Beef Wrap December 10

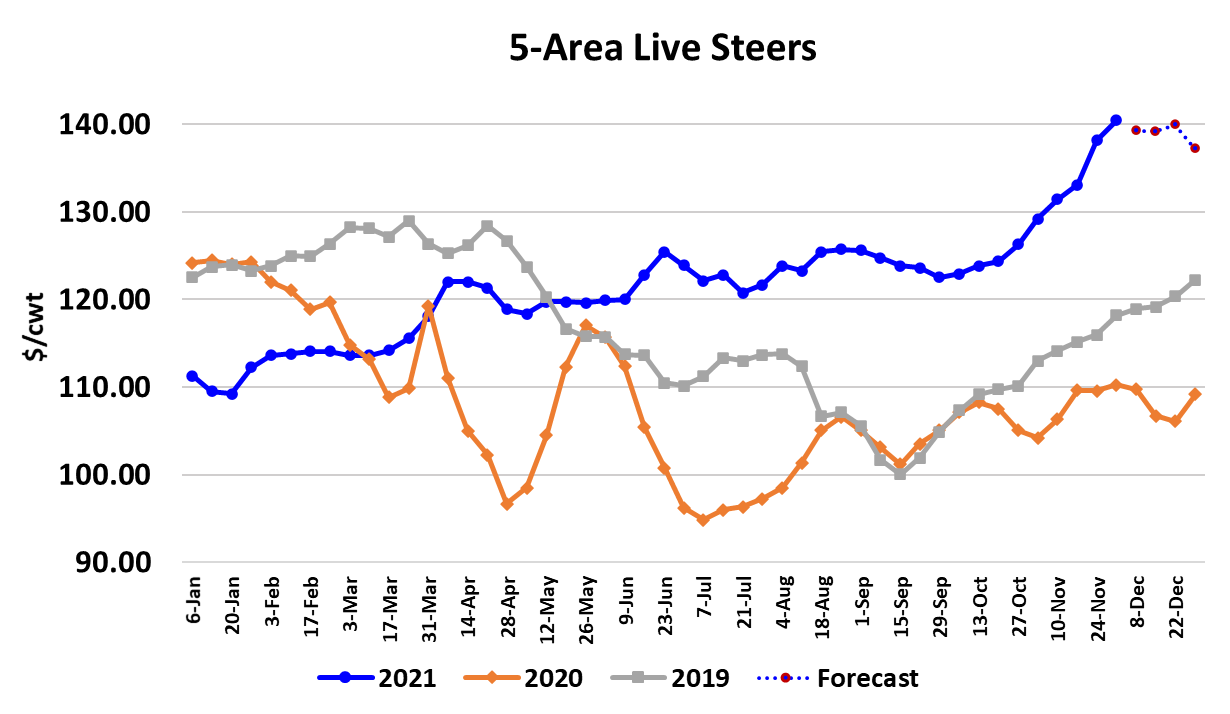

The cash cattle market finally took a breather this week. It looks like

live prices will average around $139.50, which is down about $1 from

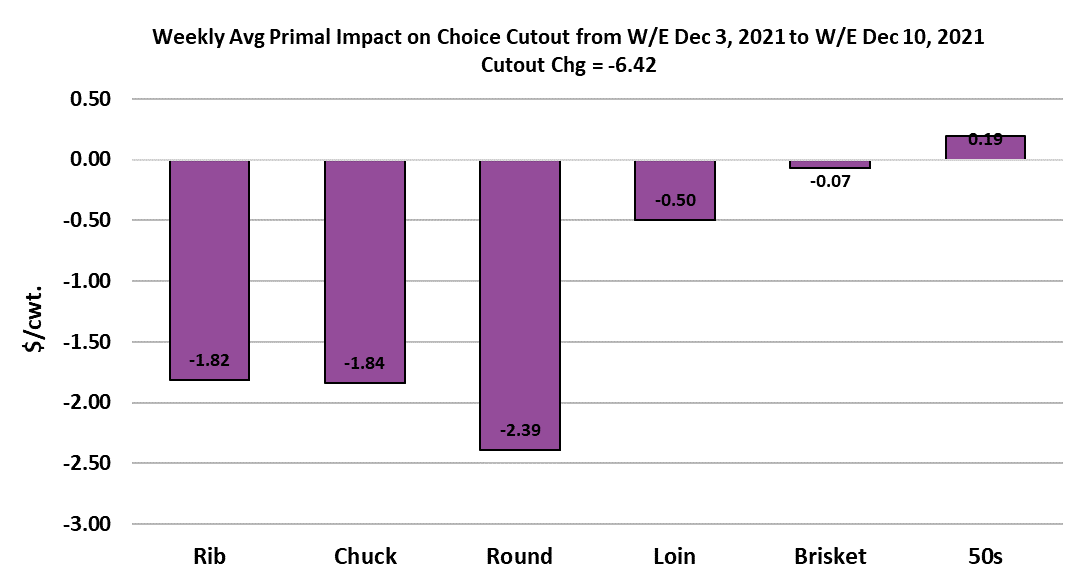

last week’s average. Beef markets remained under pressure, with

the Choice cutout dropping $6.42 on a weekly average basis and the

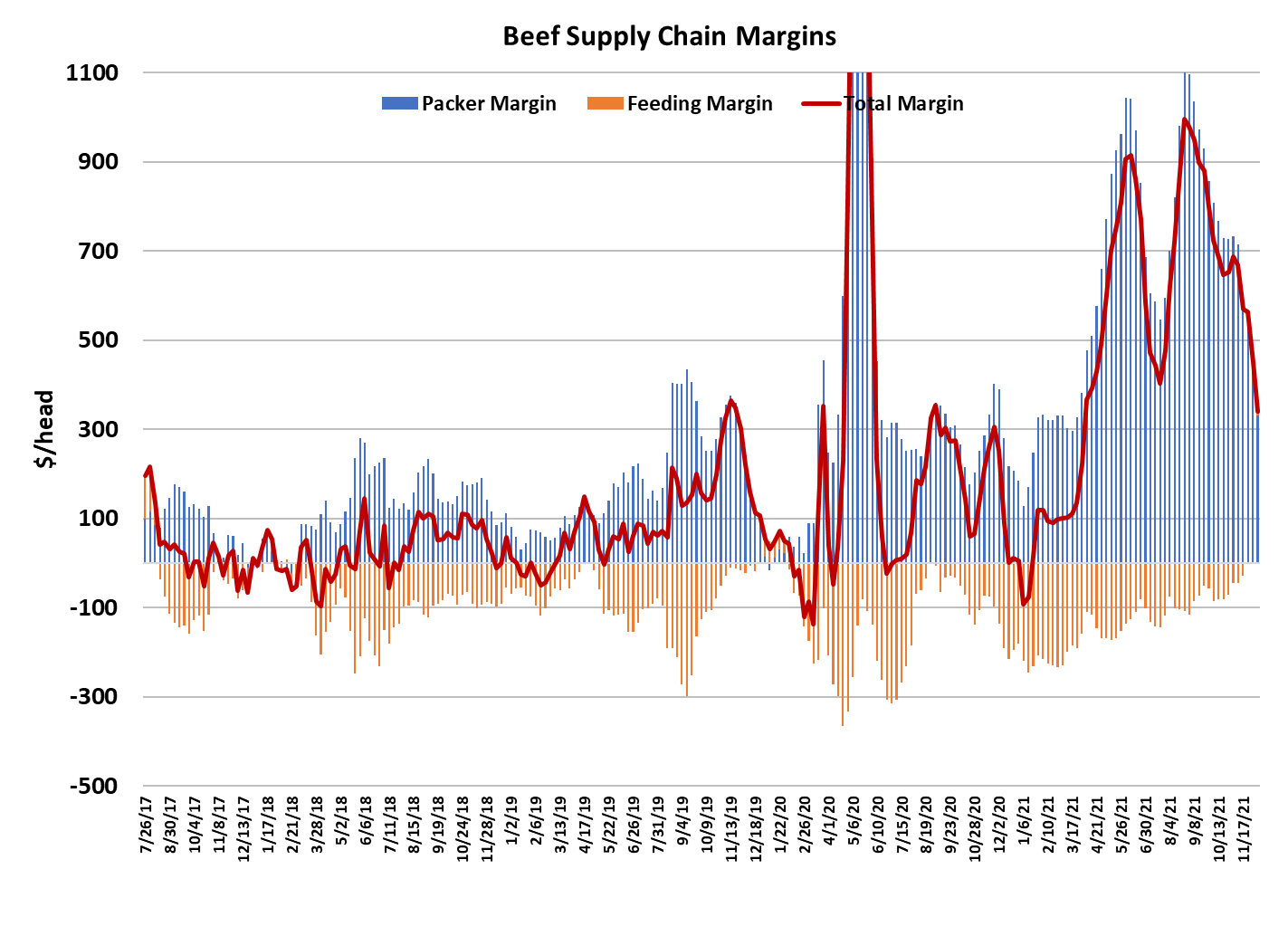

Select down $5.33. Packer margins compressed further, losing

almost $100/head to average $330 for the week. Packers will be

killing cattle next week that were a little bit cheaper, but I think that

the cutouts have further downside risk and thus I’d have packer

margins shrinking to about $255/head next week. The last time

packer margins were that small was in January of this year.

The shrinking of packer margins was the last piece in “normalizing”

this market after a series of catastrophes that started with the Finney

County plant fire back in August of 2019.

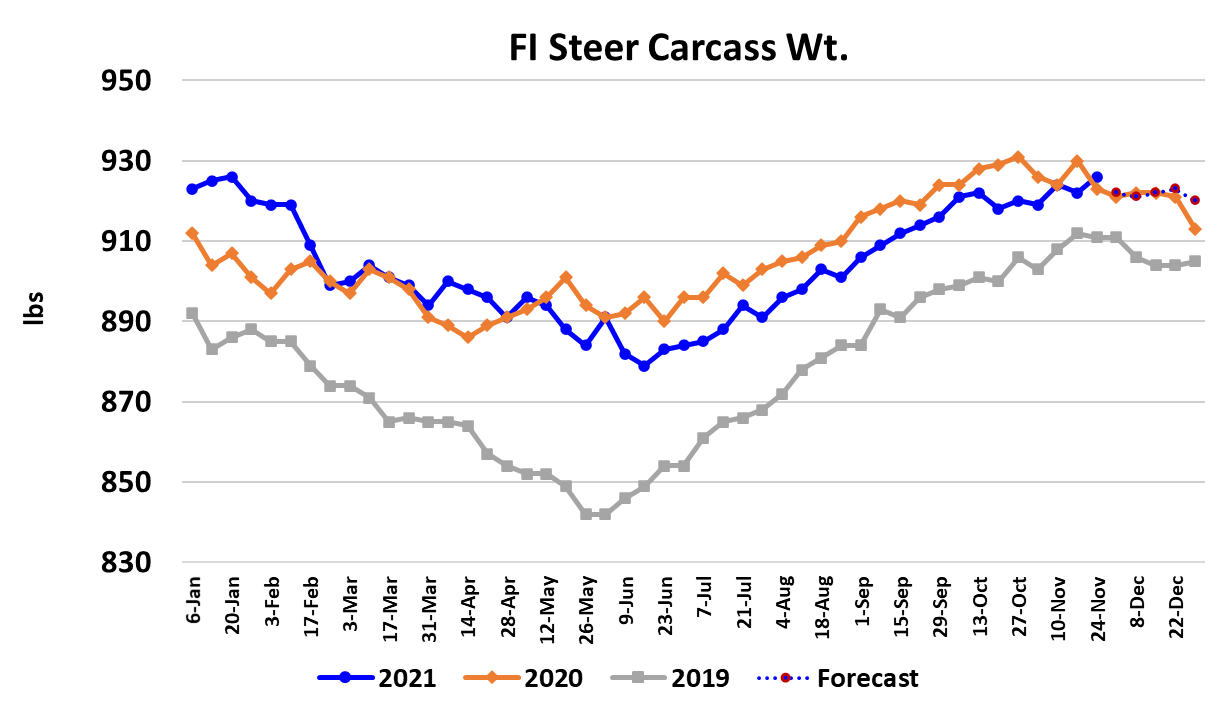

Packers are probably not happy about being weaned off of the margin teat here in the last month of the year and I’d expect them to start resisting higher cattle prices with more vigor. The ease with which cash cattle prices rose from $125 to $140 in just a matter of weeks has left cattle feeders feeling pretty invincible and they will probably resist lower cattle prices pretty vigorously also. The problem for cattle feeders is that they are now coming out of the hole created by light placements in early summer and the tightness in market-ready supplies should be easing. There are also two holiday weeks on the horizon where packers will need fewer cattle. Further, the weather in cattle feeding country has been very good and cattle are performing very well. Carcass weights are still rising, as verified by this week’s FI data which showed steer weights up four pounds for the week of Thanksgiving. So, cattle feeders might dig their heels in and refuse to move cattle at lower prices in the coming weeks, but that would just set up a bigger problem down the road. Now, if the cutouts were to suddenly jump higher then packers would have more room to continue paying $140 for cash cattle, but I really don’t foresee a strong move up in beef prices as we move closer to the holidays.

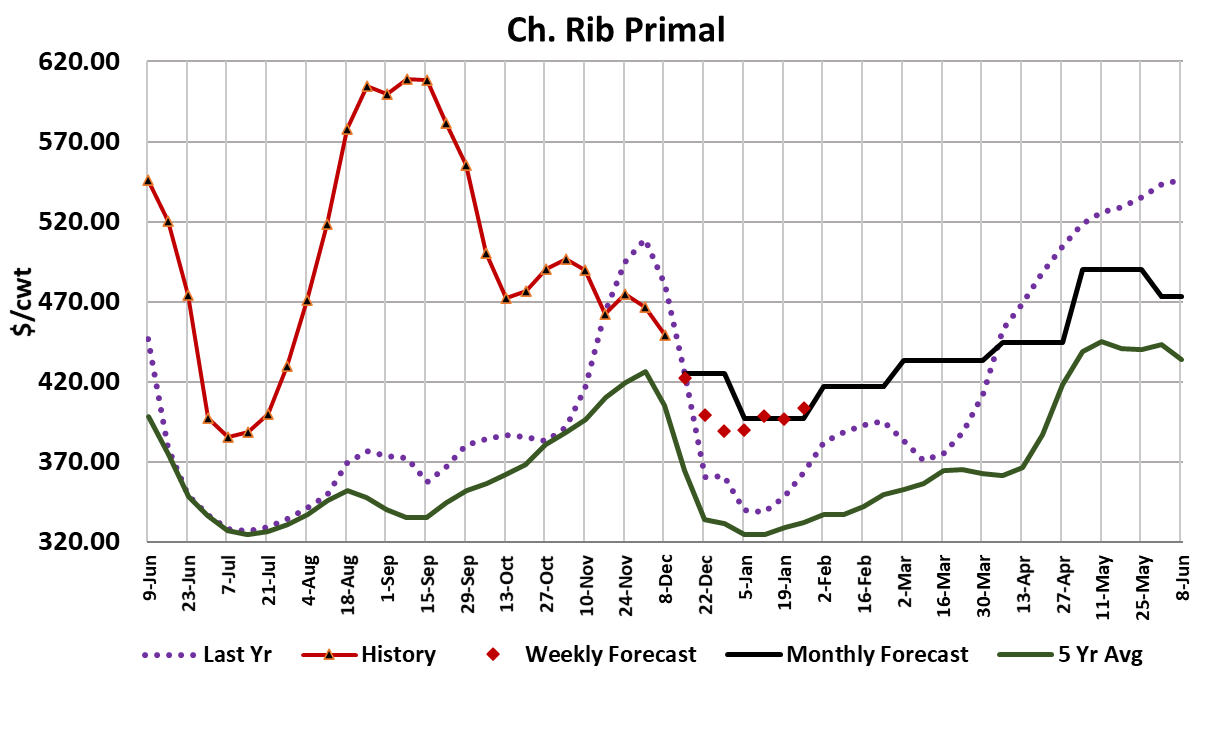

With all of the logistics delays that are part of our new reality, any

buyer that has last minute Christmas needs probably only has a few

more days to make those purchases. After that, middle meat

values will likely start to move lower rapidly and it will be difficult for

the other parts of the carcass to keep the cutouts from sliding lower.

The chart below indicates that it was the ribs, chucks and rounds that

applied most of the pressure to the cutout this week. All of those

are forecast lower again next week.

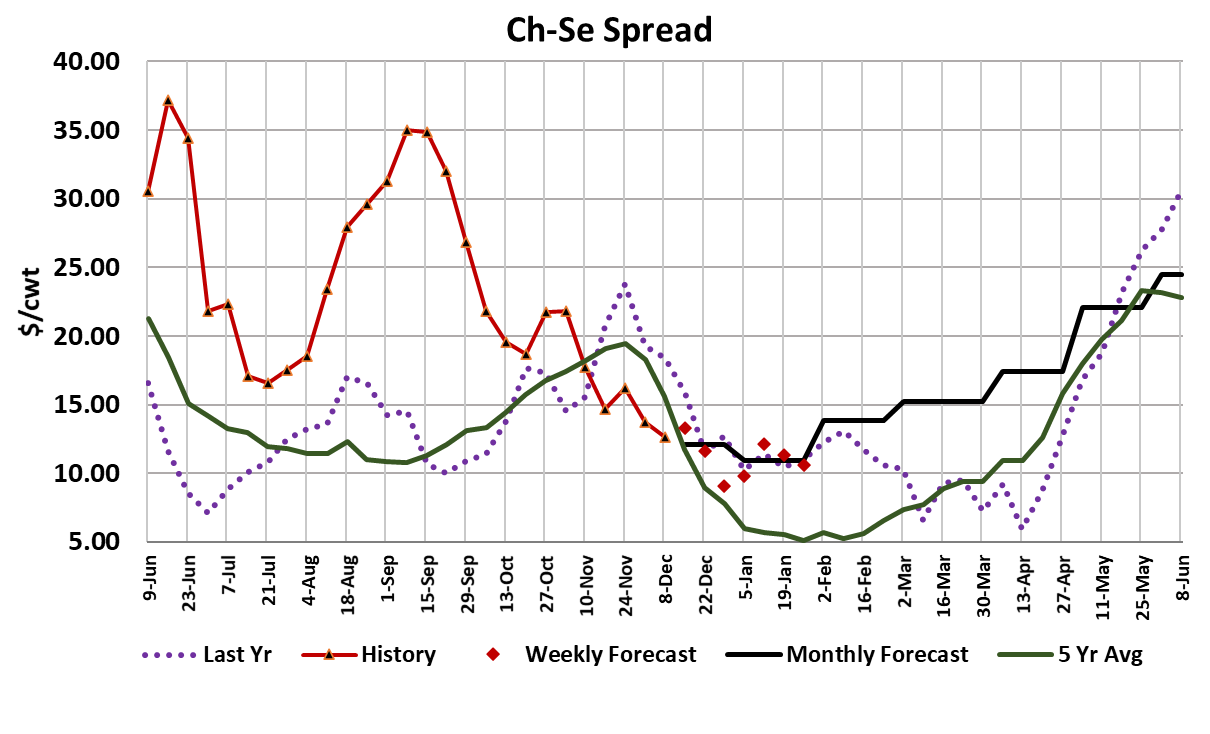

50s have been one of the bright spots, trading over $100 for the past

few days, but there is a strong tendency for 50s to move lower into

year’s end. The downside in the end meats should be limited by the

high price of lean trim. The 90s market has consistently traded in the

mid-$270s since June. If these chuck and round cuts keep losing

value, at some point they will get bought up for grinding. The

fundamental forecast has the Choice cutout down around $250 by

year’s end. It makes sense then, that cash cattle should decline a

few dollars if the cutouts are going to keep moving lower. I see cash

cattle back to perhaps $135 in mid-January, if not sooner. January

and February are normally poor demand months and I’d expect that

to be the case again this year. Consumers are going to party hard

this holiday season after being confined last year during the

holidays due to COVID.

Still, we should see some uptick in the cutouts during January as

cold weather spurs demand for the end meats. It is pretty clear

from the price action over the past couple of months that domestic

beef demand is slowly fading. International demand also seems to

be down somewhat, but is way better than it was last year at this

time. The market needs that strength in export demand to carry

into Q1 to help offset slowing domestic demand and I think it will get

it. USDA released the official export totals for October this week

and it showed a 9% YOY increase. The forecast has November and

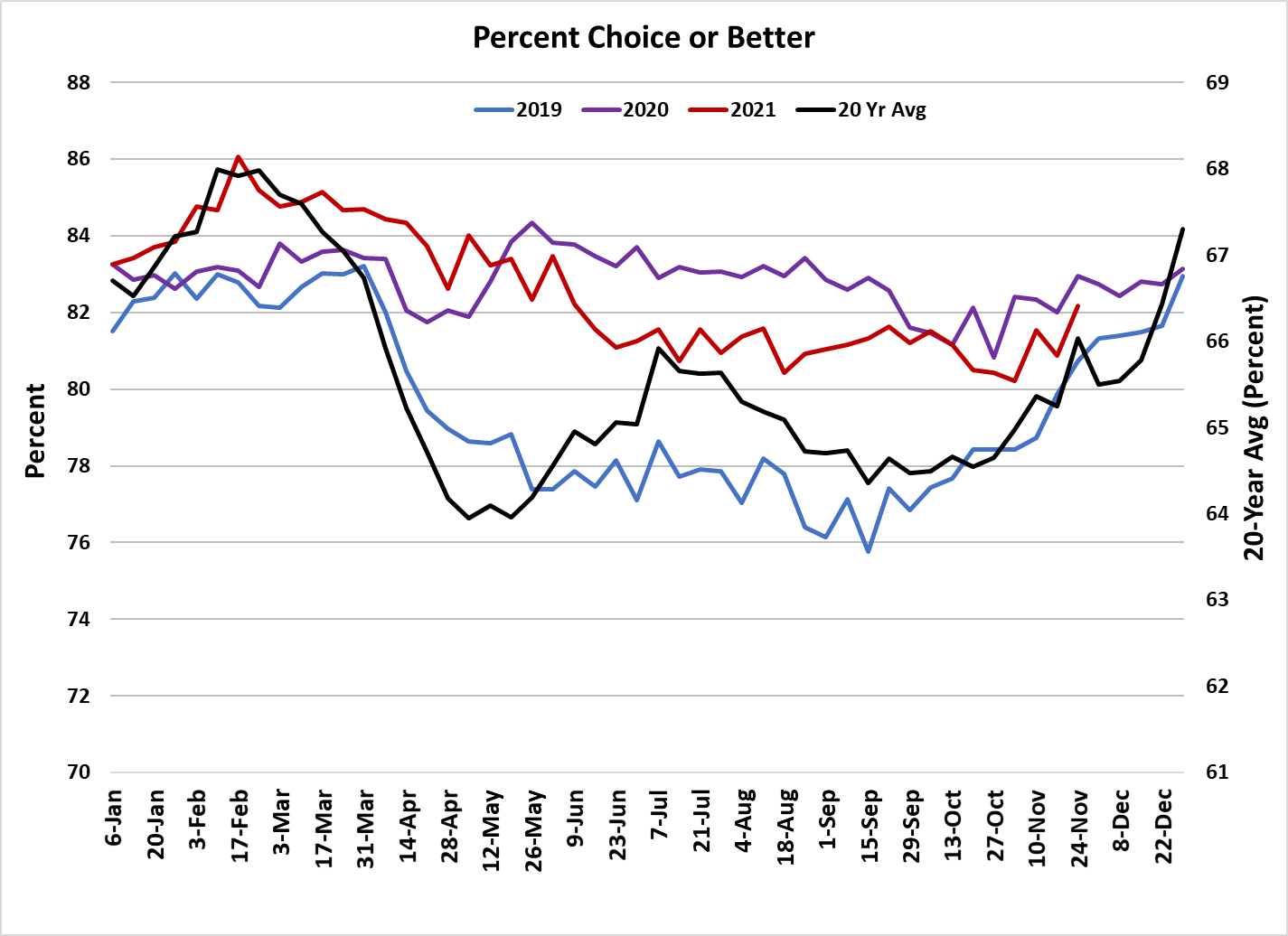

December up a similar amount. Grading has improved recently,

with the Choice or better percentage now over 82% and

approaching last year’s strong level. Holiday kill reductions help to

add fat to animals and that normally drives the Choice or better

numbers higher in December and January. The Choice-Select

spread is reflecting the improvement in grading, this week at $12.64,

down from almost $35 this summer.

This week’s fed kill came in at 516k, down about 10k from last

week’s total. Cow and bull slaughter registered 152k—the largest

non-fed kill since 2012 when the industry was liquidating rapidly and

corn prices were over $7/bushel. I expect next week’s steer and

heifer slaughter to be a little bigger than this week as packers try to

get a little ahead before the holiday weeks. After the holidays, I see

packers trying to shrink the fed kill a bit in order to better align the

beef supply with seasonally weaker demand. Next week, watch for

the ribs to roll over, cattle feeders to dig in, and packer frustration to

mount.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}