Beef Wrap January 26

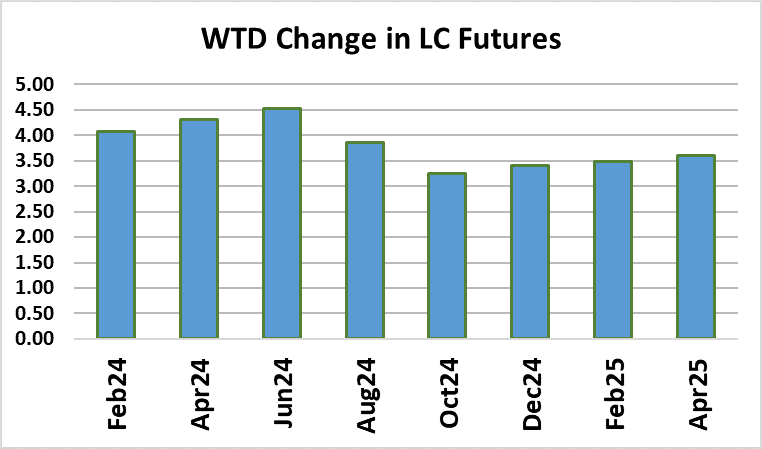

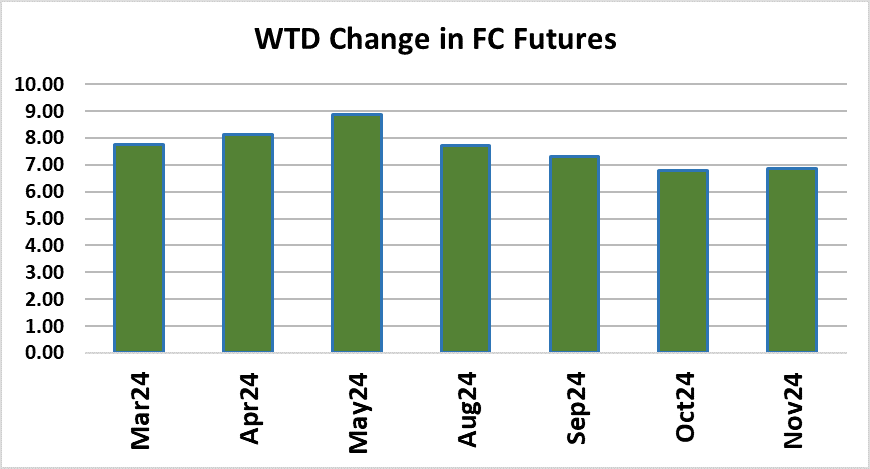

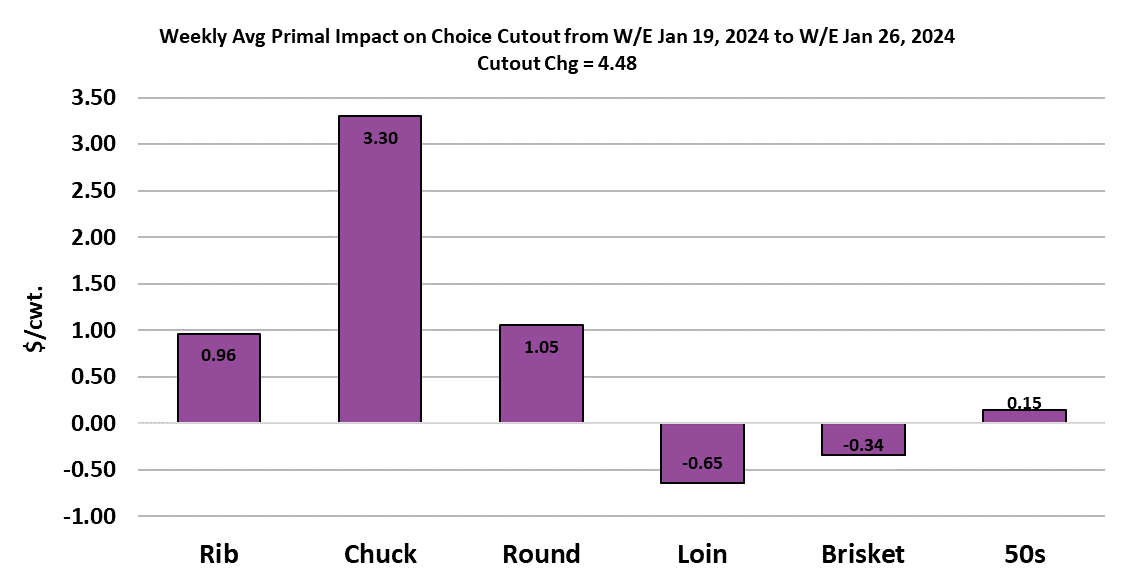

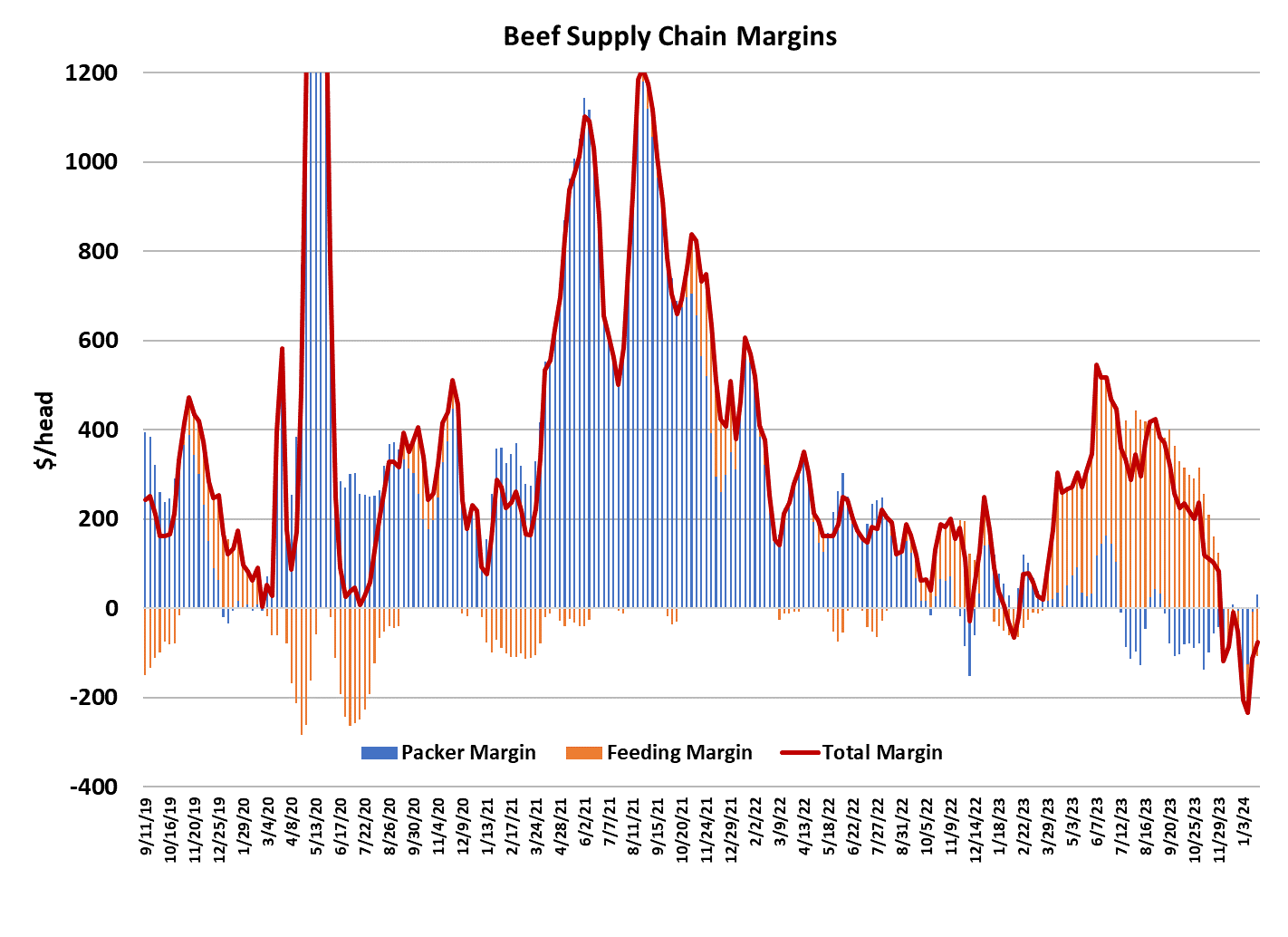

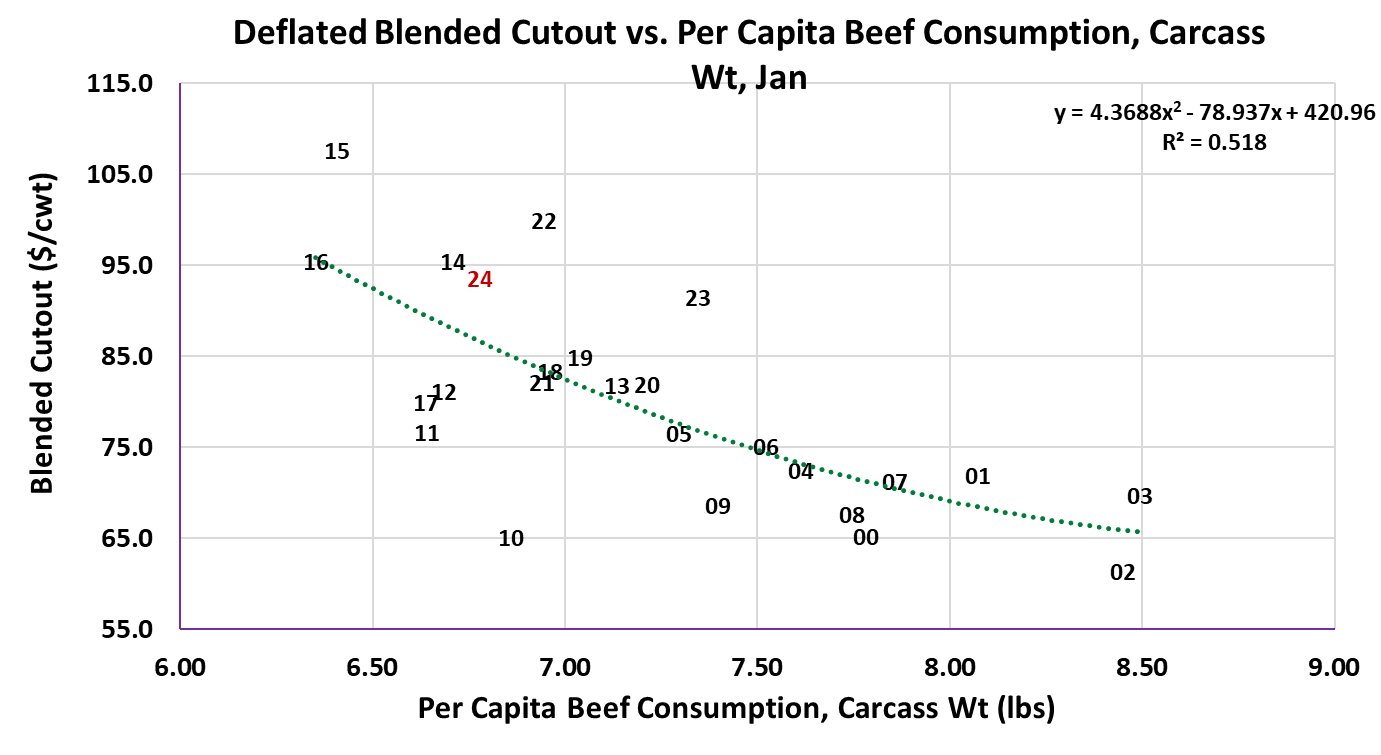

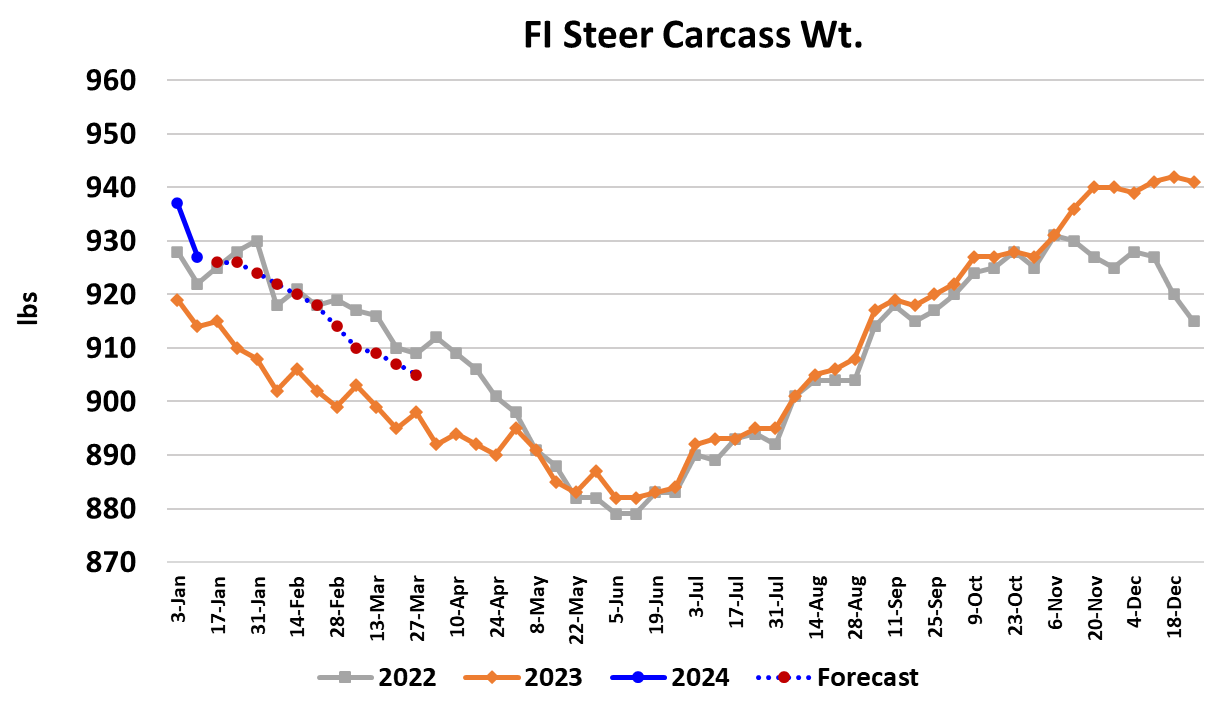

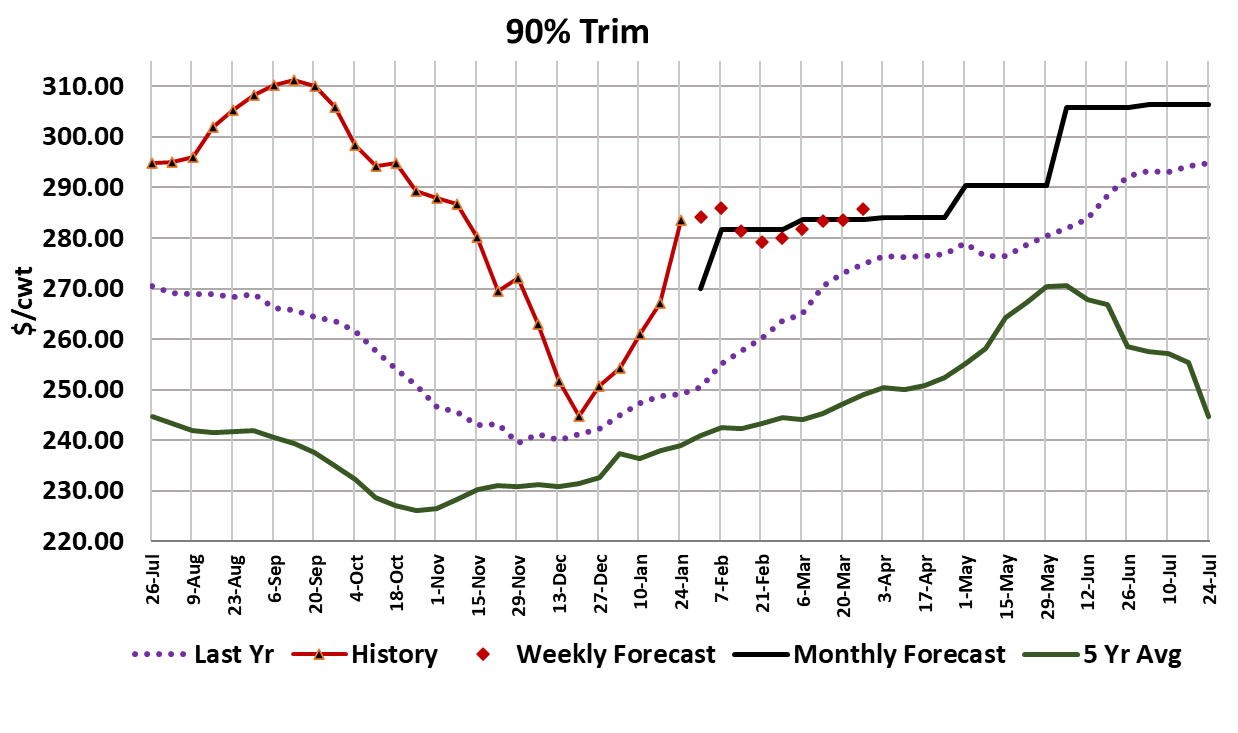

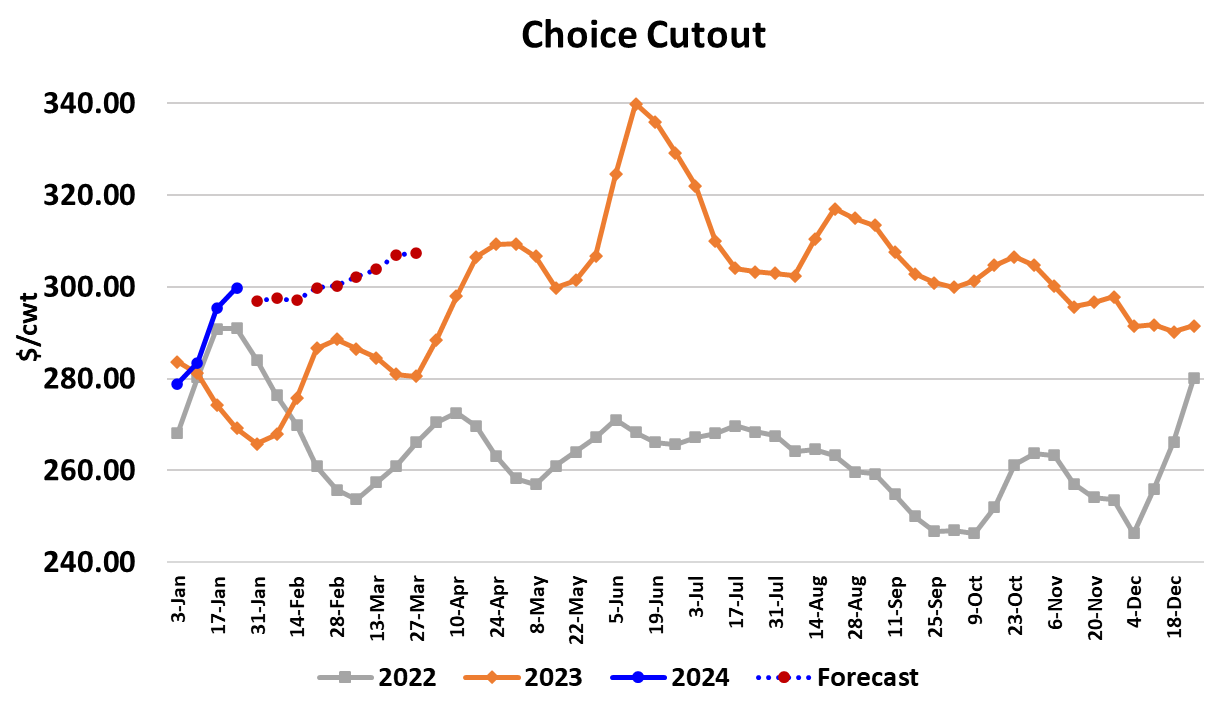

Small purchases in the cash cattle market over the past few weeks finally caught up with packers and they found themselves having to pay up in order to secure enough live inventory to operate next week. It looks like the average live price will be close to $175.40, which would be up about $1.75/cwt. from last week’s average. The futures market jumped for joy at this news as it became clear that cattle feeders had won price battle—at least temporarily. Feb LC futures added a little over $4 on the week to finish close to $178.50. Clearly, traders took this week’s action as a sign that cash is going to continue to climb over the near term. Feb will enter its delivery period in about a week and last year it was very common to see cash cattle prices advance once the delivery period started. The exception to that came in Q4 when the market was generally trending lower. However, the way traders acted this week it seems as though they believe the bull market is back on in a big way and that will likely begin to attract managed money back into long positions. They would be wise to park those long positions in the deferred contracts because the near-term fundamentals are not particularly bullish. Another thing that helped goose the market this week was the FI carcass weight data which showed a 10 pound drop in steer weights. Never mind that heifer weights were only down 2 pounds. This data was for the week when the coldest part of the polar vortex hit the Midwest and so it shouldn’t have been a surprise that weights were going to be down. Daily liveweights have been indicating this for some time, but to see it in the official FI data sealed the deal for any potential bulls that were still sitting on the fence. Cattle feeders always expect cash prices to advance in the wake of serious winter weather and this week proved them right. However, the weather forecast across cattle country looks very mild for at least the next two weeks, so that could give cattle performance a chance to rebound. It is also important to keep in mind that carcass weights were at all-time record highs before the weather event so the damage to currentness is probably not as bad as it seems. Packers have already begun to fight back by keeping this week’s fed kill down to 485k. They know that next week they will get access to their February formula cattle and this week’s purchase volume was the largest since the third week of September. So they probably won’t need to be very aggressive in the cash market next week. Further, there is still the issue of cattle backing up due to very light slaughter levels over the past few months. The weather may taken that concern away for a week or two, but unless we see more nasty weather the cattle will catch up quickly and cattle feeders could begin to feel a sense of urgency to get cattle marketed. One weather event, even a severe one, doesn’t usually make for a weather market. That usually only happens when several storms hit back to back. The cutouts continued higher this week with the Choice adding $4.48/cwt. on a weekly average basis and the Select gaining $7.36. The chuck primal was the biggest contributor to this week’s gain, but there was also some modest improvement in rib prices as foodservice and retail gear up for Valentine’s Day. The small kill could keep product relatively tight next week and thus we might not see much retrenchment in cutout values. The 50s market traded in the mid $90s this week, probably as a result of cattle losing finish during the weather event and thus production of 50s has declined. The 90s market is also on fire, with domestic product averaging $283.50/cwt. this week, up $16 from last week’s average. The lean trim appears to be seeing very much improved demand all of a sudden and that fits with the idea that post-holiday demand favors the end cuts and grinds. The combined margin continued to move upward this week, but it is still not back to the zero line and the upward momentum slowed. It is possible that this recent boost in demand was, to some degree, driven by buyers coming into 2024 rather short-bought because they expected production to be large and then they got surprised by the weather, forcing them to scramble to cover needs. If that is the case, then that activity should have largely run its course by now and buying interest in the beef market could die back down next week. With the Choice cutout now back challenging the $300 level, there is some risk that retailers will put the brakes on lowering retail prices and that could cause a problem with movement down the road. There could be some organic demand improvement coming from consumers however, as recent data paints a picture of a very strong US economy. GDP was reported up 3.3% YOY in Q4 and personal spending during December was up 0.7%. The stock market has been making all-time highs recently. When asked, many consumers say they the economy is in bad shape, but the data says otherwise and interestingly, these consumers continue to spend like crazy so there is a disconnect between what they say about the economy and how they are behaving. On Wednesday, USDA will release the results of its annual cattle inventory survey. I expect it to show the total US cattle herd as of Jan 1 down 2.2% and the number of beef cows down 2.6% YOY. The 2023 calf crop is forecast to be down 1.9%. If traders are already inclined to think the bull market is back on, then this data will likely play right into that narrative. However, there still is no evidence that producers are holding back heifers in order to expand their herds. When that happens, we can expect much stronger price gains. January FC futures had a strong expiration this week as cattle that couldn’t make it to the auction during the weather event showed up for sale this week while the futures board was bright green. If traders truly believe that the bull market is back on, then we should see feeder prices gain on fat prices, much like they did in the first half of 2023. Next week, watch the cutouts to see if packers have any luck extracting higher prices from beef buyers—that would be an indication of some organic demand improvement. It is also reasonable to expect another small kill as packers try contain cattle prices and thus preserve their margin.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}