Beef Wrap July 7

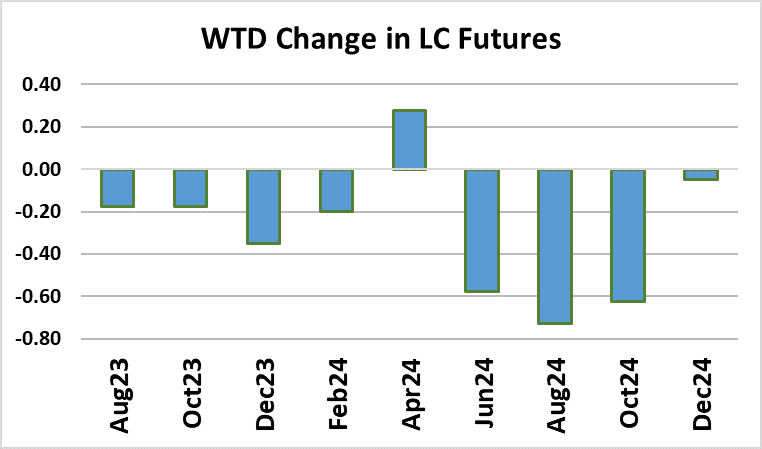

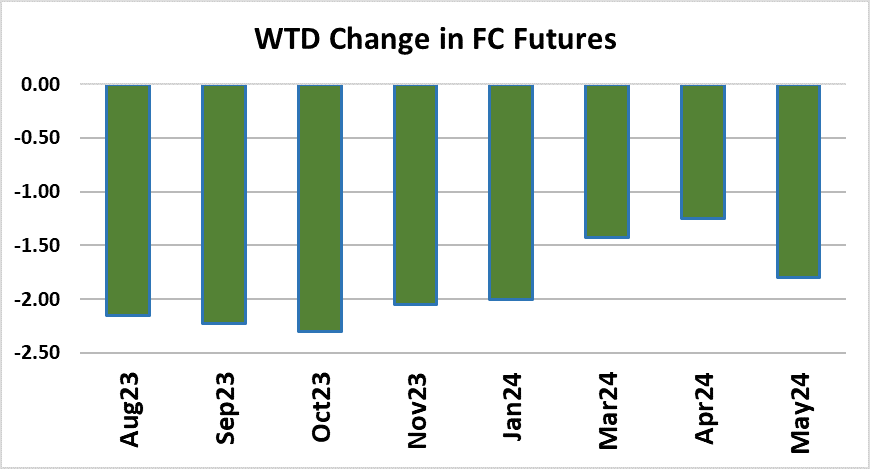

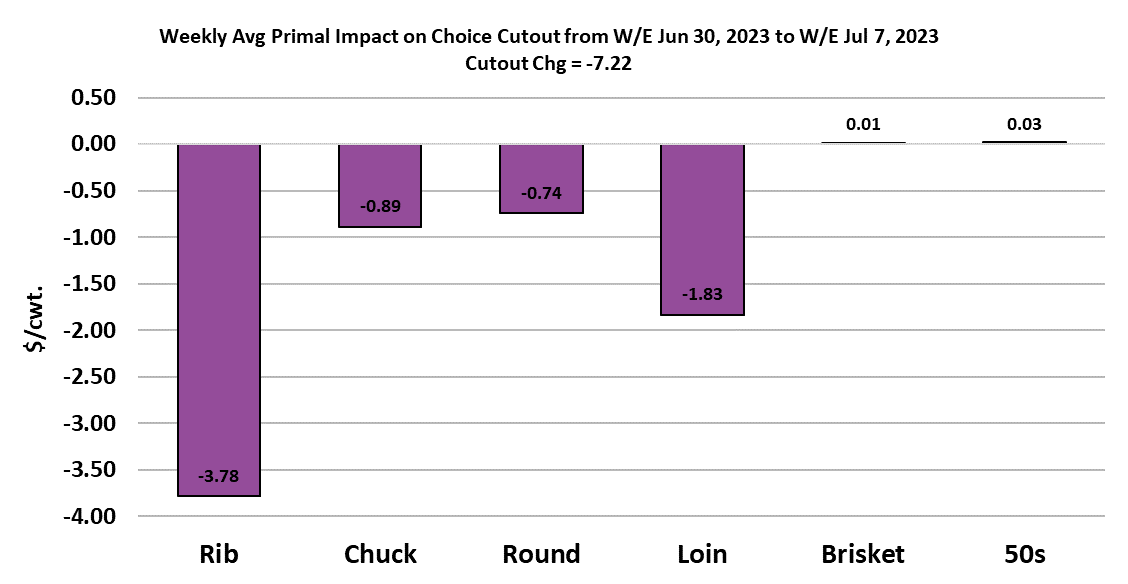

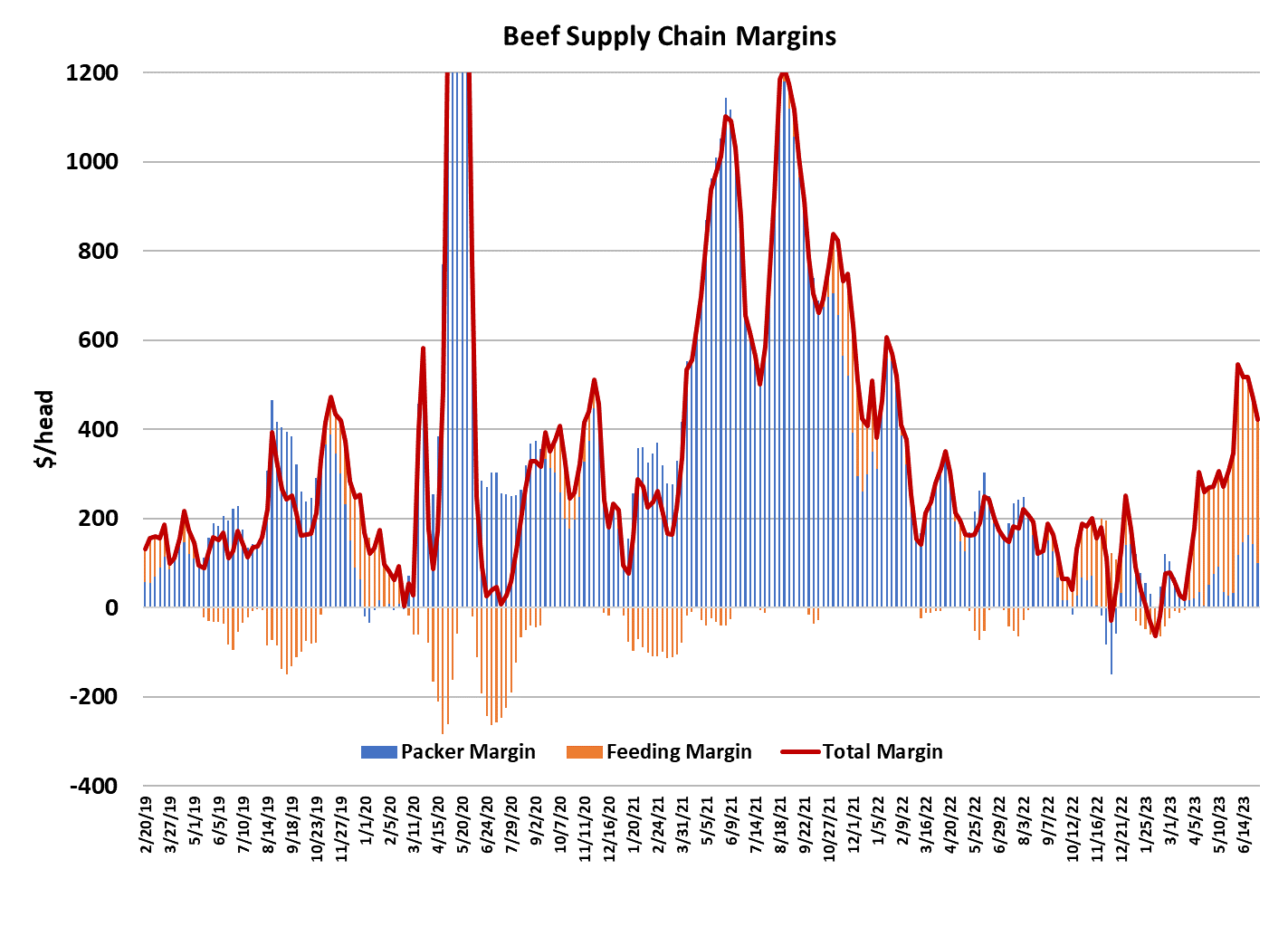

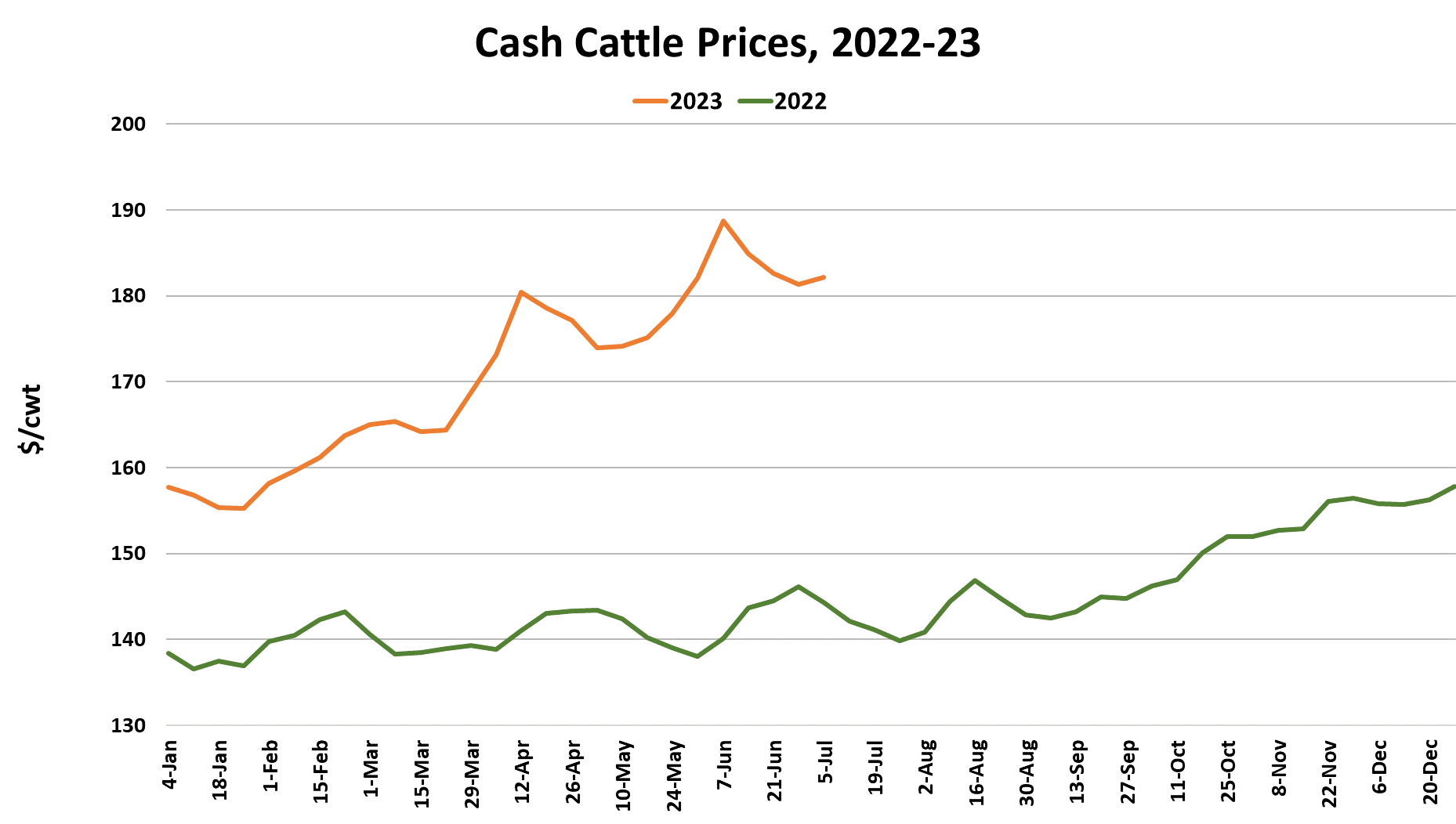

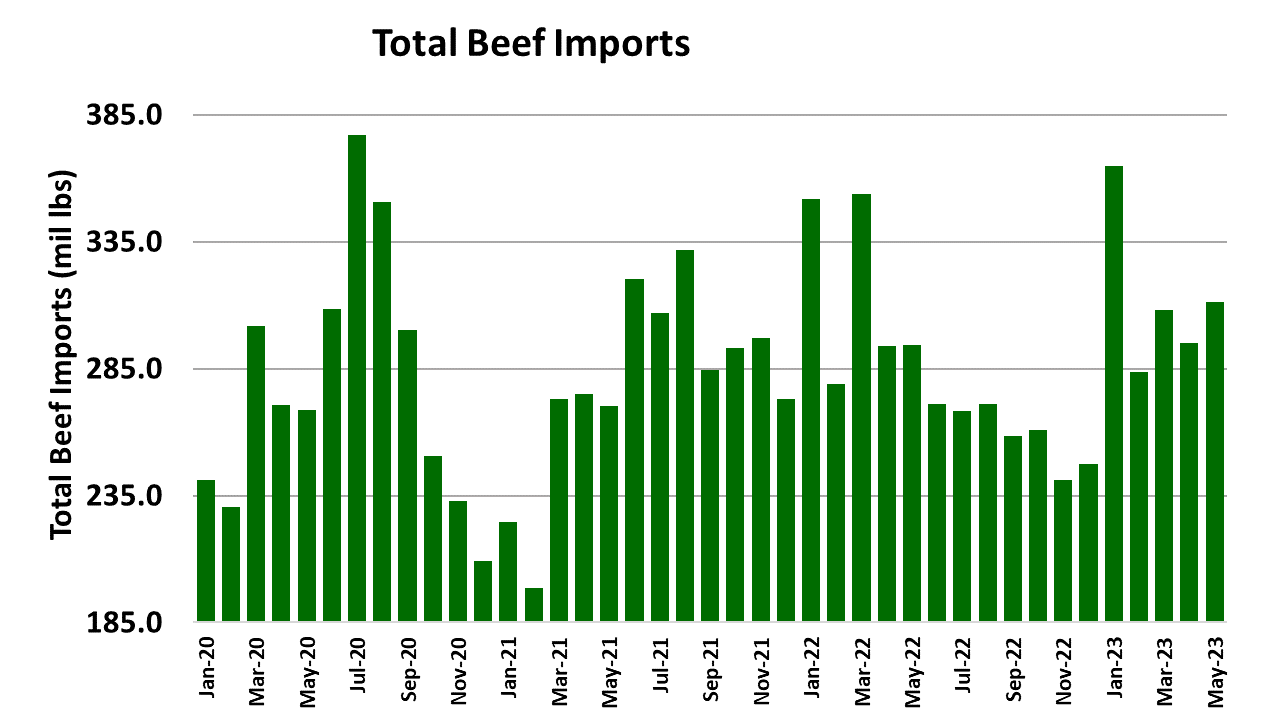

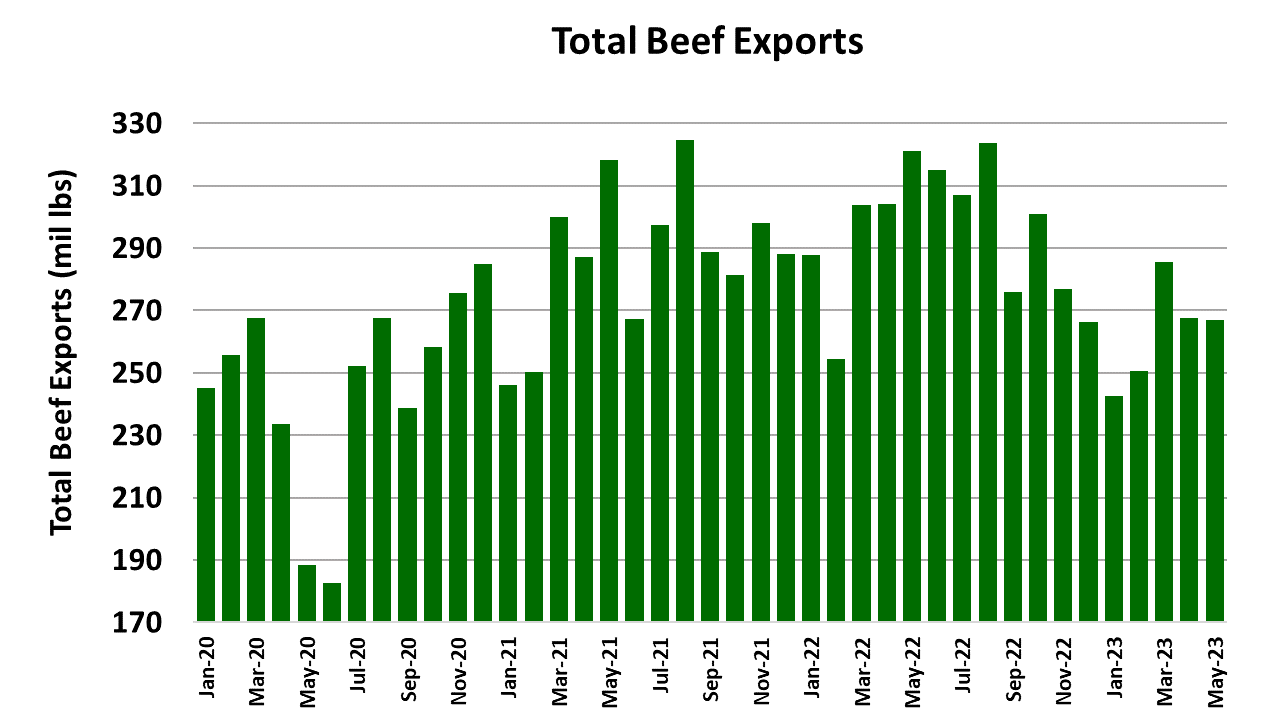

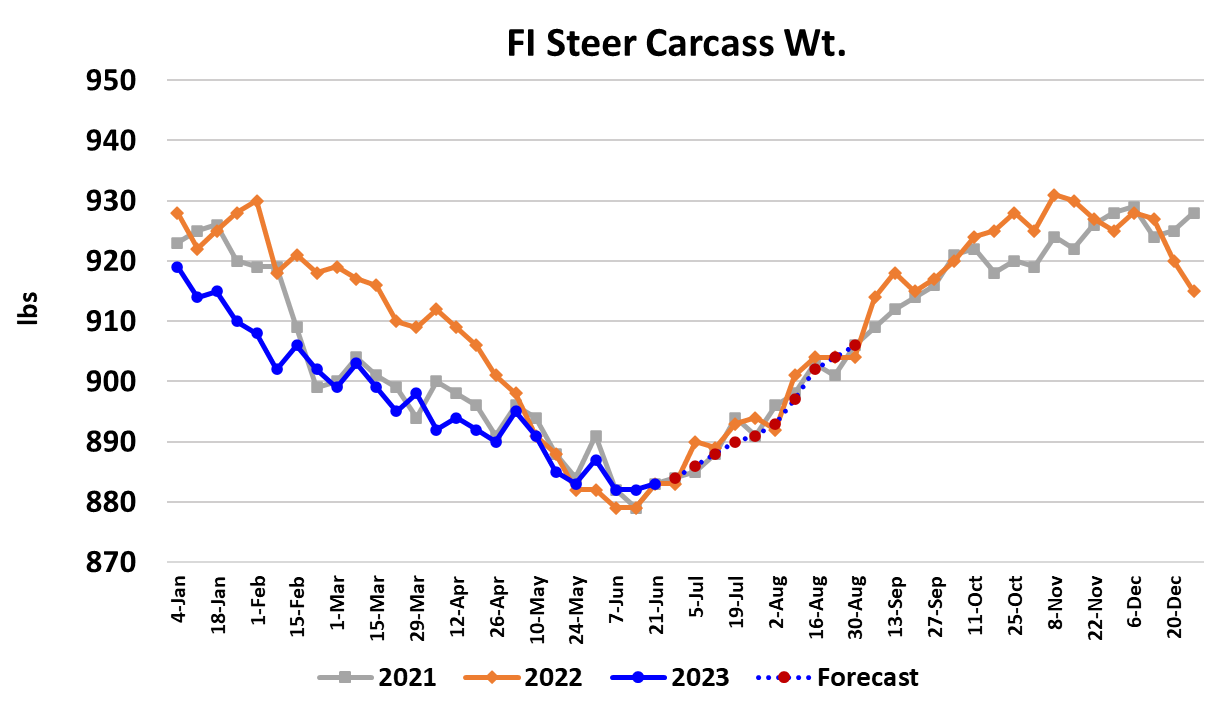

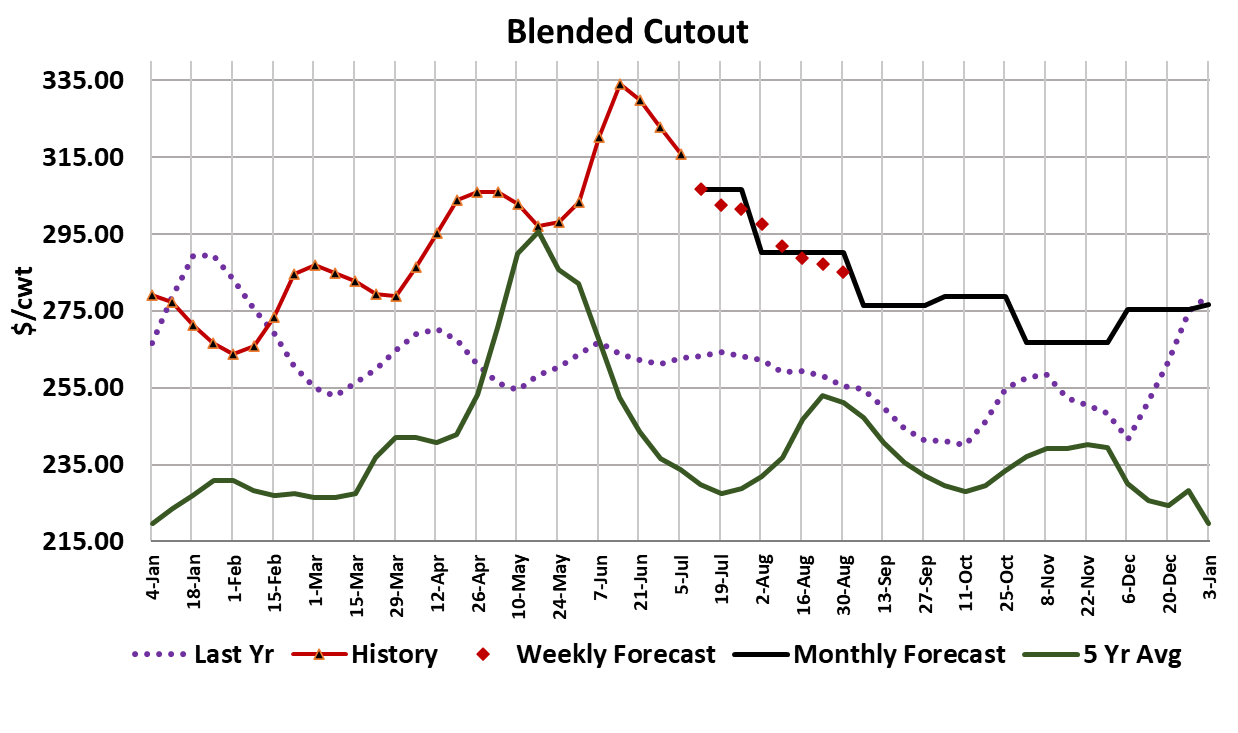

The beef market continued lower this week, with the Choice cutout dropping $7.22/cwt. on a weekly average basis and the Select cutout losing $6.47/cwt. All of the primals were down to some degree, but the middle meats, and particularly the ribs, were the biggest losers. As they watched the beef market unravel, packers tried their best to get cattle bought cheaper, but it doesn’t look like they had much success with that. Once all of the data is reported on Monday, I expect the weekly average live price to be about $182.15, up almost $1 from the week before. In the South, cattle traded mostly steady at $178, but in the North, cattle feeders held out until Friday and finally sold cattle in the $182-185 range, which was steady to $2 over last week’s prices. Clearly, market-ready supplies are not abundant, particularly in the northern feeding regions. Futures traded lower early in the week, but then rallied on Friday as it became clear that packers were going to have to pay up. Nearby Aug now sits at $177, which is only $1 below this week’s trade in the South. One reason that futures traders are showing little fear with respect to the August contract is that they recognize cattle prices have been cycling for much of the past year and a half and this week’s up-move sure looks like it could be the start of another move higher in cash cattle prices. So far this year, the downward price moves have lasted only a few weeks and have been followed by rising prices that peak at a higher highs than the previous cycle (see attached chart). Will that happen again this time? It is hard to forecast higher cash cattle prices at this point in the calendar and, indeed, my fundamental forecast has them drifting lower through July and into August, but I’m not very confident about that. Further, the volume of cattle that packers have bought in the last couple of weeks has been relatively small. That makes me think that they could be forced back into the spot market by the middle of next week and that might result in another price advance. Some will point to the beef market and wonder how cattle prices can advance when beef prices are falling like a rock. Well, in the short run the correlation between cattle prices and beef prices isn’t all that great. It certainly isn’t nearly as tight as what we see in the hog and pork sector. If cattle prices move upward quickly and in big chunks, then packers often can pry more money out of beef buyers, but when cattle prices slowly work higher, it is much more difficult to recoup that loss from the pockets of beef buyers. This week packer margins slipped to just below $100/head, so there really isn’t much justification for needling the beef buyers at this point. However, if the cutouts continue to ease and the cattle market holds steady or advances, packers could see negative margins within a couple of weeks. I am forecasting every primal lower over the next few weeks. Ribs still have considerable downside risk and the end meats normally don’t start to get traction until early August. Even the 50s are starting to look a little bit vulnerable and they have so much air underneath them at the moment that the break could be a pretty sharp one when it comes. So, the near-term picture for the beef looks pretty bleak. I’m not totally convinced that it looks nearly as bad for cattle. For one thing, carcass weights are telling me that feedyards remain very current. The DTDS moved lower yet again this week and is now approaching -20 pounds. Steer carcass weights did tick one pound higher in this week’s FI data, so maybe the bottom is finally in, but it sure doesn’t look like seasonal move higher in weights will be a quick one. This week’s fed kill was only 425k due to the July 4th holiday, so perhaps that might temper the declines in beef prices early next week. However, I see the fed kill bouncing back to about 515k next week and it just doesn’t feel like the beef market can handle production of that size without further price concession. The combined margin moved lower again this week and now it is pretty clear that we are in a near-term demand downcycle that could easily last another month before it bottoms. Retailers probably won’t be inclined to lower consumer-facing beef prices even though the Choice cutout has lost close to $20/cwt. over the past three weeks. In fact, retailers are probably still raising prices to catch up with the late May/early June surge in wholesale beef prices. That could slow consumer off-take and necessitate that packers cut back on the kill later this summer or face deeply red margins. Today’s US employment data continued to point to a strong jobs market and increasing hourly earnings, so the probability of a recession later this year seems to be slowly diminishing. There is even talk that the Fed might manage to pull off a “soft landing” and tame inflation without having to cause a serious recession. Time will tell on that. USDA released the monthly export data today and it showed total beef exports down nearly 17% YOY during May. That shouldn’t be too surprising given how strong US beef pricing has been. Imports were reported up 5.7%. I think that is reasonable to expect continued YOY declines in exports for a least a few more months and that will probably be accompanied by modest YOY increases in imports. Next week, look for further pressure on the cutouts as production ramps back up following the holiday week. The cash cattle market may be a different story. Stay tuned.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}