Beef Wrap January 14

Cash cattle traded $2 lower this week, averaging close to $136.50.

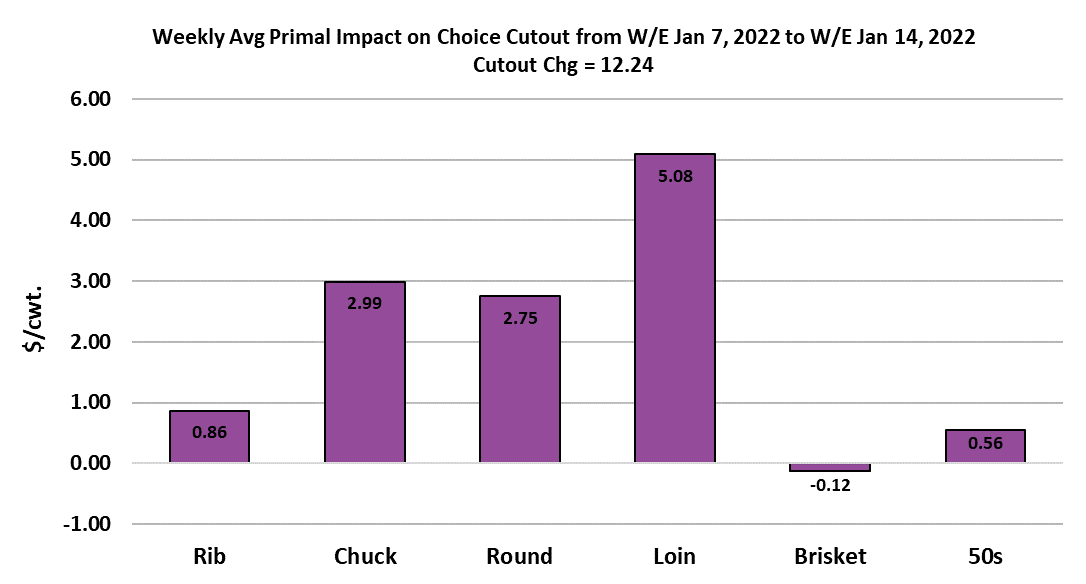

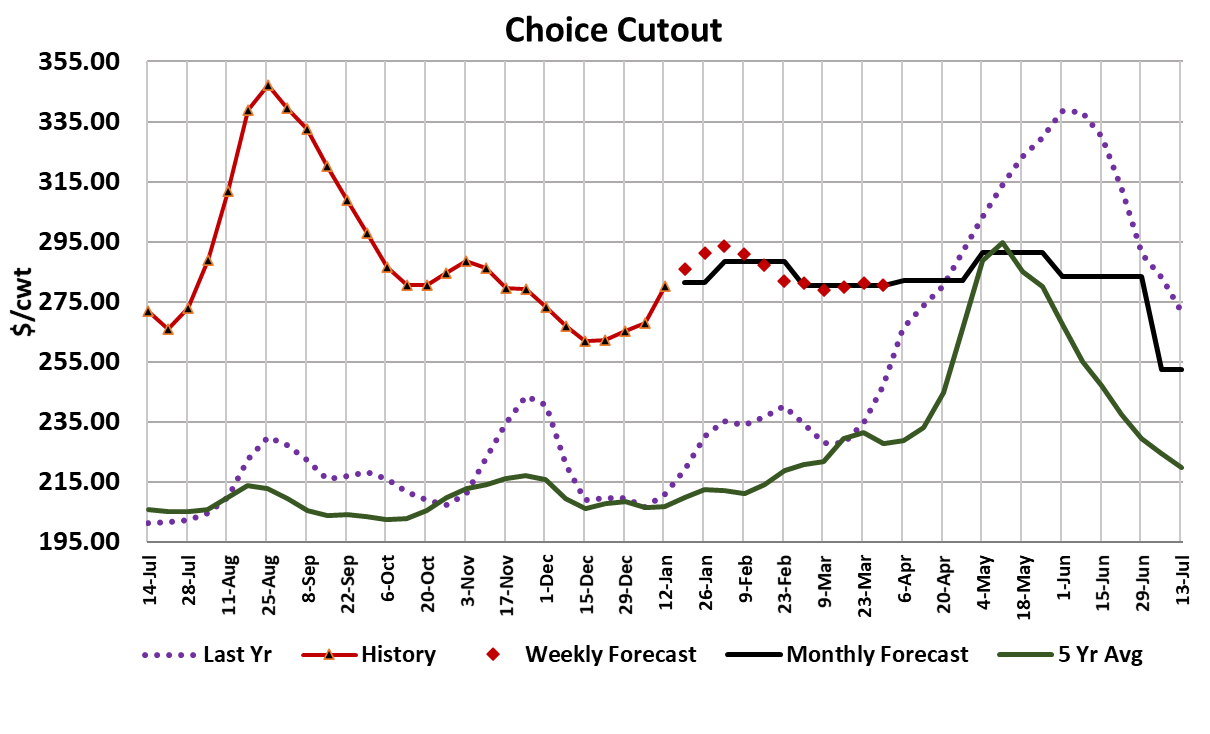

The cutouts roared higher, with the Choice gaining $12.24 on a

weekly average basis and the Select up $10.67. That provided a

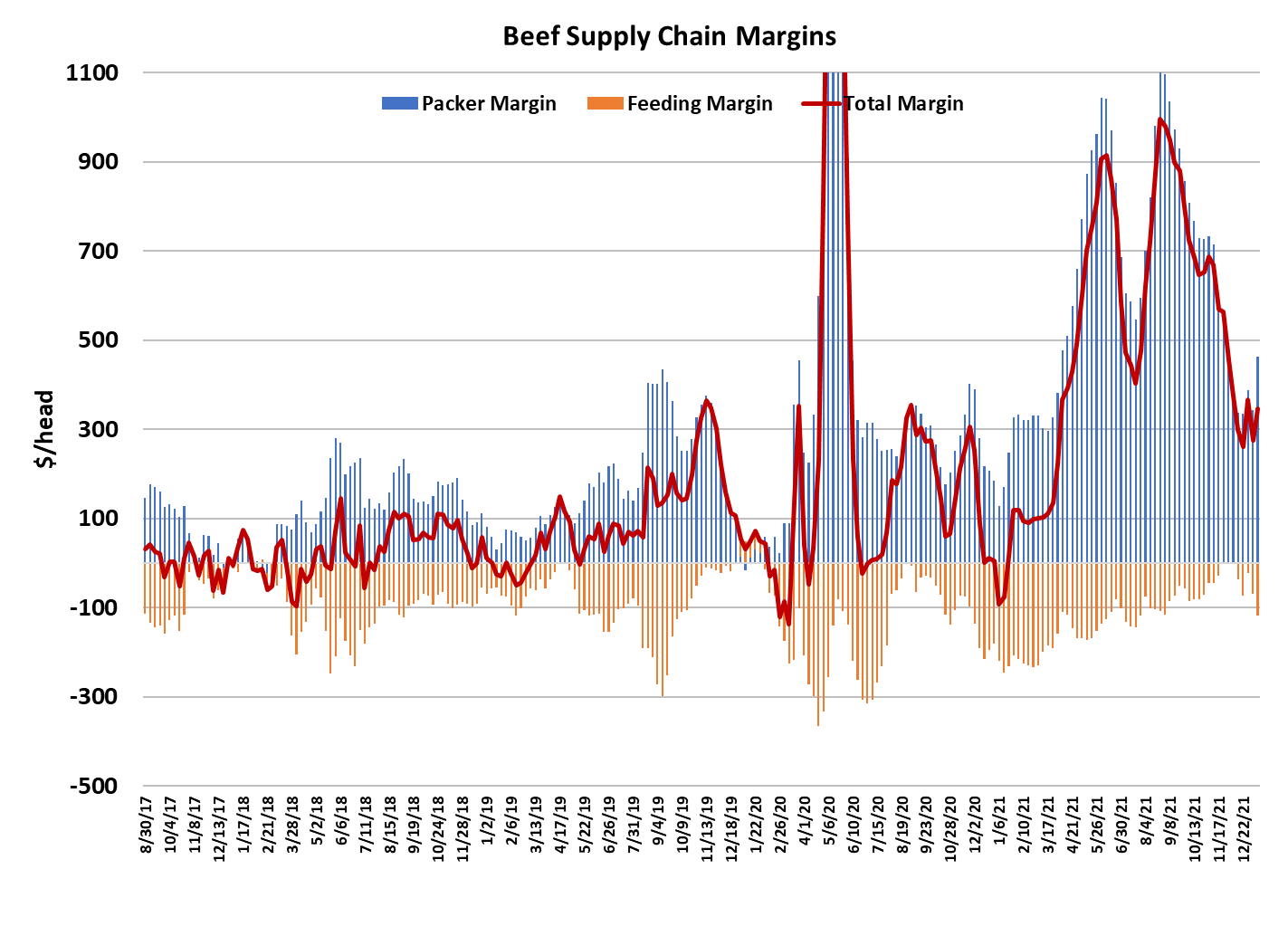

huge boost to packer margins, which averaged $473/head, up $130/

head this week alone. It seems like restricted throughput in the

packing segment is once again limiting feedyard’s leverage in the

cash cattle market. Packers didn’t buy a whole lot of cattle this week,

so perhaps they will need to be more aggressive next week and that

might allow for some increase in cash prices. However, the weather

in cattle feeding country remains relatively good for this time of year

and that means cattle performance has been above average. This

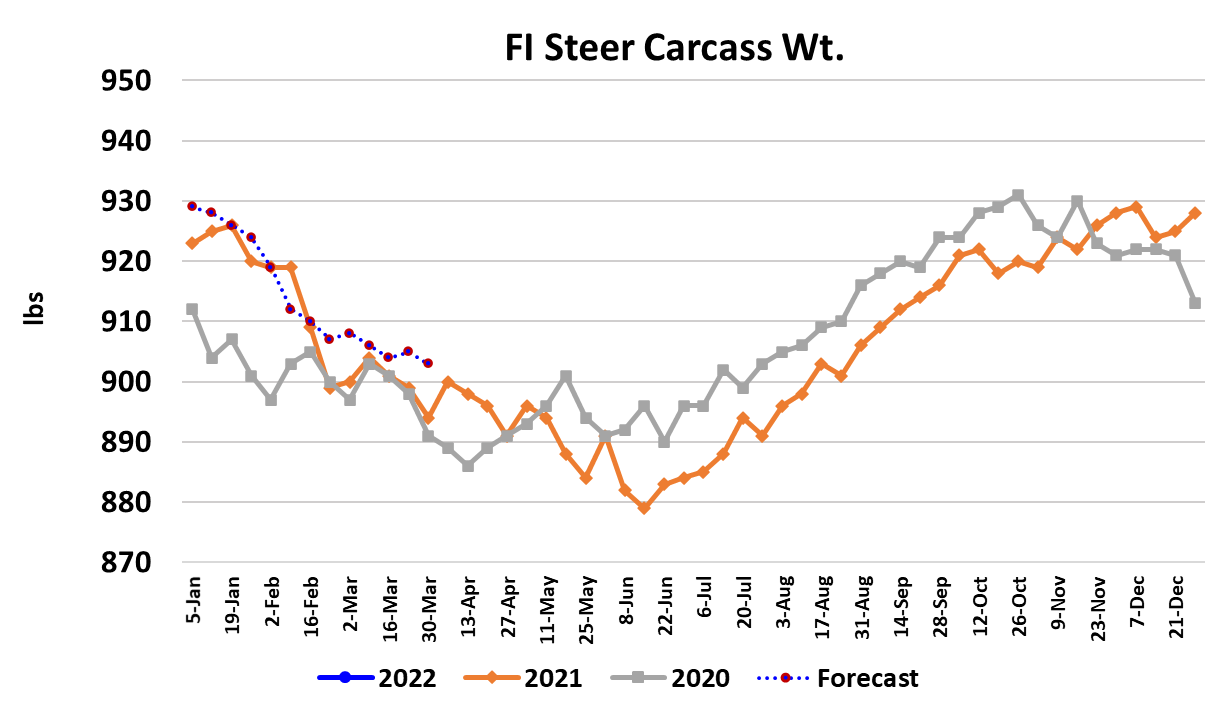

clearly is not a weather market year. Steer carcass weights were 3

pounds higher in this week’s FI data release, which was for the final

week of 2021.

The DTDS weights increased again as well. It is not the type of

supply environment that is conducive to higher cash cattle prices. Of

course, packers might be reluctant to push downward too hard on

cash cattle prices when their margins are heading back toward

$5-600/head, but if the cutouts should stall and turn lower then cattle

prices will be at risk. Right now it seems that beef prices are going to

keep going up forever, but once the COVID-related absenteeism dies

down in the packing sector, production should expand and that might

mean the end of the strong rally that we’ve seen here in early 2022.

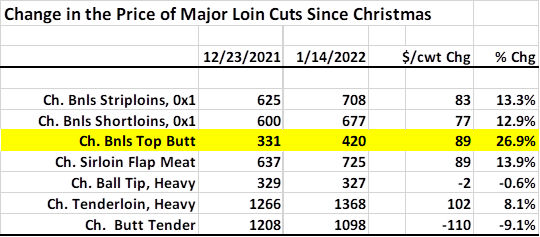

All of the primals except the brisket were supportive to the cutout this

week, but the loin primal was a strong driver. That is really unusual

since loin items typically don’t see strong demand at this time of year.

The table below indicates that the top butts have been on fire since

Christmas, with price levels up 27% over the three-week period.

Strips and shortloins have also posted gains, but the top butts really

stand out.

I have to believe that this is retail business, with grocers looking to

feature a lower-priced steak item in the Jan/Feb time frame. The

end meats have also posted strong gains, but that is pretty normal for

this time of year. Fat trimmings have jumped higher, quoted this

afternoon over $122 after finishing last Friday at $103. Labor issues

in the packing plants mean that they are doing less trimming and thus

fewer 50s are being produced. This comes right at the time of year

when retailers want to feature ground beef. So the rally in 50s might

still have a ways to go. I really think that the lion’s share of this

January rally in beef prices is coming from the supply side and not

demand growth. Of course, when supply is constrained

unexpectedly, it always generates a temporary demand surge from

buyers who get caught out of position. The combined margin made a

tick upward this week, but has not really shown a strong trend in the

last few weeks.

This week, packers only managed to slaughter 475,000 steers and

heifers, which was 9k below last week and a good 35k less that what

they were processing in early December. Interestingly, the cow

killers managed to kill 146,000 this week, up 10k from the week

before. Maybe they are having fewer COVID problems. I expect that

next week, absenteeism will decline a bit and packers will be able to

put together a little larger fed kill—maybe close to 490k. However,

February is right around the corner and kills normally dip in February

to better align production with the softest demand period of the year

from a seasonal perspective. I’ve been projecting February fed kills

around 475k, without any COVID considerations. There should be

enough capacity to kill more in February if demand warrants it. My

fundamental forecast has the Choice cutout peaking in the mid $290s

during the first week of February and then retreating as the COVID

surge fades.

I could see maybe a $2-3/cwt increase in cash cattle prices during

that time if packers are feeling generous, but I wouldn’t count on it.

Packer margins are likely to go to $600/head. Normally, packers see

their worst margins of the year in February, but it looks like this

February is going to be far better than December for packers.

International demand for US beef has been a little difficult to ascertain

due to spotty reporting over the holiday, but Q4 looks like it was pretty

strong for beef exports and I don’t see any reason why that wouldn’t

carry into 2022. However, beef imports have also been pretty strong

in the past couple of months, with a lot of product coming in from

Mexico. That is canceling part of the benefit of strong exports, but it

looks like for 2021 as a whole the US will export slightly more beef

than it imported. Next week, USDA will give us another COF survey

and I’m expecting it to show December placements up 2.8%, but I

don’t feel particularly confident in that number.

December placements are notoriously hard to project and many of

the indicators I look at for the forecast were pointing to smaller

placements that what I finally decided to go with, so I wouldn’t be

particularly surprised if placements come in a little below last year’s

level. The number of cattle on feed as of Jan 1 should be nearly

dead-even with last year. I calculate cattle feeding margins to be

about $115/head in the red right now—the result of paying nearly $160

for feeder cattle back in August and corn that has hovered around $6/

bushel. Break-evens on cattle leaving the yards today are around

$145/cwt, so there is little chance of cattle feeders turning a profit in

the near term. Next week, the focus will be on the daily kills for signs

that absenteeism is improving and packers are able to put more cattle

through the plants. Beef prices should continue to rise, but not as

fast as they did this week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}