Beef Wrap January 21

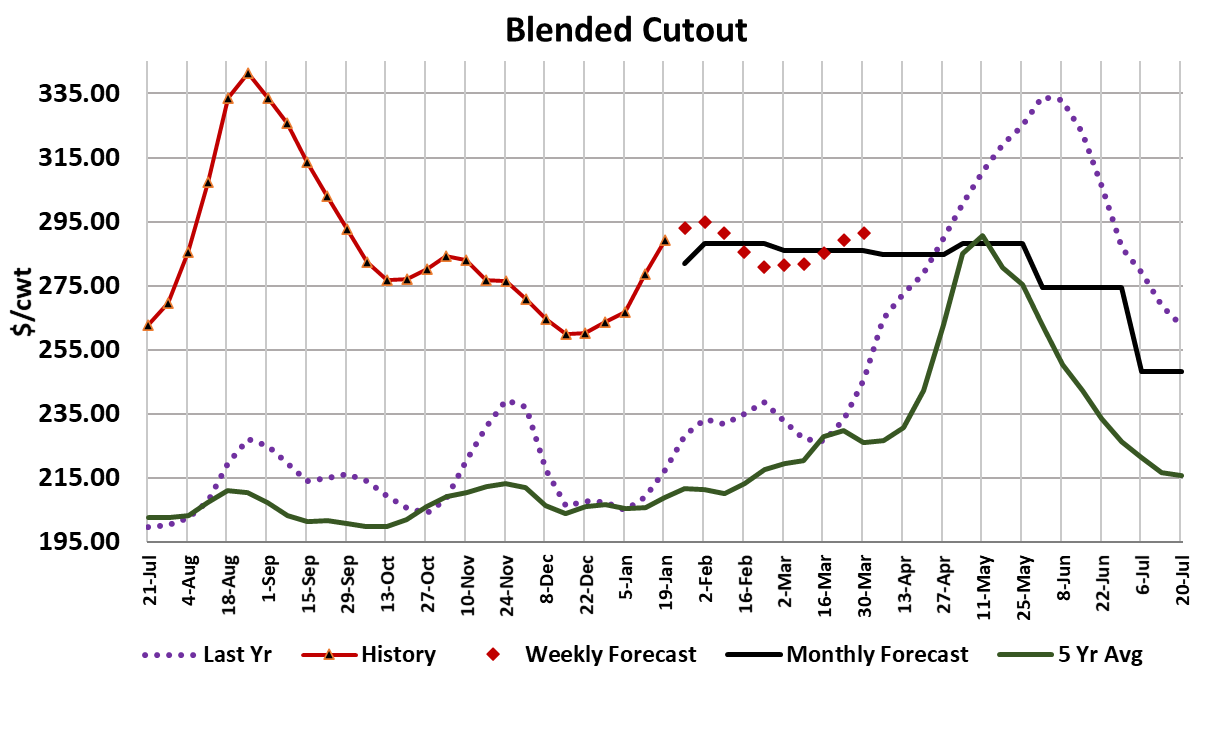

The cash cattle market averaged $137.39 this week, up about $0.78

from last week’s average. Packers bought more this week than

they did last week, so perhaps that signals growing confidence that

they will have enough labor to move kills higher next week. Both

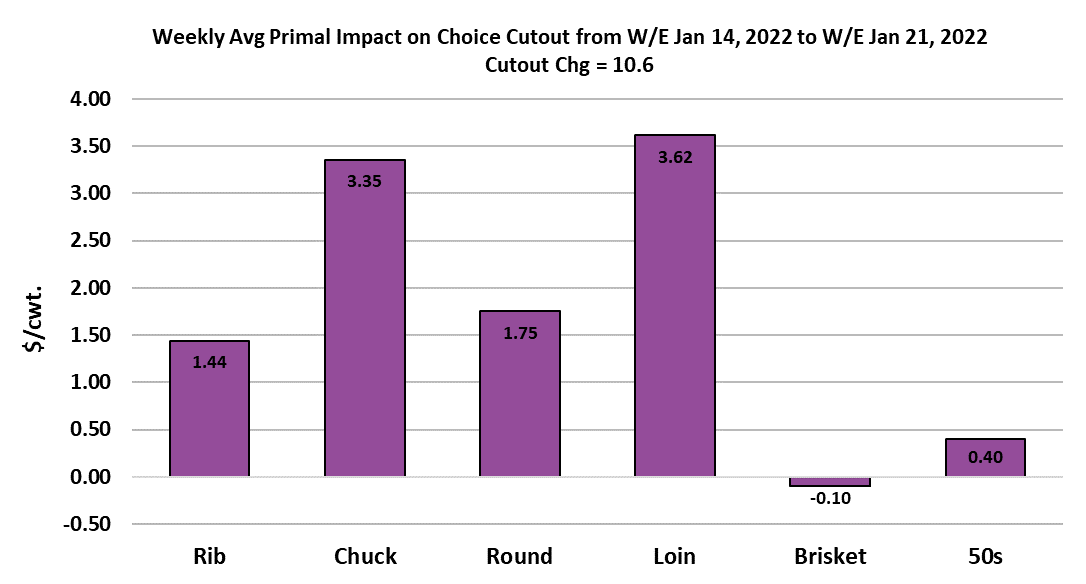

cutouts gained about $10/cwt this week, but by Friday they were

showing signs of topping. We are now beyond the peak in omicron

infections here in the US and next week will likely see pretty sharp

declines in the infection count. That should take some of the

pressure off of the supply chain and also reduce any stockpiling by

consumers. It is likely that retailers stockpiled also as omicron was

rising, so they may have less need to be in the spot market next

week and that would provide some room for the cutouts to retrace a

bit. Beef supplies should be bigger also, as this week’s fed kill

came in at 491k, up 20k from the week before.

Some cattle likely got backed up over the last few weeks and

packers may step up next week’s kill a little to help clear that

backlog. Of course, cattle feeders aren’t likely to have much

leverage as long as a cattle backlog exists. Packers will probably

pay steady money since their margins are so strong right now, but if

they really wanted to, I’d bet they could push cash lower. Today’s

bearish COF report will probably generate some red ink in the

futures early next week and that will just give more ammo to

packers in the cash market negotiations. Carcass weights held firm

at a high level this week and we saw the DTDS weights shoot

higher, now at +10 lbs. That also reduces cattle feeders’ leverage.

So there are a lot of factors right now that are aligning against cattle

producers.

As expected, this omicron wave brought with it some improved beef

demand as consumers hunkered down once again. However, now

that the wave has crested, people will soon feel more comfortable

doing things outside of the home and that generally leads to softer

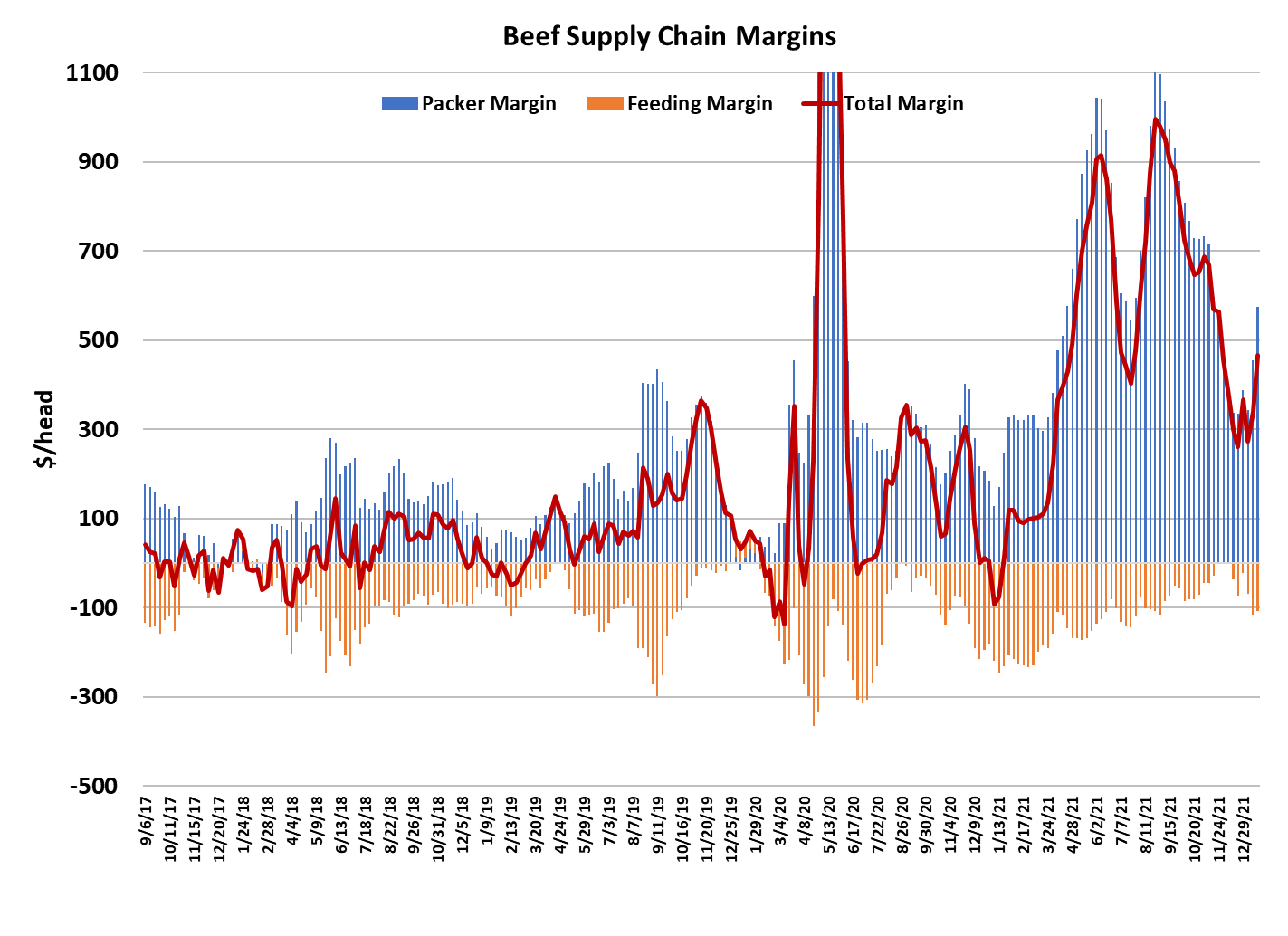

demand. The combined margin made a nice move higher this

week, but I really don’t think it is going to peak over $900/head the

way it did in the last two supercycles. In fact, we could see it turn

lower again next week if the cutouts struggle. Corn futures were

higher all five days this week and thus grain is very pricey at the

moment. That will put more hurt onto cattle feeding margins if it

persists. I estimate that cattle feeders were about $100/head in the

red this week and it would take cash cattle at $145 for them to

breakeven.

That’s unlikely to happen anytime soon. Export business has been

a little slow to restart following the holidays, but I think it will pick up

in the next few weeks. China still has a very strong appetite for US

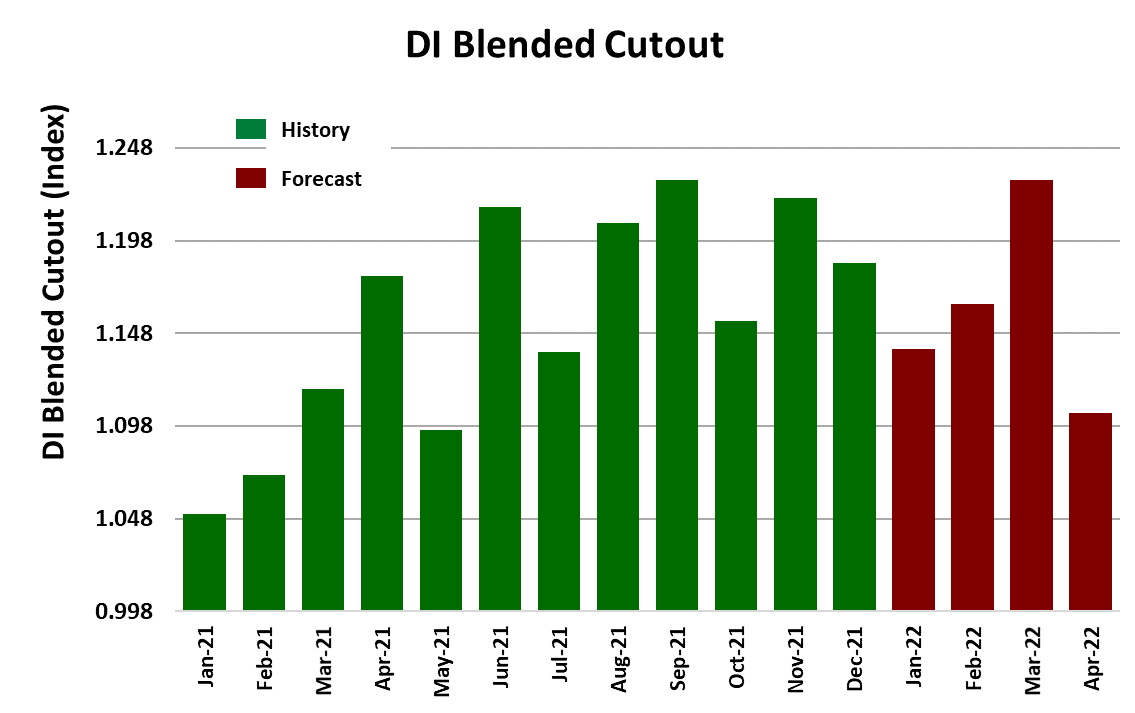

beef. The chart below plots the demand index for the blended

cutout and it’s clear that beef demand has been softening since its

peak in November. Outside of the strong index I’m showing for

March (which may be too optimistic), I think the longer-term trend in

domestic demand is lower. Cattle and beef prices are somewhat

sensitive to movements in the equity markets and this week has

been a bloodbath for stocks.

The deferred futures have been very over-priced relative to my

fundamental forecast and that is probably because I see demand

fading back to more normal levels as the year progresses, but

futures traders seem to want to project the current demand strength

right through the balance of the year. They may also be expecting

cattle supplies to tighten up more than I’m forecasting, but there is a

good chance that today’s COF report, which showed December

placements up 6.5% YOY, will temper that thinking somewhat.

Packer margins increased $120/head this week to $574. Next week

could easily bring $600/head margins. I don’t see them getting

much larger than that, but rather slowly shrinking throughout

February, which is typically a poor demand month. At the end of

January, we will get USDA’s annual cattle inventory report

I think it will show the cow herd down about 500k from last year and

the total inventory about 1.1 million below last year. It doesn’t

appear that producers are holding back heifers in order to rebuild

numbers yet—that is something that likely won’t occur until 2024 or

later. So there is a very good chance that cattle and beef supplies

will be down this year, but that doesn’t mean prices will be higher,

because the demand structure is expected to soften. Next week,

watch for some fireworks when the futures open on Monday

morning and keep an eye on the cutouts for signs that the top is in.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}