Beef Wrap January 19

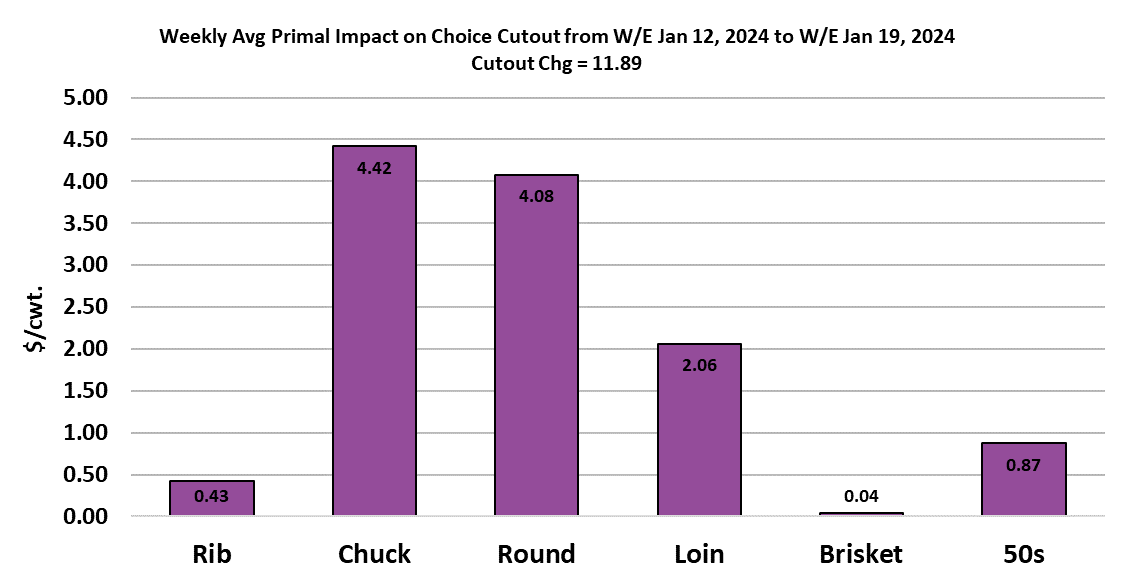

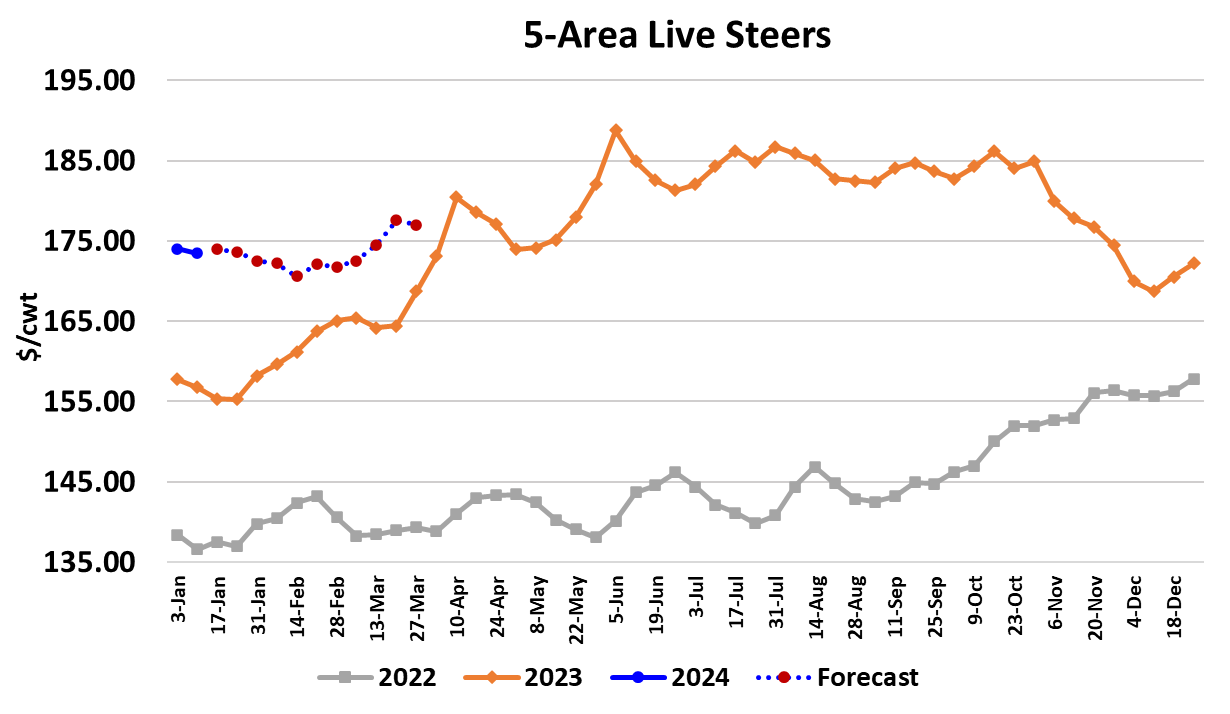

Following the previous week’s weather events, things slowly returned to normal in the cattle and beef complex this week. The cutouts continued higher as buyers chased product in an environment of tighter availability brought on by the previous week’s small kill. On a weekly average basis, the Choice cutout gained $11.89 while the Select cutout added $14.29. Most of the big gains were seen early in the week and by Thursday and Friday some weakness was beginning to materialize in certain primals. Still, the huge gains in beef prices helped packers nearly eliminate their margin stress with margins going from about -$125/head in the previous week to -8/head this week. Of course, cattle feeders saw the cutouts surging higher and fully expected to get more for cattle this week, but packers resisted. The standoff continued until late on Friday, but there were signs that the market mostly likely would trade mostly steady around $173 or perhaps a little higher. Packers can likely sense that the cutout is going to come down next week as full production resumes and they don’t want to get behind the eight ball again by paying too much for cattle. Of course, cattle feeders feel like the weather took a lot of weight off of cattle and if packers won’t raise prices, then they will hold the cattle back a week and try to put some weight back on. This week’s fed kill logged in at 490k, which is about 10-15k below what the flow model suggests that they should be killing in order to keep feedyards current. On one hand, we have the potential to backlog additional cattle by keeping the kill down and on the other hand there is potential for significantly slowed weight gains due to the weather. At this point, it is hard to tell which effect will dominate, but clearly packers are trying to skew the game in their favor by keeping the kill constrained. Steer weights declined four pounds in the data released this week that was for the week including New Year’s Day. Next week’s weight data will give us better visibility into the weight losses that occurred during the weather event. For the first three weeks of 2024, steer and heifer beef production is down about 3.2% from the same period last year and that comes at a time when we have 2% more cattle on feed than last year. The weather forecast for the next couple of weeks looks fairly favorable for the Plains States and that could help cattle performance rebound rather quickly. This afternoon’s Cattle on Feed survey reported December feedyard placements down 4.5% YOY and that was nearly dead-on with pre-report estimates so it isn’t likely to generate a big market reaction. Marketings during December were down 0.9%, also fairly close to the trade guess. That marks the second month in a row where USDA has reported YOY placement declines, so that should help traders get over the longer-run supply fears that were generated by YOY placement gains in September and October. The market reset lower in Q4, but now appears poised for a re-emergence of the cyclical supply bulls who will likely want to focus their buying efforts on the deferred live and feeder cattle contracts. Of course, there is a potential near-term bearish supply picture building and, absent any further weather events, that is likely to weigh on the front end of the futures curve at least through February. The demand side of the market is holding together a bit better than expected here in January, although it is difficult to separate out how much of the demand strength is due to buyers caught out of position when the weather hit from organic demand strength emanating from consumers. That should become clearer in the next couple of weeks. This week, the gains in the cutout were led by the end meats, but all primals posted some price increases. 50s prices reached $90/cwt. this week, likely driven by small production. There isn’t much that will substitute for beef 50s in the short run, so demand tends to be rather inelastic and that makes movement in the 50s price a decent proxy for the underlying fundamental picture. Look for 50s to ease back down now that production is normalizing. The combined margin shot higher this week on the surge in cutout values, but it is possible that some retracement will occur in the next couple of weeks. Still, we are overdue for the demand cycle to turn higher, so I wouldn’t be surprised if it eventually gets into an uptrend. Next week, it will be all eyes on the battle between packers and feeders, as feeders will insist their cattle are worth a lot more because performance has suffered and packers registering their disagreement by keeping the kill light.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}