Beef Wrap February 10

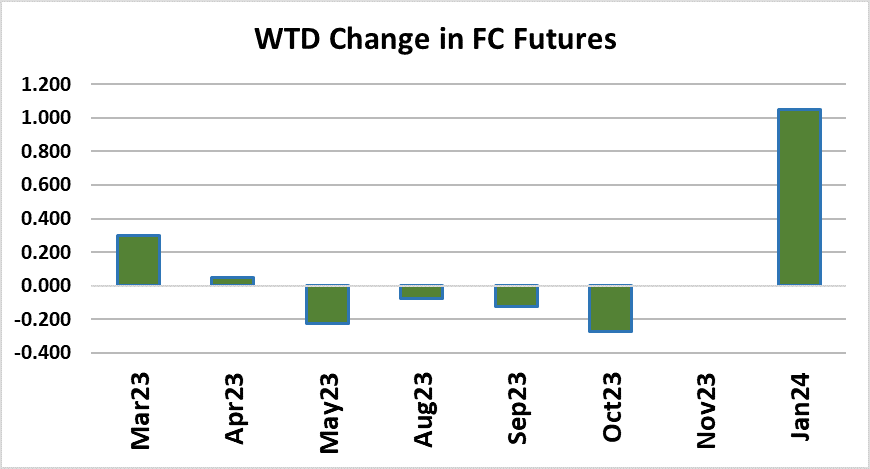

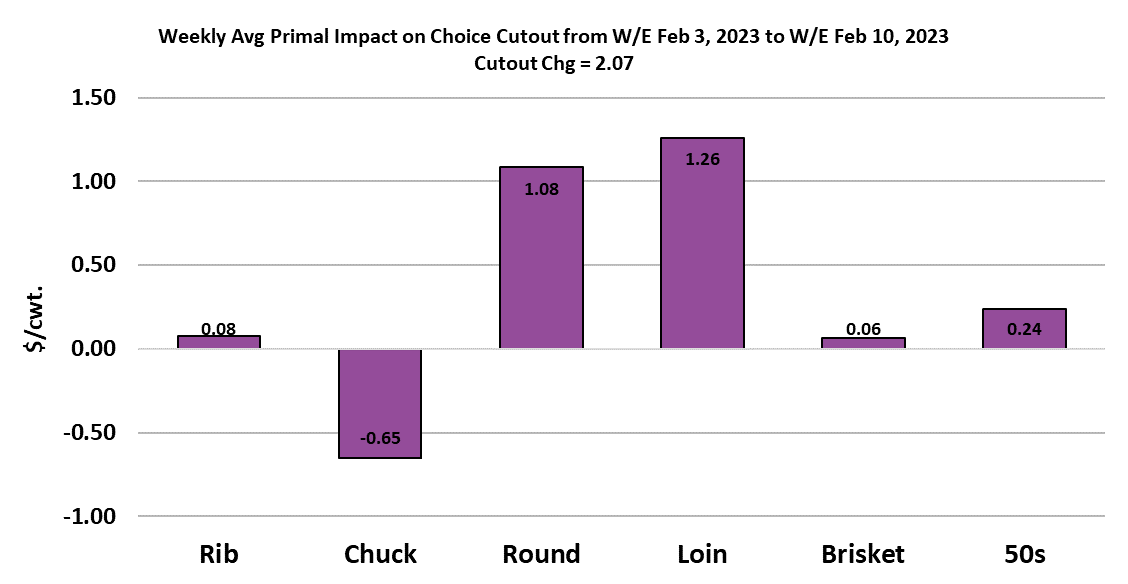

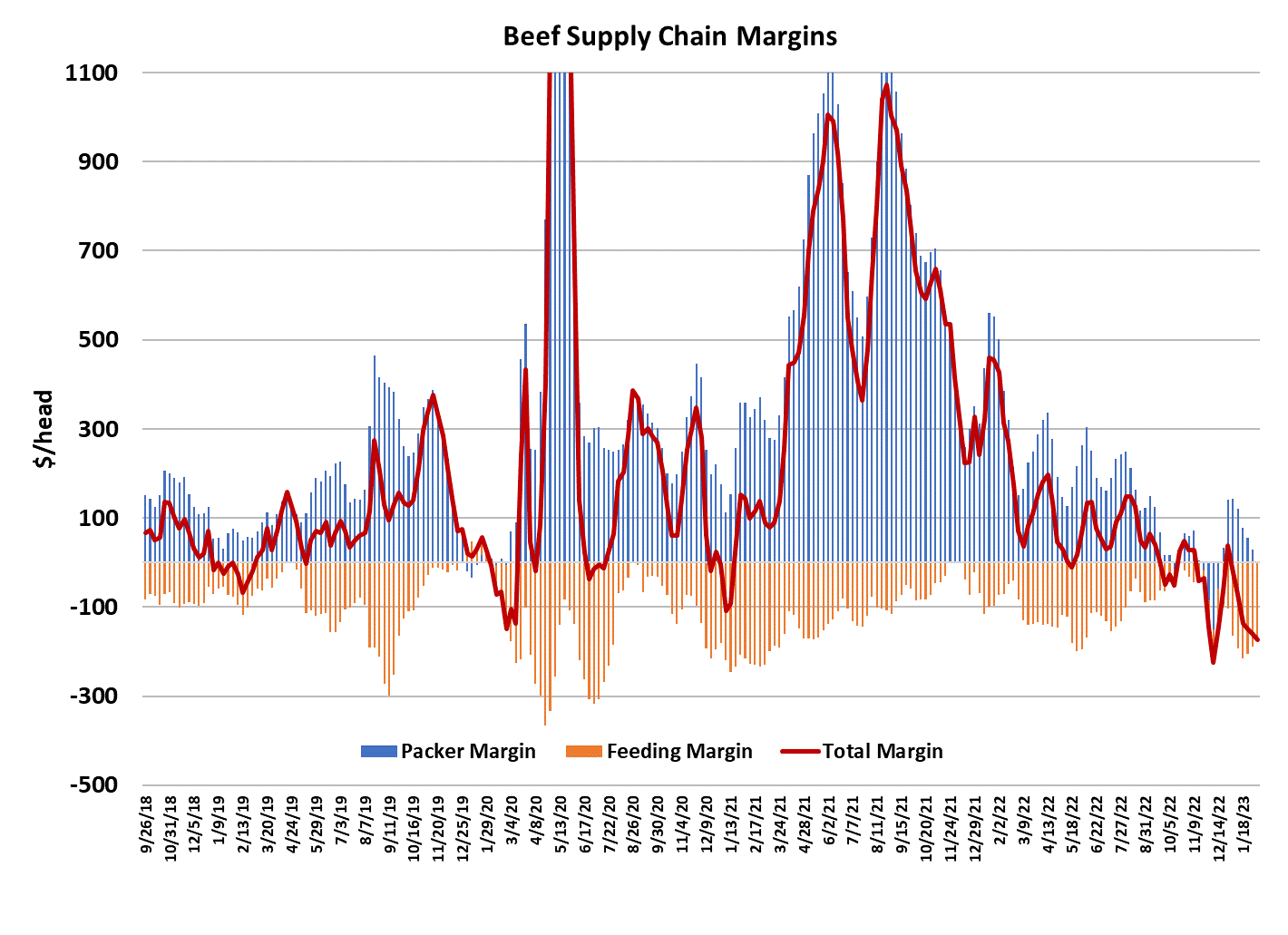

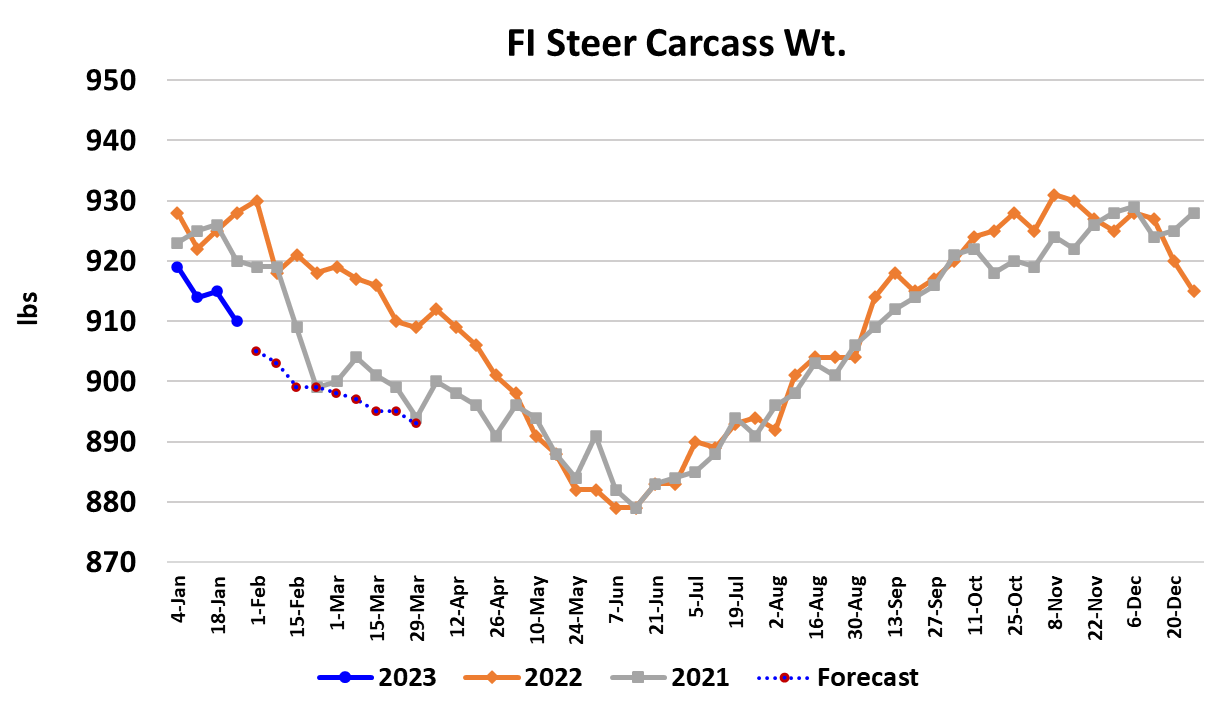

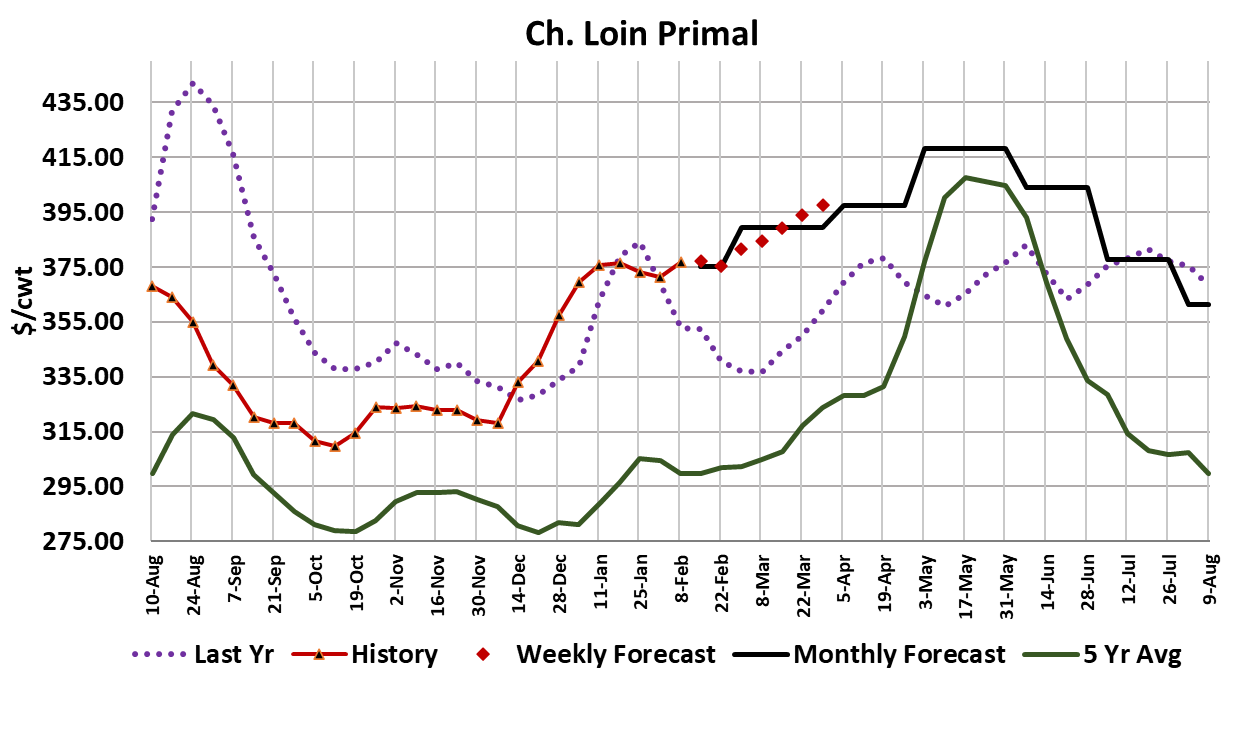

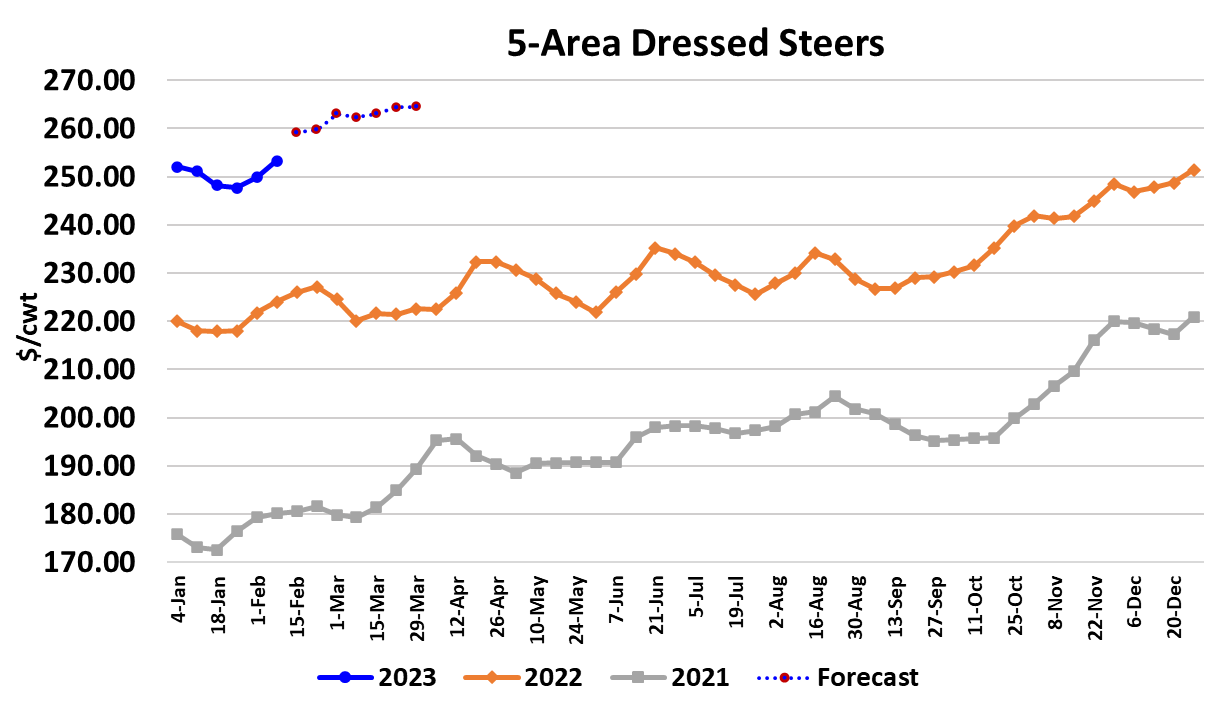

The beef cutouts moved modestly higher this week, with the Choice and Select both gaining a little over $2/cwt. Of course, cattle feeders wanted their share of the bounty and they forced packers to pay about $1.50/cwt. more for cattle than they did last week. Cash cattle prices in the Southern Plains were in the $160-161 range late on Friday and in the North the dressed trade was mostly in the $253-254 range. Packers seem almost powerless to stop the advancing cattle market. This week their margin was only about $2/head and when these more expensive cattle show up for slaughter next week packer margins should move to about $20-30/cwt. in the red. Cattle in the South have been affected by several winter storms now and that has increased cattle feeder leverage in that region. Some feedyards are sloppy in the North too, but on-feed numbers are likely a little larger in that region. As a result, the South is quickly becoming the price leader. This week there were 10 deliveries tendered against the Feb futures to a delivery point in the Northern region—a sign that the North has the cheapest cattle right now. Those 10 deliveries were retendered and then quickly demanded, which could be a sign that at least one packer fears that cash will rise again next week. It looks like the volume of cattle traded this week was bigger than last week, so it probably puts packers in a better inventory position. This week’s fed kill was pretty conservative at 483k, down 13k from last week. That is right in the ballpark of what our flow model has suggested would be available during February. It is definitely in packers best interest not to get too aggressive with the kill, especially because there seems to be a considerable number of weather-impacted cattle in feedyards right now. Steer carcass weights dropped another five pounds this week and the forecast has them tracking rapidly lower over the next few weeks as a result of the weather. That may lead to higher cattle prices, but it also leads to higher cost of production for feeders. Beef demand doesn’t look great at the moment, but the smaller kills could keep the cutout from sliding any lower. March is not to far in the distance and we should start to see some decent demand improvement once it arrives. If packers can just keep the kill contained for a few more weeks, they might be able to move their margins back in the black this spring. However, if they go on another over-killing binge like they did last fall then spring could be a real problem profit-wise. Middle meat demand continues to be very good for this time of year, especially for loin items. That is a reflection of strong demand from upper-income consumers through both the retail and foodservice channels. Lower-income consumers have mostly burned through their pandemic savings and are more focused on end cuts and grinds from the beef complex, but here beef has to compete with cheaper pork and chicken and so demand from this large swath of consumers hasn’t been all that great. It creates a delicate balancing problem for packers who want to produce lots of the middles that are bringing strong prices, but yet that also produces a lot of the ends and grinds, which are not doing as well. It is one thing to “kill for the middles” in anticipation of the holiday season, but that strategy probably won’t work very well in the dead of winter when demand for the ends and grinds is softer. One thing we can see very plainly: aggregate beef demand isn’t strong enough to cover the cost of producing it in this high corn price environment. Just look at the attached combined margin chart which suggests that the industry is about to re-test the multi-year lows that were set last fall. This is the market’s way of sending the signal that downsizing is needed so that prices can rise to a level that provides at least modest profitability for the supply chain players. But the cattle industry is like a big battleship and the long production cycle means it takes a while from the time that the signal is sent until the necessary outcome is achieved. Chicken and pork can respond much quicker to market signals and they likely will. International demand seems to be holding up pretty well since the first of the year, so that is a demand bright spot but unfortunately only about 12% of US beef production gets marketed through the export channel. I’ve adjusted cut price forecasts upward recently and thus don’t have a lot more near-term downside risk built into the cutouts, but they might not move a lot higher either due to relatively soft demand. March should bring better demand and solid gains in the cutouts. Buyers that need Choice+ middles for spring grilling season might want to consider booking at least a portion of their needs now while the market is relatively tranquil because those items could get pretty pricey this spring. Next week, watch for packers to reduce the kill even more than this week as they try to tip-toe through the minefield that is February without getting a leg blown off.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}