Beef Wrap August 11

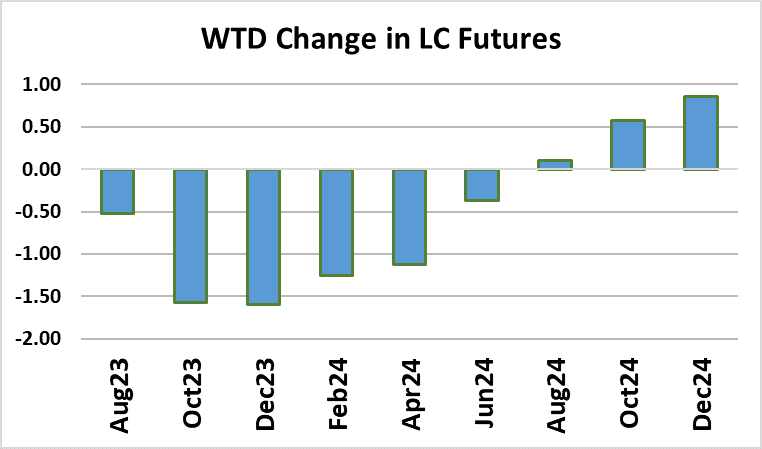

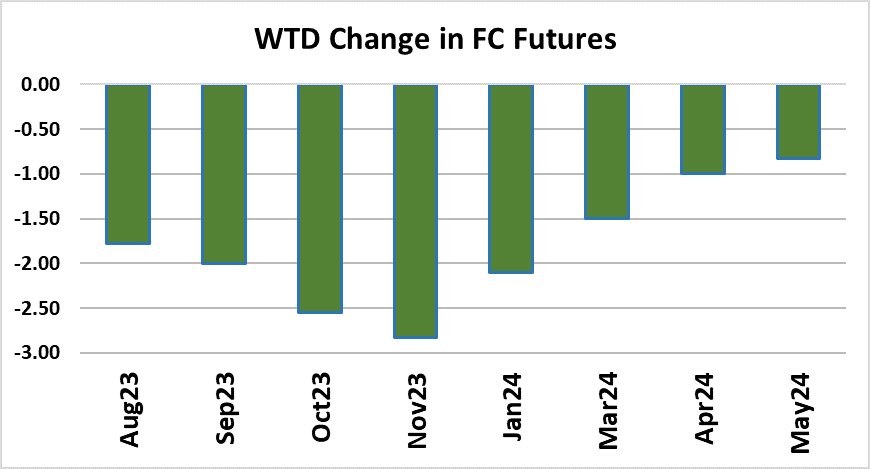

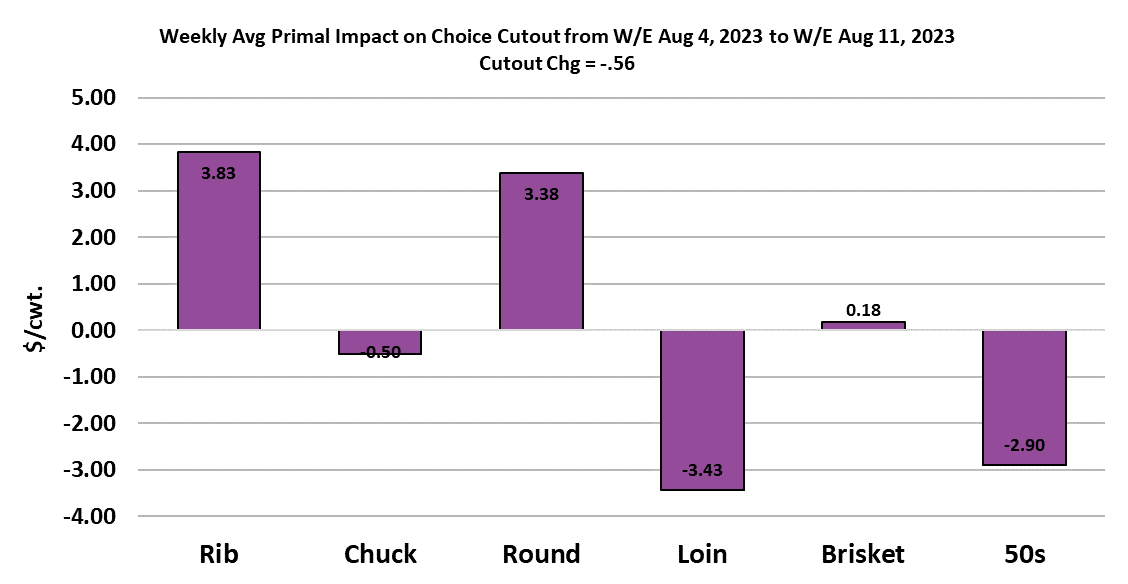

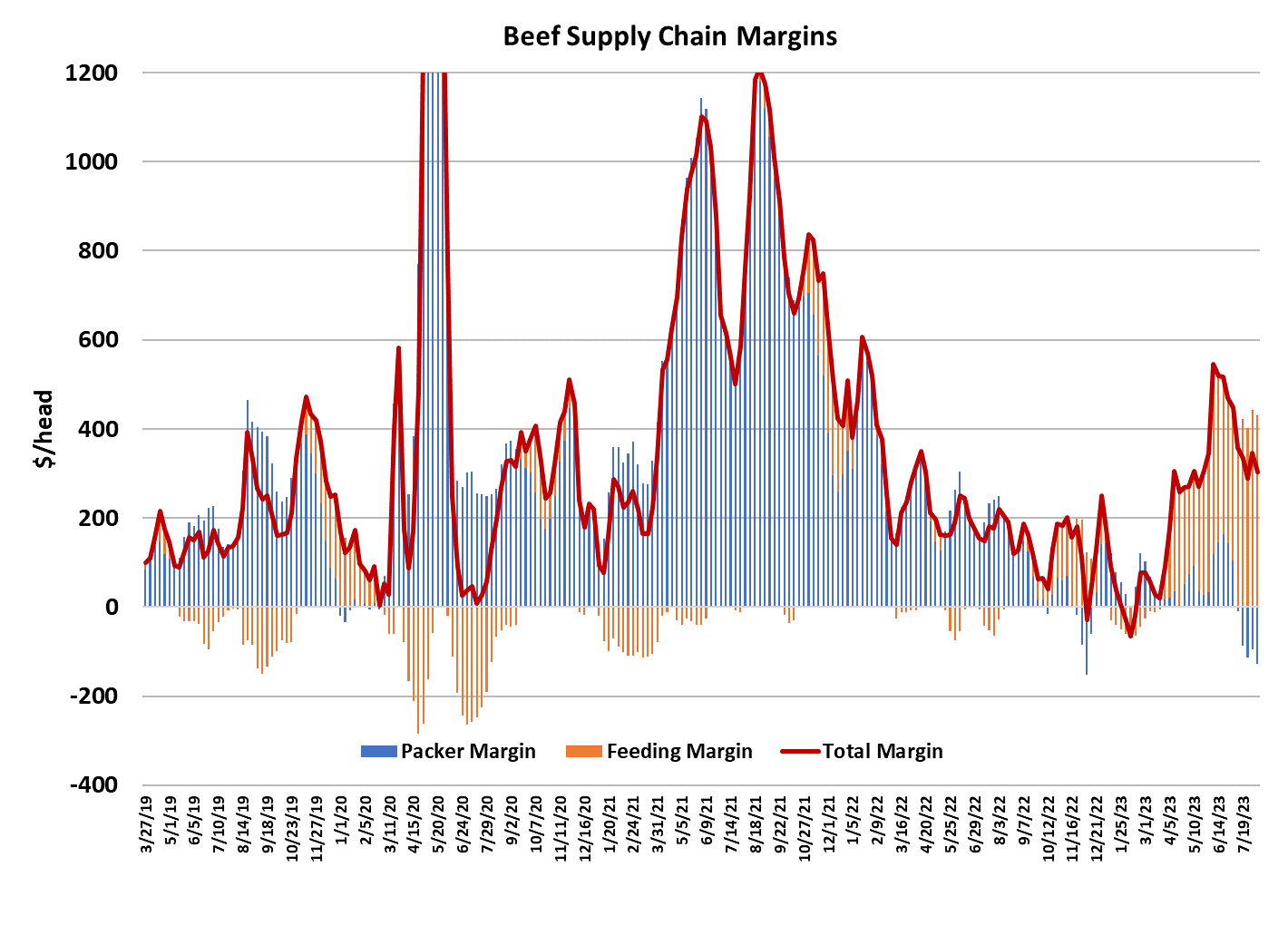

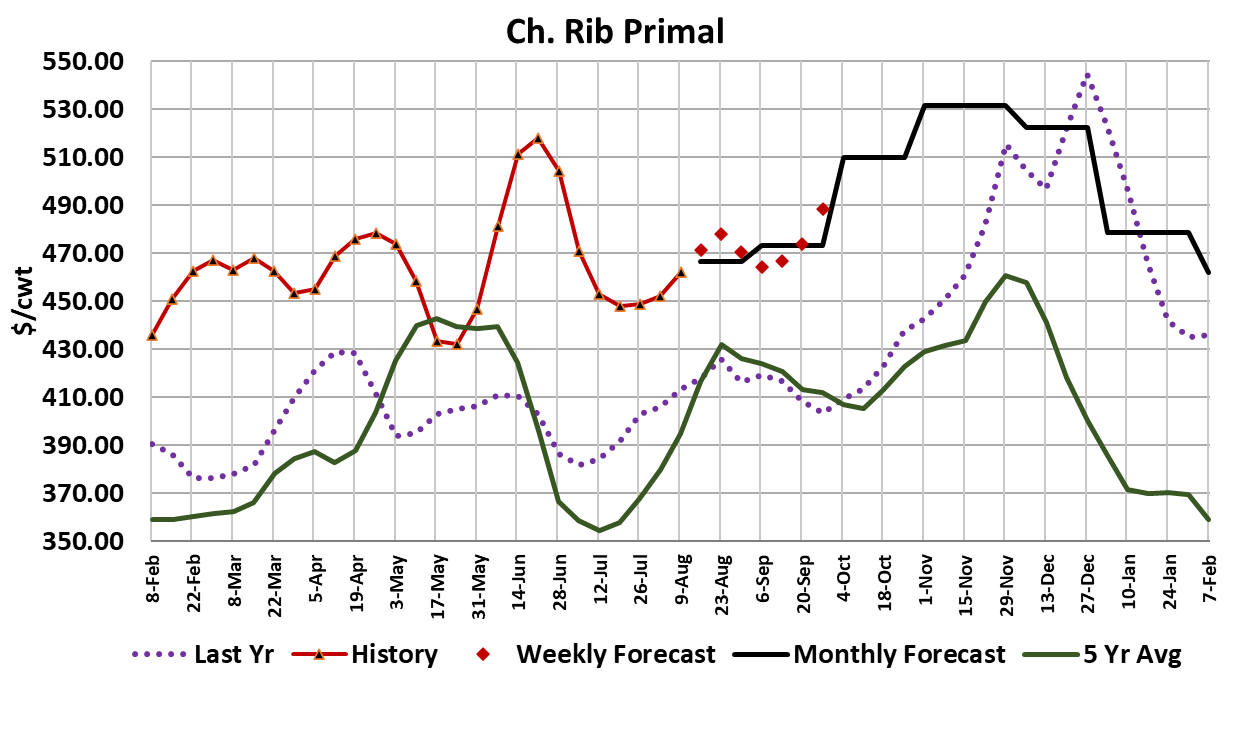

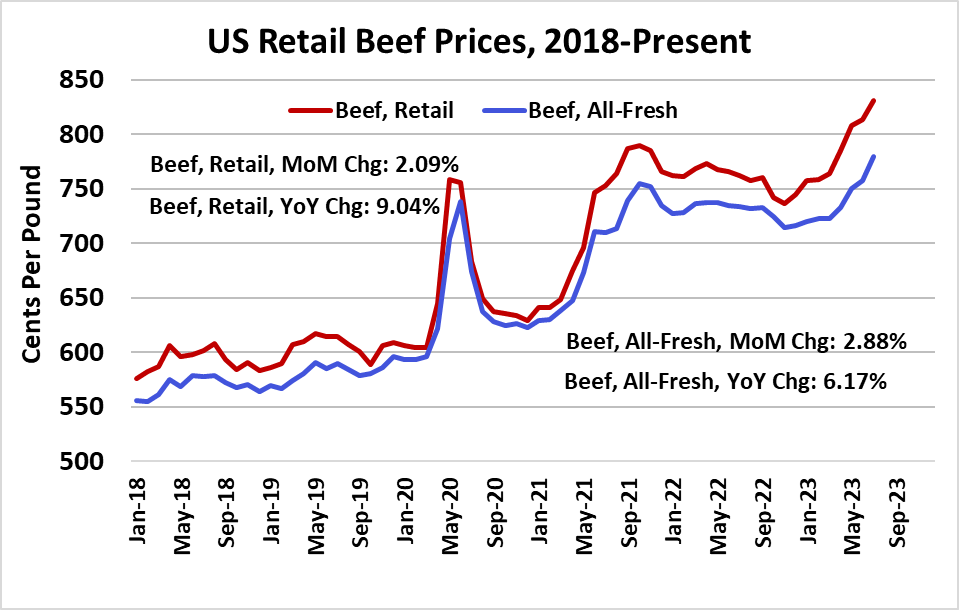

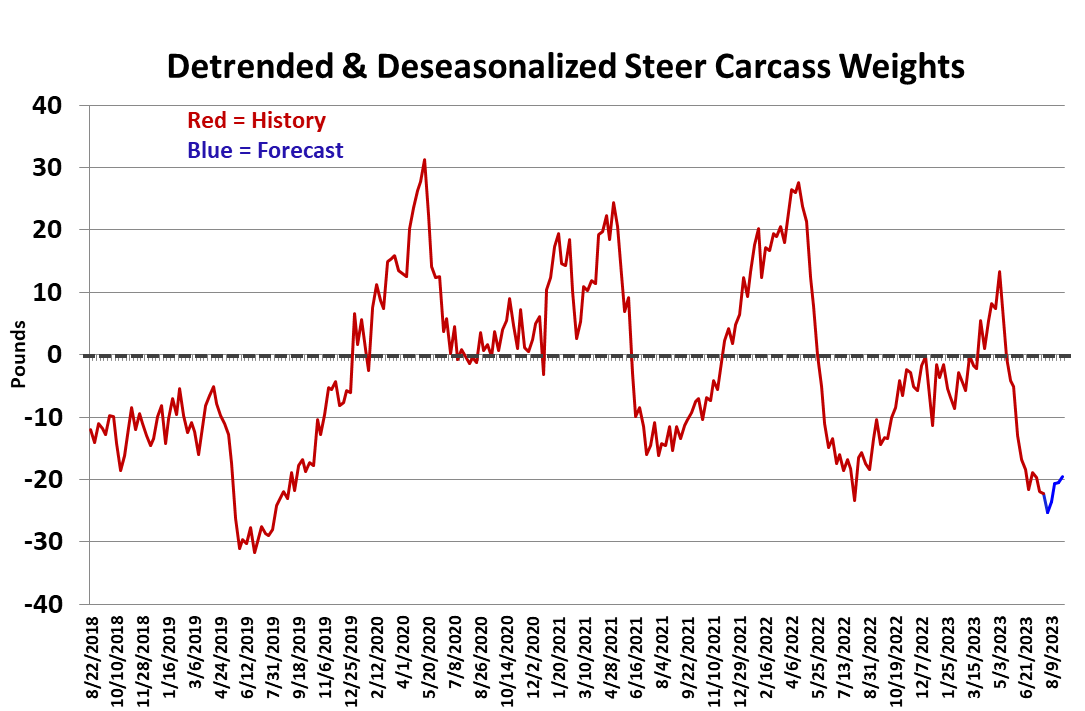

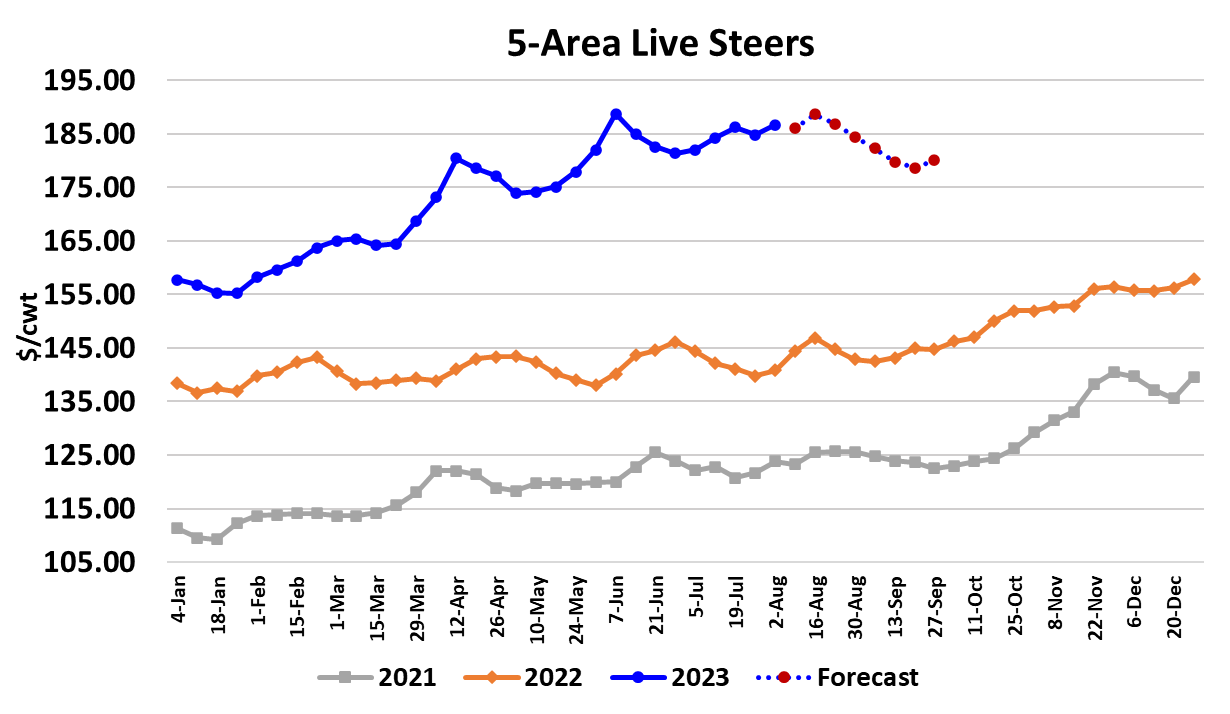

The beef cutouts eased a little lower this week, with the Choice losing $0.56/cwt. to average $302.41 on the week and the Select dropped $1.05/cwt to average $276.87. For about a month now, the Choice cutout has been stuck between $300 and $305 and the Select cutout has held mostly in the $275-280 range. This has happened in spite of packers throttling back on the kill, so the natural conclusion is that demand has softened enough that smaller production has not been able to materially lift prices. That may be about to change as there could be some improved buying interest in the next couple of weeks as retailers gear up for the upcoming Labor Day holiday. That interest would likely be focused on the middle cuts and grinds. With that in mind, I’ve got the rib primal advancing a bit more over the next couple of weeks, but that might not be enough to offset further weakness in other parts of the carcass and so we could actually see the cutout hold steady or dip a bit. The loin cuts are unlikely to get much of a boost from last minute holiday buying and those items tend to trend lower through September/October before late-year holiday buying causes prices to firm. The biggest risks to the cutouts are the end cuts and fat trim over the next few weeks. 50s moved sharply lower this week and are now trading around $140/cwt., with further price erosion anticipated. Of course, further kill cutbacks could boost beef prices, but I’m not sure that packers can go much lower than this week’s estimated fed kill at 473k. The flow model suggested availability would be something closer to 500k per week during August, but obviously the beef market can’t digest that amount at this point in the calendar without significant price concessions. Packers have done an admirable job of restraining the kill over the past month or so, but it hasn’t yet paid them dividends. This week’s packer margin was -$128/head and that is the fifth week in a row that packer margins have been negative. Over that five-week period, cash cattle prices have been firm to a little higher, so the kill cutbacks have yet to give packers enough leverage to pressure the cattle market. That may be coming, but it didn’t happen this week. Cash trade in the northern regions was mostly steady around $188/cwt and the South hadn’t traded much as of Friday afternoon. Packers are bidding $180 in the south, but many cattle feeders are holding out for $181, so we may see a small increase in average prices out of the South. The bears are getting frustrated that several weeks of small kills have yet to turn cash cattle lower, but this is a process that sometimes takes months to yield results. It is a testament to how current feedyards were when this process started back in July. My guess is that we won’t see cash cattle move decidedly lower until near the end of August and then I’d look for further weakness in September, which is not typically a great month for beef demand. Part of the problem is related to the consumer’s ability to afford beef. This week, USDA provided retail price data for July and it showed a whopping 2-3% increase (depending on the series) from the month prior. We knew this was a risk back in May and June when the cutouts were soaring like there was no tomorrow. Retailers have been busy raising retail beef prices ever since and now that the calendar has moved to a slower demand period, those high retail prices are choking off consumption. Don’t expect retailers to back off from their recent price increases either. They have been burned more than once in this cattle cycle by hot wholesale markets and with smaller cattle supplies on tap for Q4, they will not want to get caught in that trap again. The average retail price of beef in July was $8.31 per pound. Let that sink in. With consumers budgets stretched by inflation in other goods and services, their ability to purchase beef at these price levels is waning. Eventually, this will mean a much smaller cattle and beef industry in the US, but that will take some time to manifest. Before this cattle cycle bottoms and production starts to increase, we will likely see cattle and beef prices move to much higher levels than where they are today, and the industry will shrink. Beef will become more of a luxury item reserved for special occasions. We should have suspected that it would take many weeks of short kills before cattle prices turned south based on what the DTDS weights have been telling us all summer. Even now, after significant reductions in the kill, the DTDS weights are still losing ground. Of course, that calculation is based on FI weights, which are reported with a 2-week delay, so they may have improved but it just hasn’t shown up in the data yet. Still, those weights rarely get down to this level so when they do it is indicative of extreme currentness in the feedyards. As we have seen here in late summer, that doesn’t resolve overnight. We also got trade data for June this week and it showed a 14.3% YOY decline in beef exports. That shouldn’t be too surprising given how high US beef prices were back in early summer. The next opportunity for a YOY increase in exports might not come until November or December when we start to lap some very soft export numbers from last year. Bottom line, in this phase of the cattle cycle, where production shrinks and prices rise, we should expect ongoing erosion in beef exports. Next week, watch for some pre-Labor Day buying to provide a lift to the ribs and possibly the cutout. Expect packers and feeders to arm wrestle again with no clear winner and a reluctant trade late on Friday.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}