Beef Wrap December 24

The cash cattle market declined again this week, dropping about

$1.50 to average $135.55. The cutouts stabilized, with the Choice

nearly unchanged on a weekly average basis and the Select up about

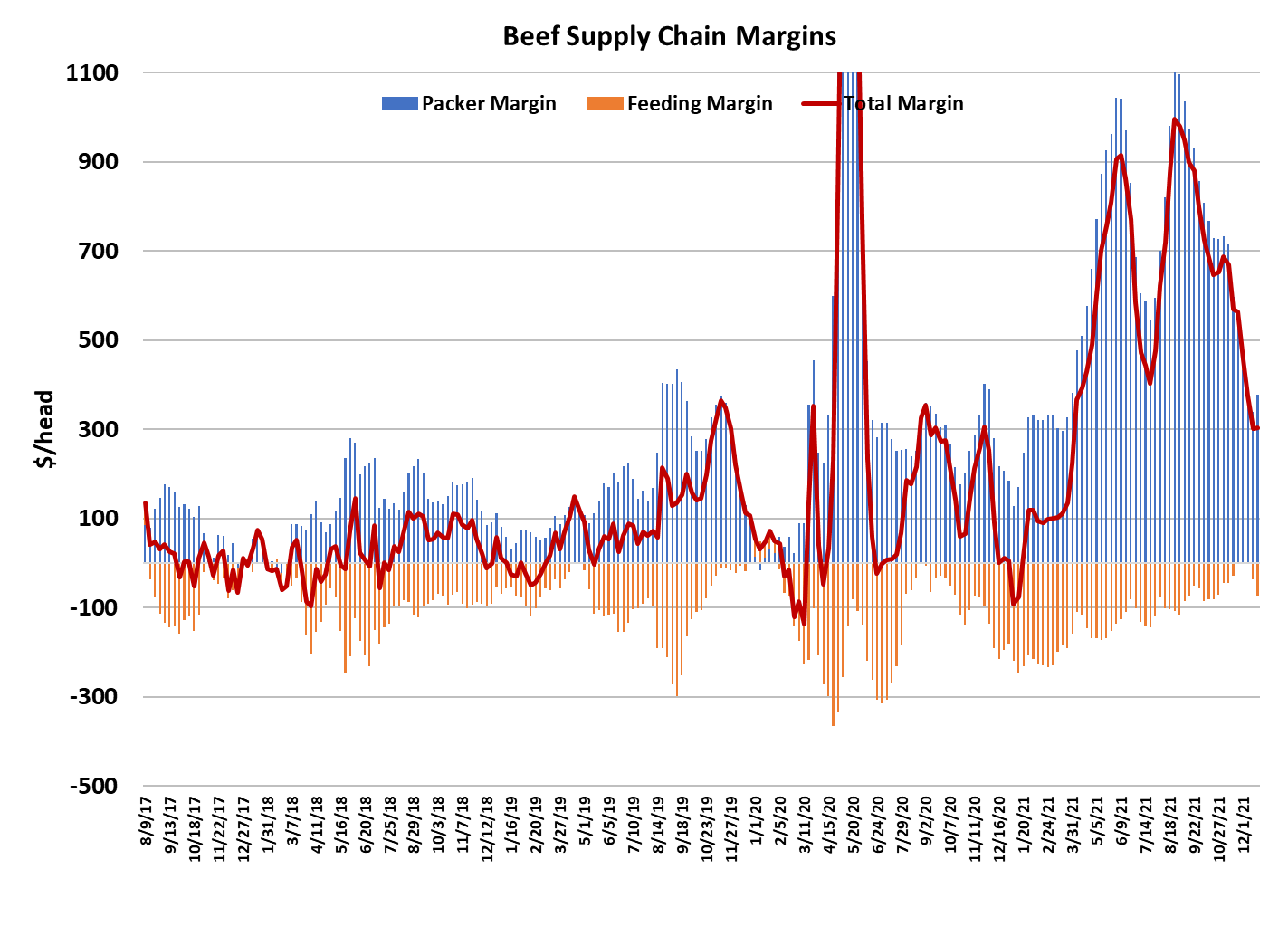

$2. That allowed packer margins to increase modestly, now at $377/

head. Analysts are watching the COVID situation closely in the US

as the virus seems to be spreading rapidly right in the midst of the

biggest travel season that has occurred in over 2 years. It seems

almost a given that infections are going to spike in the next 2-3 weeks

to levels we have never seen before. That spells trouble for the 40%

of the population that is unvaccinated. The important question for

meat demand is how will society react? Already we are seeing

important sporting events like football bowl games being cancelled

because one or both teams has so many COVID infections that they

can’t field a team.

Restaurants are cautiously eyeing this trend and my guess is that a

lot of them will be forced to close over the next few weeks. That could

result in a surge in retail meat demand yet there is no indication that

retailers are ramping up purchases in order to prepare for such an

event. That is probably because we were headed into Christmas

week and everyone figured it could be dealt with after the holiday.

That makes me nervous that we are going to see aggressive buying

in the next couple of weeks just when the supply chain is rather bare

because of holiday-reduced kills. Of course, we could see an

offsetting decline in purchases from the foodservice sector, but that

might lag the retail surge by a few weeks. The other thing that needs

to be considered is the impact of rapidly rising COVID infections on

harvest operations. Most of the major packers have been requiring

employee vaccination for some time and my guess is that they will

aggressively step-up their booster programs since it seems that

having the booster is the key to not getting infected with the omicron

variant. They also have pretty solid routine testing procedures in

place so they are likely to catch most COVID infections before they

are spread among co-workers.

Still, a lot of plant workers are likely to get infected visiting with family

and friends over the holidays and that would cause them to need to

be quarantined for a few days. So we might see a situation where

plants are able to operate, but at a reduced capacity. We already

know from previous experience that when plants can’t run at normal

rates, it is positive for beef prices and negative for cattle prices.

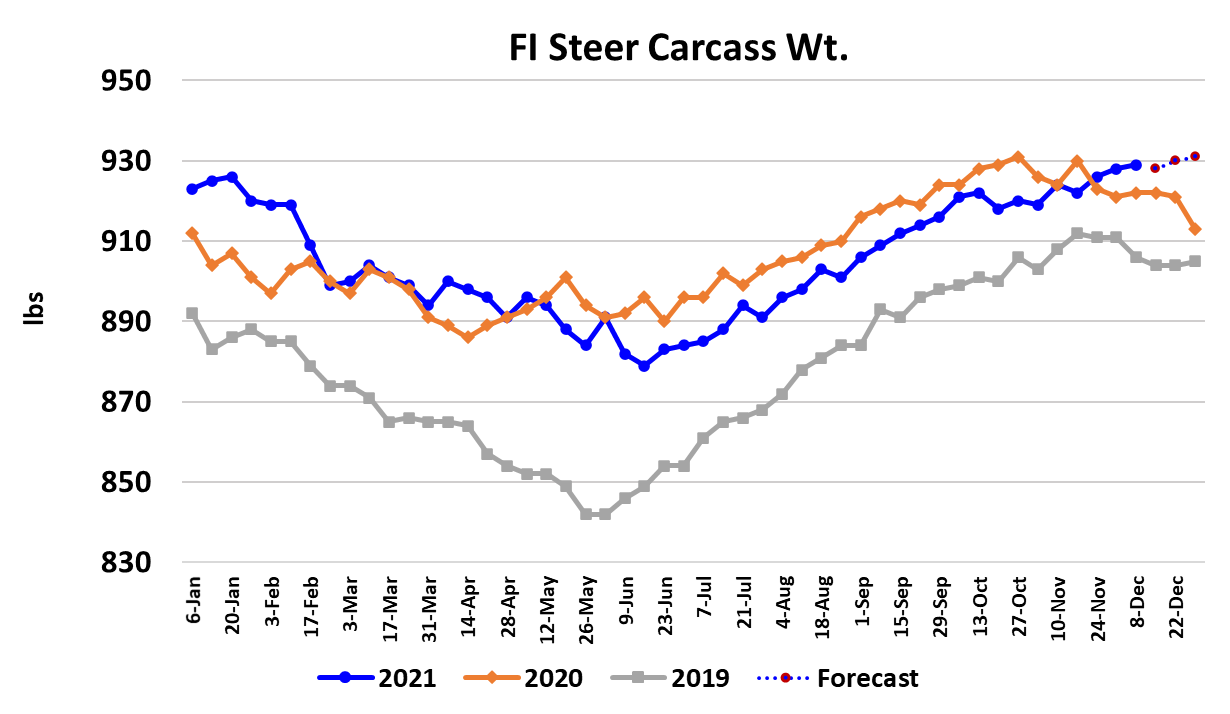

Unfortunately for cattle producers, feedyard supplies are quickly

rebuilding after the Oct-Dec “hole” that was created by small

placements back in late spring and early summer. Cattle

performance has been excellent also. Carcass weights are currently

near all-time highs. So there is little room for cattle feeders to absorb

a slowdown in kills without a lot of cattle becoming excessively heavy.

My sense is that the supply side would backlog rather quickly. The

strong cattle performance is being driven by exceptionally mild

weather in the Plains States. There have been very few snow events

in cattle country so far this year. The chart below indicates that

carcass weights are now above the very heavy levels registered in

2020 when cattle got severely backlogged due to plant closures. The

DTDS weights are also well into positive territory now and moving

quickly higher. I have seen very little concern among industry

participants about cattle weights and it makes me think that the

industry is going to get blindsided by this in January. COVID-related

plant slowdowns would just accelerate this brewing problem. Packers

will likely do a very light kill on Friday and zero on Saturday to

produce a weekly fed kill in the 380-390k range.

Next week, I see the Friday kill being bigger, but still way down from

normal and thus rendering a fed kill in the 410-420k range. So the

beef pipeline will be temporarily tight on product. Let’s hope retailers

don’t rush in when they see the COVID cases rocketing higher.

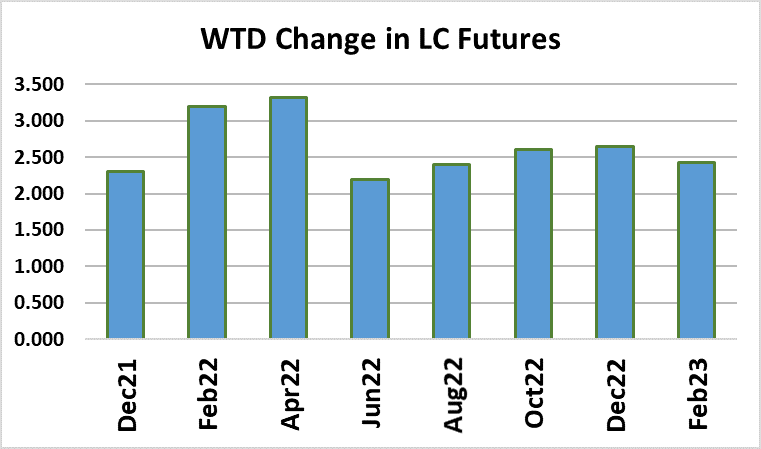

Futures traders seem oblivious to all of this as the most-active Feb

contract gained over $3 this week. There seems to be a sense in the

futures community that the cash cattle market is going to turn higher

next week as packers need to rebuild inventory for a full kill in the first

week of January. However, packers will have access to all of their

January contract cattle as soon as the calendar ticks over to 2022 and

that might allow them to be less aggressive than futures traders think,

particularly if they see rising COVID cases in their workforce and

realize that they won’t be able to run full-out in early January. On

Monday, the first order of business will be to react to Thursday’s

Cattle on Feed report. That report pegged November placements up

3.6%, which was very close to the average trade guess. That left the

Dec 1 on-feed inventory only a hair below where it was last year.

Traders will probably quickly shrug off the report and begin to focus

on the COVID situation and what it portends for the cash market in

January.

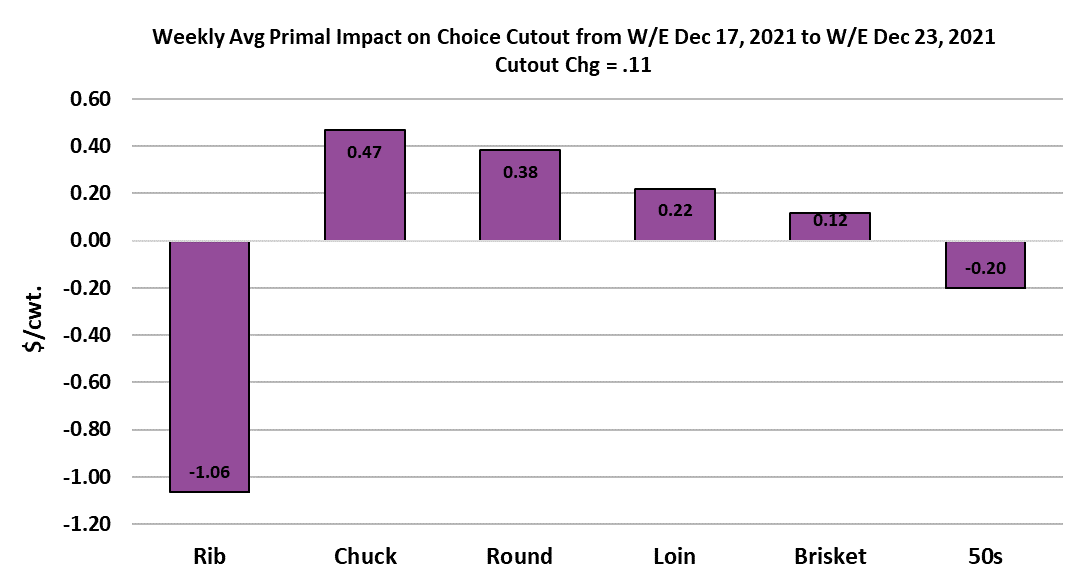

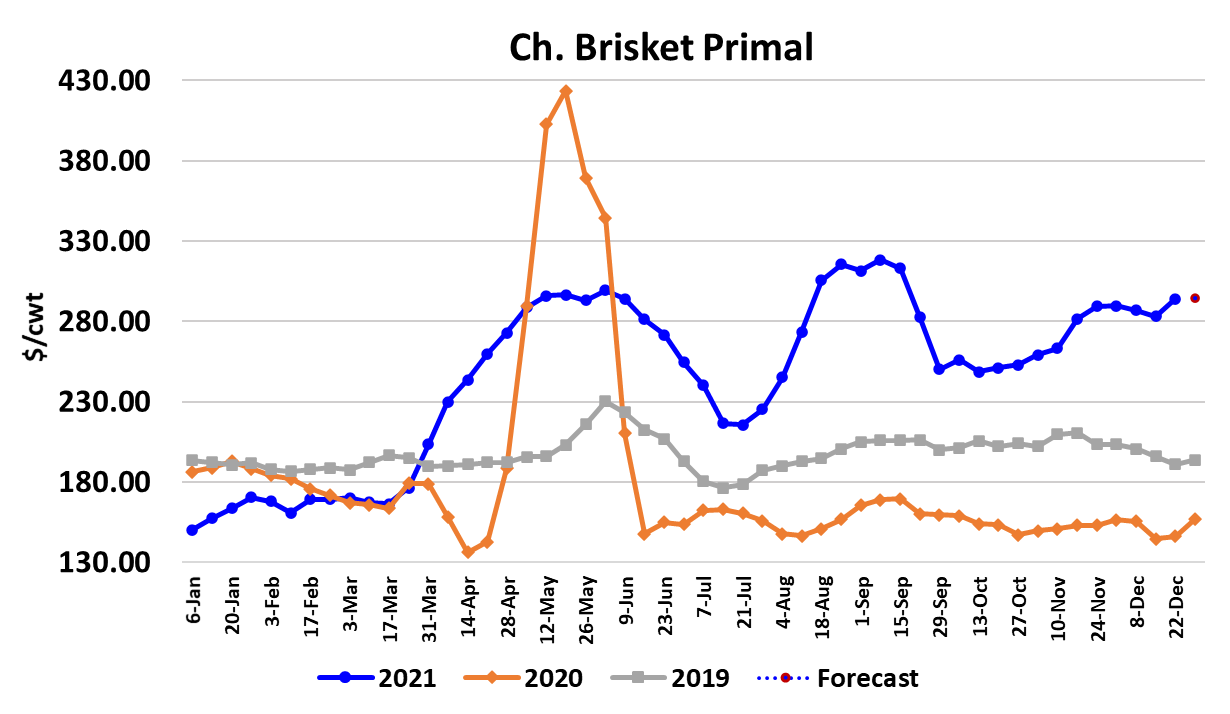

The beef market will soon be shifting out of holiday mode and into

winter mode where end meats and grinds will be carrying most of the

load in the cutout. We have already started to see that this week

where softness in the ribs was offset by strength in the chucks and

rounds. The 50s market could come under some supply side

pressure once kills get back to normal since very heavy cattle will

throw off a lot of fat trim. If retailers rush into the market out of

COVID fears, look for them to target the end meats first. Next week,

watch the news closely for rapidly escalating COVID infections and

the public’s reaction to them. In my opinion, that will be the most

important story for the next few weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}