Beef Wrap December 31

The cash cattle market bolted higher this week, averaging $139.88,

up a little over $4 from last week’s average. Packer inventories were

running low after two weeks of very light purchases and they needed

to restock ahead of next week’s return to a full slaughter schedule.

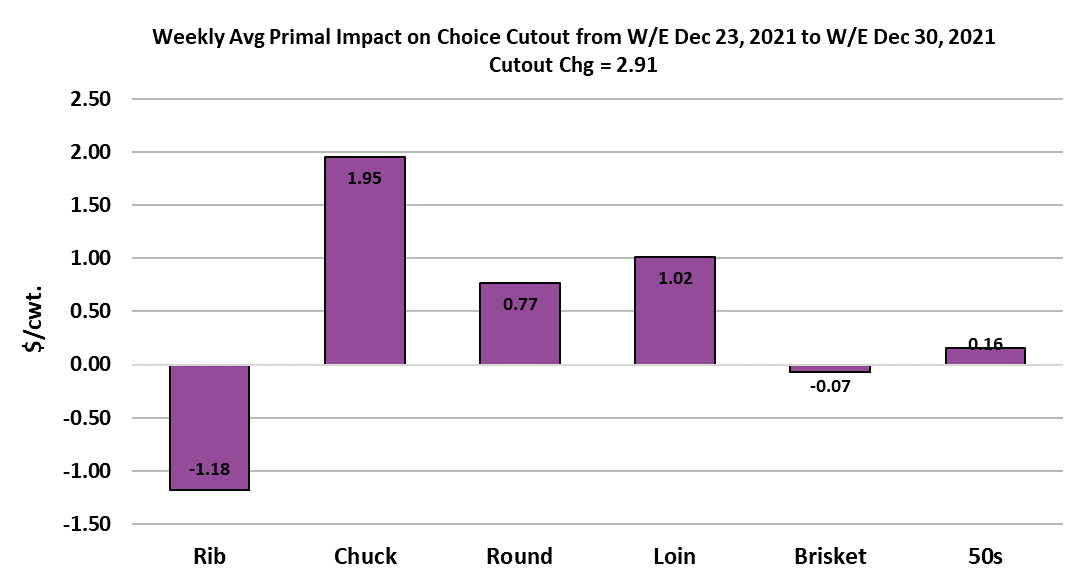

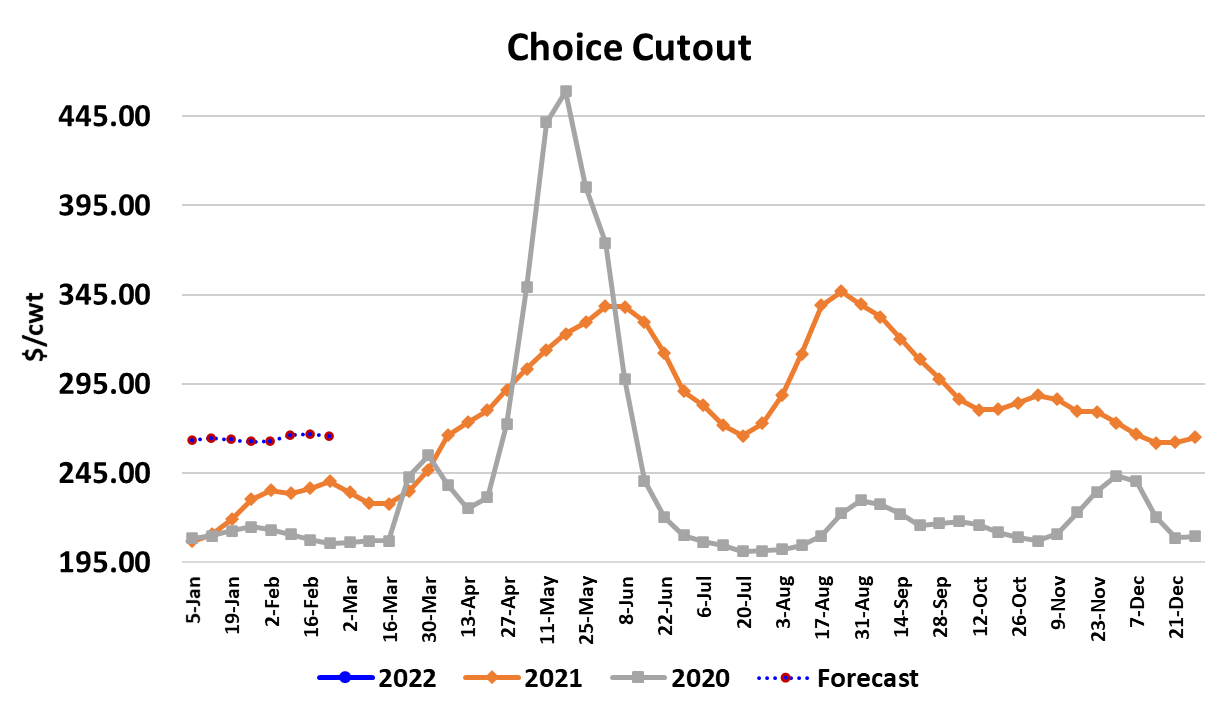

Beef markets also turned a bit higher, with the Choice cutout up $2.91

and the Select gaining $5.56. As market participants put the holiday

season behind them and look into early 2022, they see a tremendous

amount of uncertainty caused by soaring COVID infections in the US.

Will consumers be so sick next week that they just curl up in a ball

and fail to visit grocery stores or restaurants? Will beef processing

plants be able to run full schedules or will soaring absenteeism cut

near-term kills? These are the questions that will determine the

direction of prices in the near-term.

So far, packing plants appear to be operating at levels similar to

before the COVID surge, but the wave of infections has not yet been

fully felt in the heartland where many of the packing plants are

located. Cases have spiked initially in the coastal metropolitan areas:

NYC, Florida, California, and are now rising rapidly in the Deep

South. However, we have yet to see big increases in states like

Nebraska, Kansas, S. Dakota and Oklahoma. That will likely come

in the next two weeks and market participants should be bracing for it.

Meanwhile, retailers have shifted the focus of their early January ads

toward roasts and away from middle meats. The impact can be seen

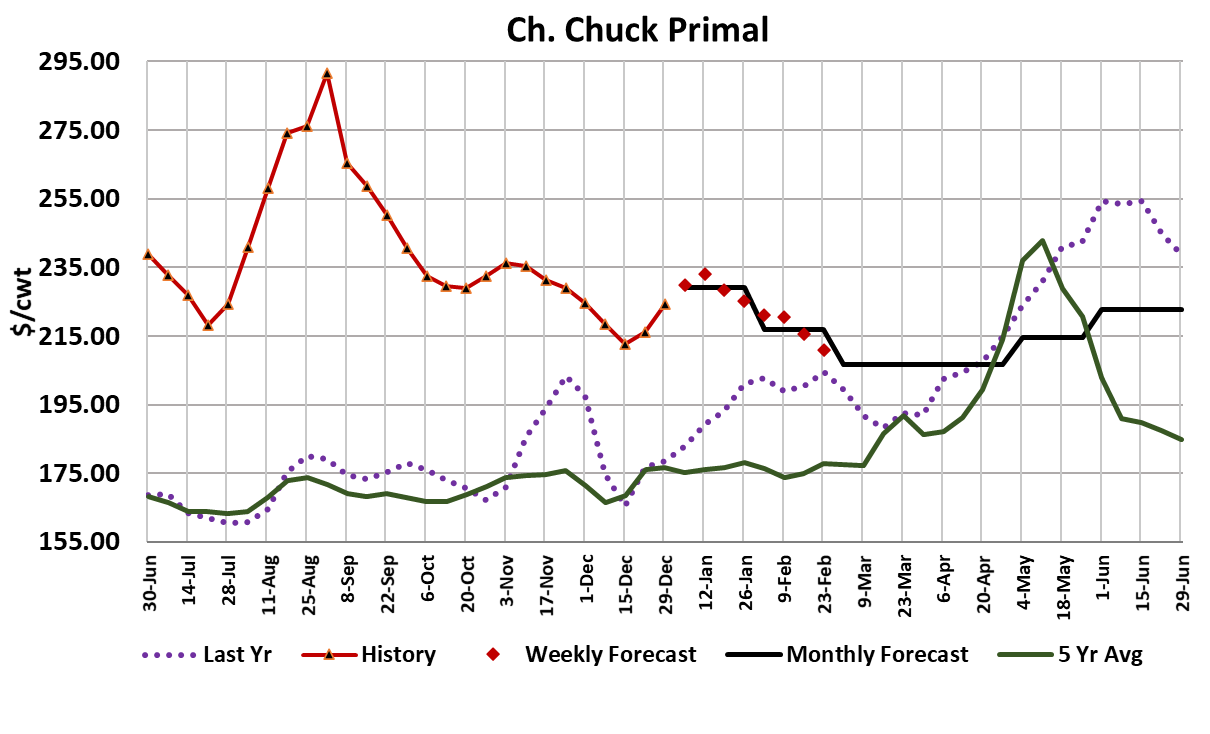

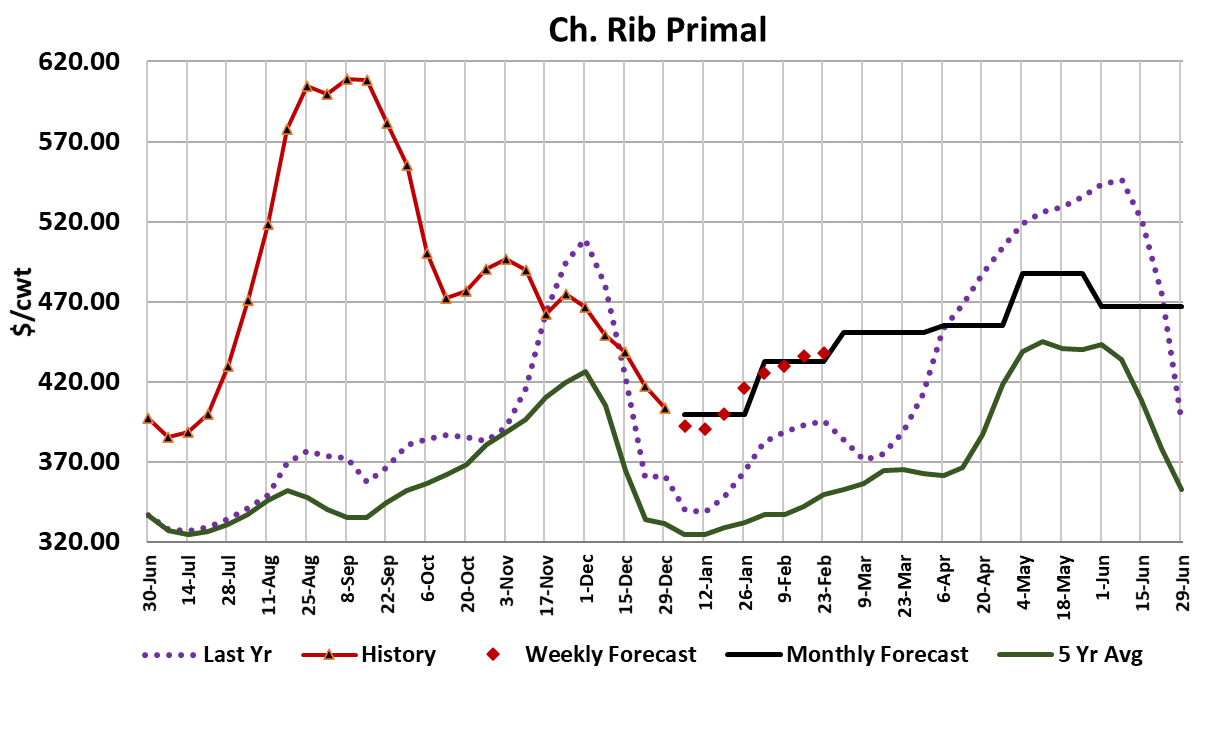

in the wholesale markets where the chucks provided the most cutout

support this week and the rib primal was weighing on the cutout. We

look for that pattern—end meats stronger, middle meats softer—to

continue for much of January and the net effect might be that the

cutout hold steady to perhaps a little higher. Much will depend on

how much production packers can crank out of the plants.

If omicron infections force packers to cancel shifts or run lighter ones,

then the cutouts are likely to push higher quickly, but if packers find a

way to keep the plants humming at full speed, then big gains in beef

prices are a lot less likely. One might expect beef buyers to try and

get ahead of any production slowdowns by ordering aggressively, but

so far we haven’t seen that. Maybe there is enough uncertainty about

how strong store sales will be with case counts soaring that they don’t

want to over-commit. My guess is that we will see a strong shift

away from foodservice over the next few weeks and retail sales will

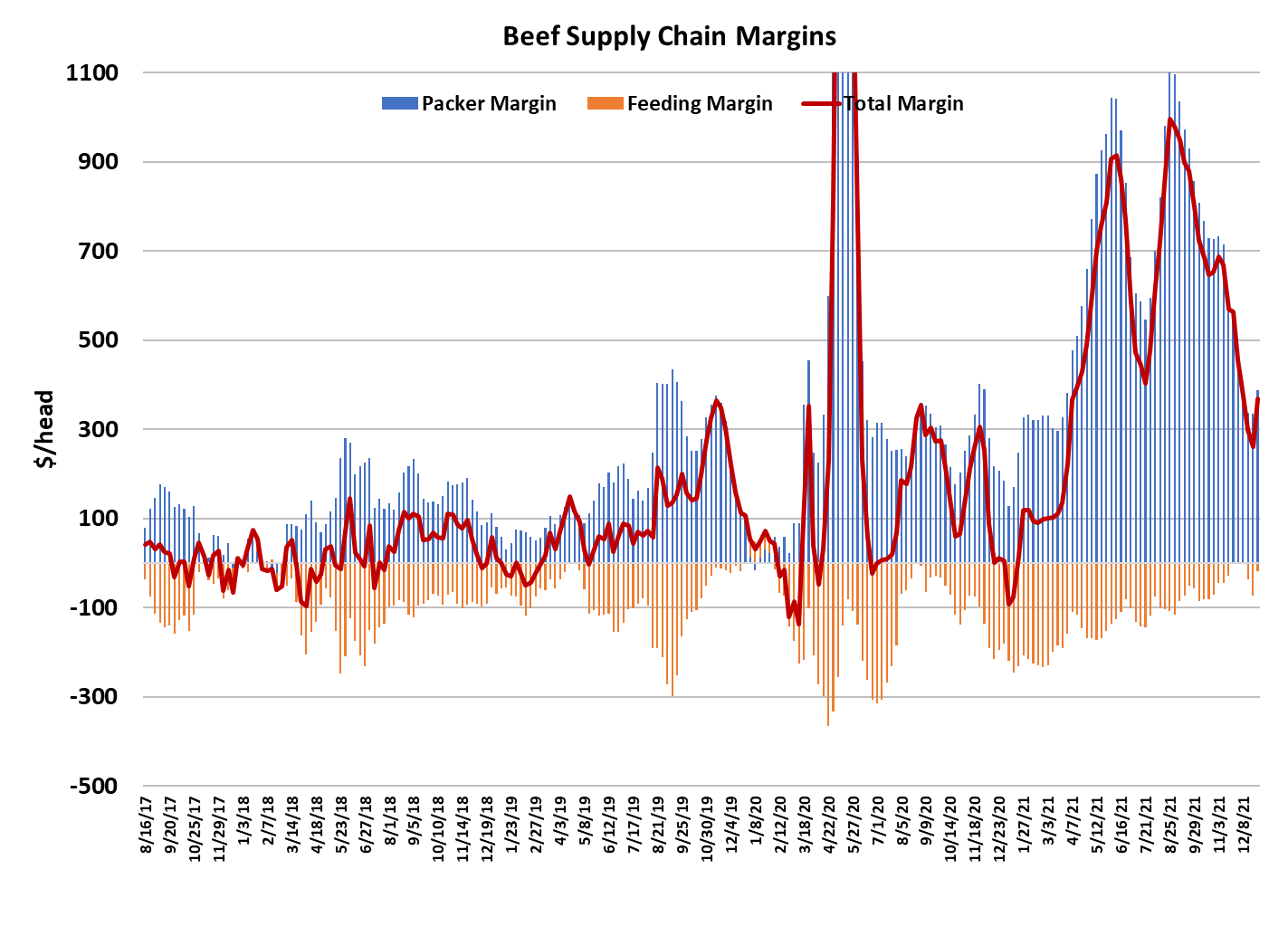

be very strong. The implied margin chart below suggests that beef

demand has started to cycle higher and that will likely carry on for

several more weeks. In addition, international buyers will be back in

full force after the holidays and we could see a fairly strong pull from

that sector.

So, the potential is there for higher cutouts in January if the virus

surge doesn’t make consumers curl up in a ball. Available cattle

supplies should be a bit tighter in Q1 than they were in Q4, but that is

a normal seasonal pattern. Absent any plant disruptions, I look for fed

kills during January to average around 500k per week. Data on this

week’s kill won’t be available until Monday, but my forecast has this

week’s fed kill coming in around 405k. The flow model suggest that

the number of animals coming to slaughter in Q1 will be about 4.7%

below last year, but last year kills were quite strong in Q1. Heavier

carcass weights could help to offset some of the tightness in animal

numbers, but I still see Q1 fed beef production down about 2%. Steer

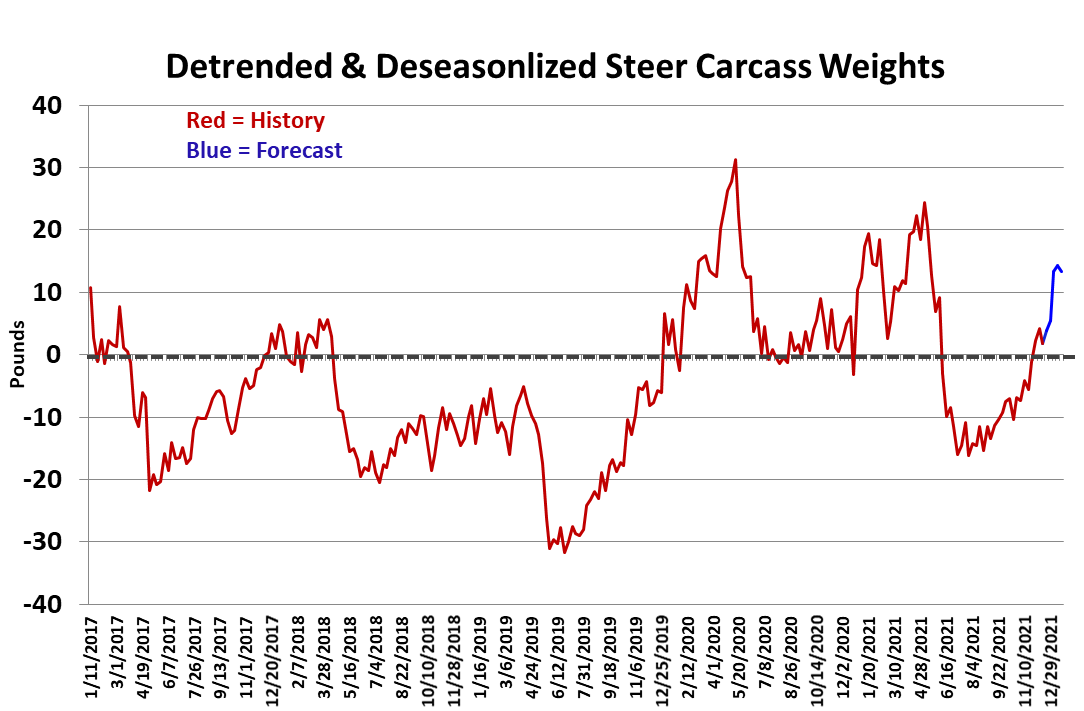

weights were reported down five pounds this week in data that was

for the last week prior to the holidays.

Fed weights are running about 2 pounds over last year and last year

at this time carcass weights were very heavy. The Northern Plains

states are in the grip of a cold snap right now and the forecast has

another frigid period set for next week. The risk of huge snow events

seems minimal in the near term however and those are usually what

cause rapid declines in carcass weights. The DTDS weights are now

solidly above zero and at their highest level since last spring. That

will provide a bit of a buffer if the winter weather should get nasty in

the next few weeks, but if a mild pattern re-emerges, we could see

weights remain heavier than expected. The alarm bells should start

to go off if the DTDS exceeds +10, so we should be watching that

closely over the next few weeks. Weights normally decline steadily

from this point until mid-April, but if COVID infections slow the

slaughter rate here in January, we would likely see weights decline

less-than-seasonal or maybe even post some small gains.

The fact that carcass weights are already quite elevated increases the

risk to cattle feeder’s leverage as we move into the period of

production uncertainty due to soaring COVID infections. The futures

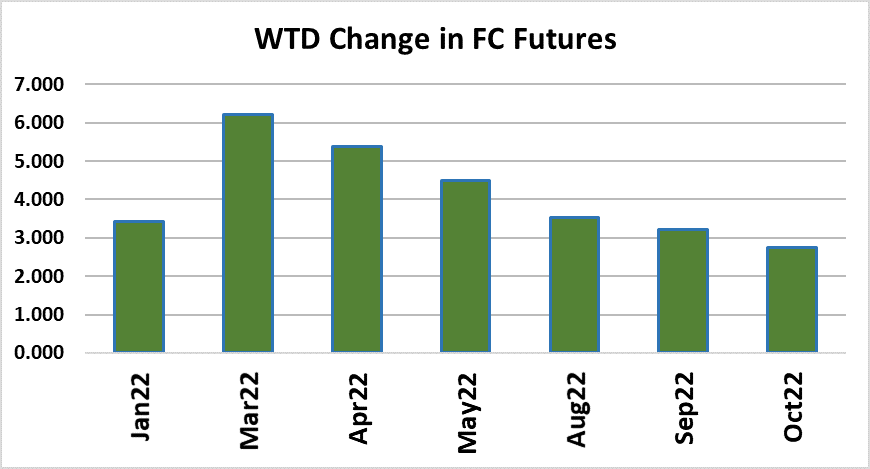

market posted gains this week as it became clear that the cash

market was going to trade higher. The Dec contract gained the most,

while the rest of the curve was less enthusiastic. Feb is now priced

close to even with the current cash market, indicating that traders

think the cash market doesn’t have a lot more upside from here. Next

week, the key variable to watch is rising covid infections, and how

consumers and processing capacity react to them. This will be the

main story for the next few weeks and the main determinant of market

direction.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}