Beef Wrap July 15

Packers continued to push the cash cattle market lower this week, with

the weekly average through Thursday at $141.94, down about $2.50

from last week’s average. At the same time, they were successful in

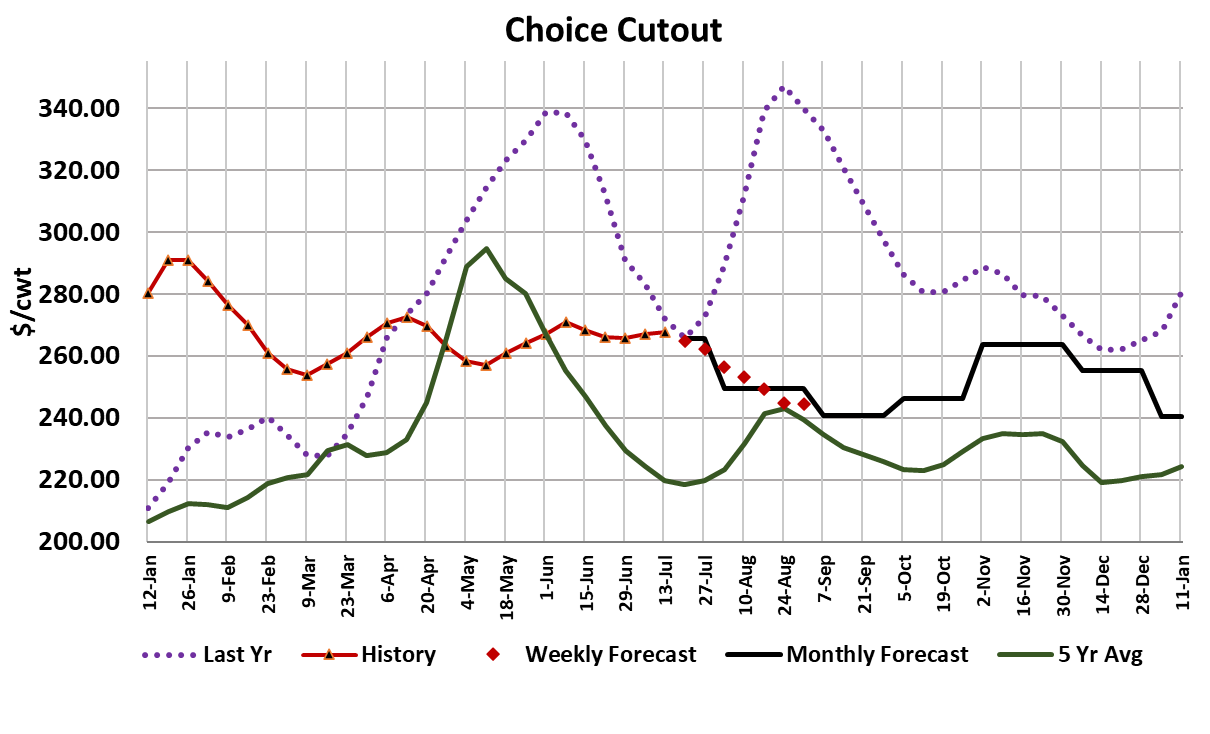

holding the cutouts mostly steady as production ramped back up

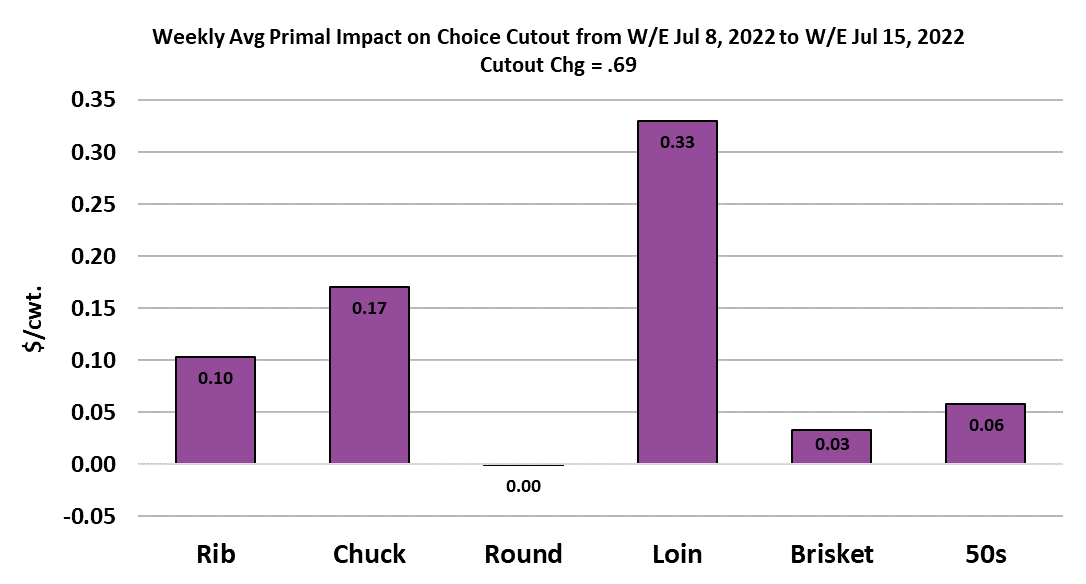

following the holiday. Through Thursday, the Choice cutout was up

$0.69 and the Select was $0.28 higher. Good thing that packers

have the cash cattle market on a downward trajectory now, because it

doesn’t feel like the cutouts are going to be able to hold at current

levels now that we are back in a high production environment. I’m

actually a little surprised that the cutouts held up so well this week, but

certainly expect them to give up more ground next week. This week

the loins did most of the work in holding the cutout up, but that is

unlikely to persist. The normal seasonal pattern is for the loin primal to

trend steadily lower from now through October.

In the next couple of weeks, the middle of the country will experience

some brutally hot weather and that seems likely to curb demand, but it

also could cause animals to eat less and gain less, so while the

demand impact of the heat event is probably negative to price, the

supply effect could be positive to price, but with more of a lag.

Hopefully, this next heat wave won’t cause thousands of cattle to die in

feedyards like the one earlier this summer did. Packers have been

aggressive with the kills going back to last Saturday and we even saw

100,000-head steer and heifer kill on Tuesday. I’m projecting the

weekly total to come in around 535,000 head, which would be about

10,000 head more than what they were killing just prior to the holiday.

Next week could be even larger. The nation’s feedyards are full and

packers are eager to keep their newly replenished workforce engaged.

Retailers should be fully replenished now after the holiday and I

suspect that if the fed kill next week is bigger than this week, there will

be ample availability and wholesale price levels will need to adjust

lower in order to clear all of the product.

USDA reported retail prices for June this week and we saw the

average retail price fall from $767.50 cents/lb in May to 766.00 cents/lb

in June. That is a very tiny decline and for all practical purposes we

can surmise that retailers are not really lowering beef prices at all.

Apparently, they will need to see more downward movement in the

cutouts before they feel comfortable lowering their retail prices. What

this means is that consumers will be asked to consume larger

quantities of beef in July than they did a couple of months ago at prices

that are very similar. I suspect that consumers will balk at that and

thus retail movement will slow, causing retailers to slow down orders

into the wholesale market. That, in turn, should cause the cutouts to

move lower and thus provide the green light for retailers to lower

consumer-facing prices. The whole process could take a couple of

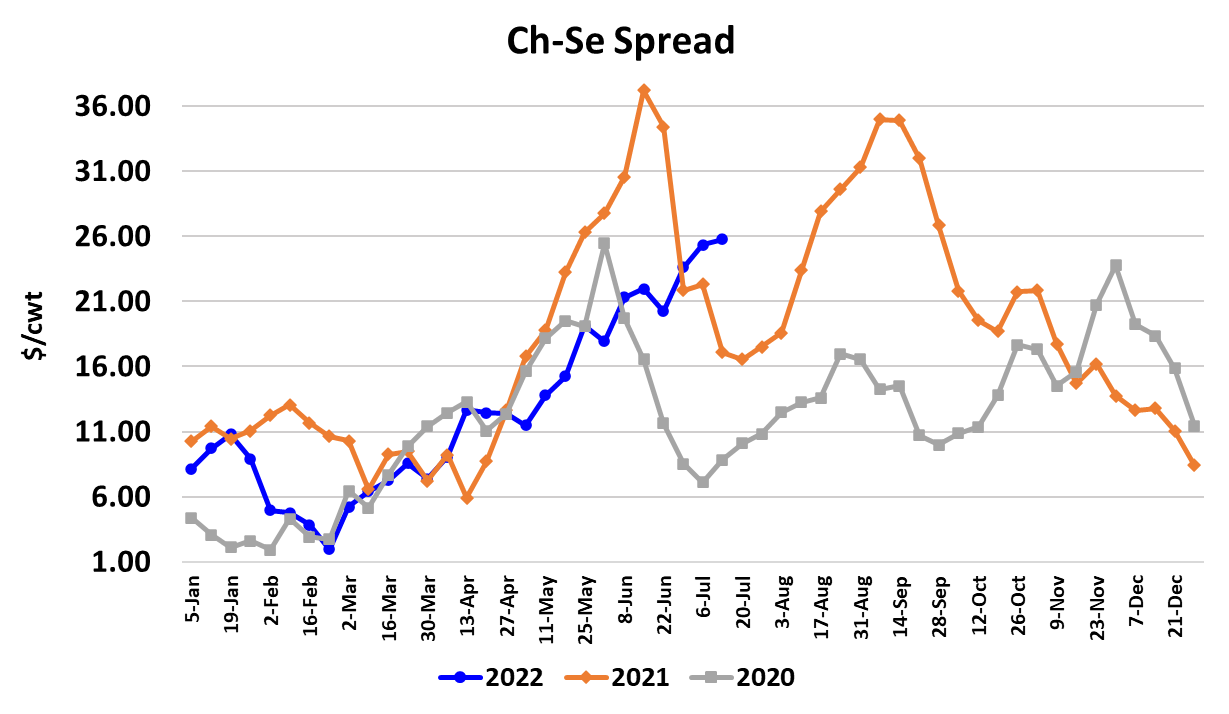

months to play out. One interesting feature of the current market is the

very wide spread between Choice and Select.

The spread averaged close to $24/cwt this week, where historically

something closer to $10/cwt would be more typical for this time of

year. We saw a similar thing back in the summer of 2019, where the

Ch-Se spread traded in the low $20s from early July through

November. A wide spread is normally indicative of strong demand

for middle meat and we typically see wide spreads in the spring as

grilling season approaches and in November ahead of the year-end

holidays. This wide spread however, might be more of a supply

issue as high corn prices and rapidly falling carcass weights this

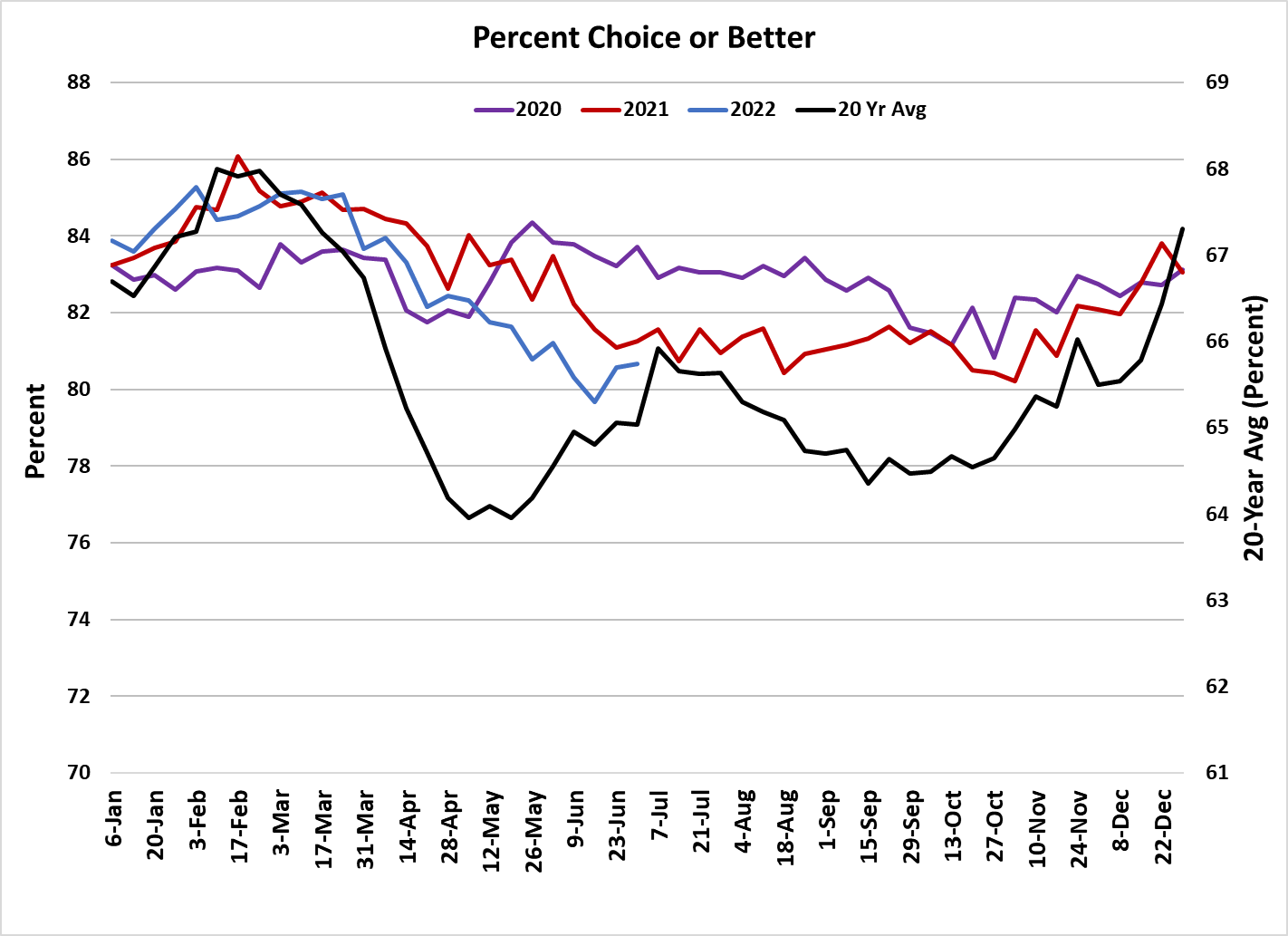

spring and summer caused the grade to decline. That attached chart

shows that currently the percentage of product grading Choice or

better is below the level seen in both 2020 and 2021.

We saw a rapid decline in the de-trended and de-seasonalized

carcass weights over the past couple of months and that points to a

rapid rise in currentness. Along with that normally comes a drop in

the grade. Back in 2019, the amount of product grading Choice or

better was about 2% below where it is today and it stayed relatively

constant (didn’t expand) for most of the rest of the year. Of course,

many producers are compensated on a grid-type system that values

their cattle on the basis of many quality attributes, and when the

Choice-Select spread is wide, those grids typically increase the

premium paid for cattle that grade Choice. To get cattle to grade well

they need to spend more days on feed and with packers killing at

such a strong clip, that might not be an option. Further, the heat

wave that is coming will have a negative impact on how cattle grade.

So, we may be stuck with a stronger-than-normal Choice-Select

spread for at least a couple more months. On the macro front, the

equity markets had another terrible week and talk of an impending

recession is growing. Neither of those things are helpful to beef

demand.

The US dollar has also strengthened considerably and that raises

concerns about beef exports in the second half of 2022. So far, we

haven’t seen much evidence of a slow down in international demand,

but that could be a feature in the market when fall arrives. For now, I

still look for the cutouts and cash cattle prices to work lower between

now and Labor Day. Forecasts have been raised a little recently to

account for firmness in the prices during early July, but I still have the

Choice cutout pulling back to around $245 just after Labor Day. The

risk to that forecast lies to the upside given that the Choice cutout has

been holding in the $260-270 range for the past nine weeks. Next

week, watch the weather forecasts for indications of hot weather

throughout cattle feeding country. If it gets abnormally hot for an

extended period of time that might provide cattle feeders with enough

leverage to slow down or stall the decline in the cash cattle market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}