Beef Wrap July 1

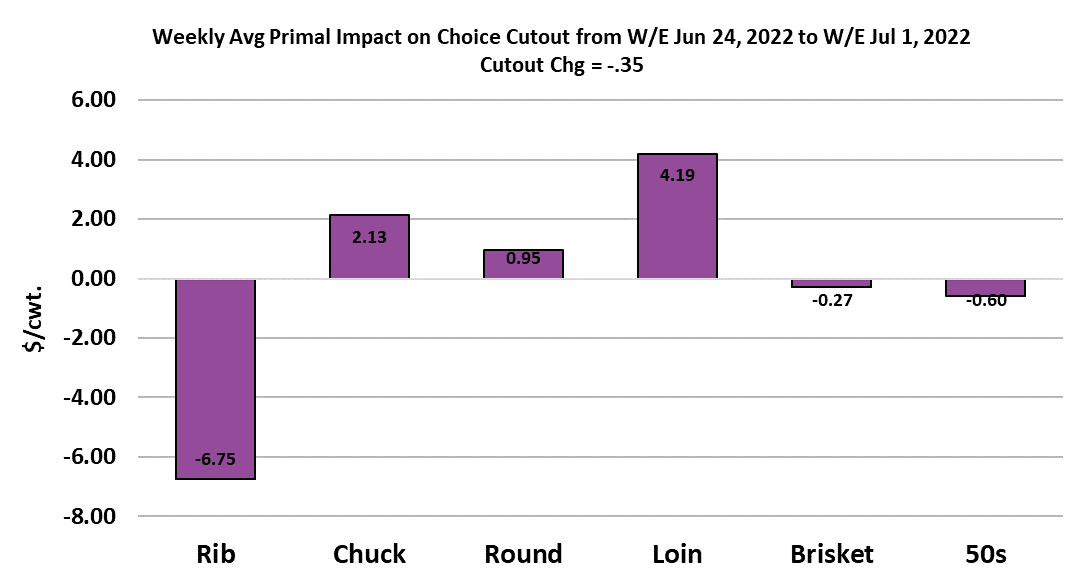

The beef packer’s woes continued to mount this week as the

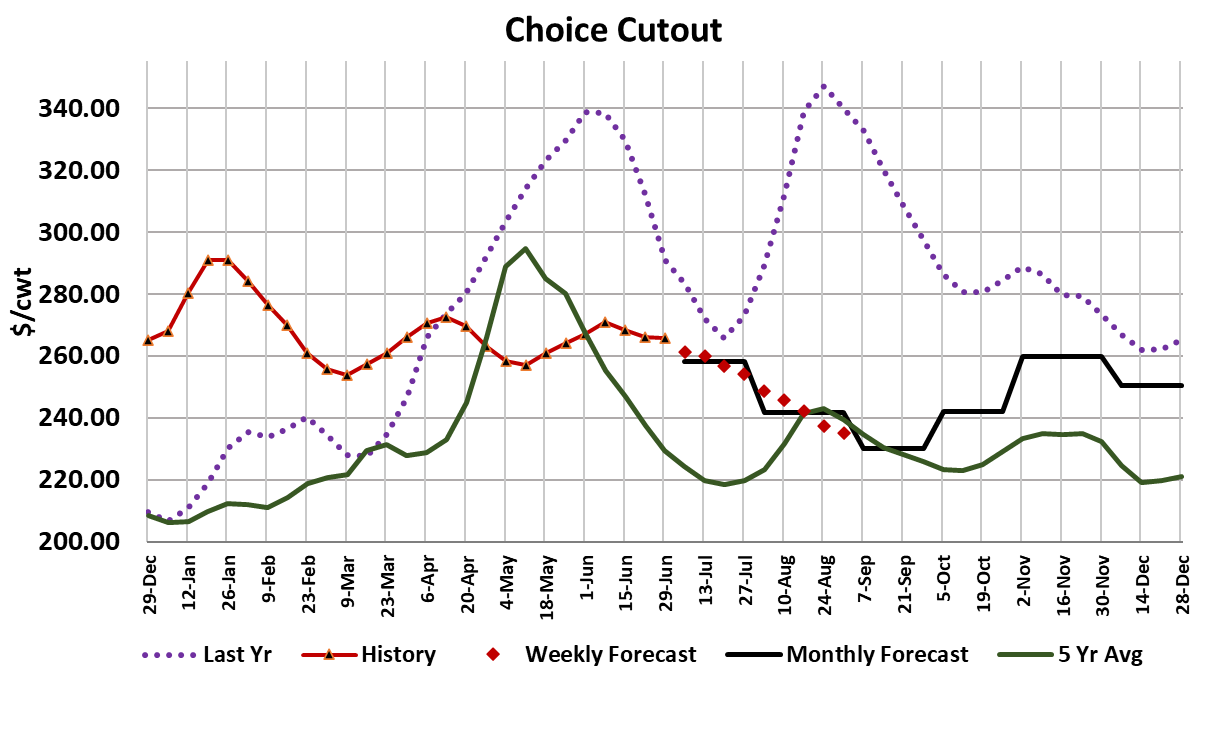

cutouts eased lower again while the cash cattle market advanced.

The Choice cutout dropped $0.35 on the week and the Select

cutout was down $3.73. At the same time, the cash cattle market

averaged almost $1.50 higher, with the weighted average coming

in at $146.10. There was a huge disparity between the regional

cattle prices, with the North seeing prices at $147 or above and

the South mostly trading in the $137-138 range. That $10 spread

between North and South is one of the largest regional price

differences in memory. With the weighted average at around

$146, that implies bigger volumes were bought in the North

compared to the South. Perhaps that is because more cattle in

the South are on formula and packers will have access to their

July formula cattle next week and thus didn’t need to procure as

much in the cash market.

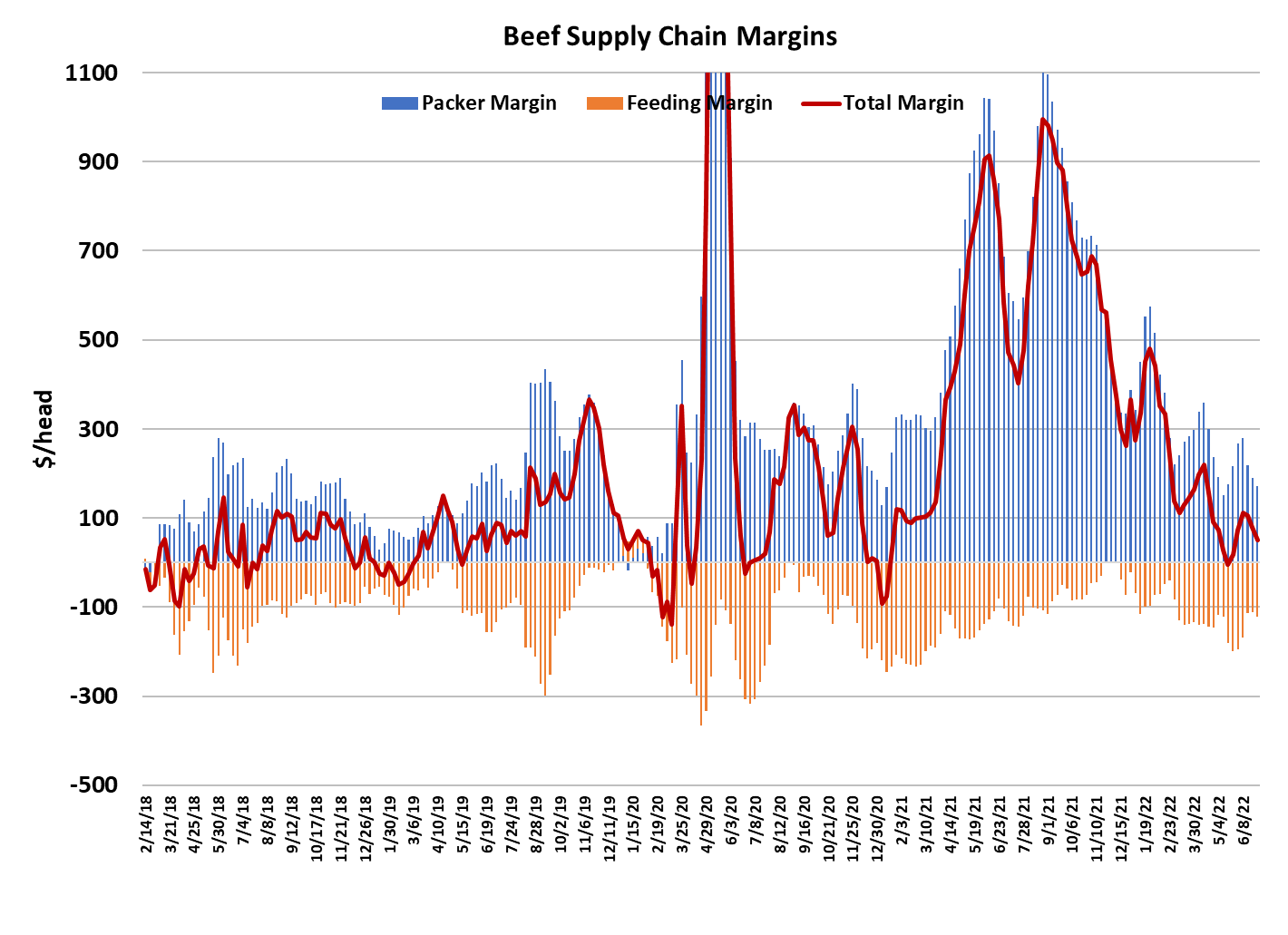

Whatever the cause, this trend toward declining beef prices and

rising cattle prices is wreaking havoc on packer margins. I

calculate this week’s packer margin close to $170/head, down

$20 from the week before. The margin problem could get a lot

worse next week when these more expensive cattle show up for

slaughter. The obvious solution for this margin issue is to slow

kills down, particularly in the Northern areas where numbers seem

to be the tightest. So far, packers have been reluctant to do that,

but the short kills around the Independence Day holiday will

provide a brief kill slowdown. However, it may not be sufficient to

break the cattle market and restore packer margins. This week’s

decline in the Choice cutout was led by the ribs, but at the same

time we saw some surprising strength in the loin cuts.

Toward the end of the week, the loins started to retreat and it now

looks like a pretty safe bet that the middles will be softening

further in the next few weeks. End meats seem to be doing well,

perhaps supported by strong pricing on lean trim, but I wouldn’t

expect them to hold at current levels all summer long. At some

point in July, the end meats are likely to join the middles and

move lower. This has the potential to push the Choice cutout

back down into the $240-245 range by the end of August, if not

sooner. As that happens, packers will need to pressure the cash

cattle market down toward $130/cwt if they want to maintain even

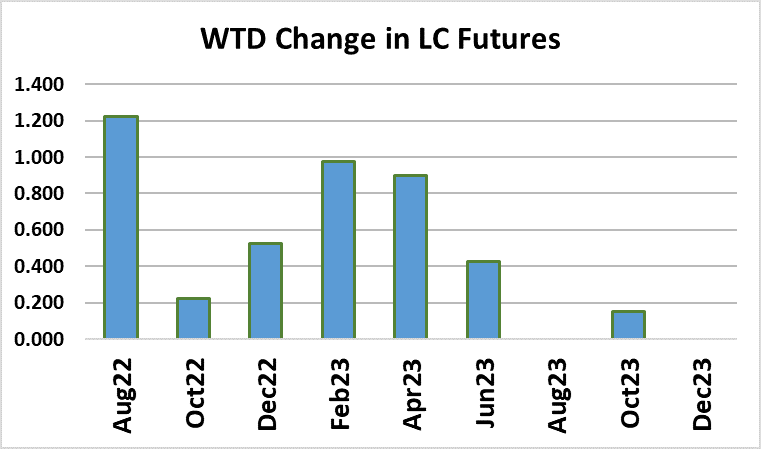

the small margin that they have today. Futures traders cast their

vote on Friday to say that wouldn’t happen and they valued the

Aug contract near $135 the day after the Jun contract expired at

$138.

Jun futures were a dream for Northern feedyards hedging cattle

this year. Those Northern cattle feeders were able to realize

cash pricing north of $145, yet their short futures hedge could do

no better than $138. They likely made a killing on the basis

alone. The combined margin continued lower this week,

confirming that we are back in another demand downcycle. The

combined margin is likely to blow right past the zero line that

marked the bottom in the last cycle. I calculate the average

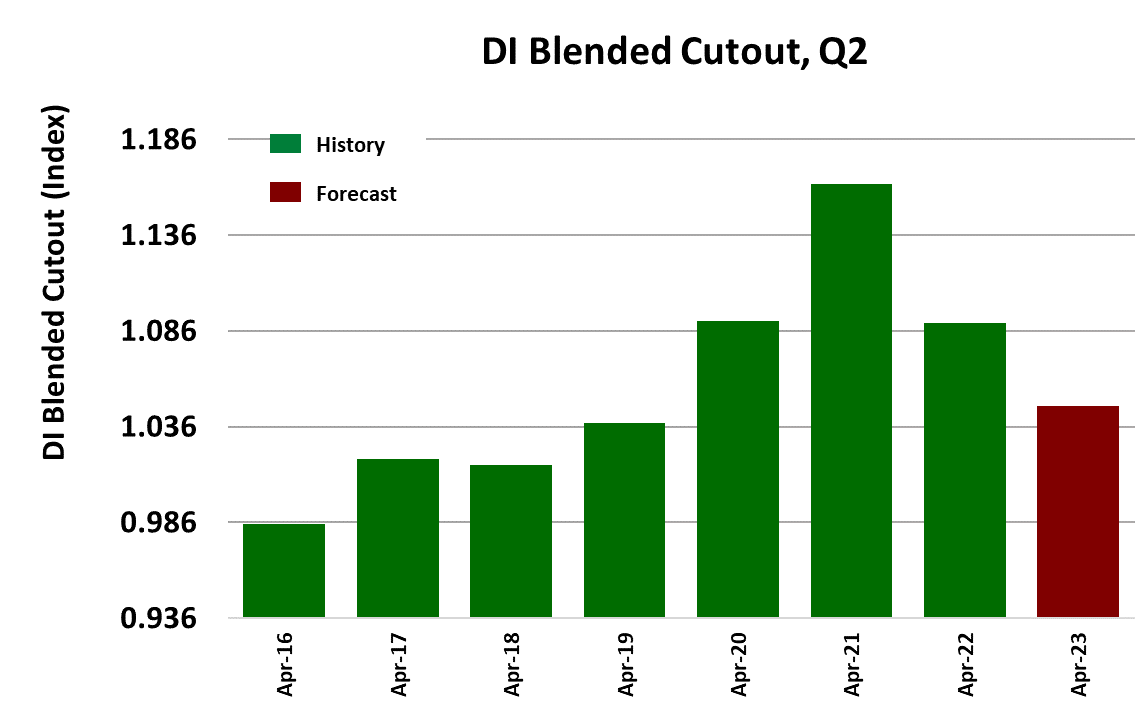

demand index over the May/June period at a little over 1.06,

which is well below the 1.17 average that was posted for the first

four months of 2022. Clearly, demand is moving back to more

normal levels after the great demand bubble of 2021.

There is some risk that I may actually be too high on my

assessment of demand for the second half of 2022, where I’m

carrying an average demand index of 1.095 at present and that

leads me to a Choice cutout forecast for the second half of the

year that averages $247/cwt—about $45/cwt below the second

half of 2021. This week’s fed kill came in at 500k, down 22k from

last week. Packers did a very small Saturday kill in order to

accomplish the reduction. Of course, the kill on Monday will be

almost zero and packers will likely expand next Saturday’s kill in

an attempt to recover the lost production from Monday.

Currently, I’m looking for next week’s fed kill to be close to 455k.

That will tighten up beef availability temporarily so we might see

a brief increase in the cutouts, but I wouldn’t expect it to be more

than a couple of dollars. The market will now have to face a long

dry stretch without any further holidays until early September.

As the dog days of summer set in, the trend should be toward

generally softer beef demand, particularly in the middle cuts.

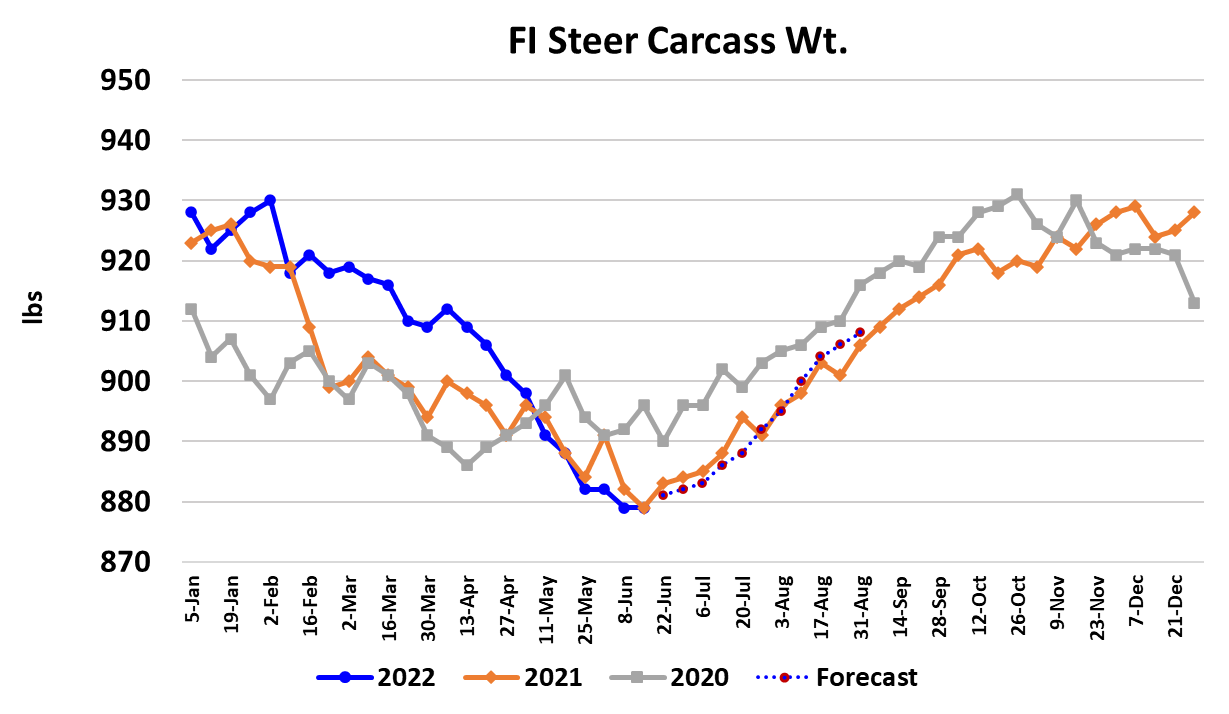

This week’s weight data showed steer weights stabilizing at 879

pounds and the comprehensive report is pointing to an increase

next week so perhaps the bottom in cattle weights is finally in.

Next week, watch for a brief improvement in beef prices followed

by more weakness. Also keep an eye out for softer pricing in the

Northern cash cattle market. That has been expected for a long

time but so far has proved elusive.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}