Beef Wrap February 17

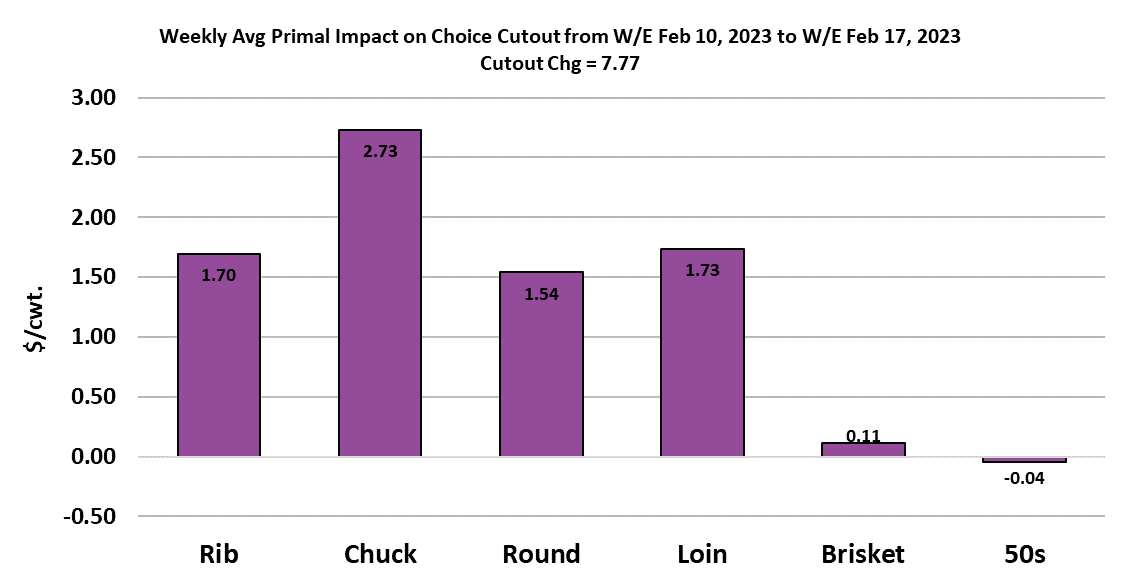

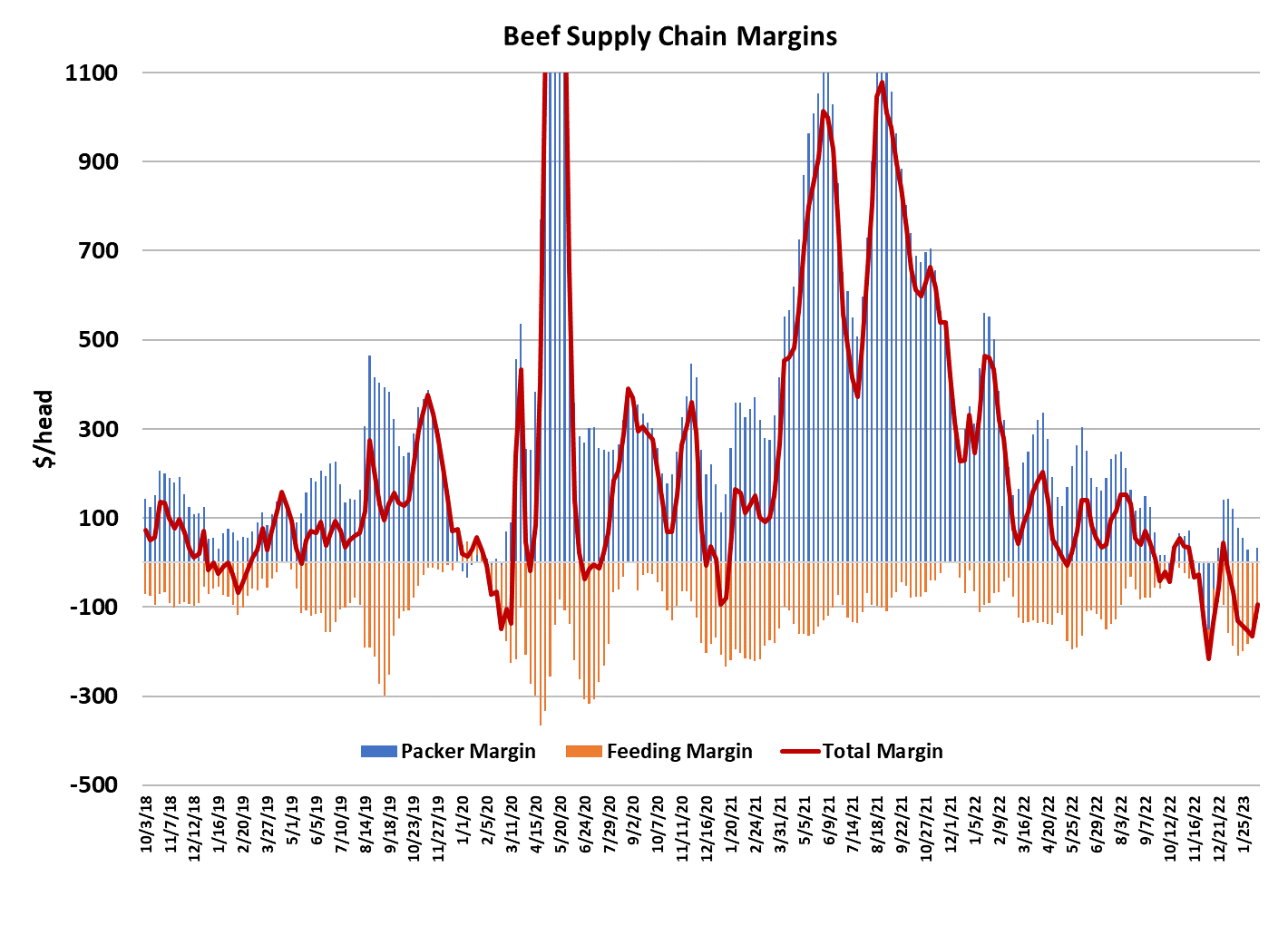

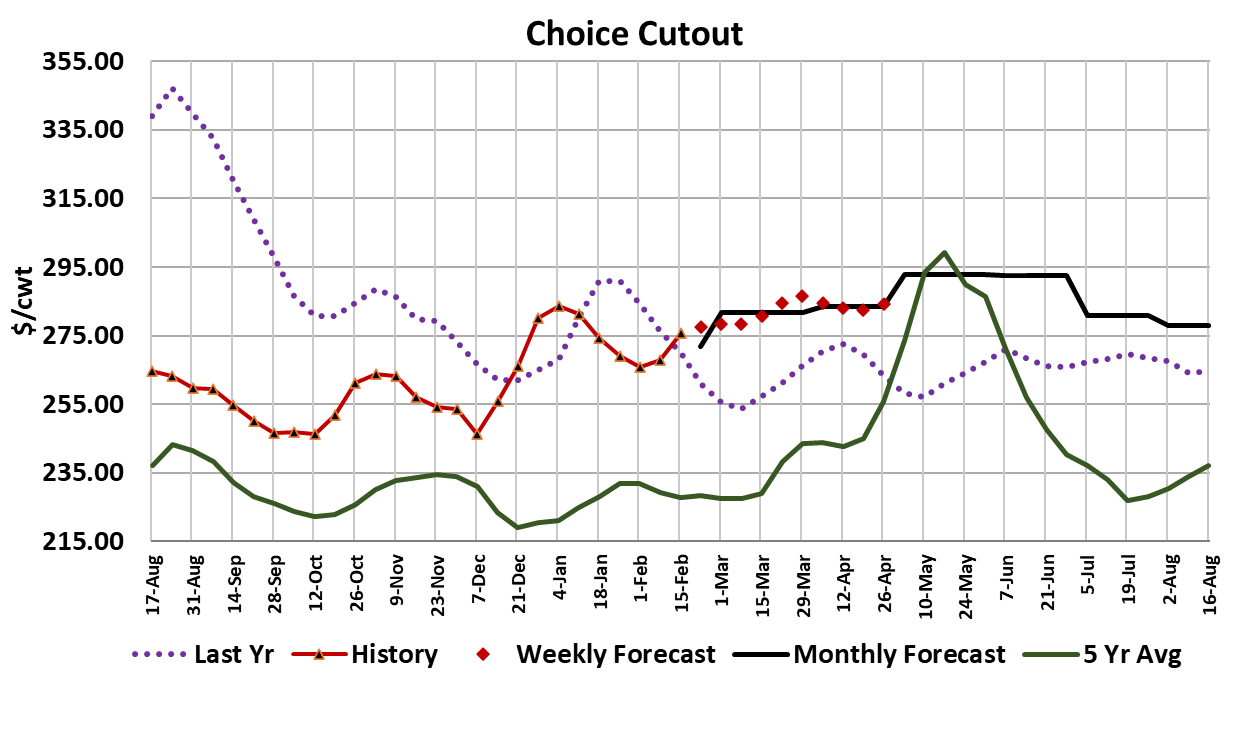

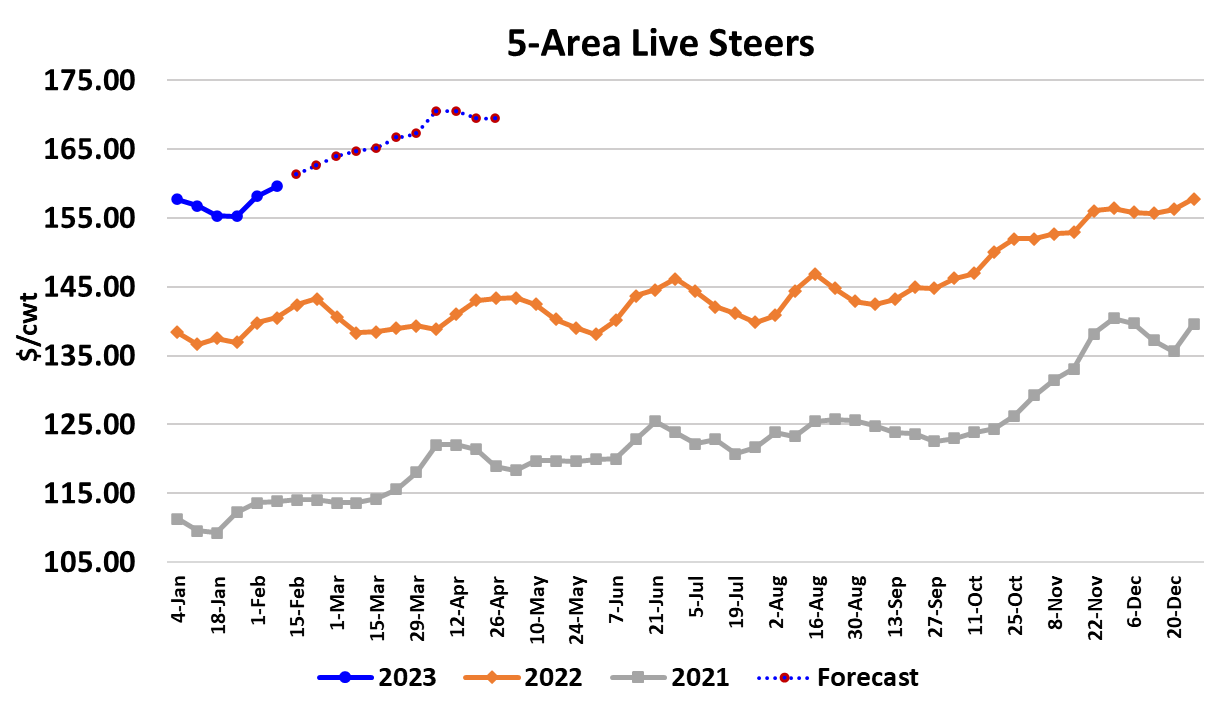

The beef market made a stunning turn higher this week, with the Choice cutout gaining $7.77/cwt and the Select adding $6.44/cwt. Packers have been having to pay up for cattle in the last couple of weeks, so they probably got serious about extracting more from beef buyers. They will need to repeat that trick again next week, because they paid up for cattle yet again. Once all of the trade is counted and reported on Monday, I expect that it will show average live prices close to $161.40, up about $1.75/cwt from the week before. There have been reports that a good chunk of cattle in feedyards are weather-stressed and probably not gaining like they should. As a result, cattle feeders feel no urgency to move them unless they see prices advance. However, even with the price gains over the past few weeks, cattle leaving the yards in today’s $161-162 market are still losing money for their owners. Breakevens on those cattle are probably north of $165 and may be approaching $170. Packers are doing a bit better, as their margins moved higher this week given that the gains in beef prices outweighed their increased cattle costs. I have this week’s packer margin at roughly $45/head, up from almost zero last week. The combined margin took a strong turn higher this week, signaling a new upcycle in demand. It seems too early for this to be the spring demand surge, so it is likely that this upcycle will peak and move through another downcycle before the spring demand surge becomes evident. I don’t want to attribute all of the recent price gains to demand however, because kills have dropped back into the 480-490k range from around 500k in January so smaller beef production is helping to boost prices. The attached chart shows that the chuck, round, rib and loin all participated in driving the cutout higher this week. Middle meat demand continues to be impressive with the rib primal currently priced 17% above last year and the loin primal up 9% from last year. These are the highest rib and loin primal values ever for this time of year. End meats also surged this week, but grinds and trims underperformed. One thing to keep an eye out for is that the extra benefit given to food stamp (SNAP) recipients during the pandemic will expire at the end of this month. It will mean that each person in that program will receive about $90 less each month to buy food. Those folks probably aren’t buying a lot of middle meats, so I wouldn’t expect much impact on those, but lower priced items like ground beef and end meats could see a significant drop in demand when March rolls around. Equity traders had to reassess their thinking on interest rates this week as new data showed prices not cooling quite as fast as they had hoped and thus the Fed may keep interest rates higher for longer than most were assuming. I don’t think that we are going to get a recession in the first half of 2023 and I’d put a low probability on that occurring in the second half of the year. Those that were hoping for interest rate cuts this year will likely be disappointed. It is pretty clear from the combined margin chart that those regular demand cycles are still going to repeat, but they are not likely to reach anywhere near the heights that were achieved during the pandemic. This week’s fed kill is estimated at 481k, down 8k from last week and right in line with what our flow model suggested should be ready for slaughter in February. Expect the fed kill to hover around 480k for a few more weeks before expanding back towards 500k per week in March. The kill is so small now relative to capacity that packers are barely running on Saturday. This week’s Saturday slaughter was only 7,000 head and at least 3-4k of that will be cows and bulls. Steer carcass weights declined 2 pounds this week, but heifer carcasses were 3 pounds higher, so the blended carcass weight was unchanged. The DTDS weights are hovering in the -5 pound area and are not really indicating a lot of impact from the weather yet. Beef production was estimated at 513 million pounds, about 9% below last year at this time. The fundamental forecast has steer and heifer beef production down 3.3% for Q1 as a whole and it calls for a 5.7% decline in Q2, when the spring demand surge is likely to occur. That makes me think that we could have some pretty high middle meat prices this spring and thus buyers would be wise to get out in front of that now, before the spring rally. Export demand still looks good and imports have been dropping as the dollar softened, so that will contribute to the tightness in beef availability over the next several months. USDA will give us another Cattle on Feed report next week and I expect that it will show feedyard placements down about 3% YOY and total feedyard inventories down about 4% YOY as of February 1. Tightening cattle and beef supplies are going to be an ongoing theme in this market for the next 2-3 years at least. Next week, watch for indications that buyers are balking at the further price increases packers are going to be looking for. Keep an eye on the weather also, because we are not quite clear of the winter weather danger that could further curtail beef production.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}