Beef Wrap July 22

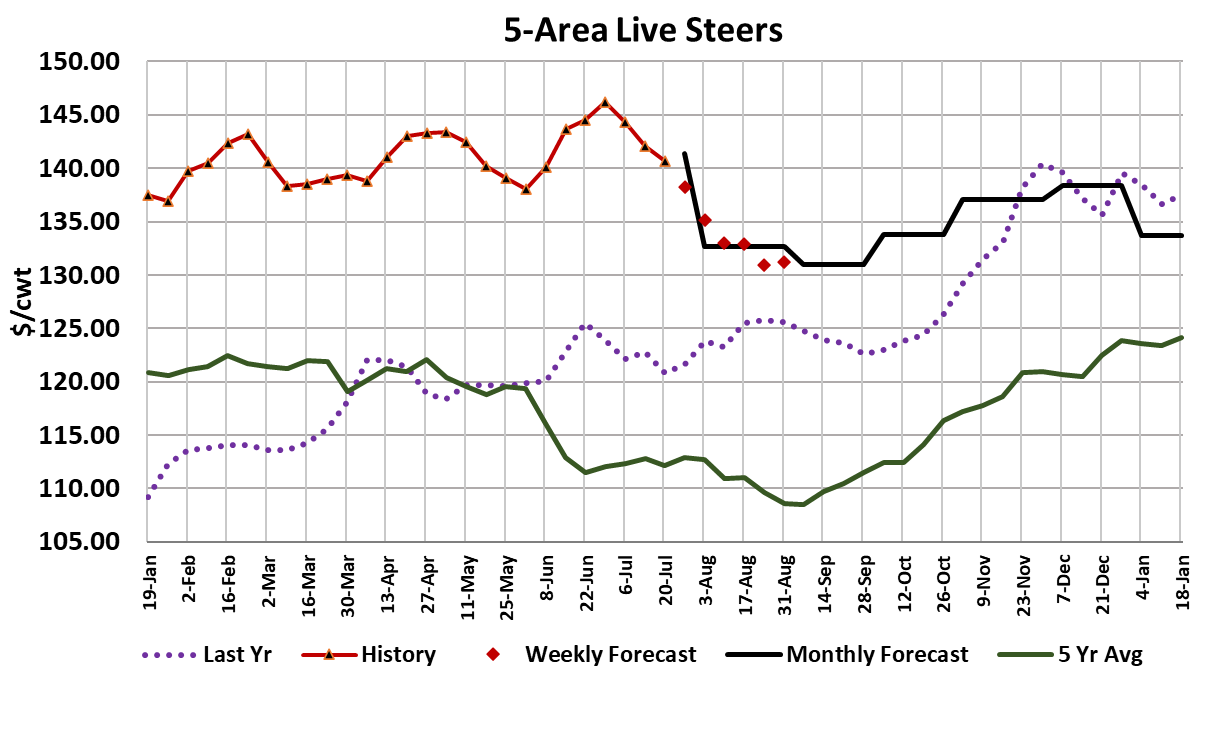

The cash cattle market continued lower this week, averaging

$140.65, which was about $1.50 below last week’s average. The

large premium that Northern cattle have been carrying over those in

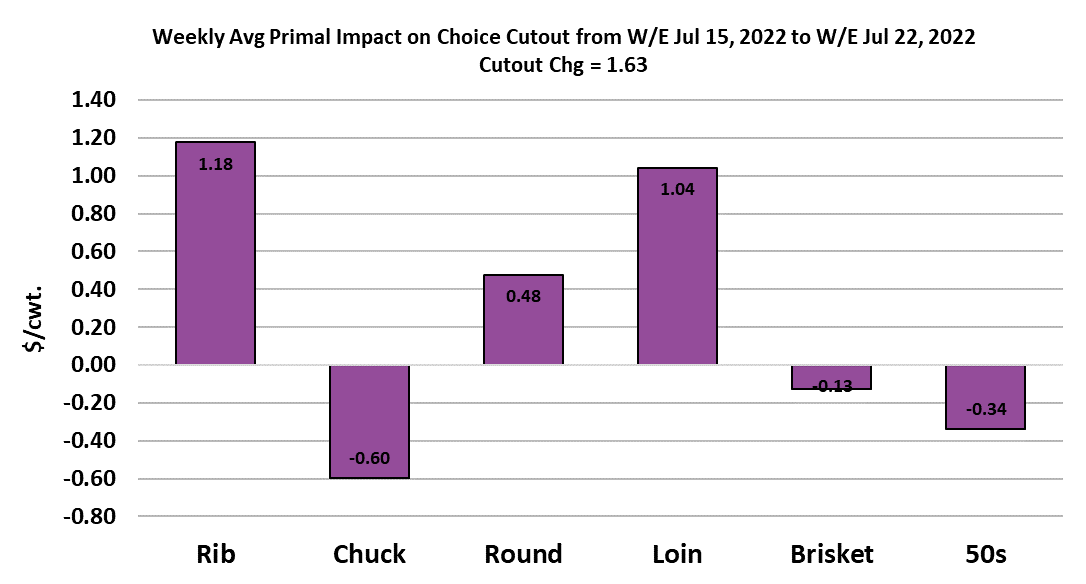

the South is starting to narrow. The cutouts were slightly higher

with the Choice gaining $1.63/cwt and the Select up $0.30/cwt on a

weekly average basis. Although the cutouts averaged a little higher

on the week, they started to exhibit some softening near the end of

the week that may carry over into next week. Middle meats were

the primary gainers this week, but those gains were rather small

and could easily reverse in the near term. Packers aren’t

displaying a lot of confidence in the cutouts since they seemed to

pull back on the kill near the end of the week. Steer and heifer

slaughter only totaled 522k, which was about 15k below what the

flow model projected. If they continue to under-kill for a couple

more weeks, it would likely put them in a much better margin

situation and help keep the cash cattle market trending lower.

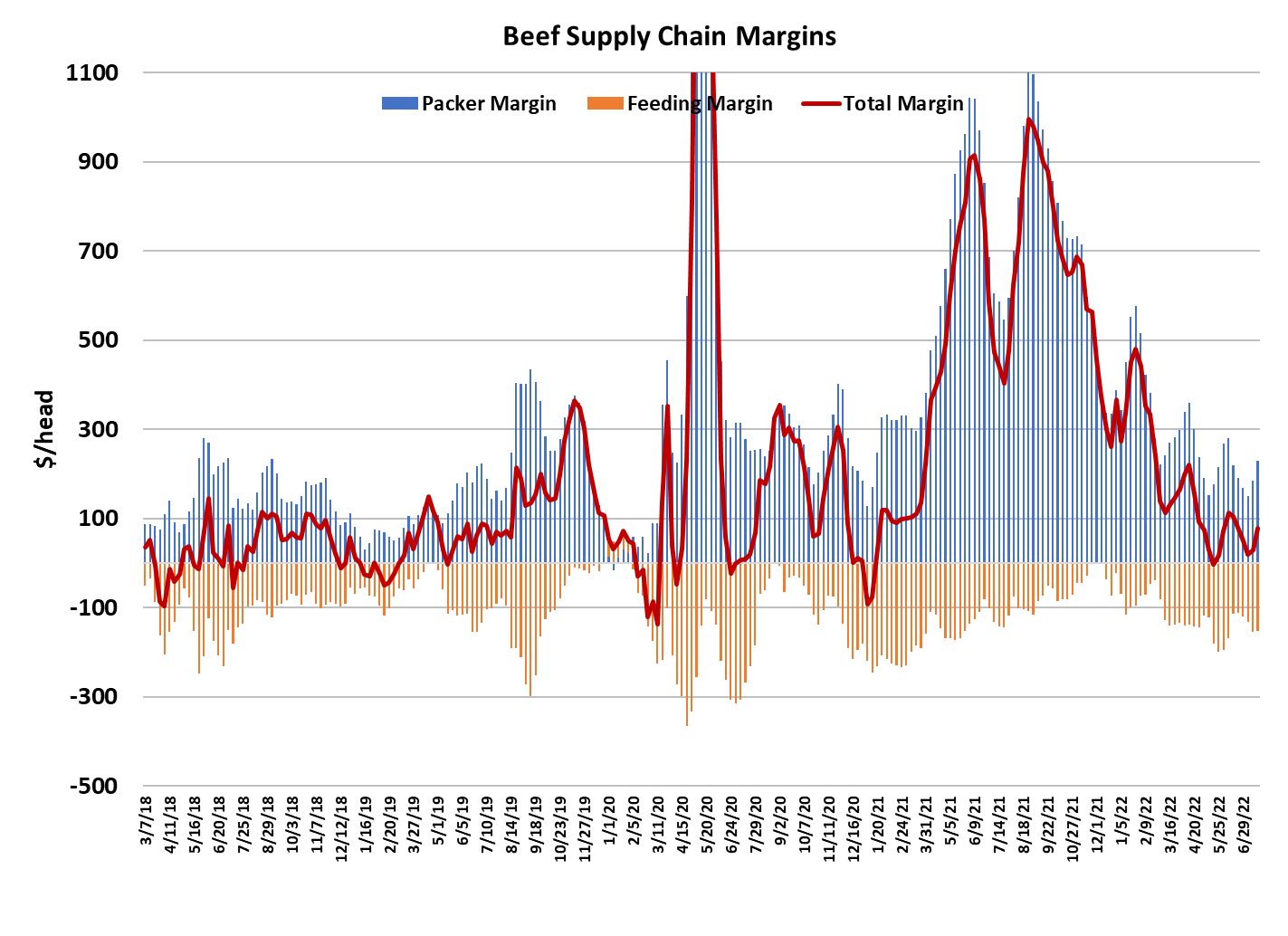

I calculate packer margins this week at $230/head, which is largely

the result of packers getting cattle bought cheaper last week. The

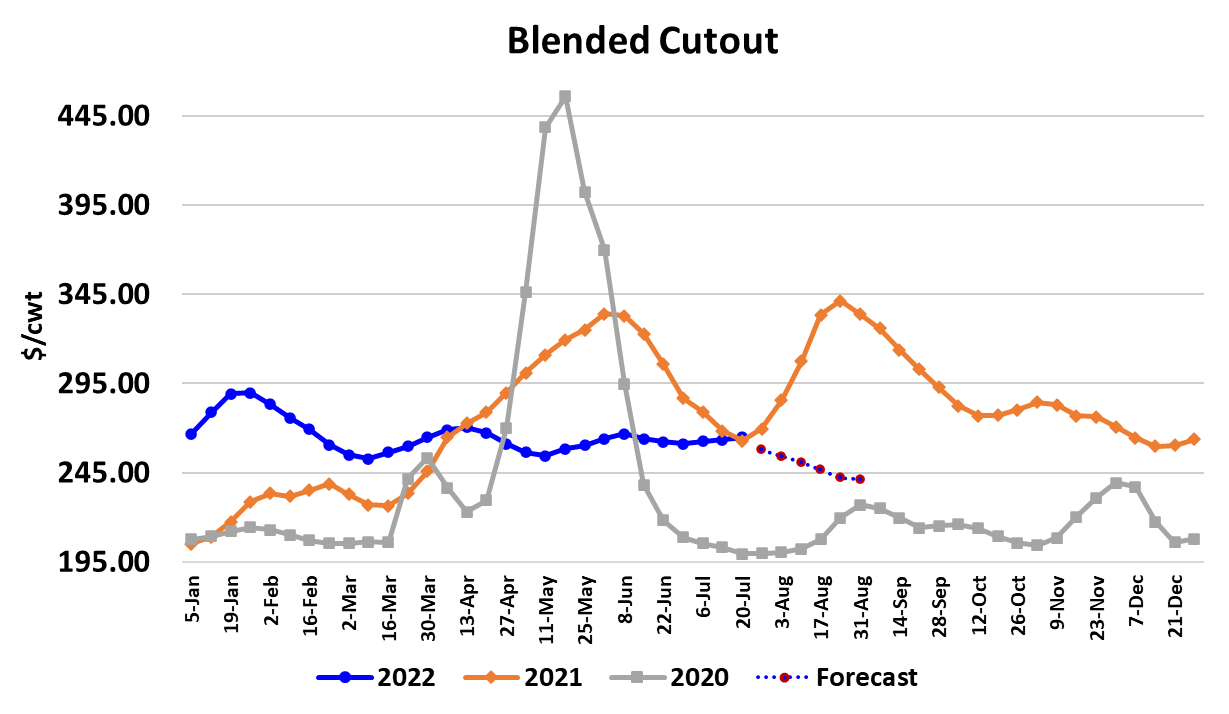

blended cutout has held in the $260-265 range now for over two

months and has been remarkably stable all year long. I suspect

that it will move lower through August and into September as macro

factors and high retail beef prices work to curtail consumption.

There is a lot of beef in the production pipeline and if off-take slows

just a little, it could cause a back-up. Retailers don’t seem to have

much interest in lowering the retail prices that consumers see and

who could blame them since wholesale prices (i.e., the cutouts)

have been remarkably stable. The combined margin chart has

shown a little uptick recently, but I’m not convinced that it is the

start of a new demand upcycle. I think it is going to turn out to be a

head-fake and soon the combined margin will be moving lower

once again.

There has been a lot of hot weather in the Southern Plains lately

and there is probably more to come, so that remains a risk to the

forecast. Cattle don’t eat as well when it is hot like this and thus

they don’t gain well either. Steer carcass weights were seven

pounds higher in the data that was released this week, but that data

was for the week of July 4, so that probably skewed weights toward

the heavy side. Still, carcass weights are now solidly in a seasonal

up trend that should last through October. Corn futures have fallen

dramatically in the last few weeks, with the Dec22 futures dropping

from a peak near $7.50/bushel back in early May to nearly $5.60/

bushel today.

That almost $2 drop could be huge for cattle feeding margins,

but most feeders are not seeing nearly that much benefit. Cash

corn remains very firm in the cattle feeding areas, with cash now

running $1.62/bushel over the futures in SW Kansas. Of course

now that the July corn futures have expired, corn is pricing off of

the new crop Sep futures. If the futures are correct about the

harvest being good, that would help to bring cash corn prices

down substantially once the new crop is harvested. The weather

has turned much more favorable for pollination in the Corn Belt

and that is what the big decline in the corn futures has been

about. USDA released its Cattle on Feed report today and it

showed placements during June down only 2.4% YOY. The

trade had been expecting a 5.3% decline. So, we have yet

another month where placements were stronger than expected

The mid-year cattle inventory report was also released today

and it showed the beef cow herd down 2.4% YOY, which was

less than the 2.8% decline that analysts were expecting. More

importantly, USDA estimated the 2022 calf crop to be down only

1.4%, not the 2% that the trade was looking for. So, both of

today’s reports were bearish from a supply perspective. Maybe

that will help quell some of the bullish enthusiasm that the

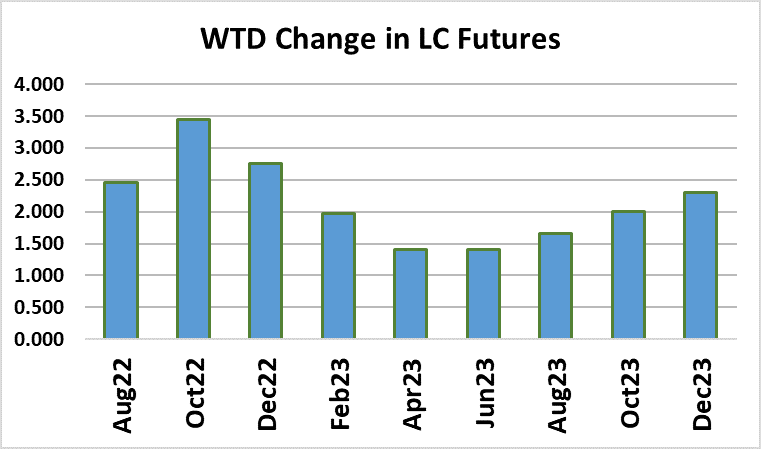

futures have been displaying lately. Oct futures gained almost

$3.50/cwt this week without much supportive fundamental news.

My guess is that traders will start working to remove some of

that next week. The focus will now shift to the cutouts and their

direction.

We are still in the dog days of summer and demand risk exists

over the next 5-6 weeks. USDA also released its Cold Storage

report today and that showed total beef in cold storage up 29%

YOY, but down about 2% from last month. Cold storage stocks

are not a very big price-influencing factor for beef. Next week, it

will be important to watch the kill for further signs that packers

are throttling back because they sense that demand is softening.

That would be bad news for the futures since any kill slowdown

could further accelerate the decline in cash cattle prices. It

would be a real feat if beef demand can hold steady or increase

between now and Labor Day, but I expect that soon the beef will

start to trend lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}