Beef Wrap February 9

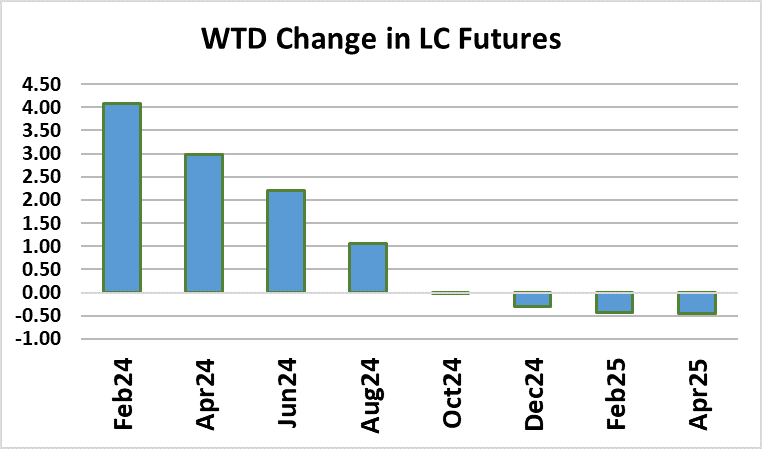

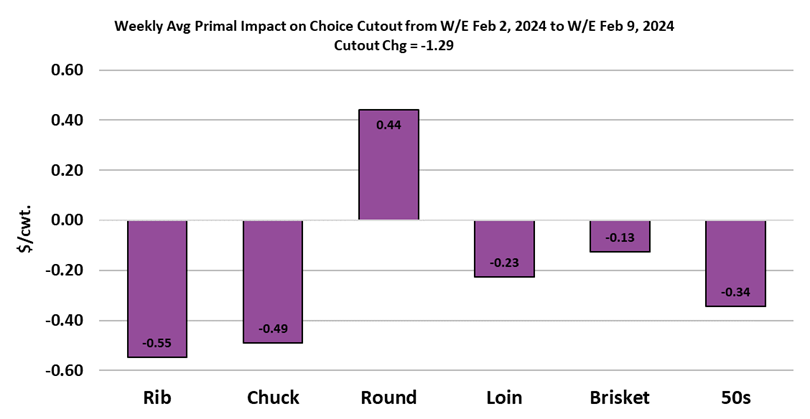

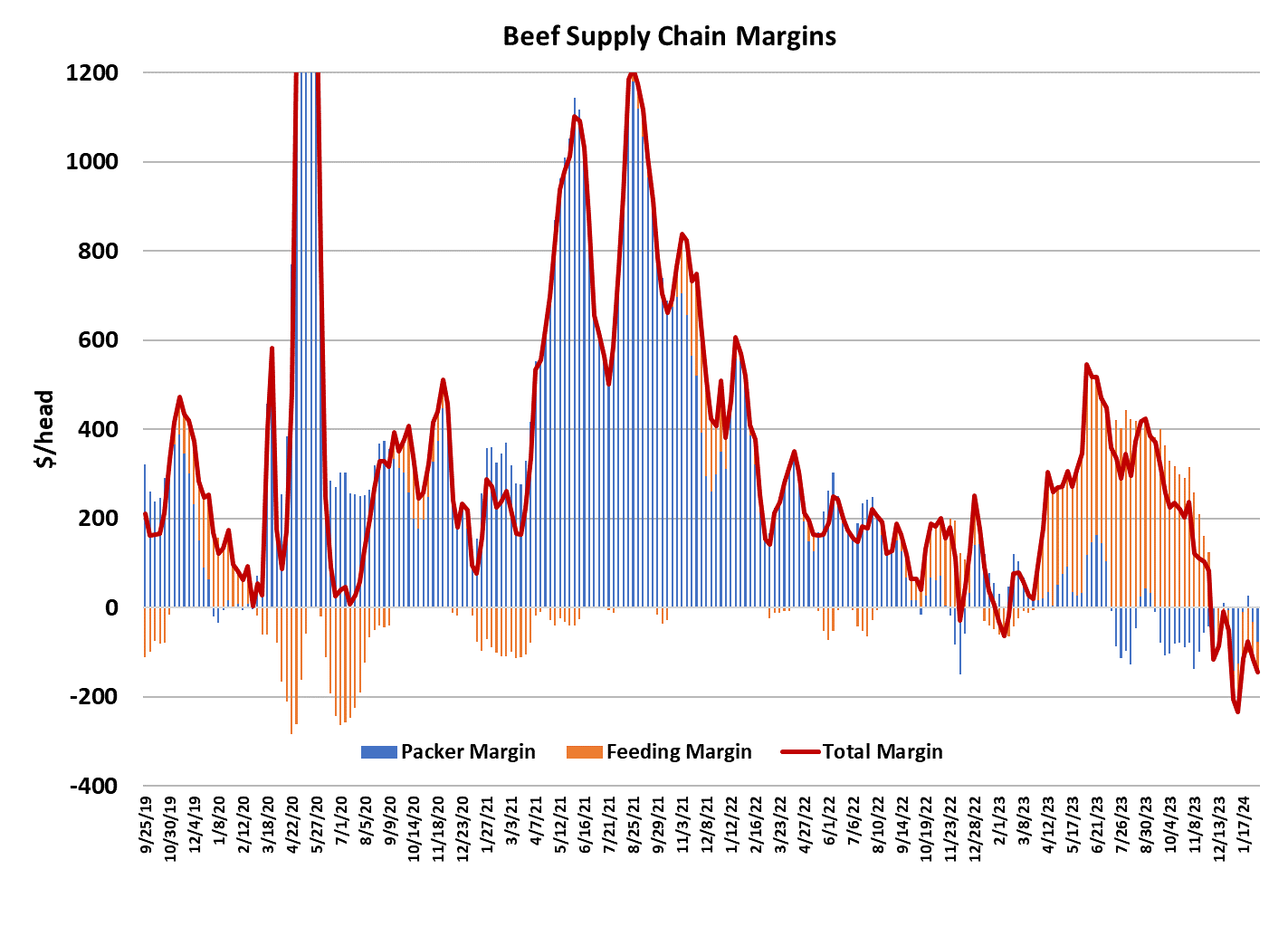

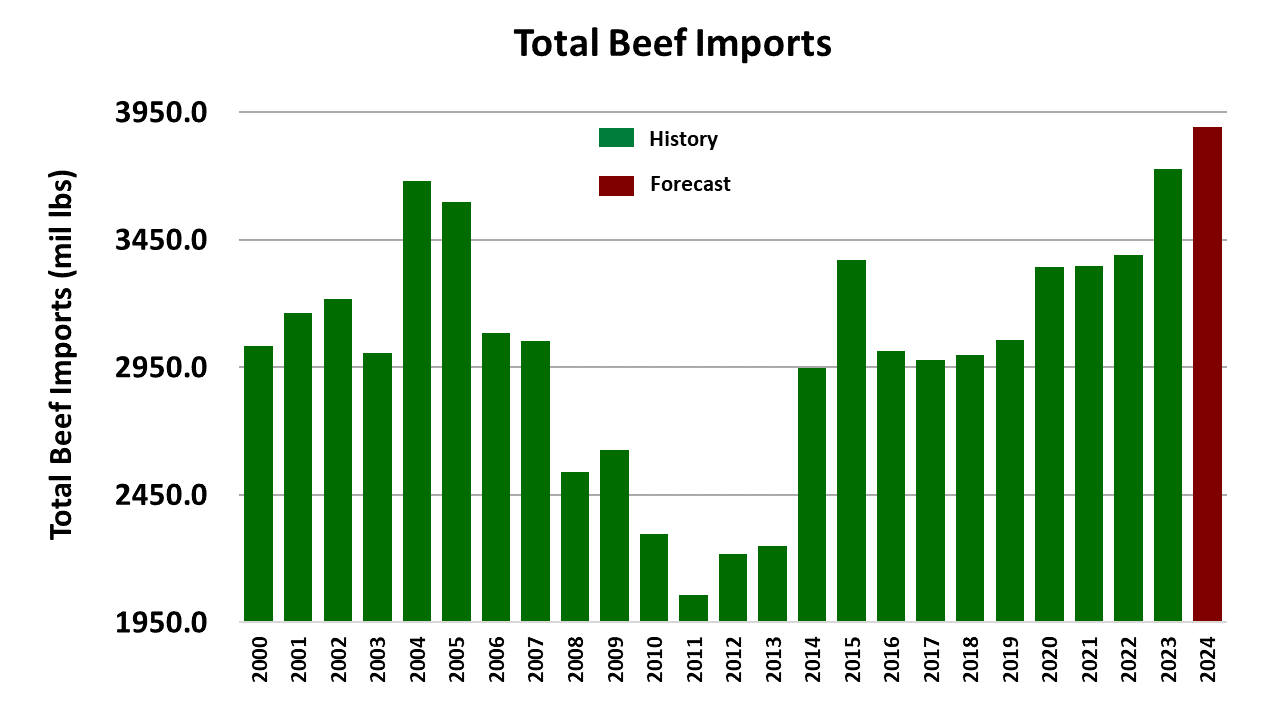

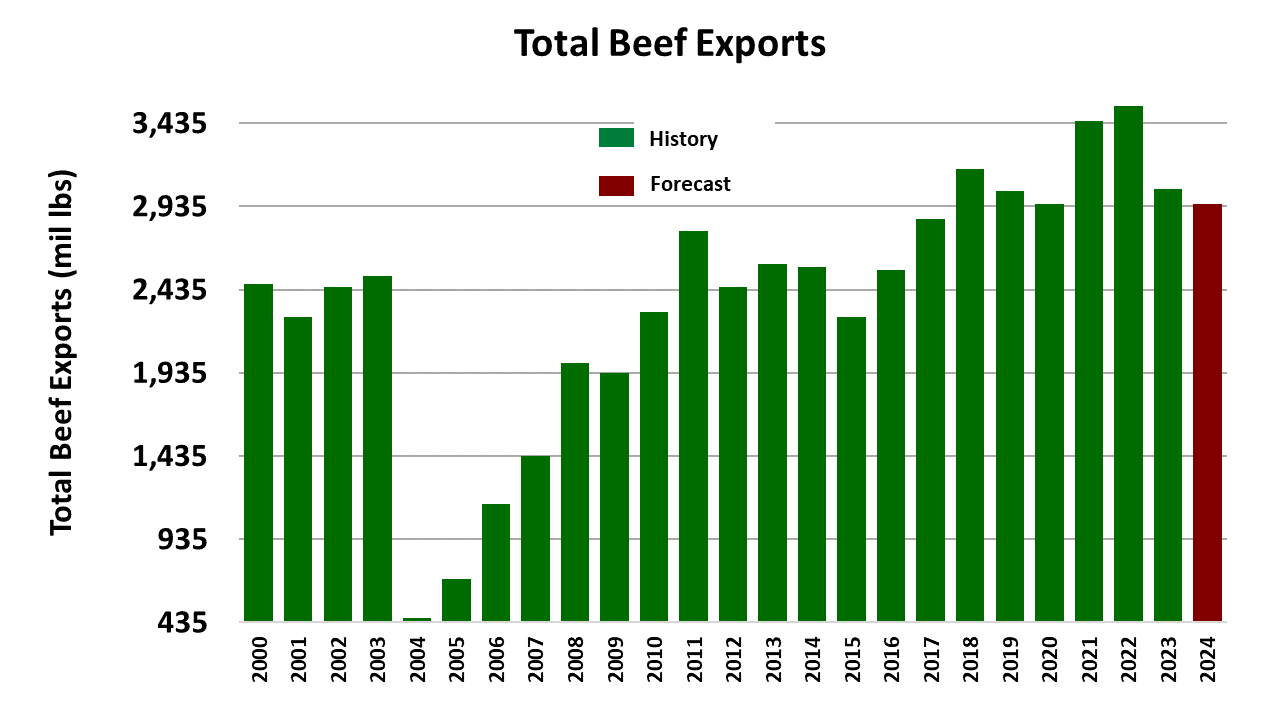

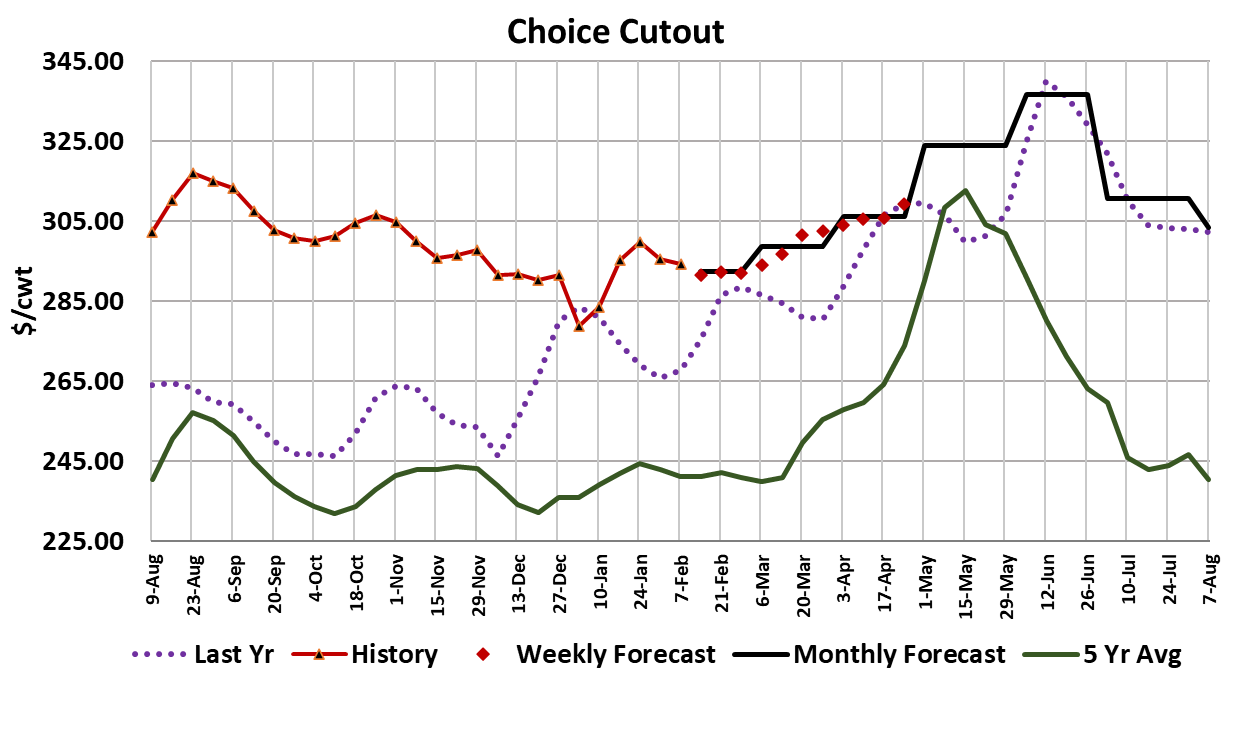

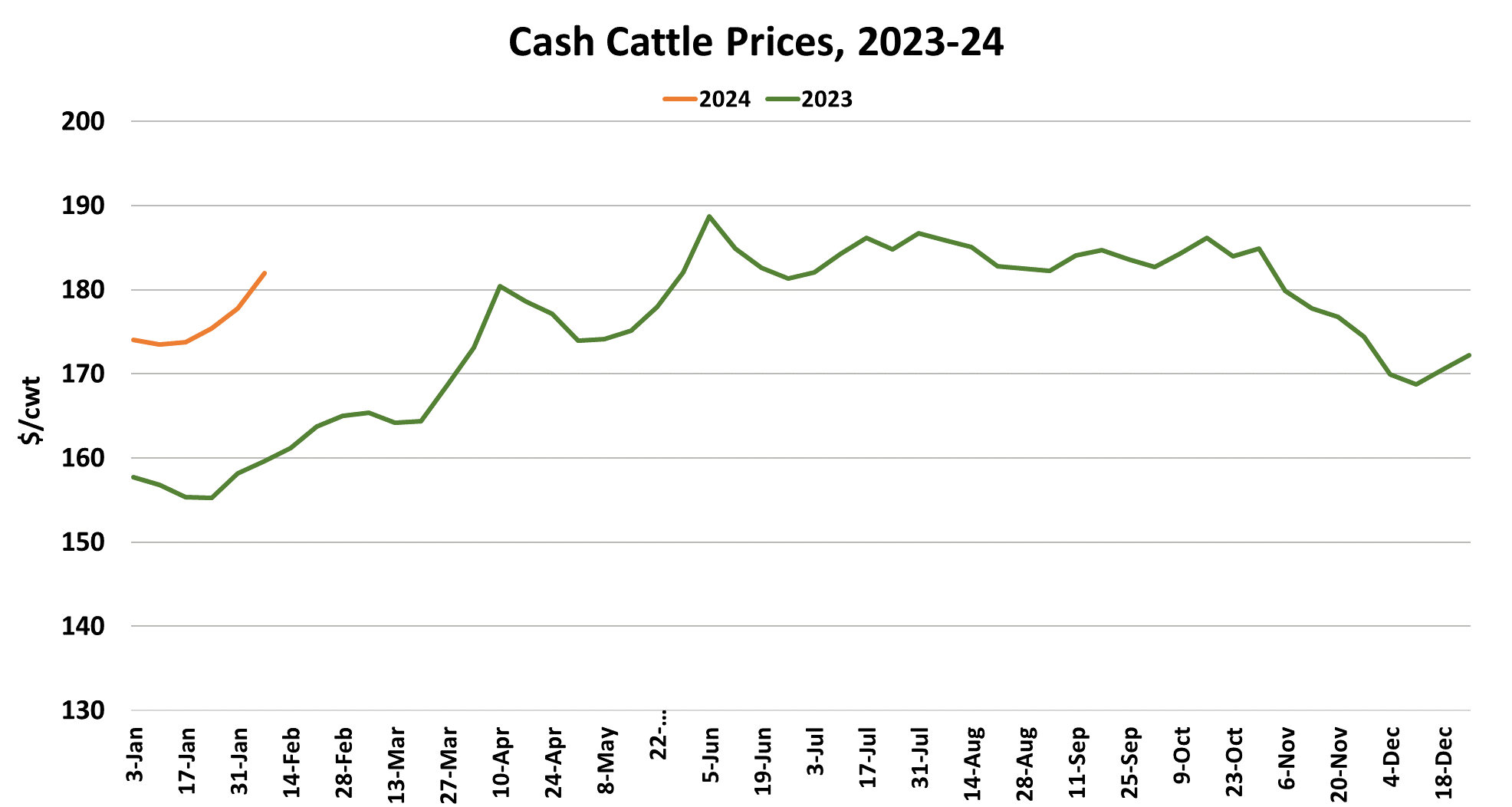

Cattle feeders held out until late on Friday and were rewarded with cash prices that were close to $4/cwt. higher. Trade in the Southern Plains developed at $182 and in the northern dressed market there were reports of cattle changing hands at $287-290, up $7-10/cwt from the previous week’s average. If there was ever any doubt as to who currently holds the leverage in this market, those doubts have been erased by this week’s sharply higher market. Feb futures, which is now in delivery, was telegraphing the cash market move as it added $4.07 on the week. It is unclear at this point how many cattle packers managed to buy at $182 but it is common for volumes to be large when the price increases several dollars. They do that when they are trying to position themselves so that they can avoid having to pay up the following week. FI carcass weights dropped hard again this week, with steer weights reported down 6 pounds and heifer weights down 8 pounds. Steer weights have now declined 25 pounds in just three weeks. At the end of 2023, steer weights were running 27 pounds over last year and that gap has now been almost completely erased. The weather in cattle country has been mild for over a week now and next week looks relatively mild also, except for a modest snowstorm that is forecast to come through the Texas Panhandle on Sunday. One would expect that by now feedyard cattle have recovered from the stress of the polar vortex in early January, but the carcass weight data makes it look like there is still some catching up to do. The frigid weather during January seemed to discourage feedyard placements and we are hearing early estimates for the upcoming Cattle on Feed report that would have January placements down 10-15% YOY. If that comes to pass, then we could easily have feedyard inventories as of Feb 1 back below last year. The futures market would likely applaud that in a big way. However, front end supplies of cattle are still relatively large and so there could be some price weakness later this month or in early March as feeders attempt to incentivize packers to run larger kills in order to work through the bulge in market-ready numbers. That is probably why the Apr futures are only carrying a slight premium to the Feb contract at present. Cattle placed in January will finish in the marketing “sweet spot” of May and June, when beef demand is usually very strong and price levels high. If January placements really were down 15%, then that strong demand period is likely to coincide with tight fed cattle supplies. That won’t be very helpful to beef buyers looking to procure middle meats for Memorial Day and Father’s Day. This week’s fed kill came in at 487k, down 15k from the week before. Packers are already starting to throttle back on the kill it seems. I estimate that packer margins this week were about $78/head in the red and that is likely to grow to $150/head in the red next week when this week’s pricey cattle show up for slaughter. Packers will be trying to coax higher money out of beef buyers early next week, but I doubt that they are going to have much success on that front. February is notorious as a soft demand month and the cutouts actually declined this slightly this week, with the blended cutout losing $1.20/cwt. to average $292.65. All primals were lower this week except the round primal and that may be indicative of generally softening demand. The combined margin has turned lower also, which may signal the start of a short-term downcycle in demand. February is rarely kind to beef packers, but this year looks particularly bleak. One piece of the puzzle that looked better was the weekly export numbers, which moved 3% over last year, even thought the cutout is running about 11% higher than last year at this time. That weekly export data can be a little goofy at times, so I’d want to see a few more weeks of YOY increases before getting too excited. The official trade data for December came out on Wednesday and export volume was down 5.2% YOY. For 2023 as a whole, beef exports were 14.1% lower than in 2022. Beef imports continue to run very strong, up almost 24% YOY in December and up 9.9% for 2023 in total. Next week, watch for the cash cattle market to cool down some. Cattle feeders may get another increase, but it isn’t likely to be more than a dollar or two. At some point soon, packers might stop tapping the brakes on the kill and actually slam down hard on the brakes. That would have the potential to move the cattle market lower and the beef market higher. Beef buyers shouldn’t get too complacent.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}