Beef Wrap December 3

The cash cattle market moved higher once again this week, with

prices averaging $140.46, up a little more than $2 from last week’s

average. The cash market has added close to $16 in the last six

weeks. Can all of that be attributed to a tightening cattle supply?

Possibly, but it seems like an awful big increase for what should

have been a moderate tightening of the cattle supply in November

due to light placements in May/June/July. In the back of my mind, I

can’t help but think that perhaps packers came to the realization that

they were going to face some significant legal problems from the

Dept of Justice if they didn’t allow more of the massive profit from the

beef market to flow through to cattle producers.

There is no way to validate that of course, but I wouldn’t rule it out.

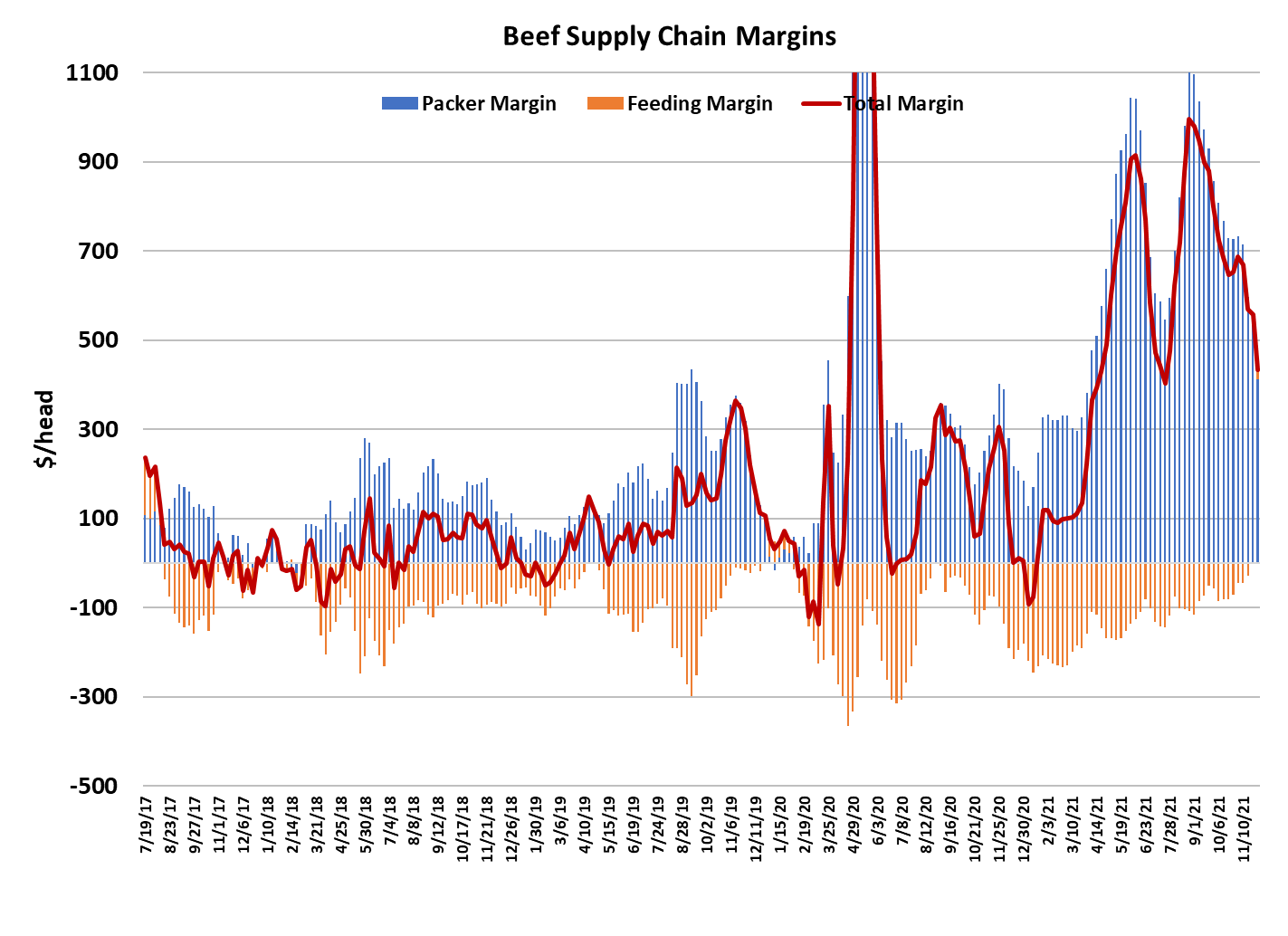

Regardless of the cause, the rapid upward acceleration in the cash

cattle market has had the desired effect of cutting packer margins

dramatically and boosting cattle feeding margins. And, all of this is

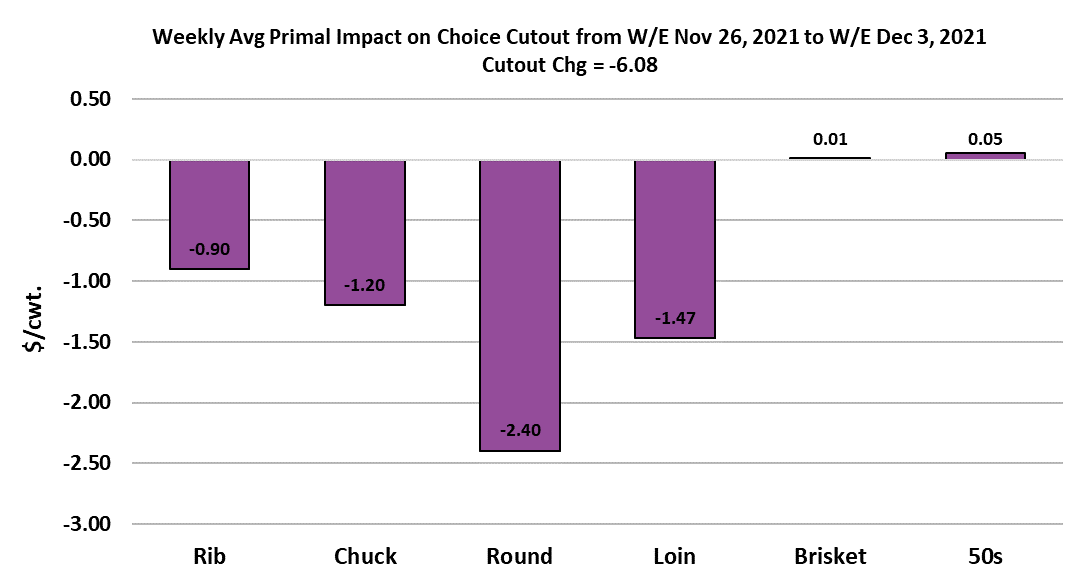

happening in an environment where beef prices are softening. The

week the Choice cutout lost a little over $6 on a weekly average

basis and the Select was down $3.60. Both end cuts and middle

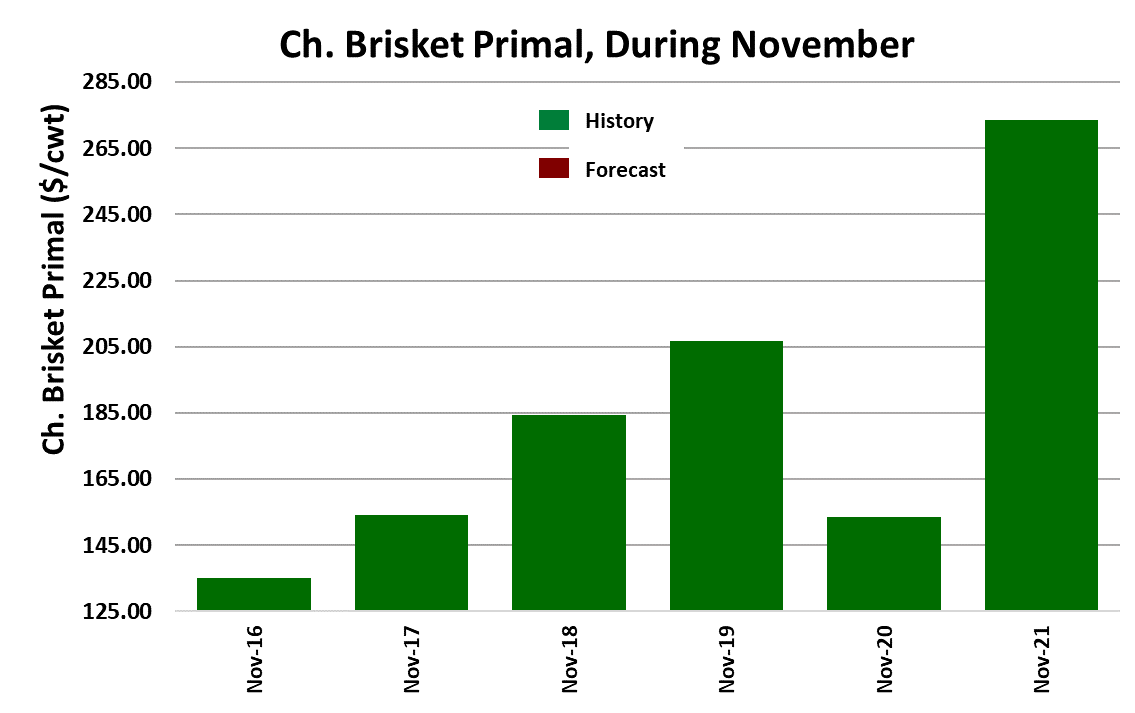

meats contributed to the declines this week. The only items to post a

gain were the fat trim and briskets. The end meats did start to show

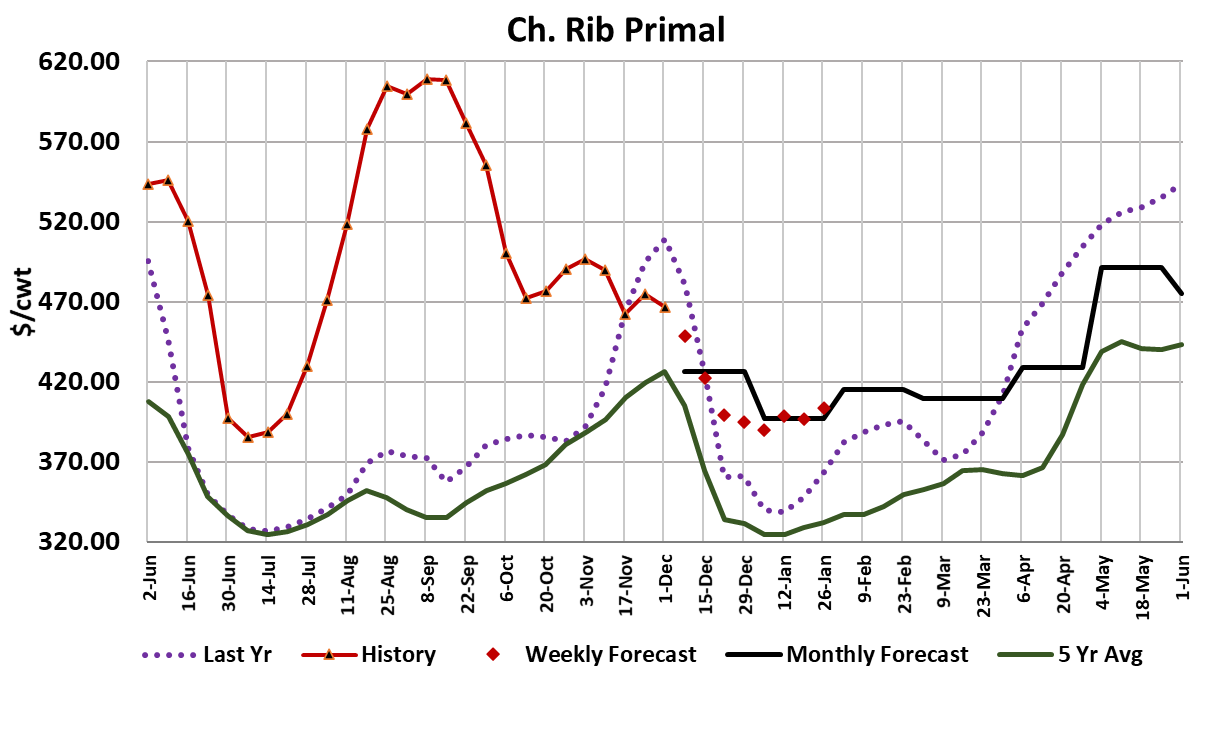

a little life toward the end of the week, but the middle meats are living

on borrowed time. Ribs normally peak in the second week of

December and then decline rapidly into the end of the year. Once

that strong seasonal pattern starts to take effect, it will be almost

impossible for the remainder of the primals to move the cutouts

higher.

Currently, I have the Choice cutout retreating into the $250-255 area

by the end of the year. That means further erosion in packer

margins, which have already taken quite a beating. Three weeks

ago, packer margins were in the mid $700s and this week they

averaged close to $400/head. Next week, I’m projecting them below

$300/head and the forecast has them moving slightly below $200/

head by January. So, if the packer’s objective was to improve the

optics around their margins, they have certainly accomplished that.

So far, they have shown very little resistance to higher cattle prices,

but that will probably change once the Christmas orders are taken

care of. Beef demand looks it is softening. The November demand

index was 1.23 and December is projected around 1.17. The

combined margin continues downward. The new COVID variant

presents the biggest uncertainly to demand direction in the next

couple of months.

If the variant spreads fast, makes people sick and evades the

existing vaccines, then we could see a return to the stay-at-home

behavior we have witnessed at other times when covid infections

spiked. That would be positive for beef demand. It might even elicit

some more government stimulus money. If, however, the vaccines

do end up providing good protection against this variant, then we

likely see a continuation of the current pattern which is more meals

from foodservice relative to retail and continued softening of

demand for beef. Keep in mind that January, and particularly

February, are not great demand months to start with.

The fed kill this week came in at 523k, down 6k from the week

before Thanksgiving. The cow and bull kill was huge at 153k. That

is probably a seasonal top in non-fed slaughter. It looks to me like

the fed kill is very close to, or maybe just a little above, what prior

placements suggest should be slaughter-ready. The weight data

doesn’t really make it look like packers are having to dig very deep

into the cattle supply either. Blended steer and heifer carcass

weights were up one pound this week, while steers-only were down

2 pounds. The DTDS weights have been slowly creeping higher—

another contradiction to the idea that feedyards are very current and

thus that is why packers keep throwing money at cattle feeders. If

nothing else, I suspect that the two short kill weeks at the end of the

month will tip the leverage meter back in the packer’s favor. Futures

traders seem to believe that also, pricing the nearby Dec contract,

which goes into delivery on Monday, $2-3 below the last traded cash

price.

Given the sharp rise in cash cattle prices, I am a little surprised that

cash feeder cattle values haven’t risen more. The FCI is above

$160 now, which is a pretty rare event in itself, but in the past cattle

feeders have been known to bid most of their profitability back into

the price of feeder cattle. Perhaps that just a few more weeks down

the road. Next week, look for cash cattle to trade steady or higher

and the cutouts to be steady to lower. Next week should be the last

hoorah for the ribs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}