Beef Wrap July 21

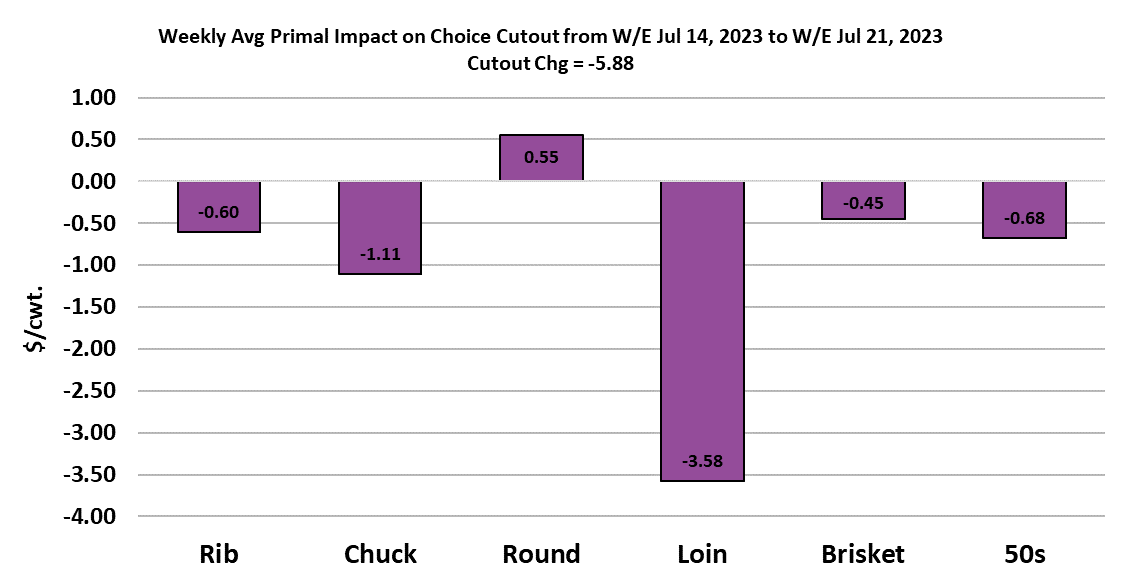

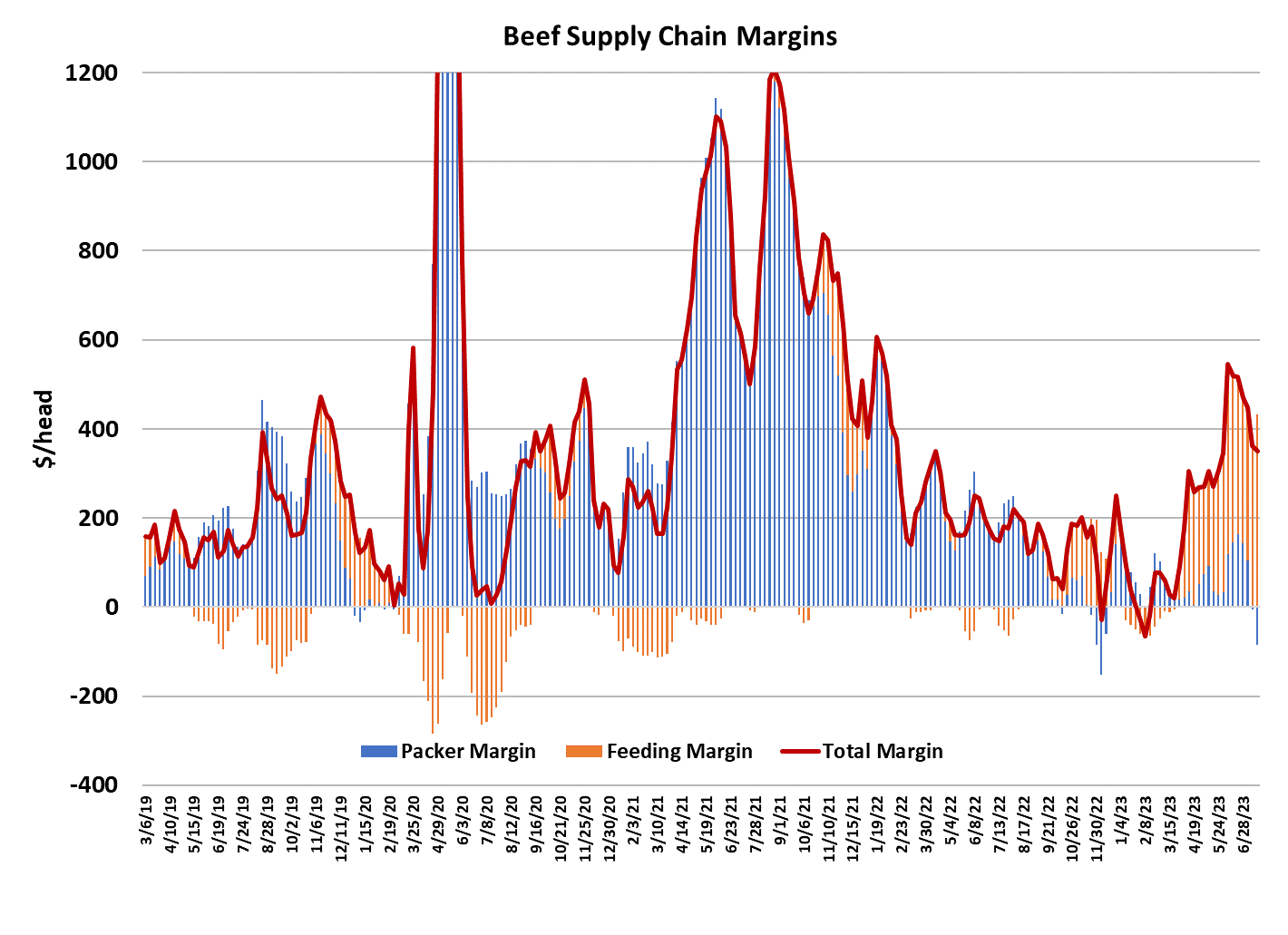

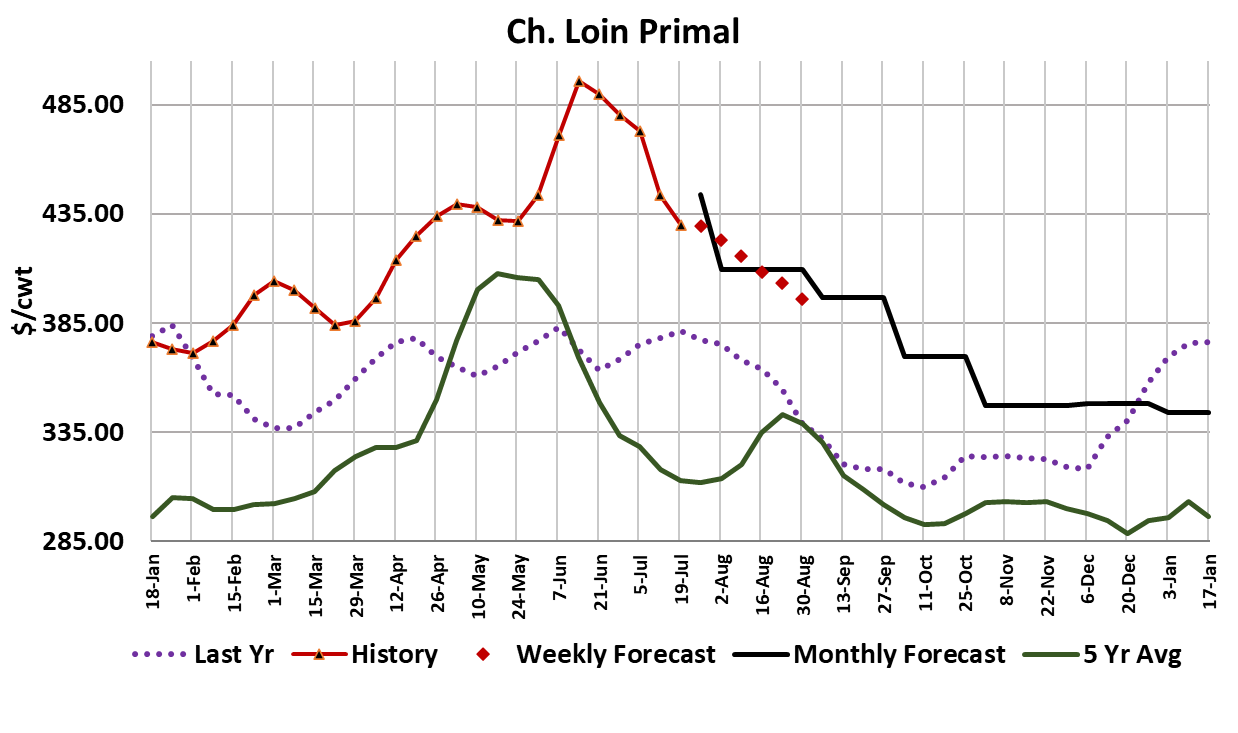

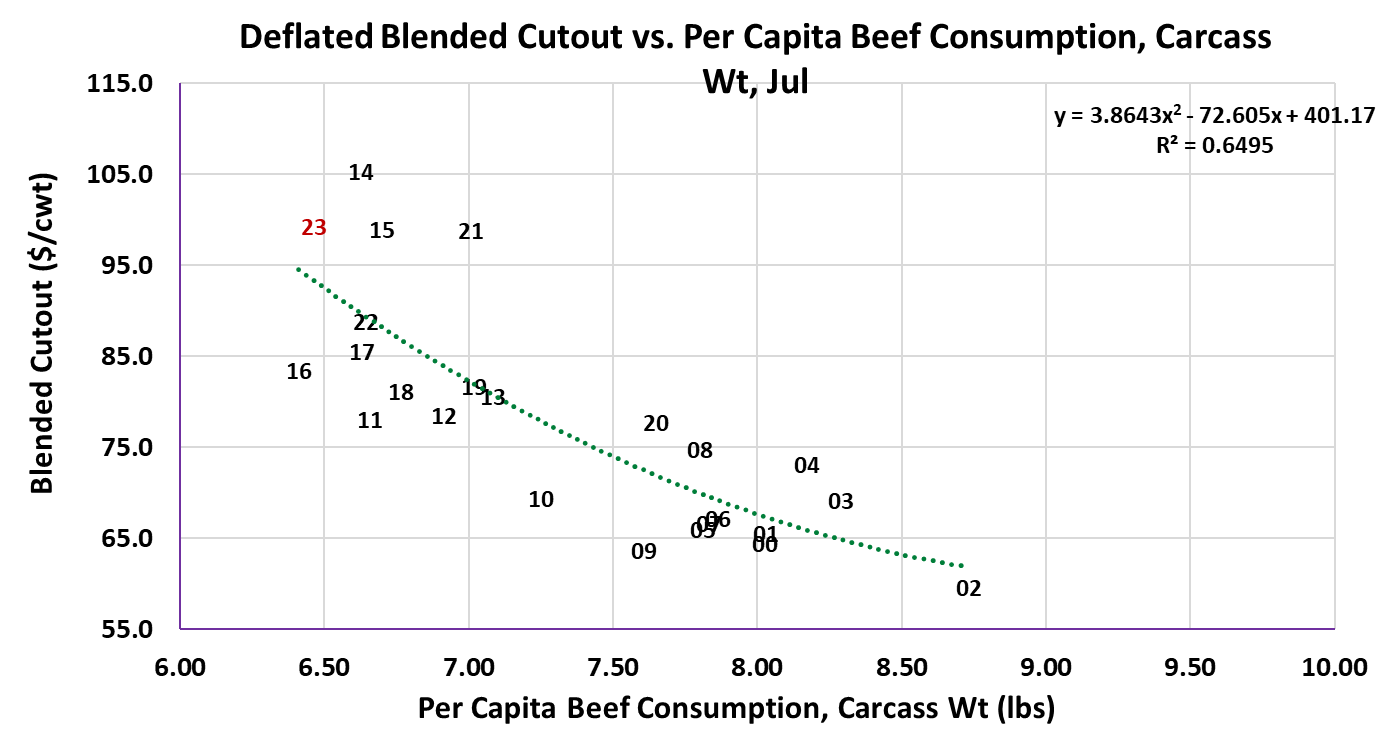

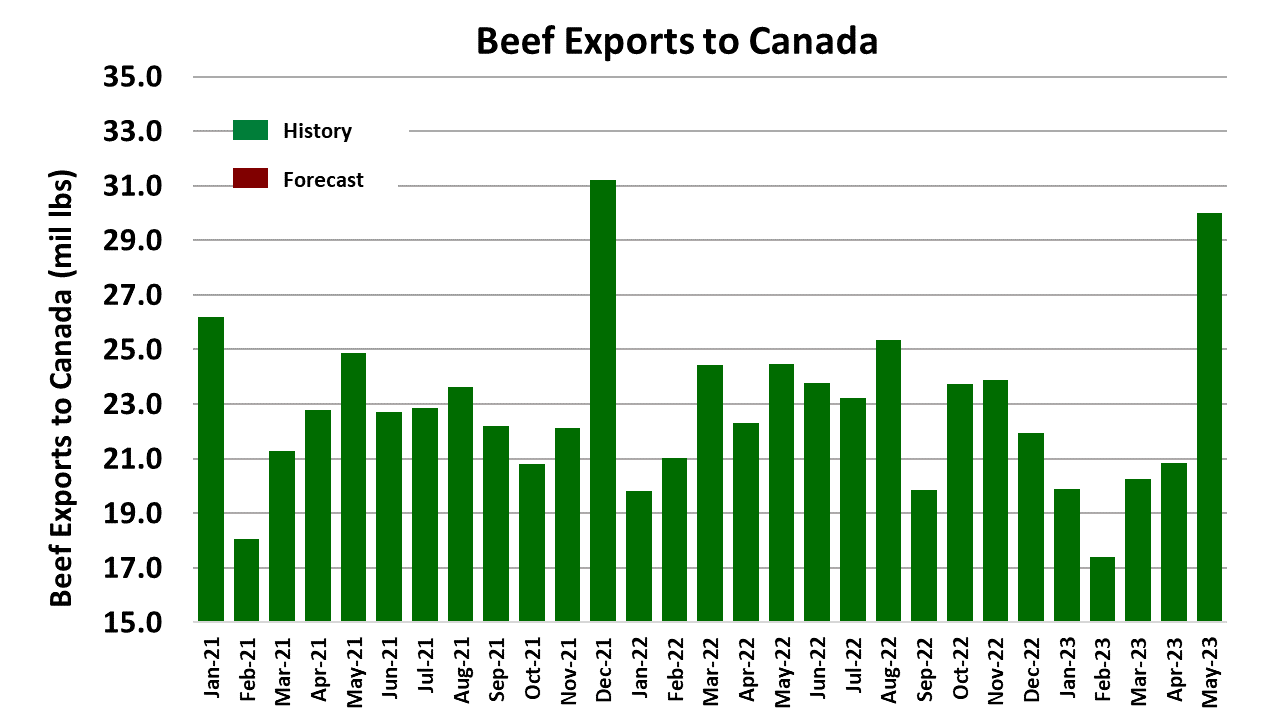

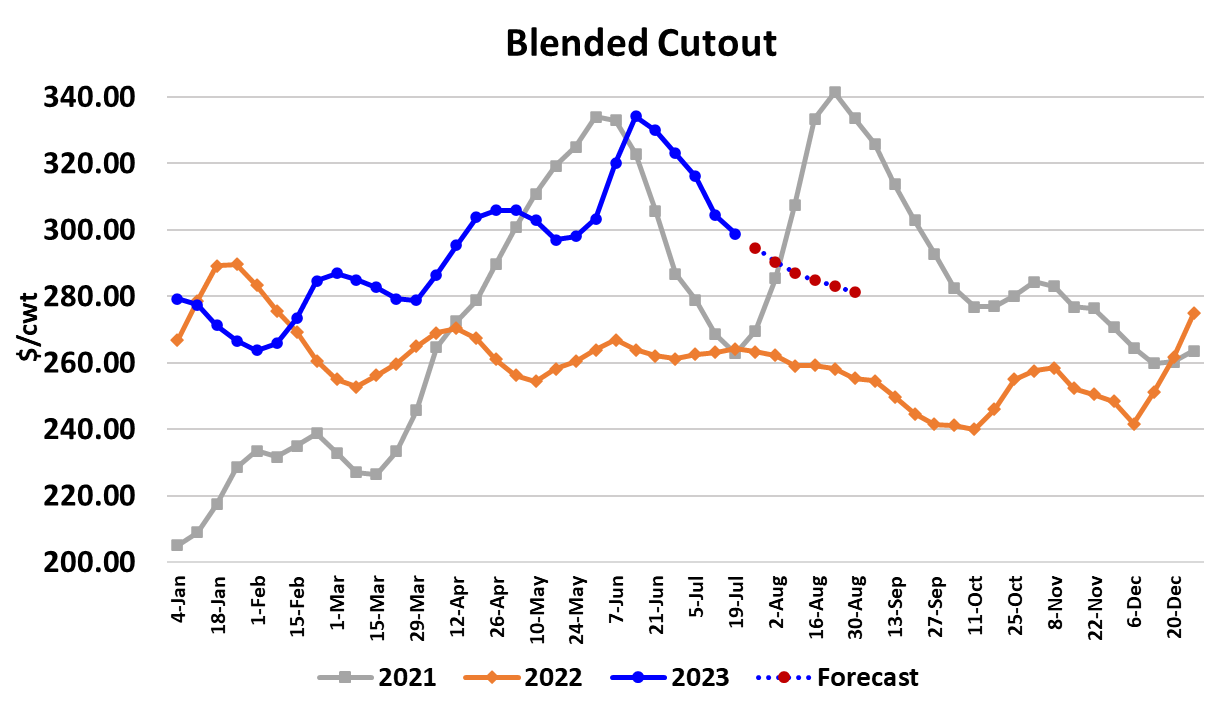

Cash cattle prices continued to advance this week, with trade in the north occurring at mostly $188 live and $295 dressed, up $2 live and up $5 dressed from the week before. In the South, trade waited until late in the week and most transactions were near $180/cwt., unchanged to $1 higher than last week. My calculations suggest that the national average live price will register close to $185.65/cwt when all of the data is reported on Monday. That would be about $1.30 stronger than last week. Higher cash cattle prices are not the packer’s friend, but even more troublesome for packers was the fact that beef prices continued to fall this week. The Choice cutout lost $5.88 on a weekly average basis and as of Friday afternoon it sits at just under $303/cwt. The Select cutout lost $4.14 and it settled on Friday afternoon at just under $277/cwt. That pushed packer margins deeper into the red and my calculation has margins averaging -$84/head this week. Next week, I’d look for margins to move below -$100/head. By late in the week, it did appear that the declines in beef prices were slowing and if that continues next week it will help to limit the damage to packer margins. Once again, it was the loin cuts that were the biggest drag on the cutout. The middle meats in general have had a tough go ever since Father’s Day, but that is a fairly normal seasonal pattern. It is also pretty normal to see the middle meats increase in the lead-up to Labor Day, the ribs more so than loins. The end cuts seem to be searching for a near-term bottom as well and so it makes sense to me that any declines in the cutout over the next couple of weeks will be smaller than what we have seen so far in July. The attached demand scatter for July shows the 2023 data point closer to the regression line than what we saw in either May or June, suggesting that some demand erosion has taken place recently. Not that demand is particularly bad at the moment, just softer than it was earlier in the summer. That too is a normal seasonal characteristic. Packers are trying to rectify their margin problems by throttling back on the kill. This week’s fed slaughter registered close to 490k, which is well below the 510k or so that our flow model suggested would be available to slaughter during July. My guess is that packers will expand the fed kill back closer to 500k next week, and August should see fed kills in the neighborhood of 505k. Weights are getting heavier, with this week’s data showing an eight-pound increase in steer weights, but that was for the week of July 4, so I’m sure that the holiday played a role in the big increase. Still, with weights moving upward and the kill expected to expand marginally in August, beef buyers should see a little better availability in August compared to July. The important question is whether or not consumer demand will remain strong in the months ahead. With retail prices for beef rising while retail pork prices are falling, it is reasonable to expect some consumer demand to shift away from beef and towards pork. There is also the specter of the student loan repayment start-up that is scheduled for October. Some borrowers may start cutting back on purchases in August and September in preparation for having to start making those payments once again. But I think the biggest problem that beef will face is the very high level of retail prices causing consumers to seek out alternatives. It is unlikely that retailers are going to lower prices anytime soon, so unless price levels for the competing proteins rise significantly there is a real risk that some beef demand will migrate over to cheaper protein sources. With the cattle herd still in liquidation mode, it is reasonable to expect consumer prices to remain on an upward trajectory for the next couple of years. Beef is well on its way to becoming a luxury item—one that people will splurge on for special occasions, but not something that lands on the plate routinely during the week. That is probably what needs to happen in order to ration an ever-shrinking beef supply. Of course, export markets will likely give up some volume to the domestic market as production shrinks and prices rise. We are already seeing that start to materialize. This week’s export data out of FAS showed total beef exports running 17% softer than last year at this time. Fortunately, our N. American trading partners, Mexico and Canada, continue to import larger volumes of US beef than they did last year. The real weakness in beef exports is originating from the Asian countries, particularly Japan and S. Korea. China is also a little less enthusiastic about US beef than they were last year. Demand during the first half of 2023, was second only to 2021 in terms of strength. In fact, demand in the last three years has been exceptional and it isn’t realistic to believe that it will remain at this level indefinitely. So, while the cattle supply cycle continues to point toward higher prices, there is a very real risk that demand could return to more normal levels in the next couple of years and that might take some of the edge off of beef pricing. USDA released two important reports today. The first was Cattle on Feed, which showed June placements up 2.7% and 4.5% larger than what analysts were expecting. That will likely be negative for the futures on Monday. The second report was the mid-year inventory report which showed all cattle and calves down 2.7% from last year and the beef cow inventory down 2.6%. There was no sign that cattle producers are routing heifers into the breeding herd just yet. All of that is just further confirmation that the herd is in the midst of a major downsizing. Next week, look for the cutouts to begin to stabilize. Watch the daily kills for signs that packers are limiting throughput in order to put pressure on the cattle market. Cash cattle might not move lower next week, but if packers can maintain discipline on slaughter levels for a couple more weeks, they might stand a decent shot at breaking cattle prices lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}