Beef Wrap February 16

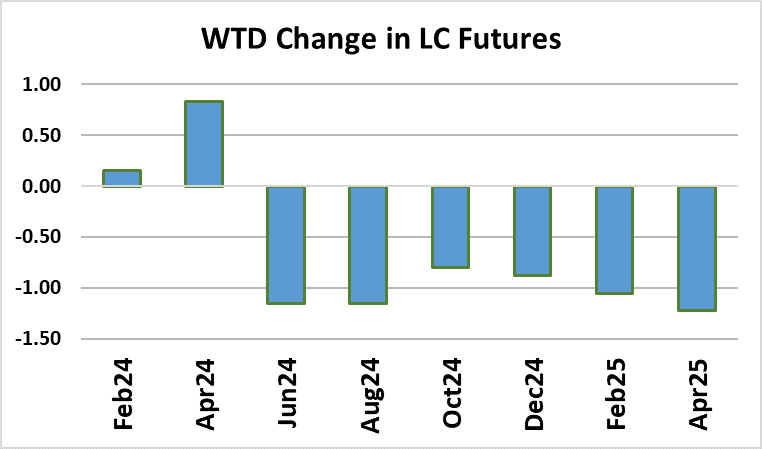

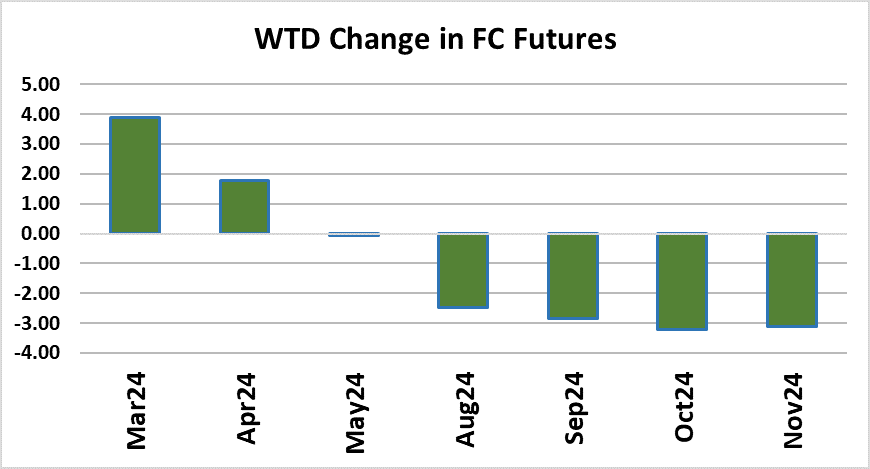

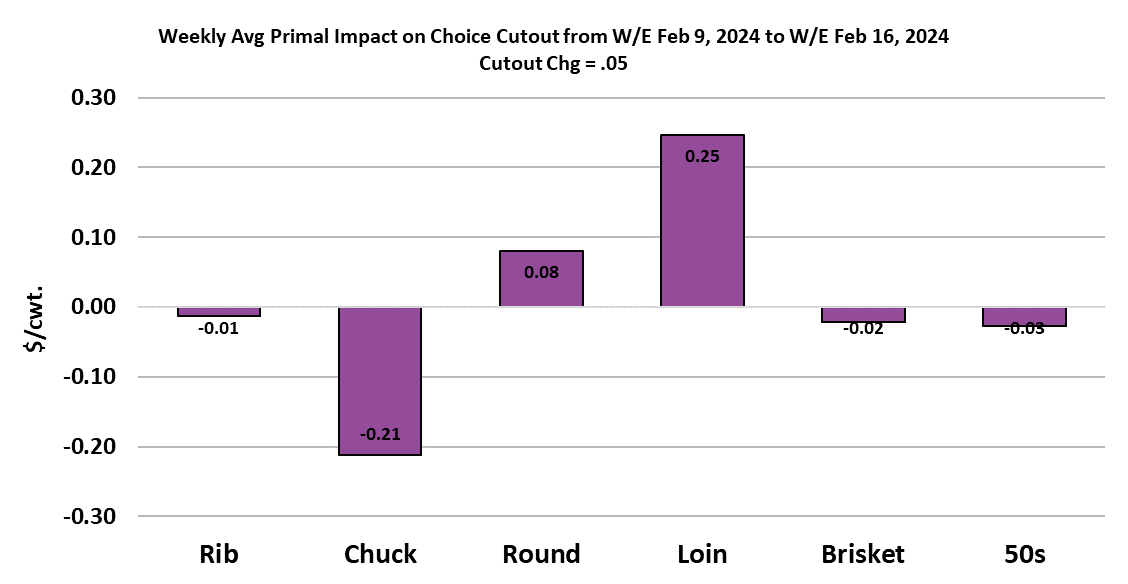

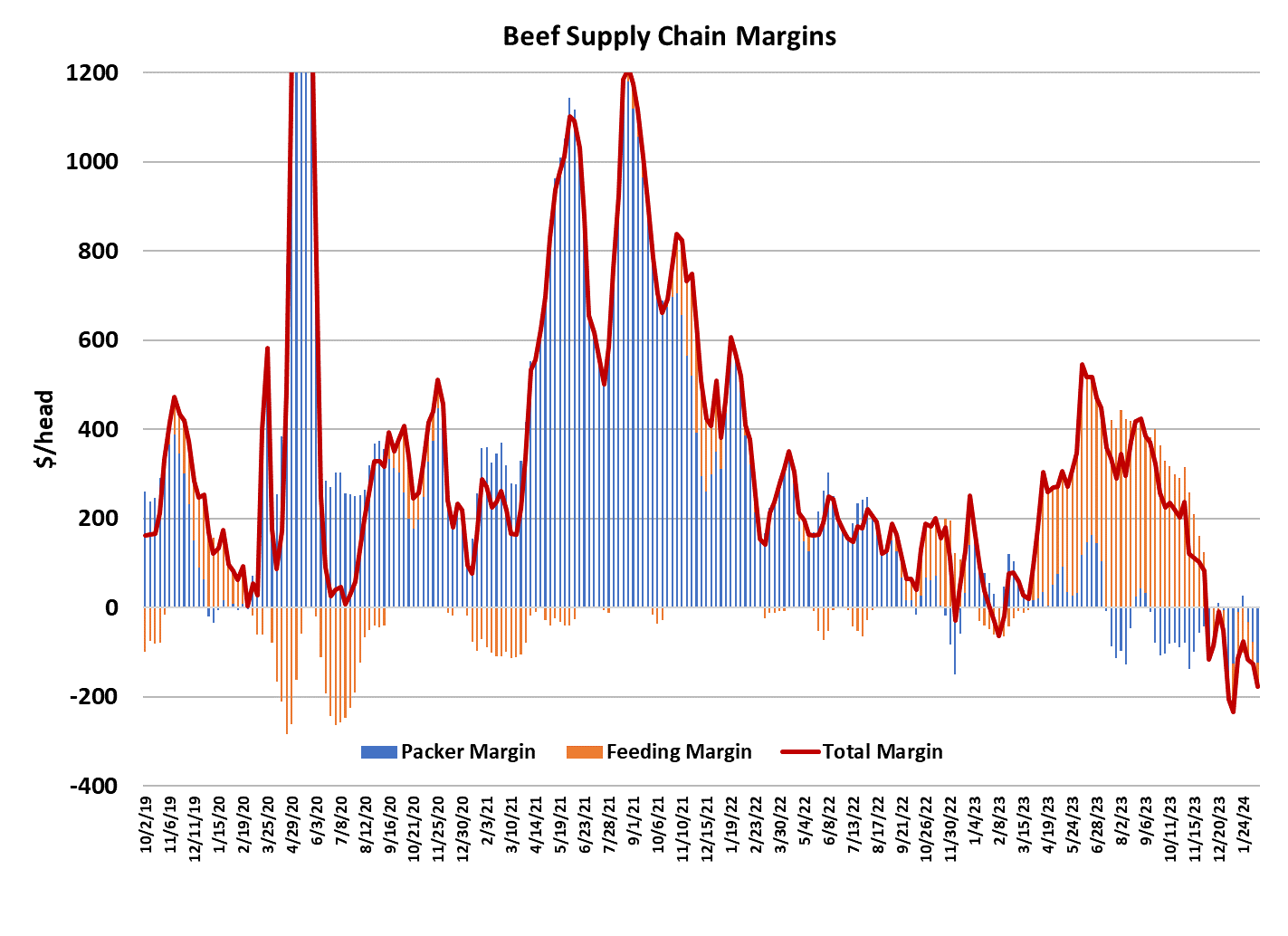

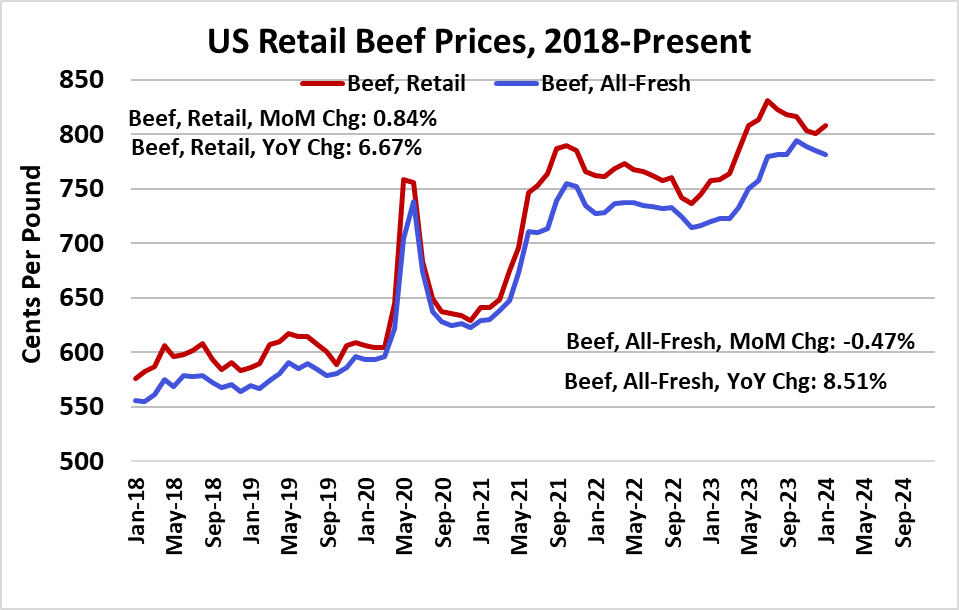

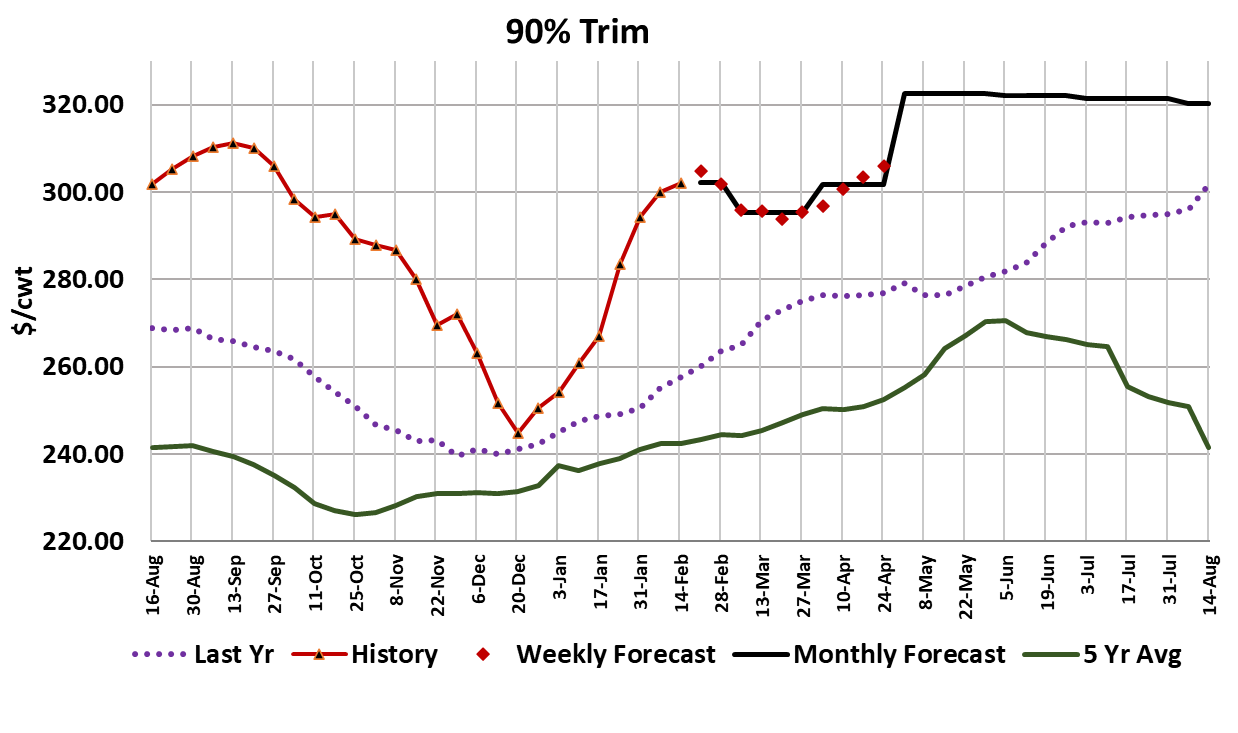

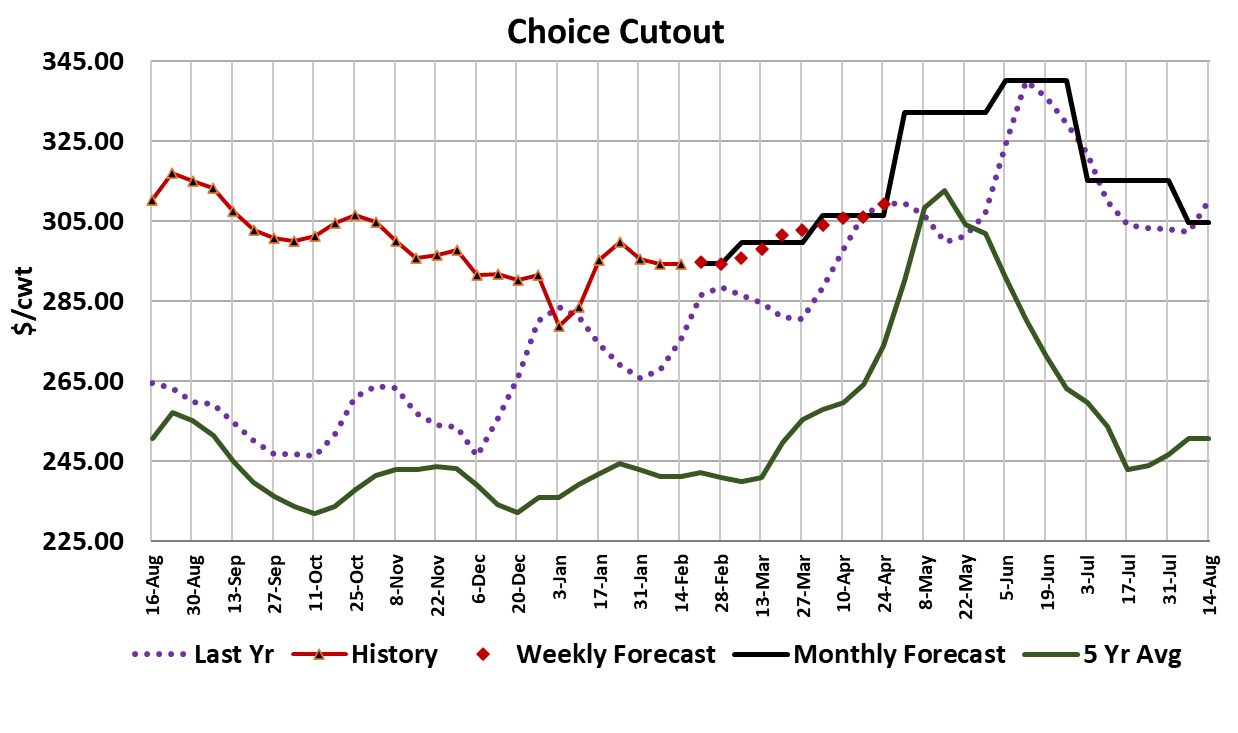

Cattle futures started the week with a negative tone, posting losses for the first three days. Packers seized on the opportunity and began bidding $178 on Tuesday. By Wednesday, they raised bids to $180 and found cattle feeders to be willing sellers at $2 under the previous week’s price. Once the cash market had largely been determined, the futures did an about-face, closing higher on Thursday and Friday. For the week, Feb futures were nearly unchanged, but Apr added close to $0.75/cwt. After seeing the late-week futures action, there were probably some cattle feeders that wished they hadn’t been so quick to jump on the Wednesday cash bids. The trade volume in cash cattle was rather large once again this week, so packers should have ample cattle inventory around them next week. That might allow them to hold the cash market steady while they try to figure out what to do about their margins, which were about $120/head in the red. Clearly, keeping the fed kill suppressed is part of their margin enhancement strategy, but so far it hasn’t yielded much benefit on the beef side of their business. On a weekly average basis, the Choice cutout only added $0.05/cwt. this week, while the Select gained $1.60/cwt. There wasn’t much in the way of clear trends in primal pricing this week. The chucks gained a little and the loins lost a little, but it was otherwise a pretty flat week. Demand is typically pretty weak in February and this week saw the combined margin drop further, which isn’t a good sign for near-term demand. Retail prices for December were released this week and the “all-fresh” retail beef price declined a bit, while the traditional retail beef price increased a small amount. Both are running 6-8% over last year. Retailers appear to be in no hurry to reduce their beef pricing and that will limit consumption at the consumer level. The CPI came in stronger than expected this week, causing traders to temper their expectations for interest rate cuts over the next few months and sending yields higher. Retail sales for January came in weaker than expected, possibly signaling that consumer spending is beginning to slow. So, the macro environment is suddenly looking a little more vulnerable than it has in a while. The cheapest items in the beef complex, trimmings, have seen very good demand lately. Beef 50s were back over the $100 mark as of Friday afternoon and the domestic 90s market topped $300/cwt., gaining over $50 in the first six weeks of 2024. Light fed kills are helping to support the 50s. Cow slaughter was down close to 20% YOY in January and that likely played a role in jump-starting the 90s, but in the last couple of weeks non-fed slaughter has pulled back to near last year’s level and prices continue to rise. That suggests some demand improvement. This week’s fed kill was estimated at 474k, down 9k from the week before. The Saturday kill was almost non-existent. It is common for fed kills to be light in February because cattle availability normally declines and packer margins are often in poor shape. This year however, I’m not sure that cattle availability is down all that much because packers have constrained slaughter for months on end now and that should be leading to a build-up of market ready cattle. I was looking for that backlog to affect the market in January, but then the polar vortex caused cattle weights to come crashing down, effectively buying cattle feeders more time with which to market those cattle. FI steer weights were reported down 3 pounds this week, but heifer weights were up 2 pounds. It looks like the weather impact on weights has now faded and the forecast for the feeding areas is rather benign for the next couple of weeks, so the risk of further weather-related problems is declining. Drought, which has plagued a large portion of cattle country over the past 2-3 years, appears to be fading and that should lead to much better pasture conditions this spring. With feeder cattle prices at very high levels, there should be strong demand for diverting more animals to grass, where weight can be put on at a much lower cost than in the feedyard. That causes the production process to take longer and thus reduces the availability of finished animals this summer and fall. Next Friday, USDA will provide another Cattle on Feed report, and it is expected to show January placements down somewhere in the vicinity of 10-15% YOY. Those are cattle that will finish this summer, so there is another source of potential supply reduction this summer in addition to more cattle taking the grass detour on their way to the feedyard. Thus, the supply picture several months down the road looks quite bullish, but the industry must first navigate through the supply of backed-up cattle and that could mean some near-term price retracement. Beef exports continue to impress in the weekly FAS data, running very near last year’s level even though prices are more than 10% stronger than last year. Next week, look for some further easing in the cutouts and a steady or possibly lower cash cattle market. Trading cattle at mid-week didn’t work out so well for cattle feeders, so it seems likely that the cash trade will wait until next Friday.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}