Beef Wrap February 11

The cash cattle trade averaged $140.52 this week, up about $0.60 from

last week’s average. Packers bought rather large numbers this week

and so may be able to pull back from the spot market a bit next week.

This week’s market had to be a disappointment for cattle feeders after

last week’s $3 increase, but there seems to be a strong feeling in the

producer community that cash prices will continue to trend higher. The

Apr futures are priced close to $6 over this week’s cash and that

provides an incentive for cattle feeders to delay marketings if they don’t

like the price that packers offer. The problem with that is that carcass

weights are already very heavy and any marketing delay is just going to

add more weight and increase the chance that cattle feeders will have

to conduct a fire sale at some point in the future.

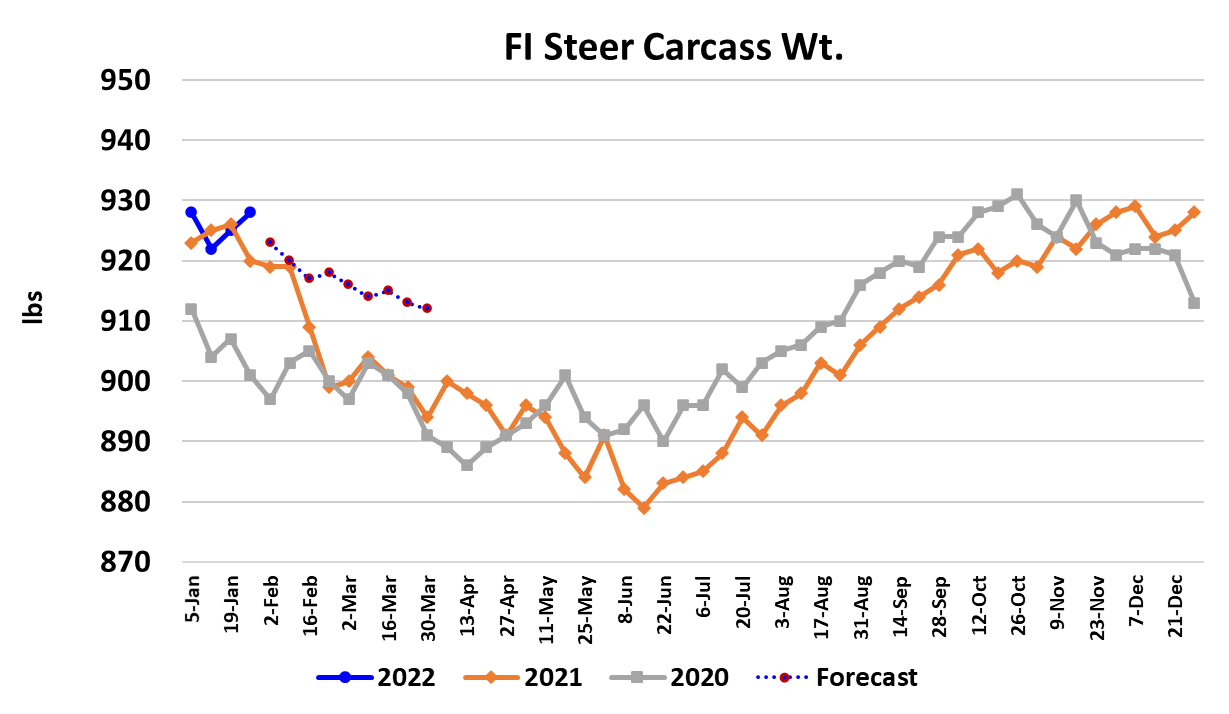

Steer weights should be trending lower seasonally at this time of year,

but instead, they jumped 3 pounds higher in this week’s data. That

pushed this week’s DTDS weights up to +20, which is a serious red flag

for feedyard currentness. The weather across cattle feeding country

was relatively mild this week and that will help the cattle to put back on

any weight that they might have lost in the previous week’s cold blast.

Some snow is forecast in the Plains late next week, but it doesn’t look

like it will be a major weather event. This week’s fed slaughter came in

at 507k, which was almost 20k more than the week before. That will

help to clear some of the cattle that were backlogged during the omicron

wave, but it will also produce a lot of beef that needs to be moved next

week. Cow and bull slaughter was 152k this week, which was over

10% stronger than last year. 90s prices are very strong and rising and

that is putting upward pressure on cull cow prices which, in turn,

encourages producers to send more marginal cows to slaughter. That

high cow slaughter rate is partly responsible for why futures traders are

so bullish on the deferred contracts. Breeding herd liquidation seems

to be moving along at a high rate and that causes traders to believe that

cattle and beef supplies are going to get very tight.

They are right about that, but I think that they are off on their timing. It

should take at least another year, and probably 2 years, before the herd

gets so small that it causes a supply crunch and sharply higher prices.

However, as long as lean beef prices hold at very high levels, it will

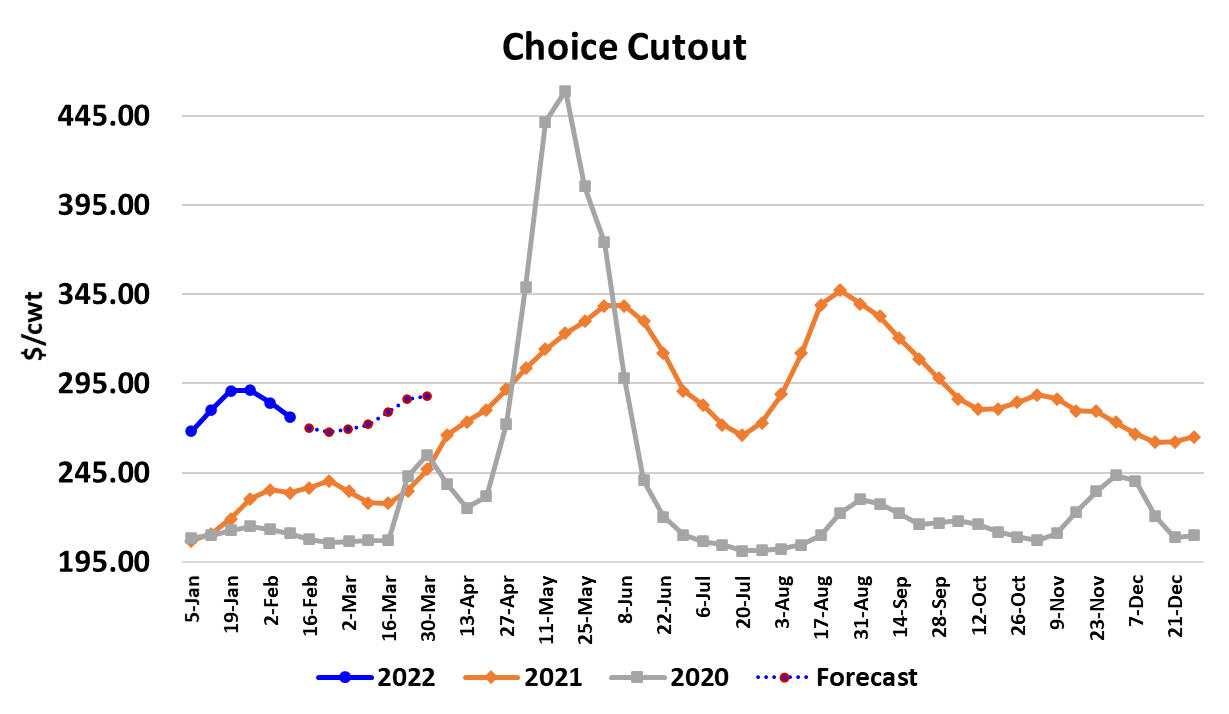

continue to encourage herd liquidation. This week the Choice cutout

fell $7.72 and the Select was down $7.57 on a weekly average basis.

All of the primals were lower, but the loin was definitely the weakest link.

Buyers backed away from top butts this week, with prices for the Choice

product down 8.6% Friday-to-Friday. Those top butts had been bid up

to very high levels in early January and they are now coming back down

quickly. End meat prices also moved lower, which is a little unusual for

this time of year. USDA released its retail beef prices for January this

week and those were down a little less than 1% from the prior month.

Retail prices are now slowly retreating, but still very high in a historical

context.

As consumers struggle with high gas prices and significant price

inflation in the other things that they buy, there will be less room in the

budget to pay up for beef. My sense is that consumers are now

“climbing back down” the protein ladder as stimulus windfalls are

depleted and inflation erodes any benefit they might have received from

higher wages. When the great demand bubble of 2021 started, you will

recall that pork demand started moving strongly higher in February of

2021, but beef demand didn’t really show any significant gain until

about 6-8 weeks later. Back then, consumers were climbing up the

protein ladder, first demanding more pork and then eventually

displaying increased demand for beef. Now they are going in the other

direction and it is manifesting as weaker beef demand first while pork

demand is improving. Eventually pork demand will ease too as more

consumers trade down to lower priced chicken. The combined margin

chart is clearly signaling a demand downcycle and the only real

question is how long it will last.

Fortunately for beef producers, spring is just around the corner and

when the calendar turns to March we should see some of the normal

grilling demand come back into the complex. However, I wouldn’t look

for this year’s spring demand to be as strong as it was last spring.

COVID infections are falling rapidly and there is a general sense in the

population that the pandemic is nearing an end. That means

consumers will be spending time this spring and summer catching up

on all of the travel and other things they couldn’t do during the

pandemic. As a result, they will probably spend less time hanging out

around their grill in the back yard. I see the cutouts working lower

through February and then turning higher in March as demand

improves. Right now, the forecast has the Choice cutout getting down

to about $265 before it makes the turn higher, but it could easily slide

below that level. International demand for US beef seems to be ok, but

not really growing like it was in the second half of 2022.

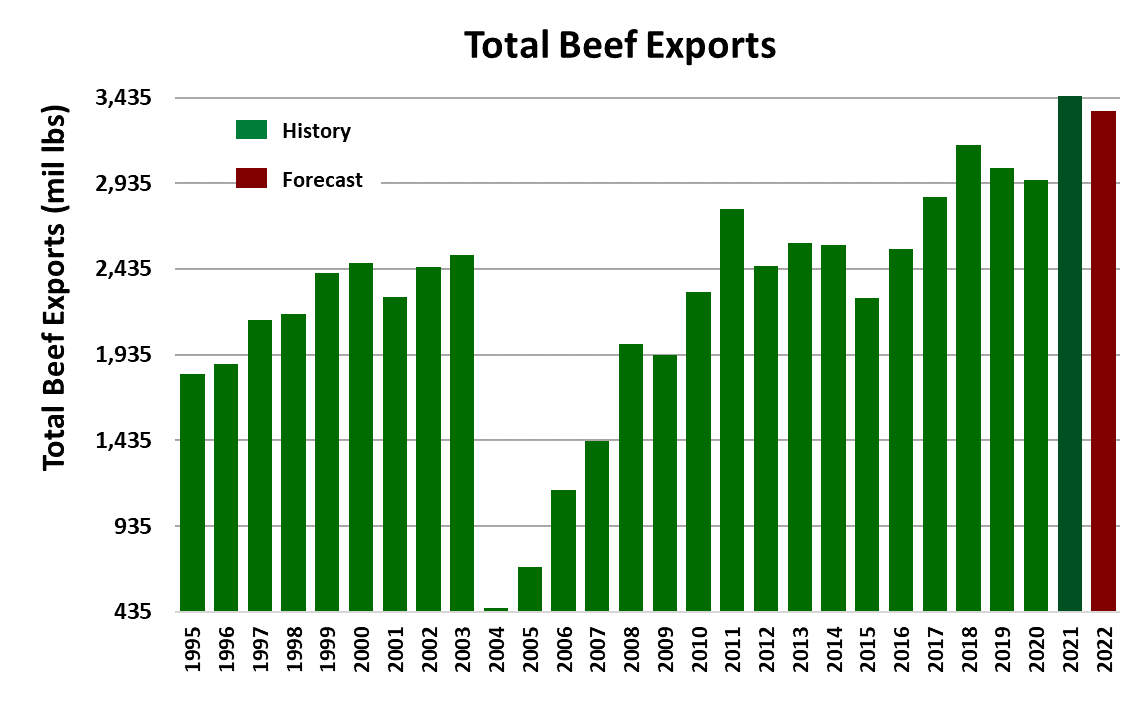

According to USDA, beef exports in December were up about 1% from

the previous year and for 2021 as a whole, beef exports posted an

impressive 16.6% gain. The last time annual exports grew by a greater

percentage was in 2011. The forecast has 2022 exports down 2.6%

from 2021, but that still be very strong export year from a historical

perspective. After big gains in the prior week, the futures market was

much more subdued this week, perhaps due to the near-flat cash trade.

There seems to be a lot of speculative money flowing into the long side

of cattle futures under the idea that price inflation will take cattle and

beef prices substantially higher this year. I think that is a mistake and

they are late coming to the party. The price inflation has already

happened and now beef prices and soon cattle prices, will be on the

defensive. Next week, watch carcass weights. They should come

down at least a couple of pounds, but if they don’t that will strengthen

the case that feedyards are still behind on their marketings.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}