Beef Wrap February 2

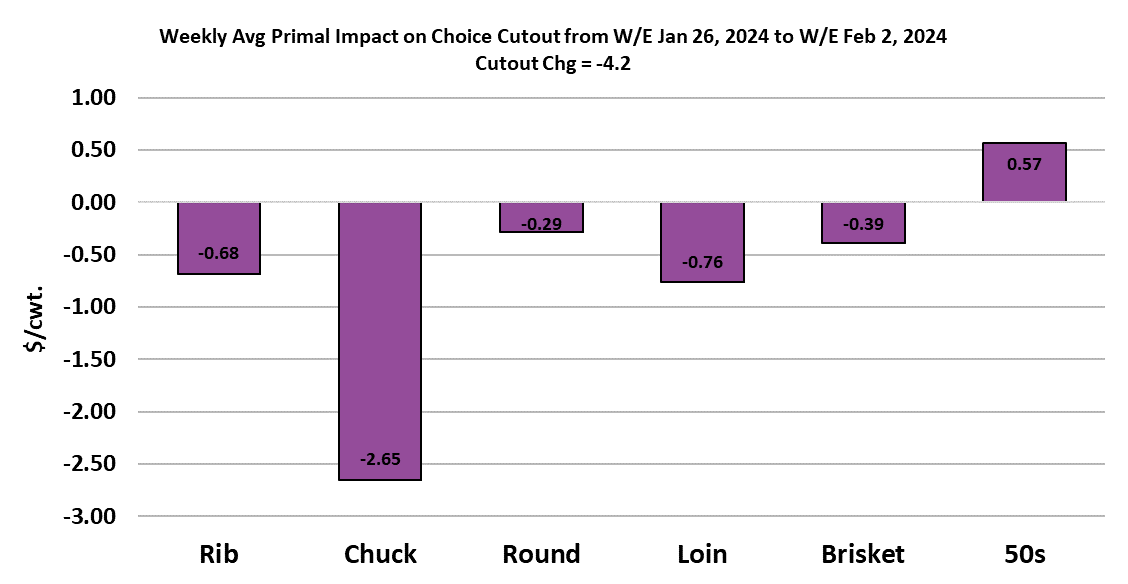

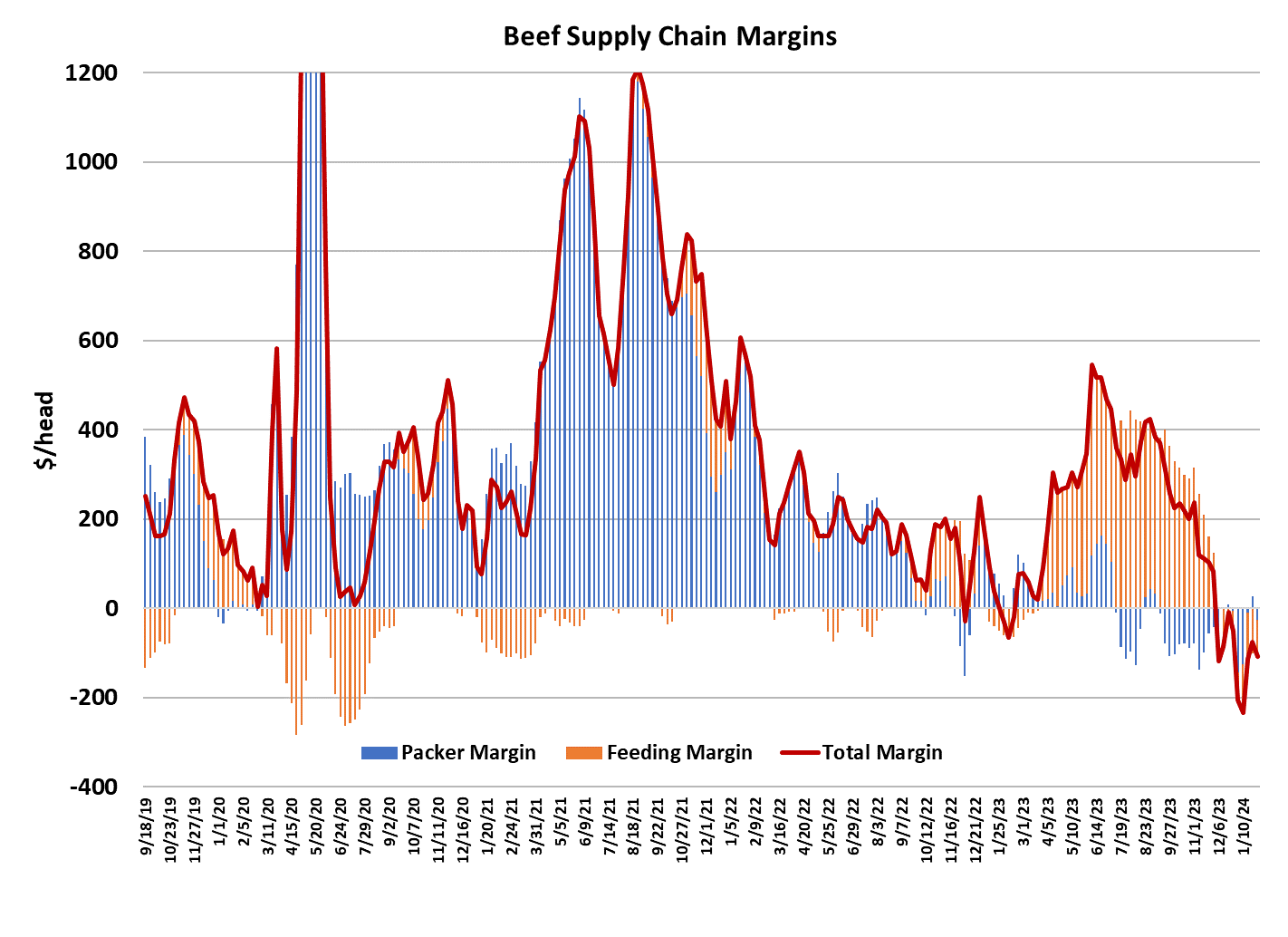

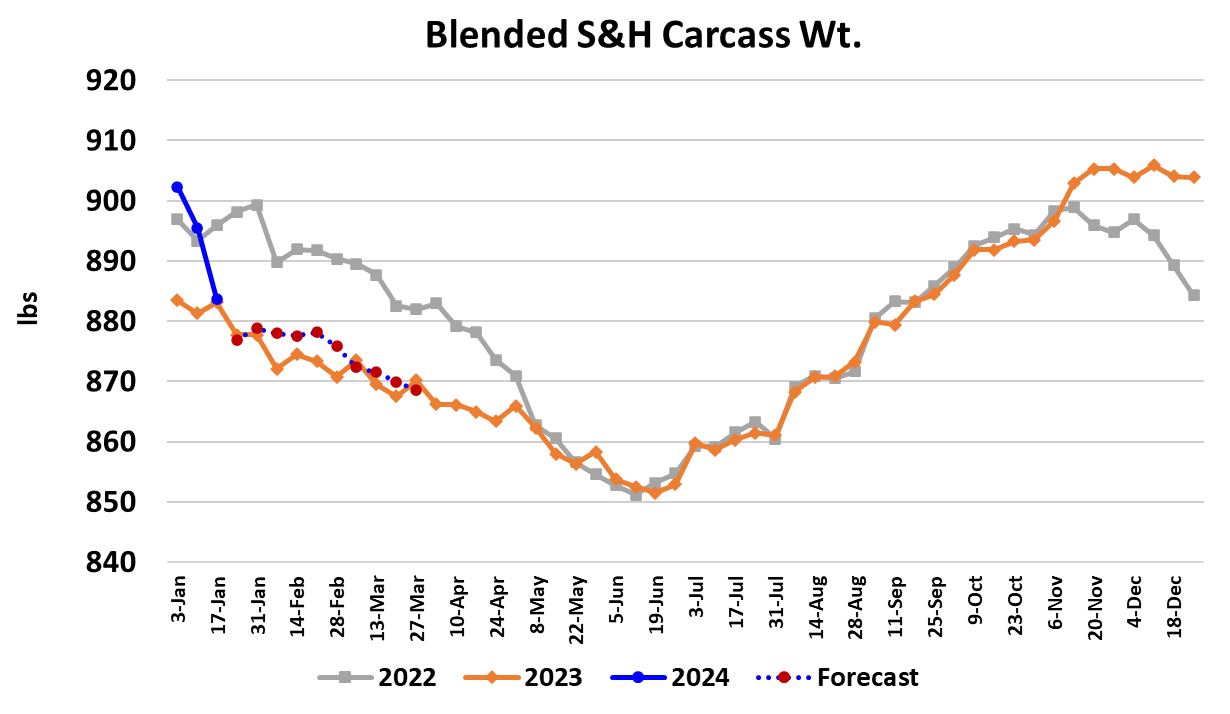

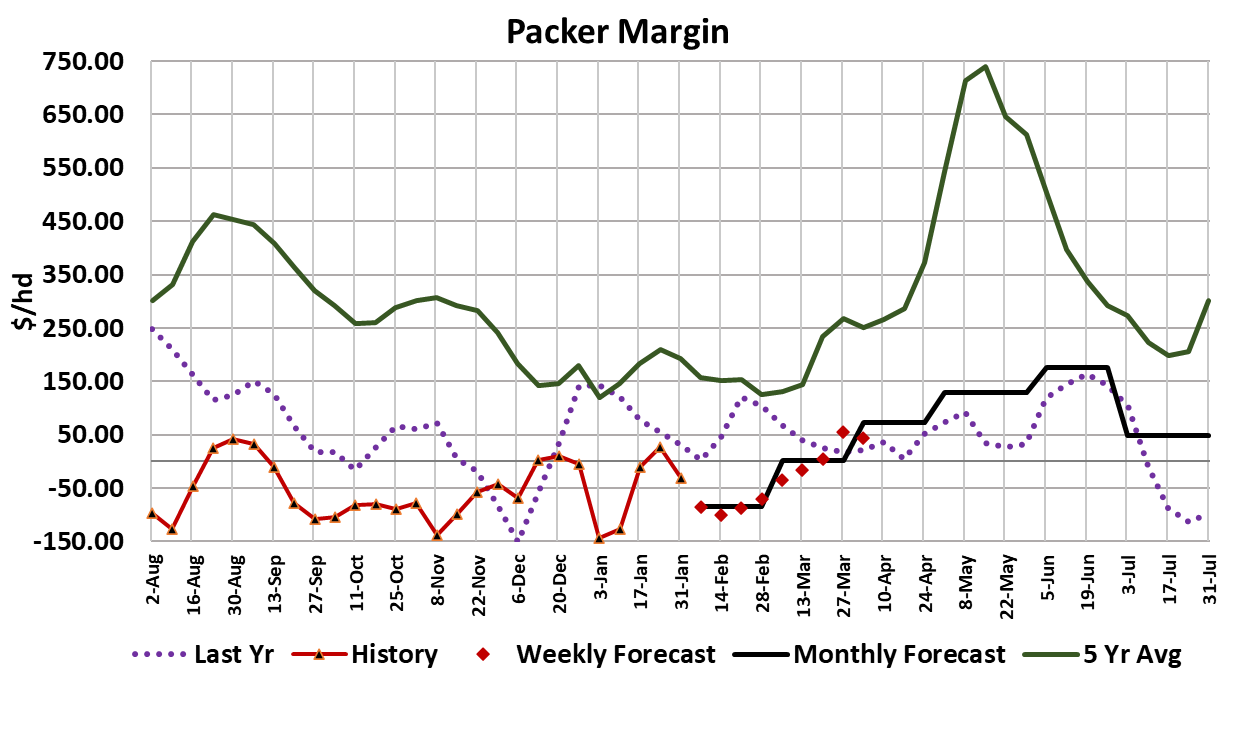

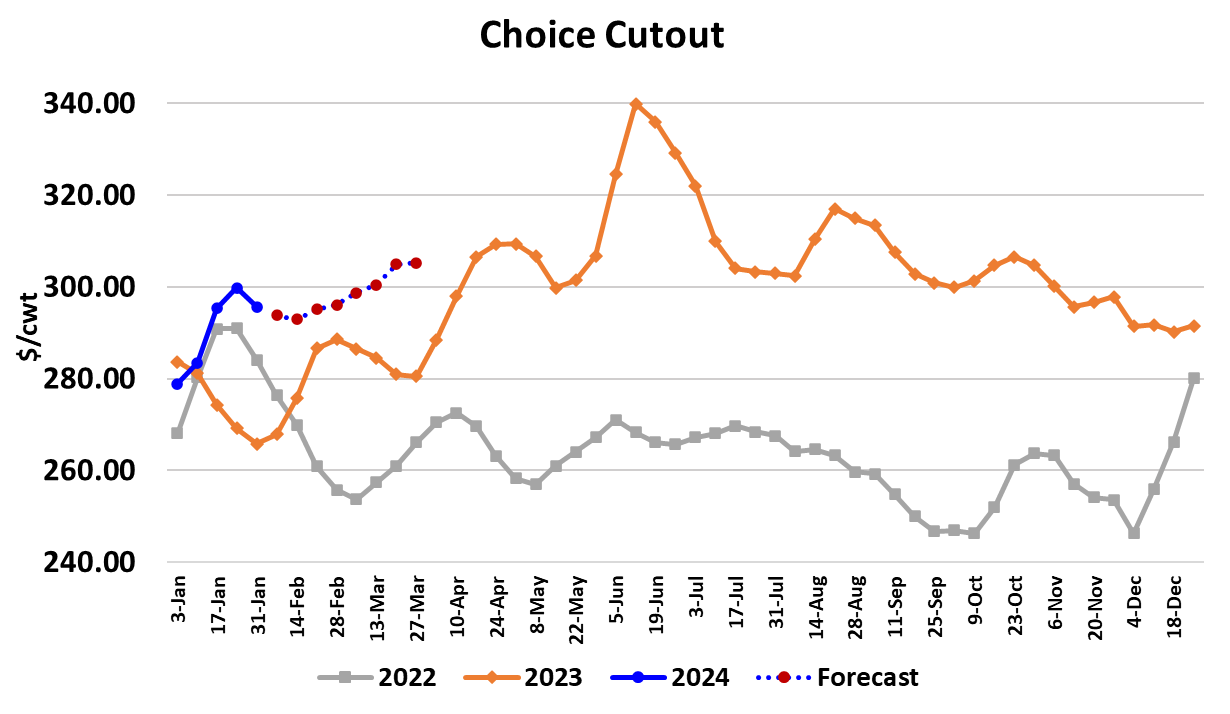

Two things became more apparent this week: the weather event in early January set cattle back more than previously thought and packers still remain short on inventory to fuel kills in early February. The confluence of those things helped to boost the cash cattle market $2-4 over last week’s prices. Trade in the Southern Plains started on Thursday at mostly $178-179 and in the North, trade was in the $177-178 range with dressed trade in the $279-280 area. My best guess would put the weekly average 5-area price at about $178.05, which is up about $2.60 from last week’s average. The fact that packers were short-bought was hinted at early in the week as bids rose over the previous week’s price by Wednesday, which almost never happens unless packers sense that they are going to have to compete vigorously in order to secure the cattle they need. Then the bomb was dropped on Thursday as USDA reported FI steer carcass weights down another 9 pounds following the 10 pound drop that was reported the week before. Steer weights were at an all-time high of 941 pounds in the last week of 2023 and it looks like they could be at 909 pounds when the data is released for the final week of January. That would be a 32-pound drop over the span of just four weeks. Clearly, the weather had a much bigger impact than initially thought. Cattle feeders are in the best position to see how cattle performance has been impacted by weather and they haven’t been very eager to sell cattle lately unless it is at higher prices. They probably feel like the cattle need some extra time to gain back the weight that was lost in January. Packers, on the other hand, have plants to run and they need an adequate supply of cattle to do that. Hence, it took nearly $4 higher in some instances this week to pry cattle away from cattle feeders. Packer margins were already tenuous before this week’s trade and those higher cash cattle prices will very likely push packer margins solidly into the red next week. That is, unless they can get the cutout moving higher again. However, it is February and beef demand at the consumer level should be trending softer, reducing the need for beef buyers to chase product in the near term. Packer reps will be working the phones early next week informing buyers of their new, higher pricing on almost all cuts and they will likely get some increases early in the week. Whether or not that can be sustained beyond about Wednesday is questionable. This week the cutouts moved lower for the first time in five weeks. The Choice cutout lost $3.57/cwt to average $296.24 and the Select cutout was down $2.01 to average $285.82. Ribs were the biggest drag on the cutout but the end meats moved lower also. Buyers finally got a chance to purchase beef lower this week, so it is unclear as to whether or not they will be willing to turn right around next week and pay up again. Packer margins for this week are estimated at -$26/head and next week, I have that dropping to -$85/head. That will be a signal to packers that it is time to slam brakes on kills again. This week’s fed slaughter came in at 500k, up 12k from the week before and the strongest fed kill since the second week of December. Cutting the kill would be the right thing to do because it would allow cattle more time to put weight back on and a decline in beef availability might help packers to move the cutouts up several dollars. It remains to be seen if packers have the discipline to slash the fed kill next week. If they don’t they will almost certainly have to pay up for cattle again. Fortunately, the weather forecast for the Plains States looks very mild for the next couple of weeks, so that should help cattle to get back on track. Weights will still be moving seasonally lower, but likely at a much slower pace than what we’ve seen in the past couple of weeks. February traditionally is a soft demand month, but the macroeconomic picture still looks very strong and consumers are continuing to spend, so perhaps beef demand this February won’t be as soft as in some years past. The stock market continues to press higher, boosting retirement accounts and making the owners of those accounts feel wealthier. That is usually quite friendly to beef demand. Export volumes in the weekly FAS data continue to run below last year by about 15-20% and that isn’t likely to change anytime soon. China has significant issues with its economy and that has caused a drop in exports to that important destination. My sense is that it would take significantly lower beef prices to spur stronger export volumes. USDA released the results of its annual cattle inventory survey and it showed the total number of cattle in the US down 2.2% YOY and then number of beef cows down 2.6% YOY. That is solid confirmation that the US herd remains in liquidation mode. The 2023 calf crop was pegged down 1.9%, which means that both cattle and beef availability in 2024 will be tighter than in 2023. Importantly, USDA found 1.4% fewer heifers retained as herd replacements and that suggests that little or no heifer retention is currently occurring. Taken together, these data points paint a picture of a shrinking cattle and beef supply that might not start to grow again until 2026 or beyond. Next week, watch the daily kills for signs that packers are throttling back and pay attention to the carcass weight data released on Thursday because another big decline might send both the cash and futures higher.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}