Beef Wrap January 28

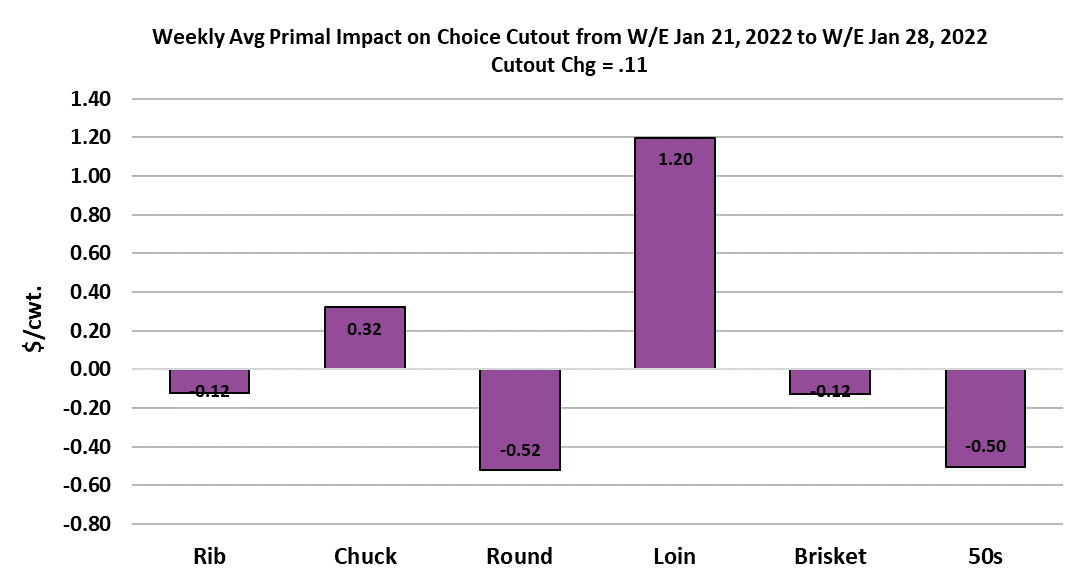

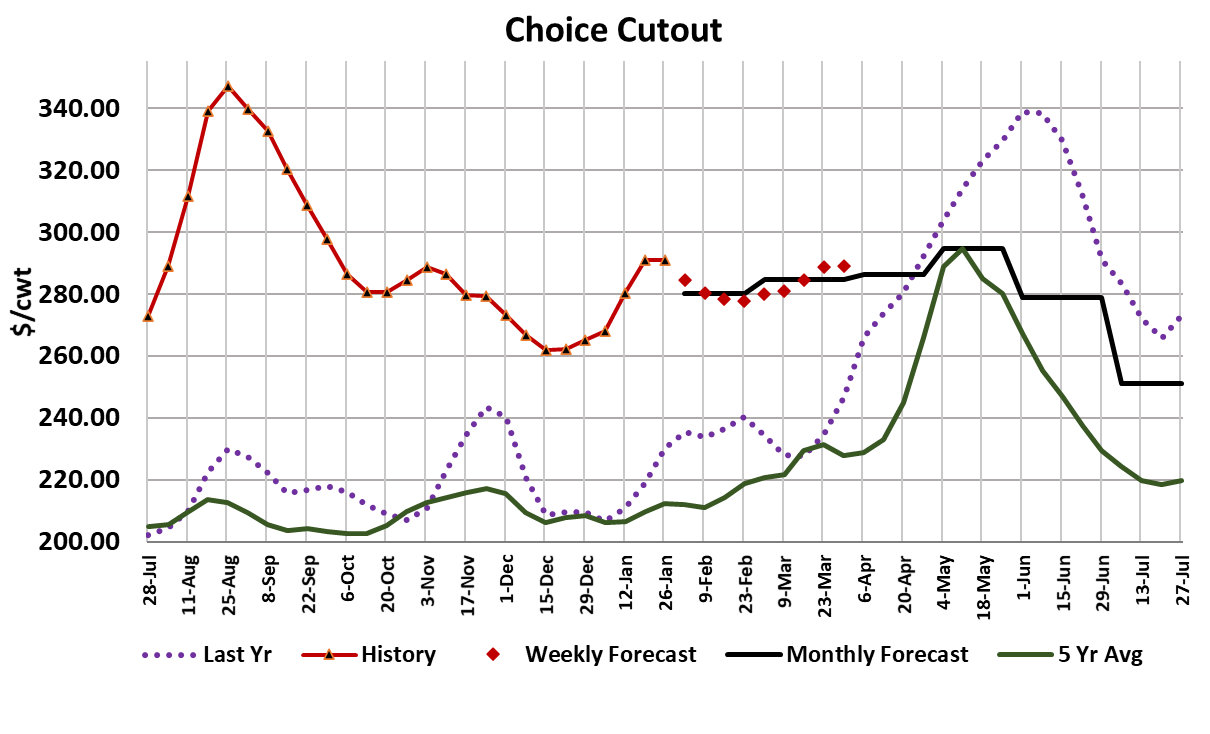

Cash cattle traded steady to slightly lower this week, averaging

$136.93, which was $0.57 below last week’s average. Packers

couldn’t get too excited about buying cattle because the cutouts were

on the defensive for most of the week. However, both cutouts posted

a rally on Friday that erased losses from earlier in the week. On a

weekly average basis, the Choice cutout gained $0.11 while the

Select was up $1.99. Cattle slaughter improved some this week, with

the fed kill coming in at 495k, up 7k from last week. There is a sense

that the COVID-related absenteeism problems are beginning to

abate. That should enable packers to begin working through the 60k

or so cattle that were backlogged in early January, if they want to.

Right now their margins are pretty good, registering $535/head, down

only $15 from last week.

Our flow model is calling for February fed kills to average around

485k, so they could easily add 15k each week and thus clear the

backlog by the end of the month. However, with beef prices already

really high and the cutouts looking somewhat tenuous, packers may

have some reservations about expanding the kill much beyond what

we saw this week. No need to force the cutout down any faster than

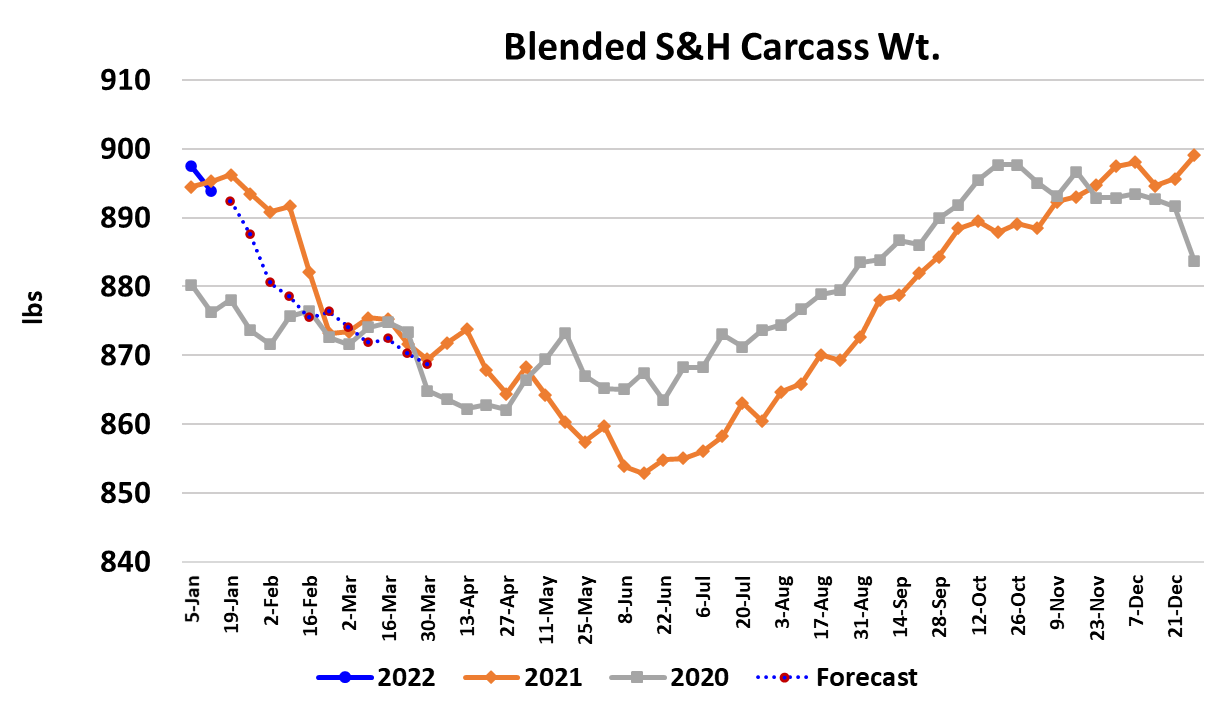

it might already be scheduled for. This week saw FI steer weights

drop six pounds, but heifer weights were unchanged. That took

blended carcass weights down three pounds, but they still are quite

heavy. The DTDS carcass weights are holding near +10, which is the

heaviest they have been in almost a year. That makes me think that

feedyards are not all that current. Packers are happy to pay steady

money for cattle as long as the cutouts are allowing for a fat profit

margin. Once the cutouts start to fall significantly then the risk to

cash cattle prices increases. This week, the loin cuts were the

biggest gainers in the cutout. My sense is that beef demand at retail

remains good because consumers are staying home a lot more than

they did back in December.

Consumers pulled harder than expected on beef out of the meat case

and that has left retailers with some gaps to fill. However, the worm

may be about to turn on the demand side and the combined margin

seems to be indicating that we are near a local top with respect to

demand. COVID cases are now trending lower and that should

accelerate in the next few weeks. I expect people to venture out of

their bunkers and they will be less concerned about stocking up on

beef at the grocery store and more concerned with enjoying social

activities once again. As a result, I’m forecasting the cutouts to work

lower in February. I have the Choice cutout bottoming in the

$275-280 are in early March and then I think we can expect spring

demand to start to lift the cutouts once again. Buyers should be

looking to fill middle meat needs during February as prices soften in

anticipation of price increases this spring.

End meats have a lot less upside potential in the spring, but also may

not come down much during February. Ground beef is likely to

remain a favorite that retailers can use to lure cash-strapped

consumers into the store during February. I’m expecting fed beef

production in Q1 to be down about 0.7% from last year, with the

recent COVID-related slaughter slowdowns factoring into that. Beef

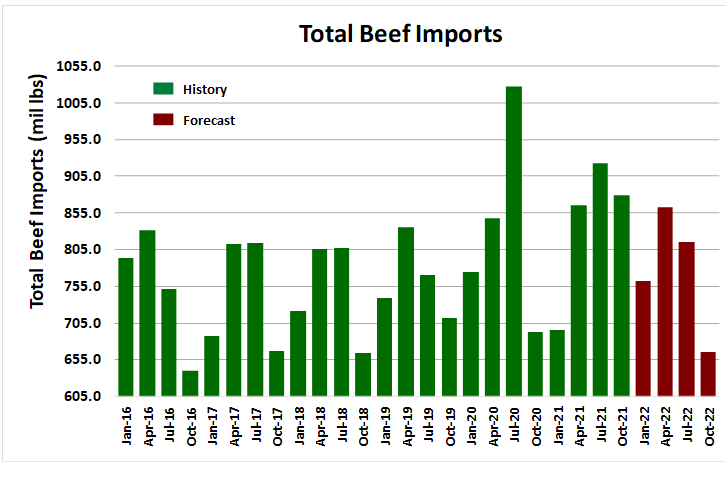

exports should remain relatively strong, down only 1.4% in Q1 from

last year’s strong number, but imports are projected to be 9.5%

above last year. That will put imports nearly equal to exports and

mitigate any price benefit the strong export market might have

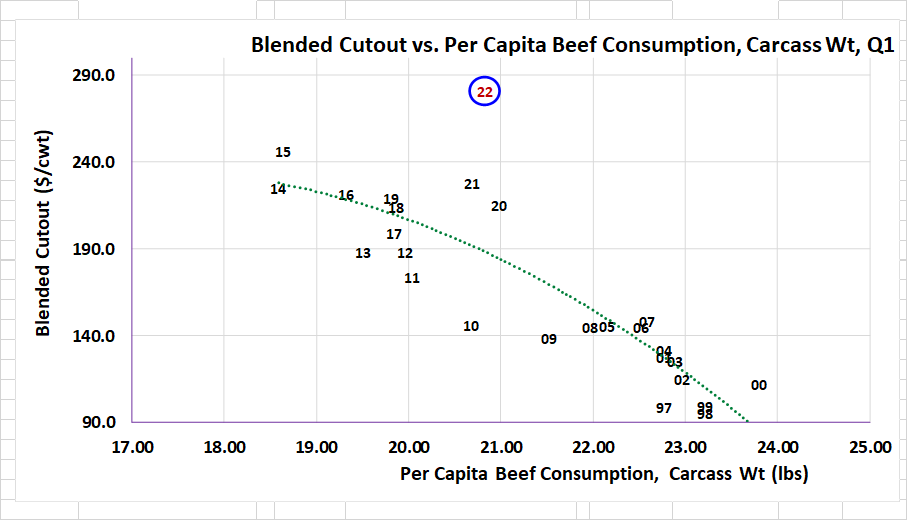

afforded. With strong imports, I’m looking for per capita beef

availability to be about 0.7% stronger than last year and last year the

Choice cutout averaged $229 in Q1.

Of course, last year at this time the demand train had not yet left the

station. This year in Q1 demand should be much stronger and thus

that leads me to a Q1 Choice cutout forecast of $282, even though

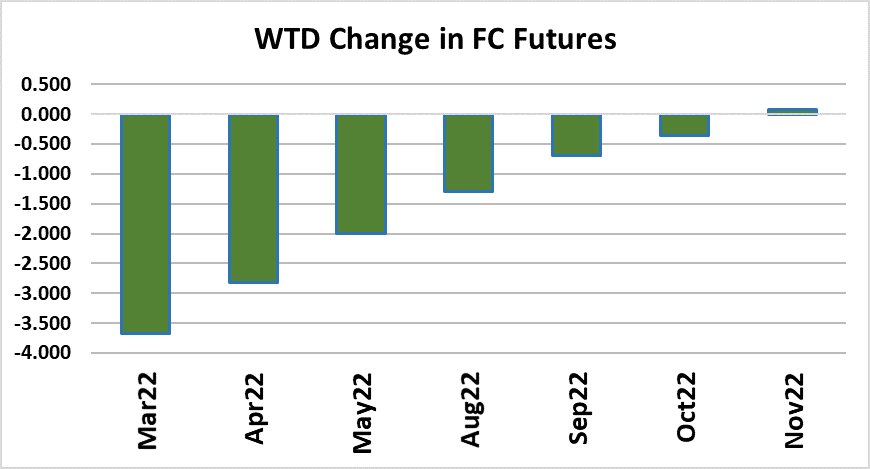

availability will be slightly larger. Last Friday’s COF report showed

December placements up 6.5%, which was well above the 2.5% that

analysts were projecting. As expected, the futures market sold off

hard on Monday and was helped along by a bloodbath in the equity

markets. Cattle futures are relatively sensitive to the state of the

economy and when the stock market takes a big dive it usually brings

out some cattle bears. For most of the week, the stock market was

gyrating up and down in big chunks and that led to some pretty strong

cattle moves in both directions. In the end, the futures found some

solid footing on Friday and all contracts finished the week higher than

the week before. The grain markets posted strong gains this week

and are back near the highs they hit last summer. Strength in the

grains normally supports the deferred cattle futures because traders

assume that eventually the high price of corn will get passed along

the supply chain in the form of higher cattle prices.

Next week, we will get the annual cattle inventory report which will

give us a snapshot of herd size and form the basis for most of the

2022 supply estimates. It is widely expected that inventory numbers

will be lower as we are still in the liquidation phase of the cattle cycle.

I don’t think the report will show any significant signs of heifer

retention, which normally signals that liquidation is coming to an end

and higher prices are on the horizon because producers will be

holding back females. I believe that is still at least a couple of years

into the future. Next week, watch the cutouts for further weakness,

which would indicate that retail demand is starting to cool after a

relatively strong January.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}