Beef Wrap January 7

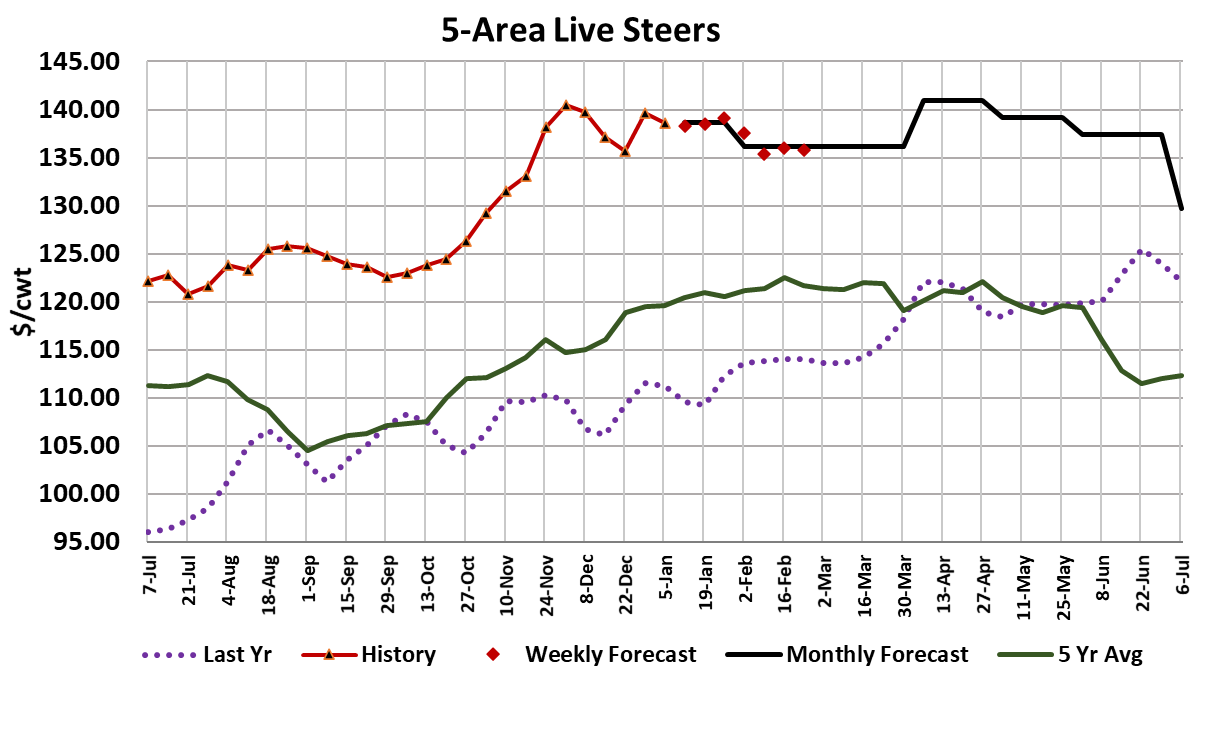

Cash cattle were mostly lower this week, with the weekly average

dropping a dollar to $138.58. It doesn’t look like packers bought

very many cattle either. That could be because some producers

didn’t want to let them go cheaper, but my guess is that packers

have so much uncertainty around their labor supply for the next

couple of weeks that they don’t want to over-commit on cattle

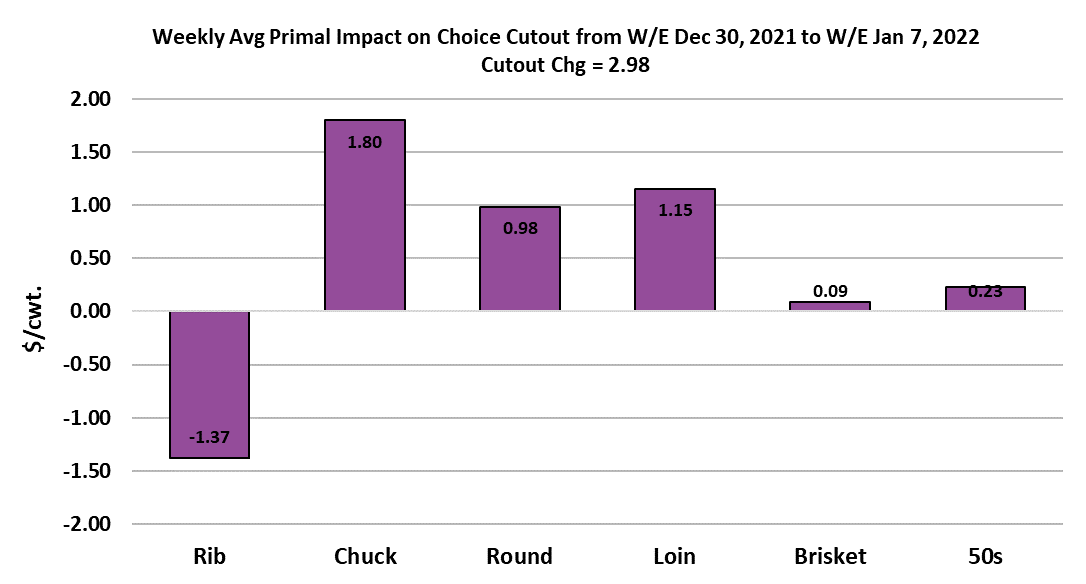

supplies. The cutouts were higher this week, with the Choice up

$2.98 on a weekly average basis and the Select up $3.25. I’ve been

saying that omicron would be the big story and that seemed to be

the case this week. Case counts are soaring and consumers seem

to be hitting the grocery stores hard. That has probably created

some additional fill-in business from the retail segment and moved

the cutouts upward.

Chucks, rounds and loins put upward pressure on the Choice cutout

while the ribs continued to be a drag on it. The surge in omicron

cases has created absenteeism all along the supply chain, not just

at packers. Trucking, distribution and retail are all dealing with a

shortage of workers. Packers are certainly seeing their share of

employees calling in sick and that has tempered the kill in recent

days and resulted in a number of daily slaughter estimates being

revised downward. The total fed kill this week only amounted to

485k, down from about 515k in the weeks just prior to the holidays.

Normally, the first week back from two holiday weeks would result in

a very robust kill, but not this year. It is almost like we had three

holiday weeks in a row. Next week might not be any better and I’m

penciling in another 485k fed kill. Even the cow kill was affected

with the weekly total there coming in at 135k, about 10k below what

I would have expected had packers been able to run like they

wanted. This just means that beef availability is going to tighten up

for at least a couple of weeks and I think we can expect the cutouts

to keep moving higher as a result. This kill slowdown comes at a

bad time for cattle feeders. I’ve already highlighted that carcass

weights have been running heavy and now they may stay heavy

longer than expected.

There was some cold weather in cattle country this week, but next

week is looking very mild and the amount of precipitation has been

very light. Thus weights could continue to be a problem and may

reduce cattle feeder’s leverage in the cash market over the next few

weeks. As a result, I’ve got cash cattle prices steady-lower through

January. Of course, if that comes true then packer margins will

widen back out again, because beef prices are likely to rise. This

week, margins clocked in at $350/head. Some observers are

wondering if the recent saber-rattling by the Biden administration will

cause beef packers to pay up for cattle even if they could get away

with paying less.

I guess that is possible, but I don’t really think packers are too

worried at this point. Every few years the packers come into the

crosshairs from activists complaining that they have too much

market power and that is hurting cattlemen. It never amounts to

anything. The appropriate way to deal with packer concentration is

through an anti-trust enforcement action and no one has ever been

able to produce enough credible evidence of collusion among

packers to make that a viable option. I doubt the current

administration will have any success in that area either. Now price

levels on all sorts of goods are going up and consumers are

bemoaning price inflation. If we get rid of the large packers and

their economies of scale and replace them with smaller plants that

have a higher cost structure, meat is going to cost more.

When a margin player like a beef packer has a higher cost structure,

he recoups that through some combination of higher beef prices and

lower cattle prices. Is that what cattle producers really want?

Probably not, cattle producers might very well find themselves

getting less for their cattle if the industry is comprised of lots of small

plants rather than a few large ones. The daily demand scatters have

indicated that spot beef demand is again moving higher, but the

combined margin made a tick downward this week. I’m thinking that

is just a brief anomaly and the combined margins will soon start

working higher. It is important to keep in mind however, that this is

just a short term improvement in beef demand and the longer-term

demand trend is lower. It is very doubtful that we can maintain the

level of demand from last year in 2022. Right now demand is still

pretty good, but my expectation is that the air slowly leaks out of the

demand bubble and by the second half of the year, demand is way

below what we saw in 2021. USDA released the official trade data

for November today and it showed beef exports up 7.6% YOY and

beef imports up a whopping 28% YOY. The quantity of imports was

almost exactly equal to the quantity of exports at 298 million pounds.

Mexico has been a big driver of US beef imports recently.

Per capita availability during November was 7.1 pounds per person,

up 6% from last year. Even though availability was way up this

November, the blended cutout was almost 25% above last year in

November. That is evidence of just how strong beef demand has

been. Next week, look for the cutouts to move higher on reduced

availability from this week’s small slaughter and the cattle market to

be steady at best.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}