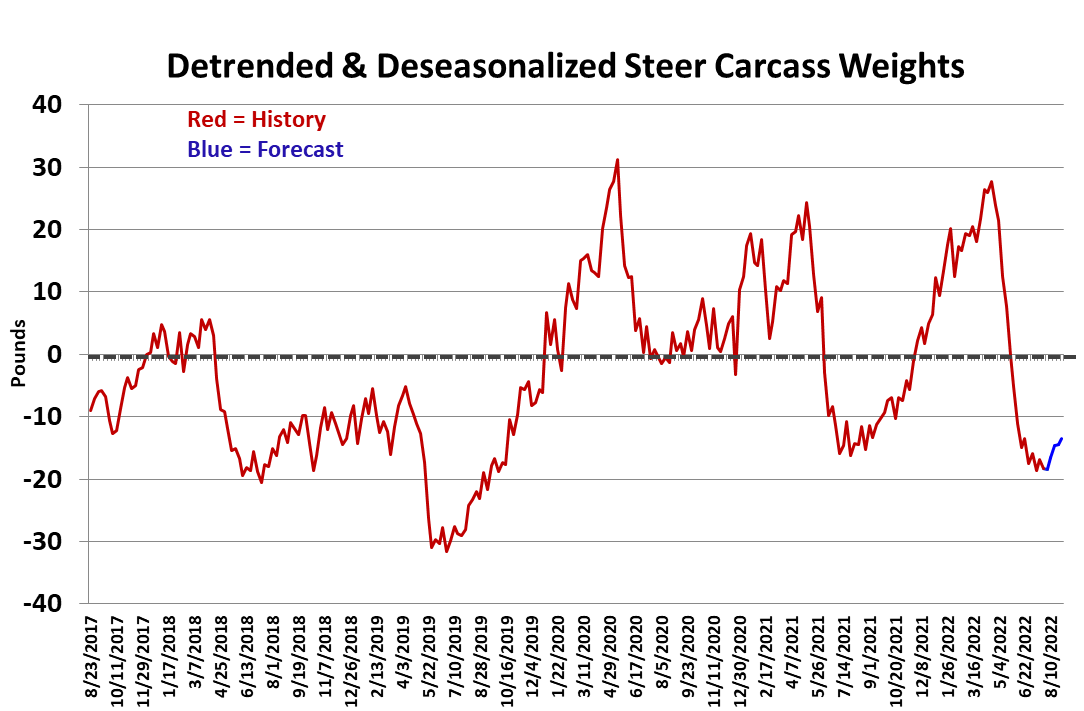

caught their attention. Steer weights came in only one pound higher

this week at 894 pounds and the DTDS weight barely budged. The

DTDS has stopped declining, but it isn’t rising much either. It is just

holding at a relatively low level which would indicate feedyards are

current and that might explain why cattle feeders were able to force

the cash market higher in a big way this week. I think packers will

have a difficult time cutting the kill further in the next couple of weeks

because that production will be needed to fill Labor Day orders.

They may just have to live with tighter margins for a few weeks. We

also need to be on alert for two short kill weeks coming up in the last

week of August and first week of September due to the Labor Day

holiday. For the remainder of September, the flow model suggests

there should be enough cattle to support fed kills near 530k per

week. The way things are going now, it doesn’t appear that kills will

get that large and thus it raises the risk of cattle getting backed up in

the pipeline. Cattle feeders have been paying some very high prices

for feeder cattle over the past few weeks and when they do that, they

often expect the finished animal will bring enough revenue to cover

those higher feeder cattle prices, even if the futures market is telling

them that won’t happen. They can dig in for a few weeks and force

the cash market higher but usually that tactic backfires and results in

a backlog of heavy cattle. We are a long way from that right now,

but it is something to keep an eye on this fall and carcass weights,

especially the DTDS, will be the leading indicator.

USDA released the trade data for June this week and it showed an

18% YOY increase in beef exports. Before getting too excited about

that, consider that the export total for May, 2021 was particularly

weak. In any case, beef exports appear to be healthy and we are

still seeing good interest from China. Exports are likely to remain

supportive over the next few months. Another piece of good news

for the bulls was that beef imports were down 15% from last year

and about 8% lower than the previous month. Stronger exports and

softer imports are helping to limit domestic availability. Next week,

watch the weight data. Carcass weights should be increasing about

3 pounds every week from now until November. If that doesn’t

materialize, then it means feedyards will have more leverage than

normal and will be supportive to cash cattle prices. Also watch the

cutouts to see if they get a bump from this week’s smaller

production. That can help provide some insight on demand.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}