Beef Wrap December 17

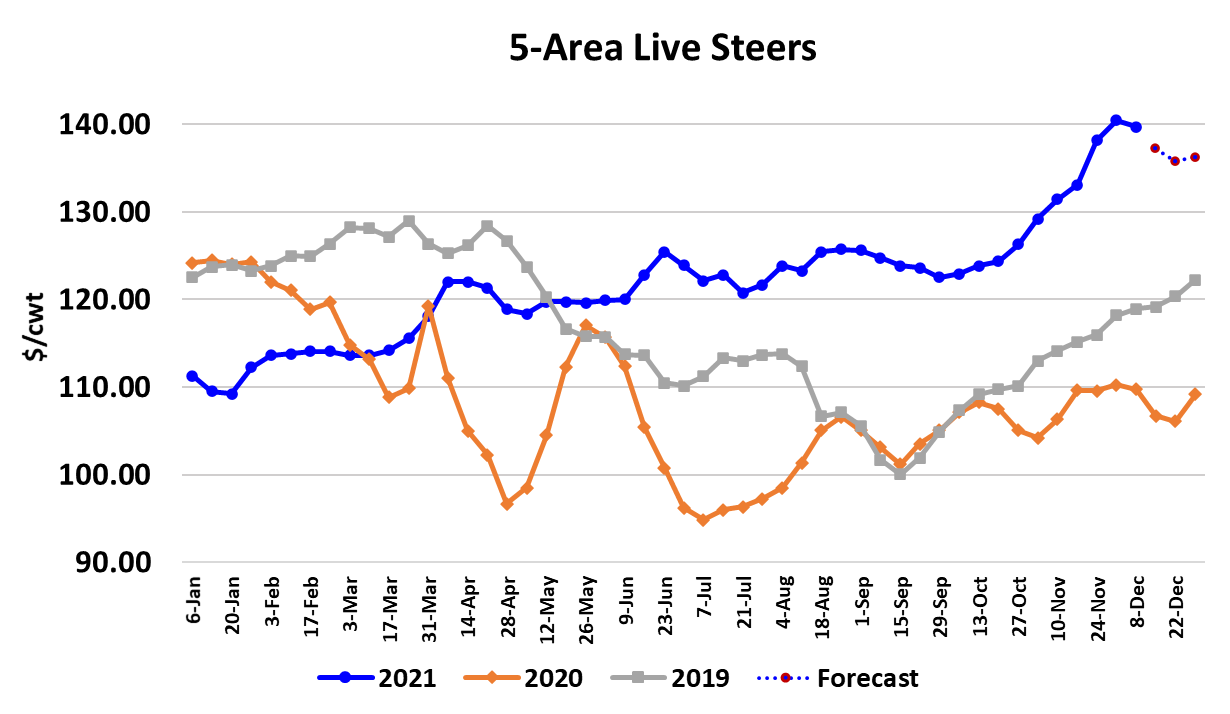

The cash cattle market continued on its lower trajectory this week,

down a little over $2 to average $137.18. Packers appear to have

bought less cattle this week than last and only about half as many as

they bought during the week following Thanksgiving when prices

peaked at $140.50. The beef market also continued its march lower

with both cutouts losing about $5/cwt on a weekly average basis.

Toward the end of the week packers were bidding $136, but cattle

feeders seemed to lose interest in trading at that level, preferring

instead to carry cattle over into next week. I wouldn’t expect packer

interest to be any stronger next week than it was this week, given the

upcoming holiday-shortened kills. Further, it looks to me like cattle

feeders might be making a serious error by not moving as many cattle

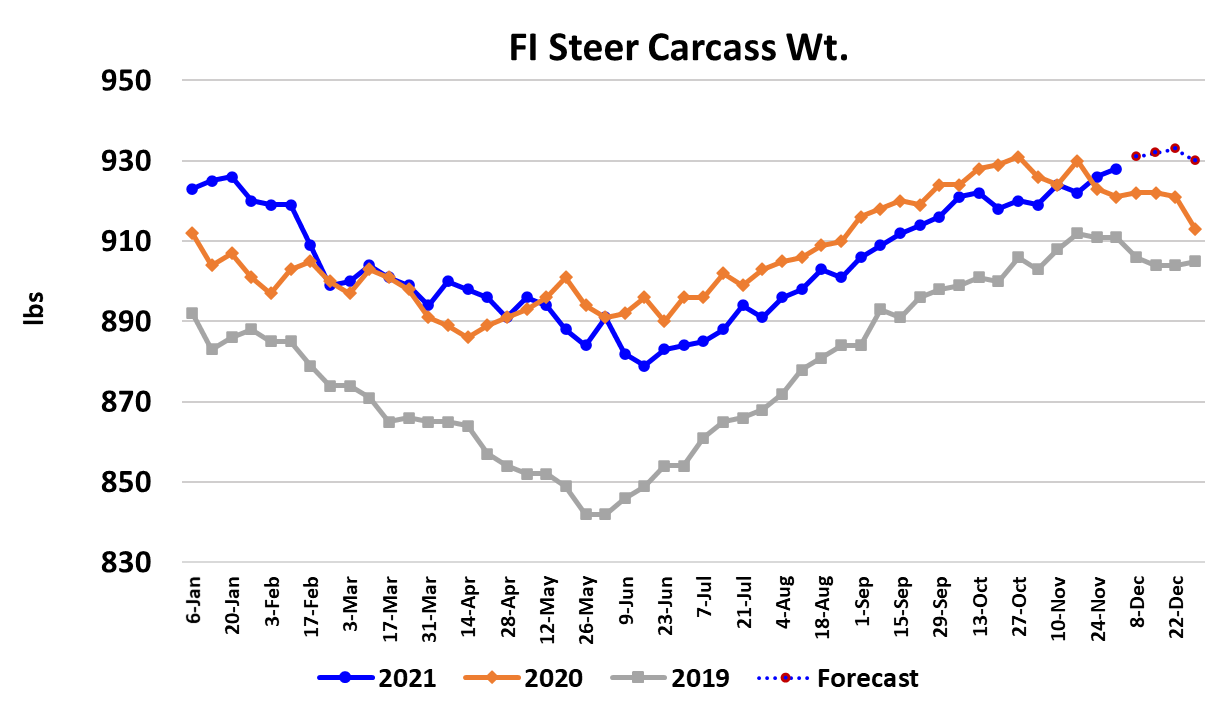

as they can right away. Steer carcass weights were reported up 2

pounds this week and the preliminary data is pointing toward another

2-3 pound increase next week.

Mild weather across much of the US over the last couple of months

has fostered an environment where cattle gained weight rapidly. The

chart below indicates that steer weights are now above last year.

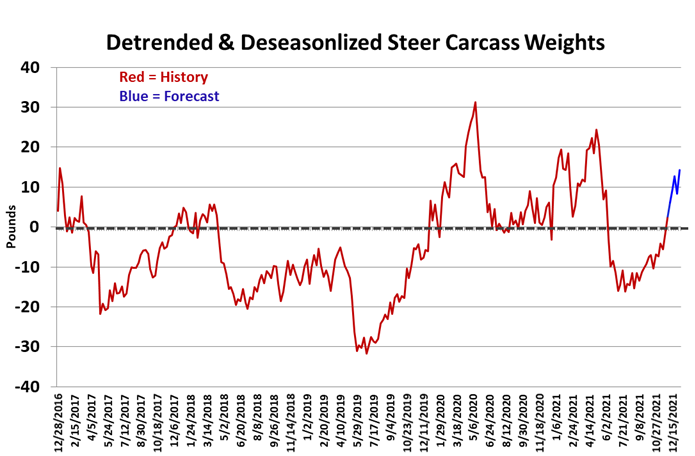

The de-trended and de-seasonalized carcass weights took a huge

jump this week and are now above the zero line and projected to

move even higher in coming weeks. For me, that is a flashing red

light that signals a shift in leverage back in the packer’s favor and I

don’t think he will hesitate to use it in order to push cattle prices lower

over the next few weeks. By limiting the number of cattle they sold

this week, cattle feeders could be setting themselves up for an even

bigger loss of currentness down the road. This week’s fed slaughter

tallied 508k, down about 10k from the week before and suggests that

the sense of urgency to kill cattle that packers were displaying in

November is no longer a factor. Next week, look for packers to do no

Saturday kill and a very small Friday. The fed kill may fail to reach

400k.

The same pattern will repeat in the week leading up to New Year’s,

but the Friday kill will likely be larger than during Christmas week and

thus the fed kill could be closer to 435k. While these small holiday

kills are taking place cattle will be enjoying warm weather in the Plains

states and continuing to pack on the pounds. There seems to be a

feeling among cattle feeders that the market might take a breather

through the holidays but then it will rally again in January. I’m not so

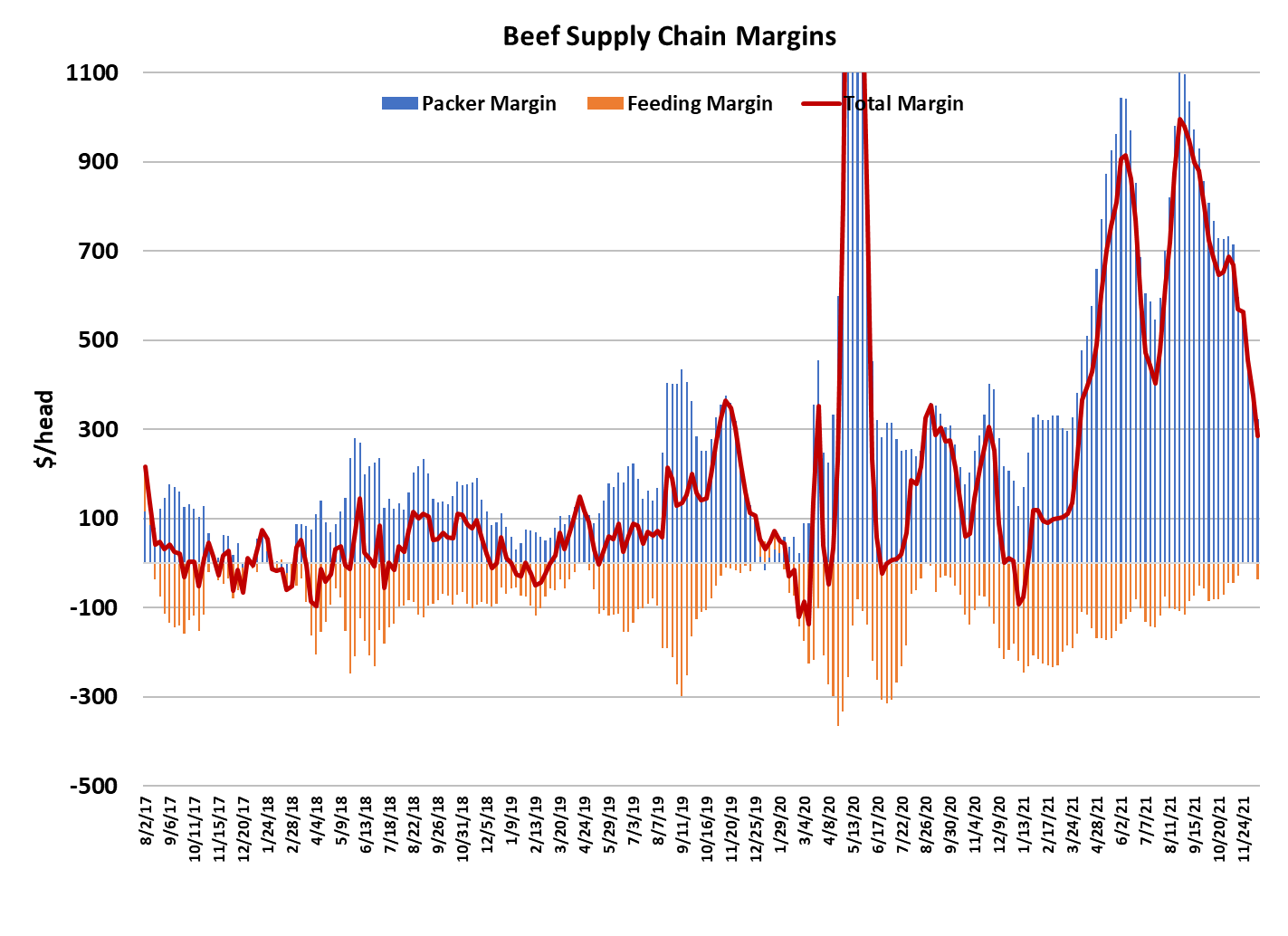

sure about that. A lot will depend on how much margin packers have

to work with. Margins this week were around $325/head, down $28/

head from the week before. An even bigger decline is projected next

week and that will leave packers in little mood to be generous. One

might think that the small holiday kills would boost beef prices, but

beef buyers are also on holiday and thus the need is less. It is

common for the cutouts to be steady-softer in the last two weeks of

December.

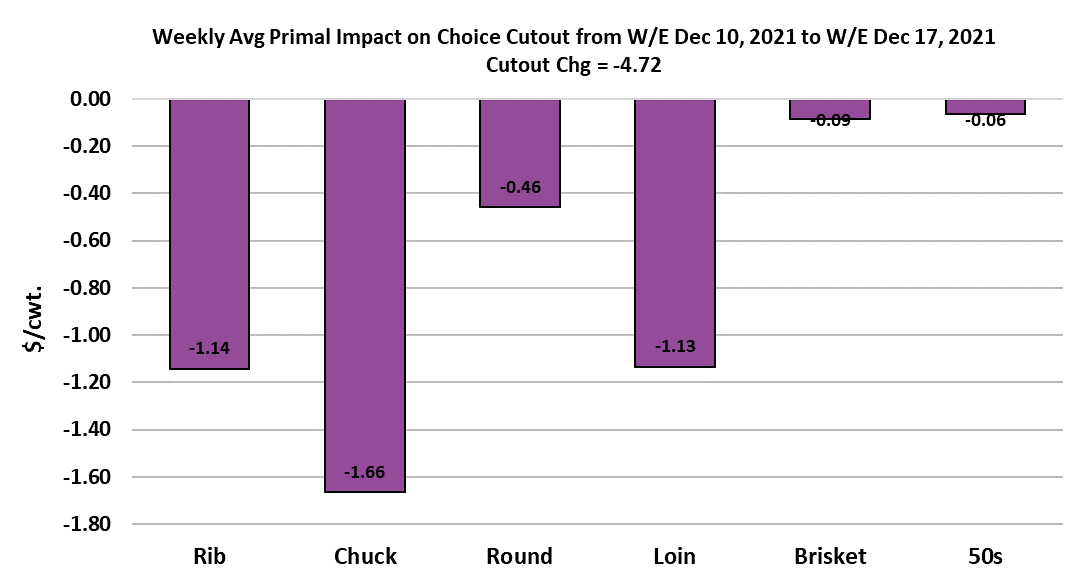

This week, once again, it was everything except briskets and 50s

pushing the cutout lower. The fundamental forecast has the Choice

cutout finishing the year in the $250-255 range. Ribs have declined a

bit less than I expected, but the damage is not fully complete there

just yet. End meats look to only have a little more downside risk and

should turn decidedly higher in January. Retailers tend to focus on

featuring the lower-value end cuts and grinds during January

because they realize that consumers will be burdened with holiday

bills. This year however, consumers appear to be in a better

financial position as a result of all the stimulus money that rained

down on them in 2021. Steak cutters normally watch middle meat

prices closely for a bottom in early January and then they swoop in

and buy product to prepare for spring. It seems to me that domestic

beef demand is continuing to leak lower, but international demand

remains very good.

Of course, the wild card is the omicron variant and if it causes

consumers to move back into stay-at-home mode and thus stockpile

meat again. Along those lines, omicron is also a concern for packing

plant workers since it seems to evade the vaccines readily. It may

not be as life-threatening as other variants, but it is more virulent and

thus could spread rapidly through packing plants causing high

absenteeism and even possibly causing some plants to close

temporarily for lack of labor. We have all seen that movie before—it

causes beef prices to rocket higher and cattle prices to tank. So far,

there hasn’t been much evidence of buyers stockpiling beef as a

hedge against such an event, but the potential is real and should be

on every buyer’s radar. For now though, the combined packer

+feeder margin continues to move lower and thus points to softening

demand. The turn higher might not come until mid-January unless

omicron causes problems that panic both beef buyers and

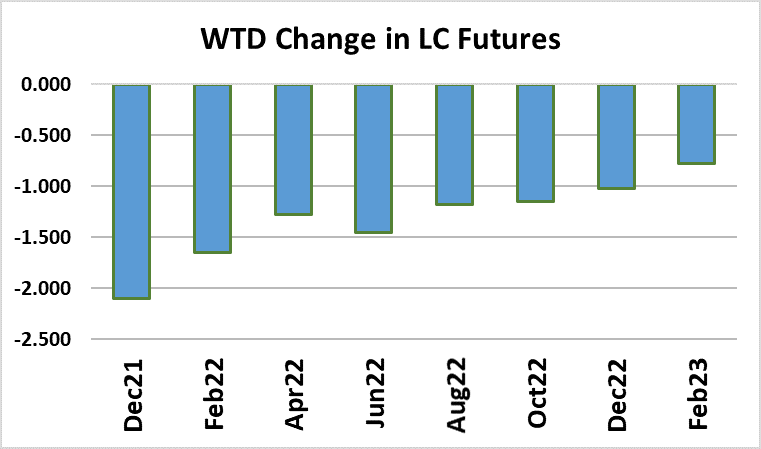

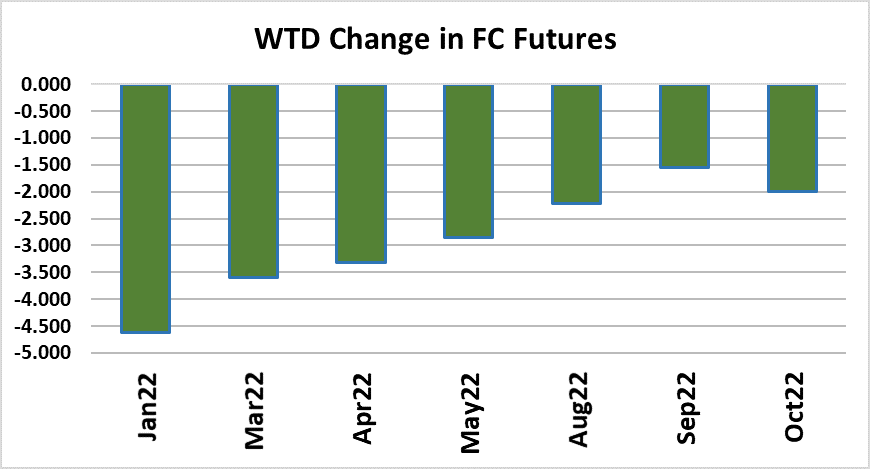

consumers. Futures traders are already beginning to sense the loss

of leverage by cattle feeders and the curve was down $1-2/cwt this

week.

If they start to believe that COVID is going to become a problem in

packing plants again, the downward reaction in the futures will be

swift. Next Thursday, USDA will issue a Cattle on Feed report. I’m

projecting it will show November placements up 7.3% and on-feed

inventories as of Dec 1 to be up 0.2% YOY. Futures traders would

likely view a placement number that large as negative to the spring

and summer contracts. Next week, watch for further weakness in

both the cattle and beef markets on light volume as market

participants begin to focus more on the reason for the season and

less on the typical course of business.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}