Beef Wrap July 29

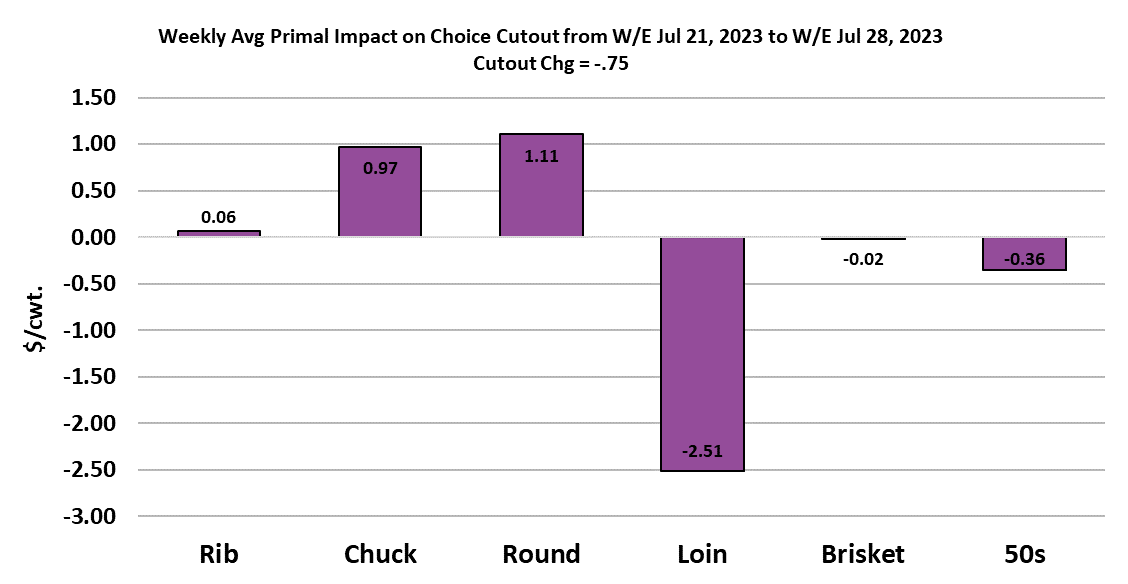

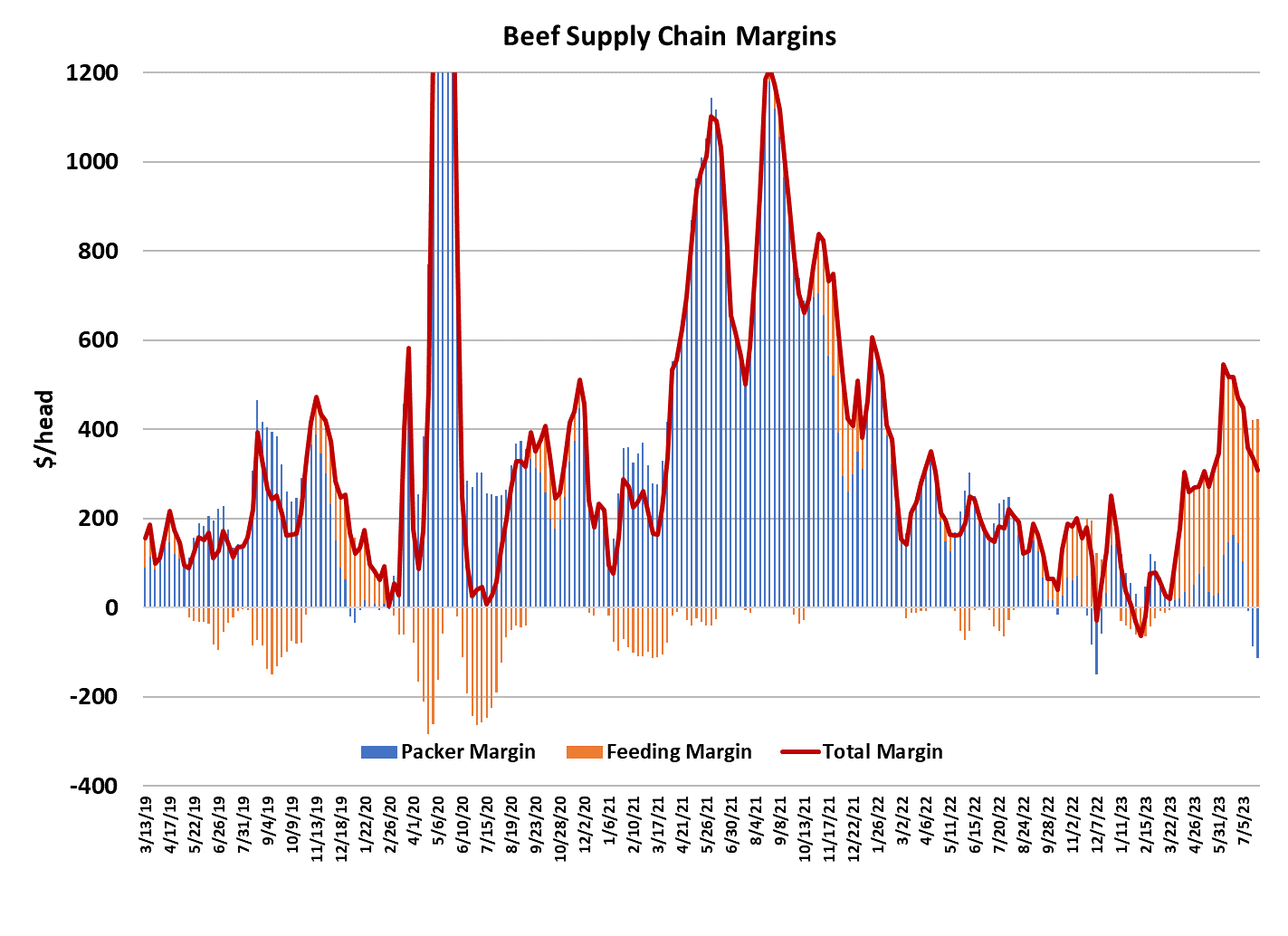

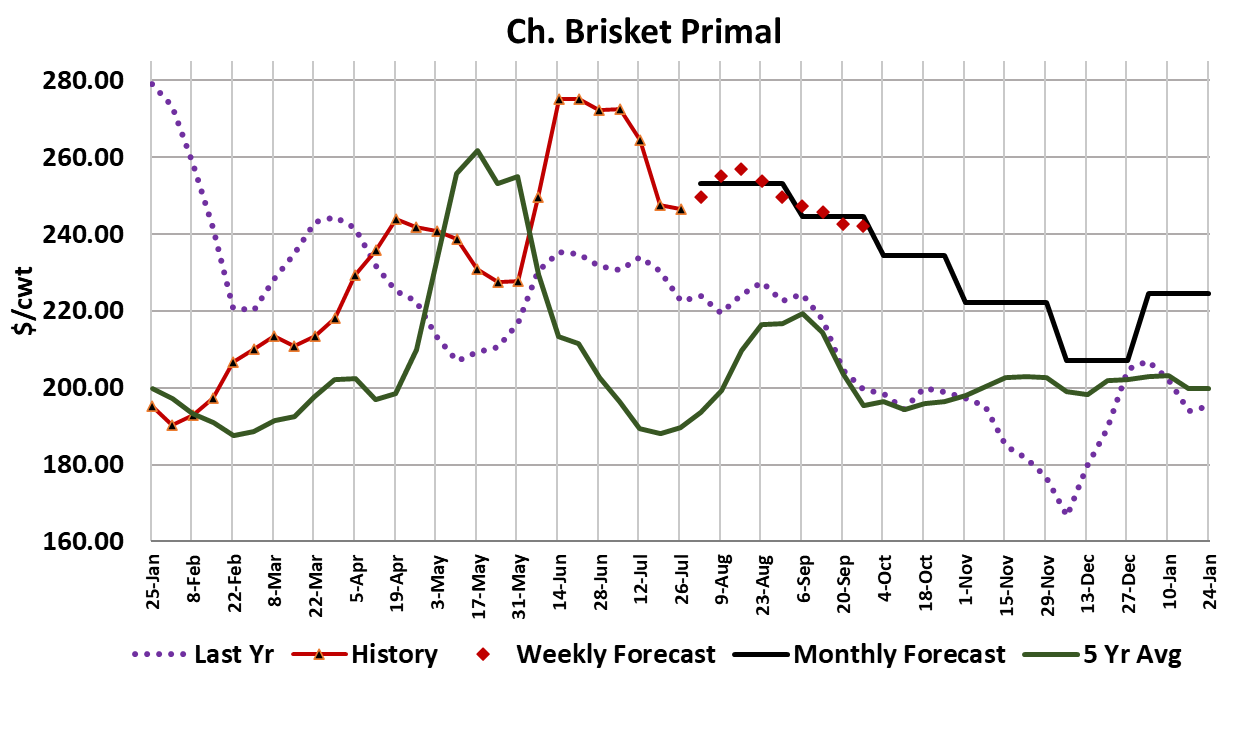

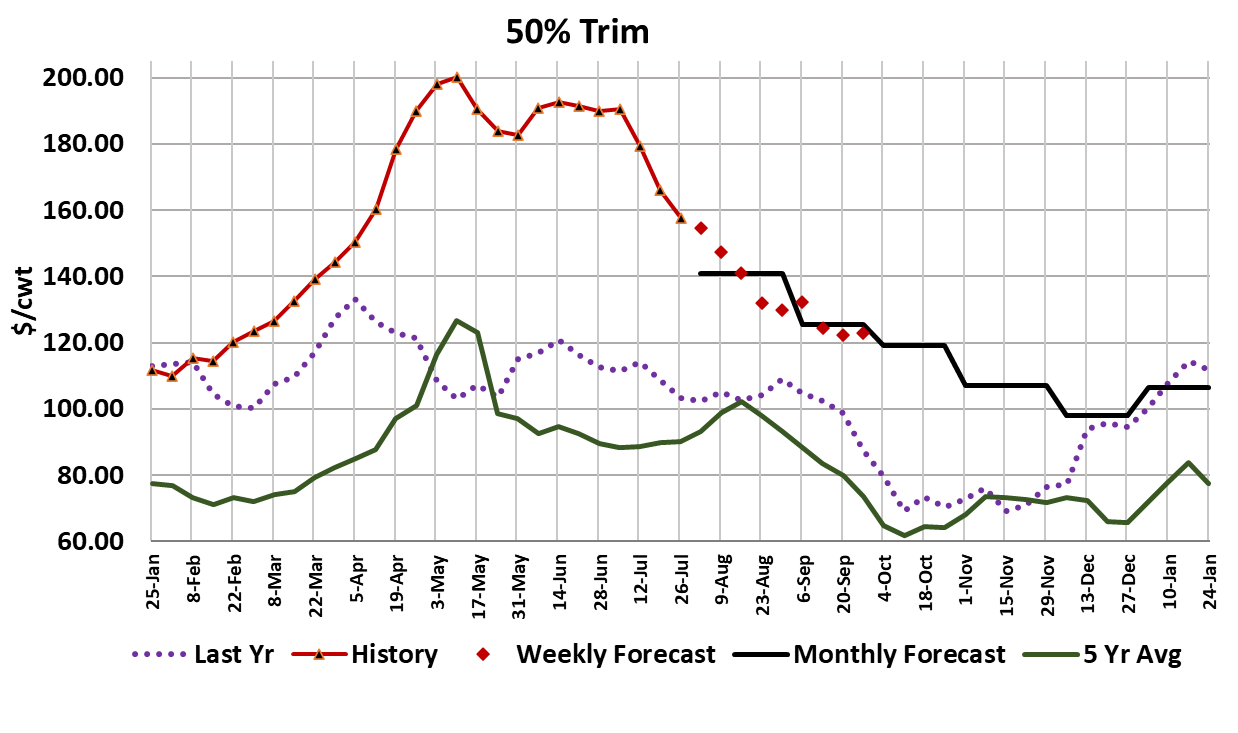

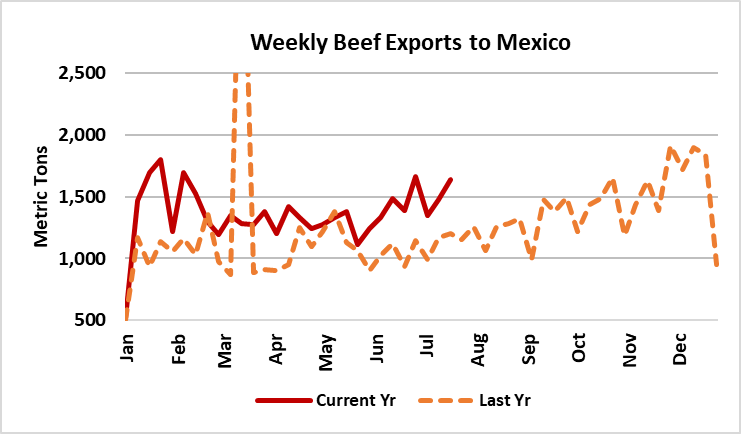

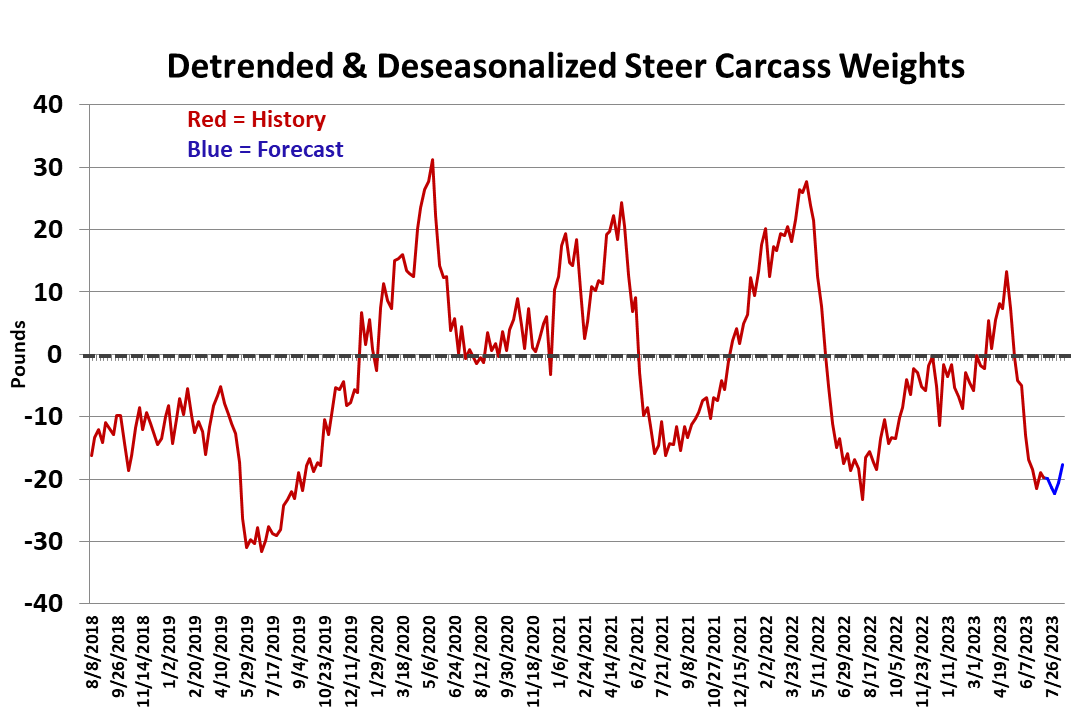

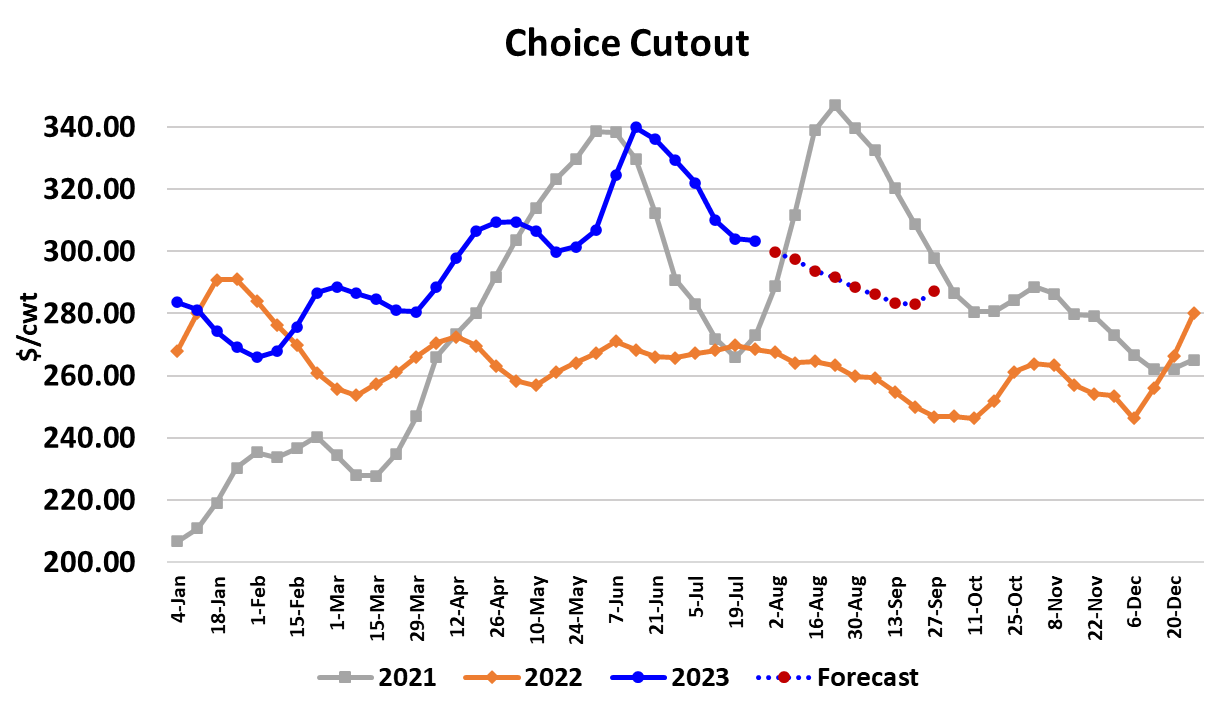

The decline in the beef market slowed this week, with the Choice cutout only averaging $0.75/cwt lower and the Select cutout gaining $2.38/cwt. If we look at the blended cutout, it was only down $0.14/cwt to average $298.36/cwt. Of course, the question on everyone’s mind is whether or not this is as low as it goes and if so, does the beef market move higher from here? I’m not ready to commit to a turn higher just yet and I’ve dialed in modest declines in the cutout for the next several weeks. The next big demand event on the horizon is Labor Day and it is possible that the cutouts could get a little bump in early-to-mid August as retail buyers finish preparations for Labor Day features. That activity is likely to be centered around middle meats and grinds, both popular feature items for the holiday that officially closes out summer. This week, it was the loins once again that were the biggest drag on the cutout. End meat prices actually posted some modest gains, likely as a result of stepped-up institutional buying ahead of the new school year. I see the rib primal as very close to a bottom right now and it should slowly work higher into September and then surge much higher in the OND quarter as the year-end holidays approach. Loin prices, however, are likely to continue lower until early October and the might see small increases as the holidays approach. Briskets might get a little bounce associated with Labor Day buying, but otherwise should trend lower over the next few months. Brisket prices have been well above last year since April and that feature is likely to continue. Chucks and rounds are more likely to move into a sideways to slightly lower pattern in the next few weeks. Fat trim is starting to come down in big chunks and averaged just below $160/cwt this week after peaking around $200/cwt back in May. The drop in 50s prices has to be driven by softer demand to some degree, because packers have pulled back on the kill over the past few weeks and that hasn’t been able to arrest the price decline. It does appear that a big part of the reason the cutouts have slowed their decent is because packers are trying to manage their margins by constraining the fed kill. This week’s fed kill registered 485k, the same as last week, and at least 20k less than what our flow model suggests should be available. I estimate packer margins this week were $114/head in the red, so this seems like a very good time for packers to attempt to boost the beef market by limiting throughput. Of course, they are also hoping that the smaller kills will put pressure on the cattle market, but so far that hasn’t materialized. Cash cattle trade was very slow this week, with packers bidding very low and cattle feeders taking a pass. As of Friday afternoon, we had only seen about 30,000 head trade in the negotiated market and much of that happened in the north at mostly steady money, while a little trade was reported in the South at $179, a dollar lower than last week. If packers don’t buy more cattle on Friday night or over the weekend, they will need to be back in the market early next week. I get what packers are trying to accomplish, but they will likely need at least a couple more weeks of restrained kills in order to break the cash cattle market significantly lower. However, they may not be able to continue with the light kills into August if they have large Labor Day orders to deliver. Further, there is an new variable entering into the calculus as a heat wave has set in across most of the middle section of the country. That could hamper cattle performance and make producers a little less inclined to stress cattle by moving them long distances. The DTDS weights are already at very low levels, suggesting that feedyards are quite current and the heat could make them just a bit more current, complicating the packers’ efforts to turn cattle prices lower. Normally, I would say that a key variable to watch in this situation in the price of 50s, since that is often an indicator of how much extra finish the cattle are carrying, but there seems to be some demand side softening currently underway in that market, so it might not be a very good indicator over the next few weeks. But we should definitely keep and eye on carcass weights and the DTDS for signs that the weather is slowing weight gains or alternatively, that small kills are starting to cause cattle to back up. From the demand side, Aug/Sep is generally not a great period for beef because families are dealing with back to school expenses and perhaps some big bills from summer vacation trips. Further, retailers are unlikely to back away from the price increases that they have been passing on to consumers in the past few months just because the cutout took a little dip here in late July. High retail prices have the potential to choke off some consumption and make beef look less attractive that other proteins that consumers might choose. And then of course, there is the re-start of student loan payments that is scheduled for October. That will take a big chunk of disposable income out of many budgets. So I’m not particularly optimistic about beef demand as we round out the summer and head into fall. The combined margin continued to move lower this week, indicating that we are currently in the midst of a short-term demand downcycle. Exports continue to run below year-ago, as one might expect given how high beef prices have been this spring and summer. We need to watch Mexico in particular because they are our best trading partner at the moment and if those buyers start to back away, it could spell further trouble for fall beef demand. The supply side is, and will remain, quite bullish for a long time to come given where we are at in the cattle cycle. Prices will almost certainly be higher next year compared to this year simply on the cyclical supply reduction. There will be periods of soft demand that temper the price increases, but in general buyers need to be prepared for sky-high beef prices to prevail in 2024. Next week, watch for a possible early-week cash trade if packers didn’t get enough bought this week. Watch kills for indications that packers are still in margin management mode and keep an eye on the weather because that could be the wild card that causes prices to surprise to the upside in the next few weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}