Beef Wrap July 14

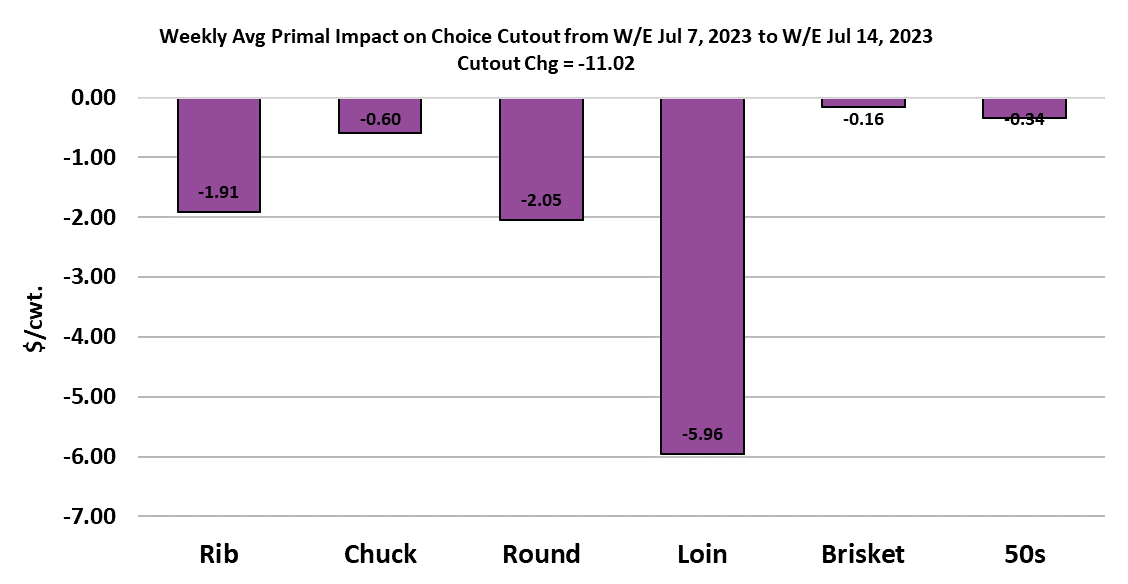

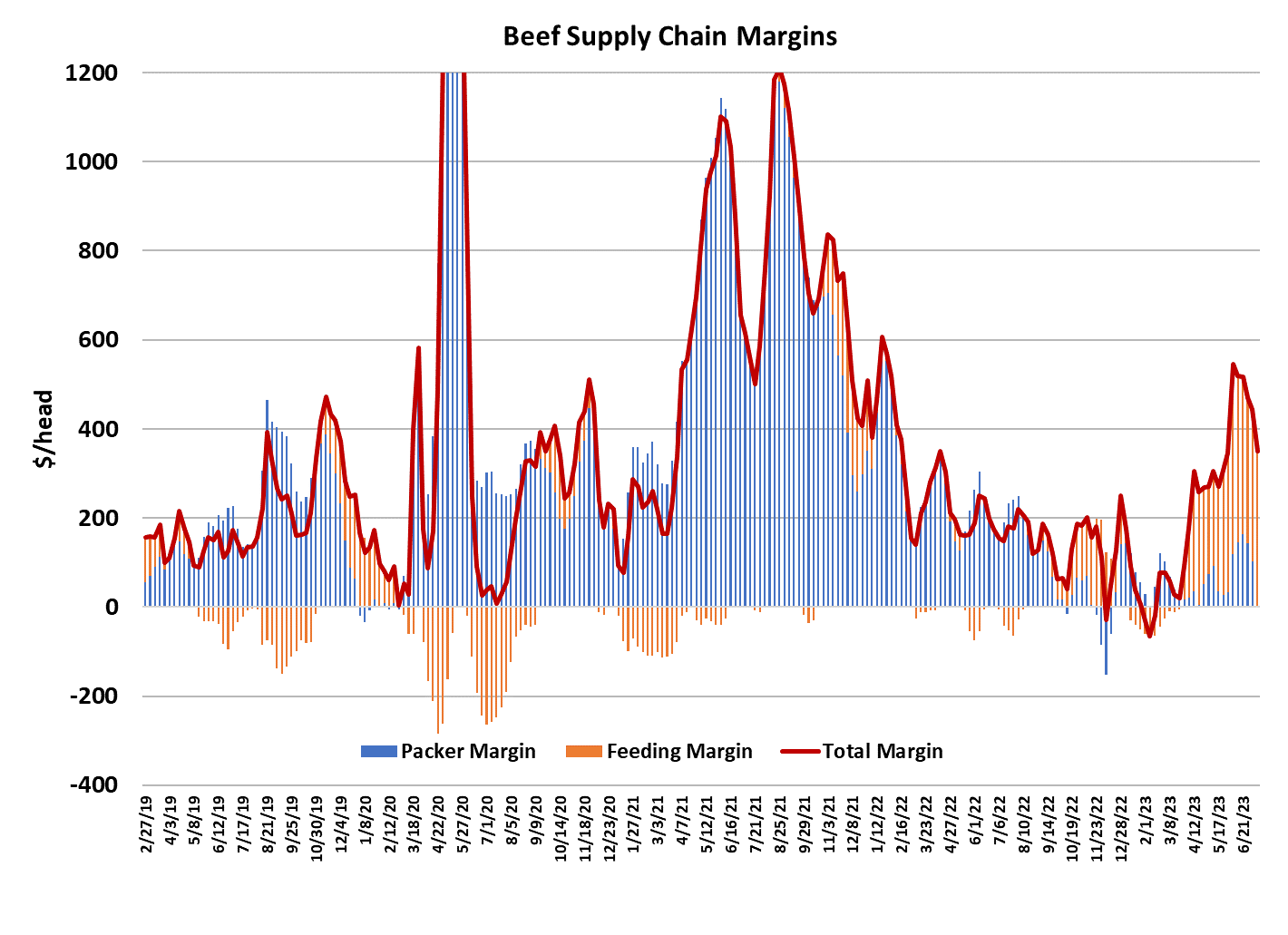

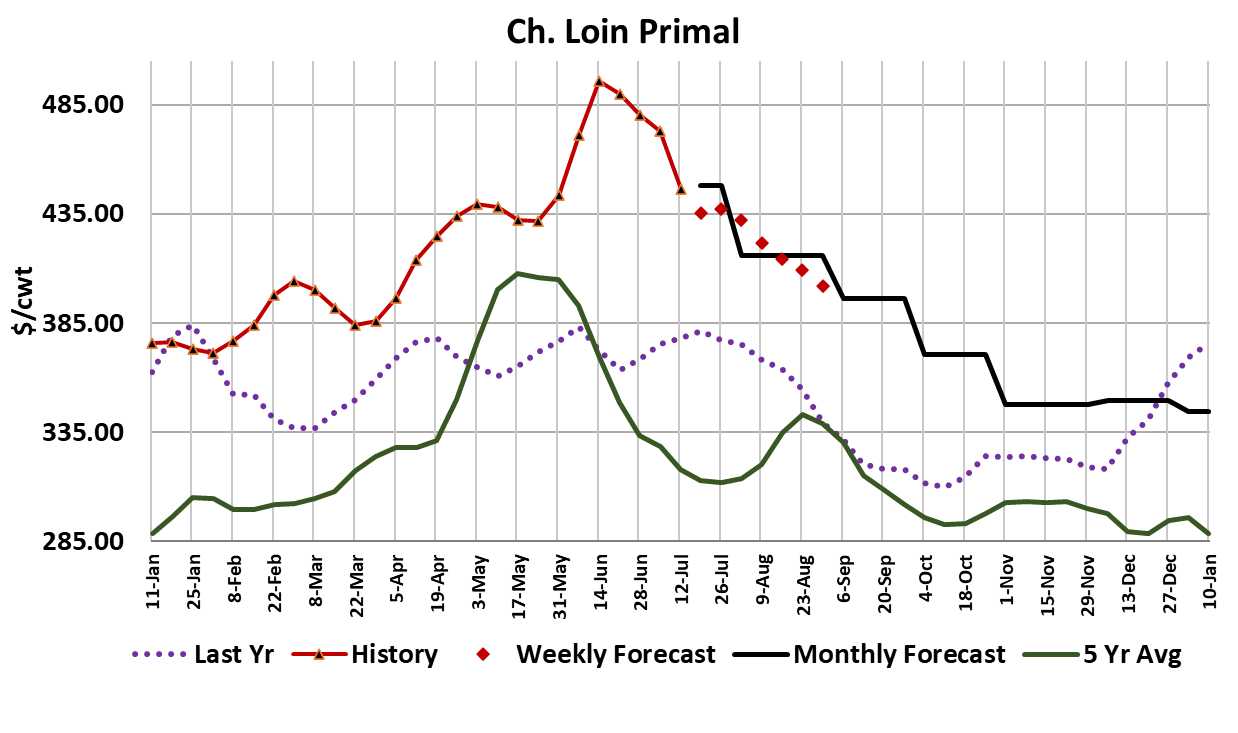

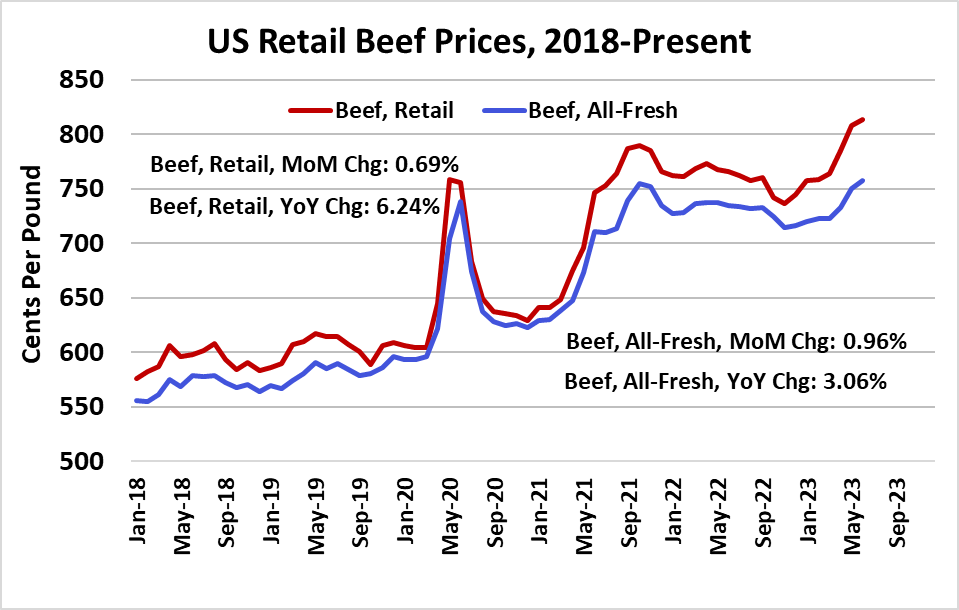

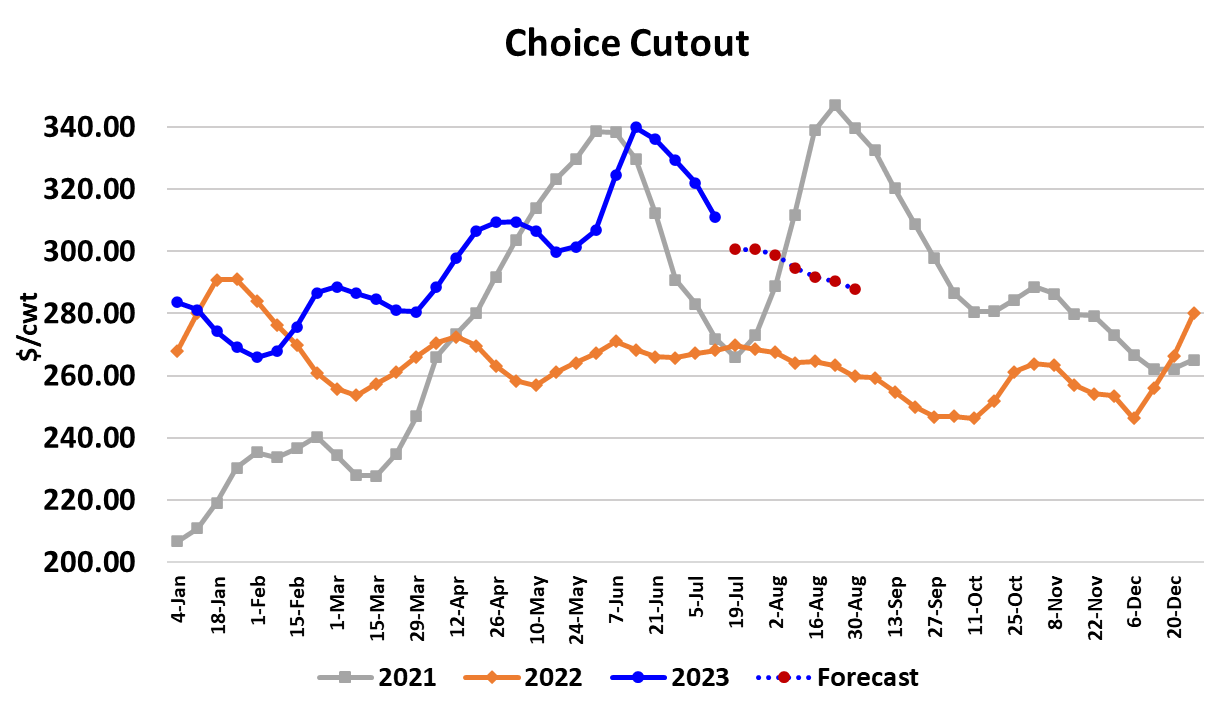

It was more of the same in the cattle and beef complex this week, with the cutouts moving lower at a rapid pace, but the cash cattle market stubbornly refusing to give much ground. Through Thursday, the Choice cutout was down $11.02/cwt and the Select was $9.69/cwt lower. The tug-o-war between packers and cattle feeders hadn’t yielded much trade as of Thursday night. There was some very light trade reported in the South at a steady $178 earlier in the week, but most cattle feeders seem to be keeping the gate closed until Friday in an attempt to get more out of the packers. In the North, there was some dressed trade in the $294-295 range, which is $4-5 higher than last week’s average. It is a pretty good bet that the live trade in the North will be at higher money, and I think it should be sufficient to push the national average close to $183 on the week. That would be up just a little less than $1 from last week. Why can’t packers pressure the cash cattle market lower in response to rapidly declining beef prices? The simple answer is that they are running the kill too large for the supply of market ready cattle. Last week, packer margins were $100/head. This week, those margins are $0/head. Perhaps that rapid evaporation in margin will get packers’ attention and thus get them started thinking about cutting the kill. They had better hurry because if my forecast is correct, next week’s margin could be $100/head underwater. In early June, packers paid up sharply for cattle and then managed to jack beef prices high enough to more than cover their cattle cost. In fact, that strategy produced some of their best margins so far this year. Maybe they should consider paying up for cattle and then calling beef buyers on Monday and asking for higher beef prices. It worked last time, but that was early June, and this is mid-July. Demand is probably not strong enough right now to pull that off and besides beef buyers are tired of high prices. You can see that is true by the way that the cutouts have been coming down in the last few weeks. Thus, it looks like the only viable margin rescue strategy is the tried-and-true cut-the-kill approach. That may be in the works as some have suggested that the Saturday kill will be very small this week. This margin problem has come upon them so fast that I’m not sure they will be able to react that quickly, but I do expect the overall fed kill to be around 505k, which is very similar to what they slaughtered in the week just before the holiday. Clearly, market-ready supplies are tighter in the North than in the South presently, and with the Choice-Select spread still above $25/cwt, there is incentive for packers to seek out the higher quality animals which typically live in the Northern region. After a couple of months where the price spread between the North and South was diminishing, it looks like it may widen back out in the next week or two. All of the primals were lower through Thursday, but it was the loin cuts that put the most downward pressure on the cutout. Choice strips and shortloins dropped hard this week, and most of the rest of the loin cuts were down to a smaller degree. The loin primal had been a major pillar of support for the cutouts through spring and early summer, so this is a major shift. Further, seasonal patterns suggest that cuts within the loin primal should continue lower from now though October. Ouch. The good news for packers is that they should soon start to see increased interest in end cuts from institutional buyers like school systems and colleges as they prep for the start of a new school year. In the Southern US, many schools are open by the middle of August, if not sooner. In the Northern states, the school year might not start until after Labor Day. Retail and foodservice buyers will be watching middle meat items closely in an attempt to negotiate their Thanksgiving/Christmas middle meat orders when the spot market for those items is at its low point. Availability should be lower this year compared to last because cattle numbers continue to trend lower, so buyers will not want to wait until fall arrives to make their commitments. Anyone that waits too long could get left out. Steer carcass weights were reported up 1 pound this week, so it looks like the seasonal bottom in weights has been made, but weights are still not keeping up with the normal annual increase. With animal numbers shrinking, that means fewer pounds of beef produced and reduced availability in the domestic market. Another headwind for the market is very high retail prices. USDA reported average retail beef prices for June this week and the “all-fresh” beef price was up nearly 1% from May. It currently is running 3.1% stronger than last year. This shouldn’t be a surprise given the rapid escalation in wholesale beef prices that occurred this spring and early summer. Now that wholesale prices are retreating, don’t look for retailers to be quick to lower beef prices. Even worse, retail pork prices dropped almost 1% from May to June. So, beef is looking less competitive compared to pork with each passing month. That could cause consumption to slow and thus force packers to cut the kill, to better align production with softer demand. The combined margin chart continues to signal that we are currently in a demand downcycle. Next week, look for further slippage in the cutouts and expect cattle feeders to continue to resist lower cattle prices. Keep an eye on the daily kills for signs that packers are getting the message that it is time to slow production.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}