Beef Wrap June 24

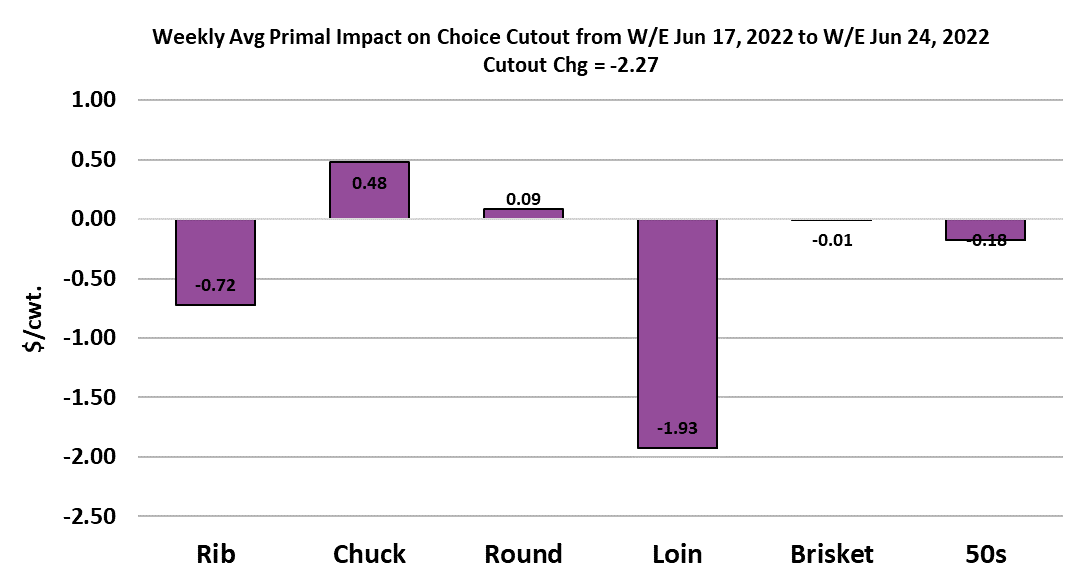

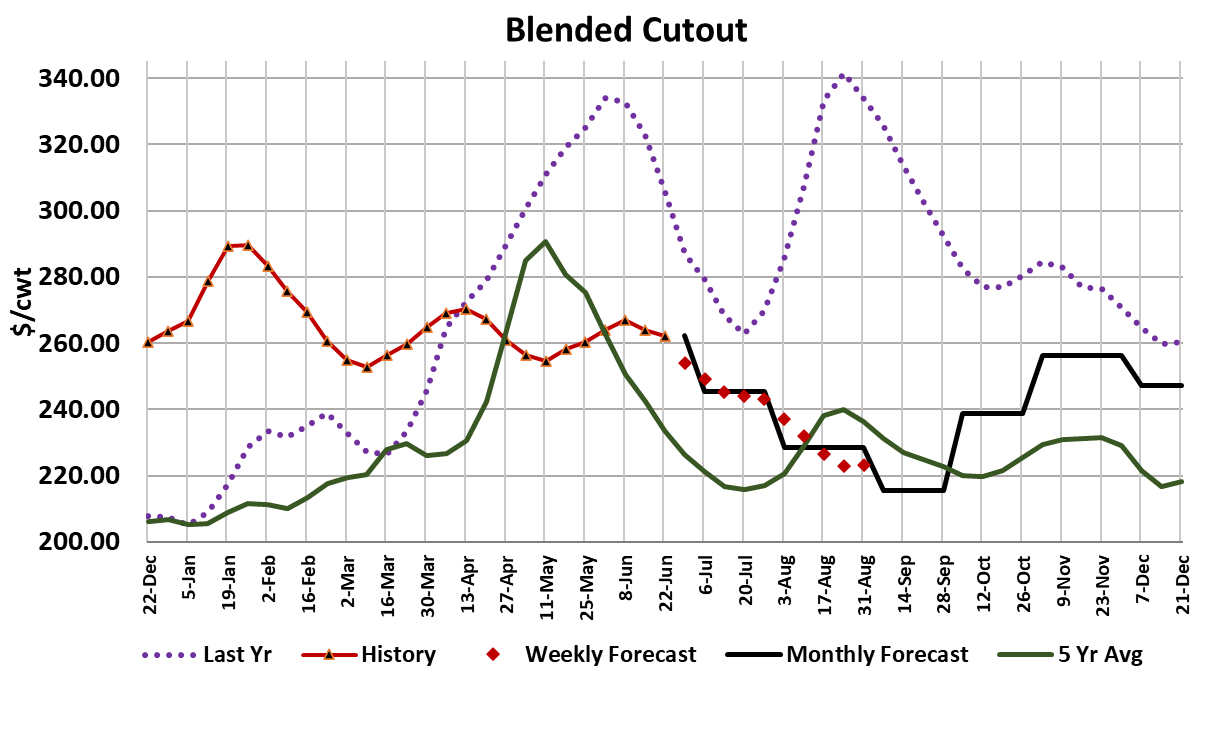

Beef packers’ margin situation got a little more precarious this week as the

cutouts turned lower yet cash cattle continued higher. On a weekly average

basis, the Choice cutout lost $2.27/cwt and the Select was down $0.56/cwt.

Thus it looks like the rally in boxes that began in mid-May has now run its

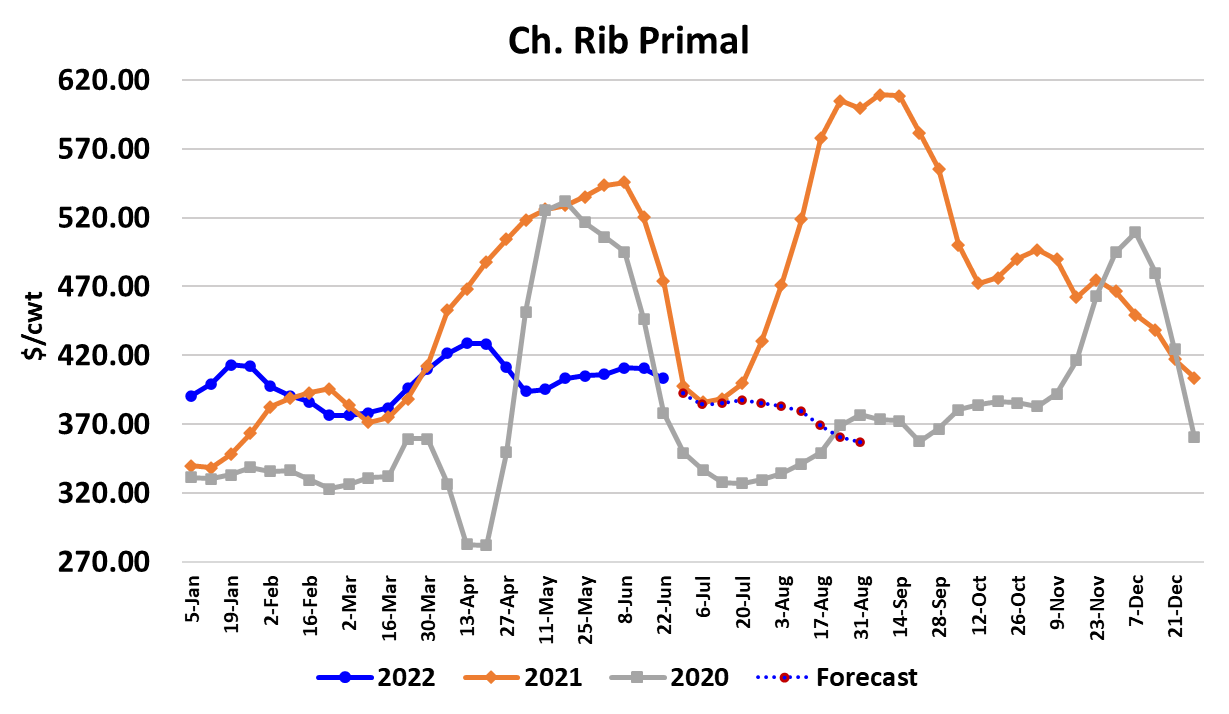

course. The attached chart shows that it was the middle meats that were

responsible for pushing the cutout lower this week. The chuck, which

traded higher, tried to help, but fell short. With Father’s Day now behind us

and all of the buying for July 4 now completed, it isn’t too surprising that the

middles would come under pressure. It seems to me that this was just the

first step in a series of weekly price declines for middle meats. In addition

to the weakness in the middles, fat trim finally posted lower pricing this

week. That could be related to the completion of July 4 buying, or it could

be that kills have just been so big lately that some supply-side pressure is

beginning to show up in the trim. Lean trim seems to be holding up very

well and we saw the 90s price gain about $2 this week.

As the macroeconomic conditions deteriorate over the next few months, it is

reasonable to expect stronger ground beef demand and weaker middle

meat demand as consumers increasingly trade down toward cheaper

proteins. While the beef market was struggling this week, the cattle market

continued to advance. The average price of cash cattle increased almost

$1 to $144.50. Cattle in the North traded at $146 or better and in the South

the trade was at $138 or a little lower. That is a huge regional price

differential. Back in pre-pandemic times, when cash prices differed that

much between regions, packers would buy cattle in the low price region and

then truck them to the higher price region. They would usually only need to

do that for a few weeks before prices would equalize. Now I’m wondering if

this big price differential is persisting because of a much higher cost to

transport cattle. High fuel costs and shortages of truck drivers might be

making it cost-prohibitive to buy cattle in one region and slaughter them in

another. Regardless of the cause, the inability of packers to get cattle

bought cheaper is going to become a real problem in the weeks ahead as

the cutouts move lower.

I calculate this week’s packer margin at $155/head and am projecting

margins less than $100/head in the coming weeks. Cattle feeders, on the

other hand, are seeing their margins improve. The combined margin turned

lower this week and it now looks like the industry has moved back into a

demand downcycle. Close inspection of the combined margin chart

indicates that the last 4 demand cycles have peaked at lower and lower

levels. The most recent demand cycle was particularly anemic and it looks

to me like the combined margin will be in negative territory soon. Given

that feedyards are full of cattle, the combination of weaker demand and big

supply points to lower cattle and beef pricing down the road. This week’s fed

kill came in at 523k, almost identical to the week before. Next week, I

expect that packers will leverage the holiday weekend to do a very small

Saturday kill and thus keep the fed kill in the 500-510k range. It is the

perfect excuse to cut the kill and make it look like they want to be nice to

their workers by giving them a long weekend. The official July 4 holiday is a

week from Monday, but it is common for packers to pull back on the

Saturday before when the holiday falls on a Monday.

Then the following week, there will be no kill on Monday and so the fed kill

might fall as low as 470k. So for the next two weeks packers have a prime

opportunity to cut kills and hopefully strengthen their margins. The smaller

kills might not be enough to boost the beef market, but it almost certainly

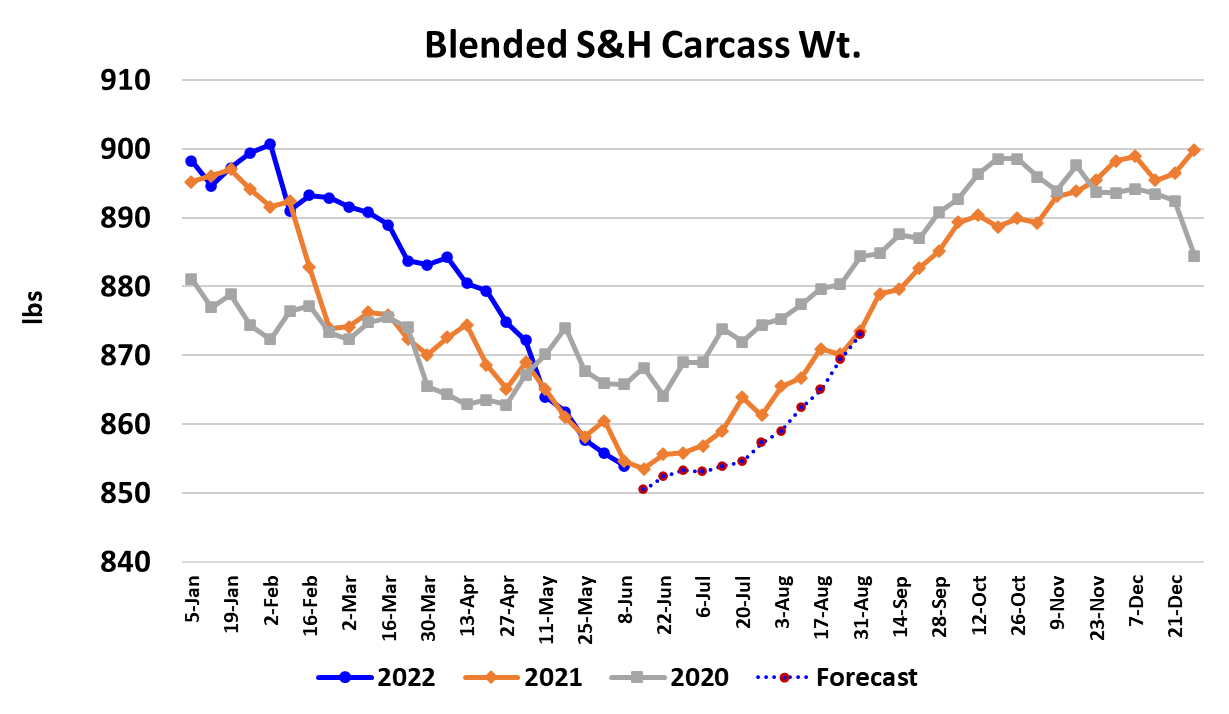

will help stop the price increases in the cash cattle market. Cattle carcass

weights continue to drop. Steer weights were reported down another 3

pounds this week. We are way beyond the normal point in the calendar

where weights bottom. If nothing else, the upcoming short kill weeks will

likely cause carcass weights to turn higher. The DTDS weights continued

to plunge this week, dropping to -10 lbs after registering +30 lbs just a few

weeks back. There are a number of theories floating around about why

packers keep having to pay up for cattle when the number of cattle on feed

is record large. One of them is that they are “chasing the grade”. Another

is that they need to fill previously booked orders.

But the weight data is very clear and it tells me that a lot of cattle are just

not ready for slaughter right now. Maybe it is the heat or maybe it is a

change in rations by cattle feeders, but the front end supply is quite current

judging by what weights are telling us. It is true that there are record

numbers of cattle in the nation’s feedyards, but that supply must be tilted

more toward July and August than June. USDA gave us another look at

the cattle supply in today’s Cattle on Feed report. They pegged

placements during May down 2.1% and June 1 on-feed totals up 1.2% and

the largest on record for this time of year (since 1996). The placement

number was about 2% smaller than what analysts were expecting, so it

might generate some buying in the futures on Monday, but I believe that

traders are now more focused on potential demand problems down the

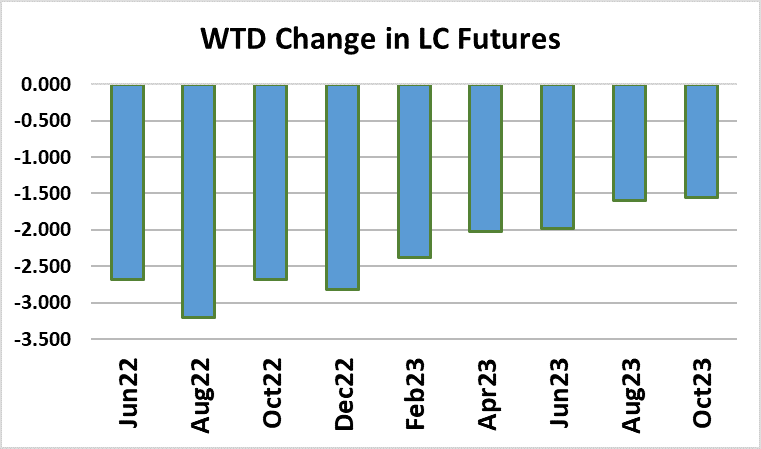

road and so any rally generated by the COF numbers is likely to be shortlived. This week the contracts on the front end of the futures curve lost

between $2.50-$3.00 as traders grew increasingly concerned about what

high inflation and a cratering stock market would mean for beef demand. I

definitely agree with them that these are the things that will determine

pricing across the complex in the coming months.

Gasoline prices have started to ease a tiny bit but still remain very high and

with each passing day that is putting more strain on consumer’s budgets.

Interest rates are rising and it won’t be long before that starts to seriously

impact housing prices. Declining housing values are a lot like declining

stock prices—it makes consumers feel poorer and thus curtail spending on

non-essentials. We can already tell from the combined margin chart that

beef demand is way off of its 2021 levels. So beef demand is coming into

this period of macro headwinds in an already weak position. That causes

me to think that things could really get ugly on the demand side over the

balance of the year. Buyers would be wise not to extend coverage very far

into the future unless it is at price levels much lower than what we see

today. Next week, watch for further erosion in the cutout and keep an eye

on the Saturday kill because if it is exceptionally small that might be the

straw that breaks the cattle feeder’s back and finally gets cash cattle prices

heading lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}