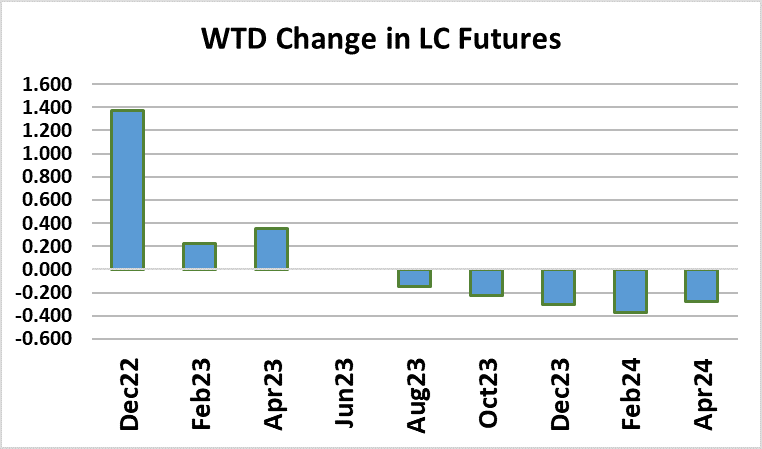

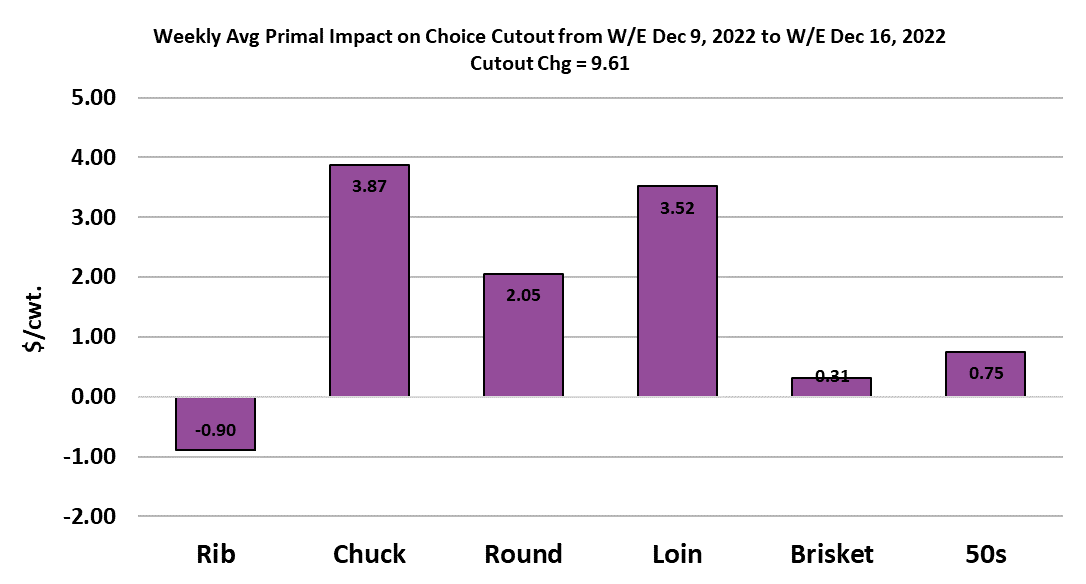

Beef Wrap December 16

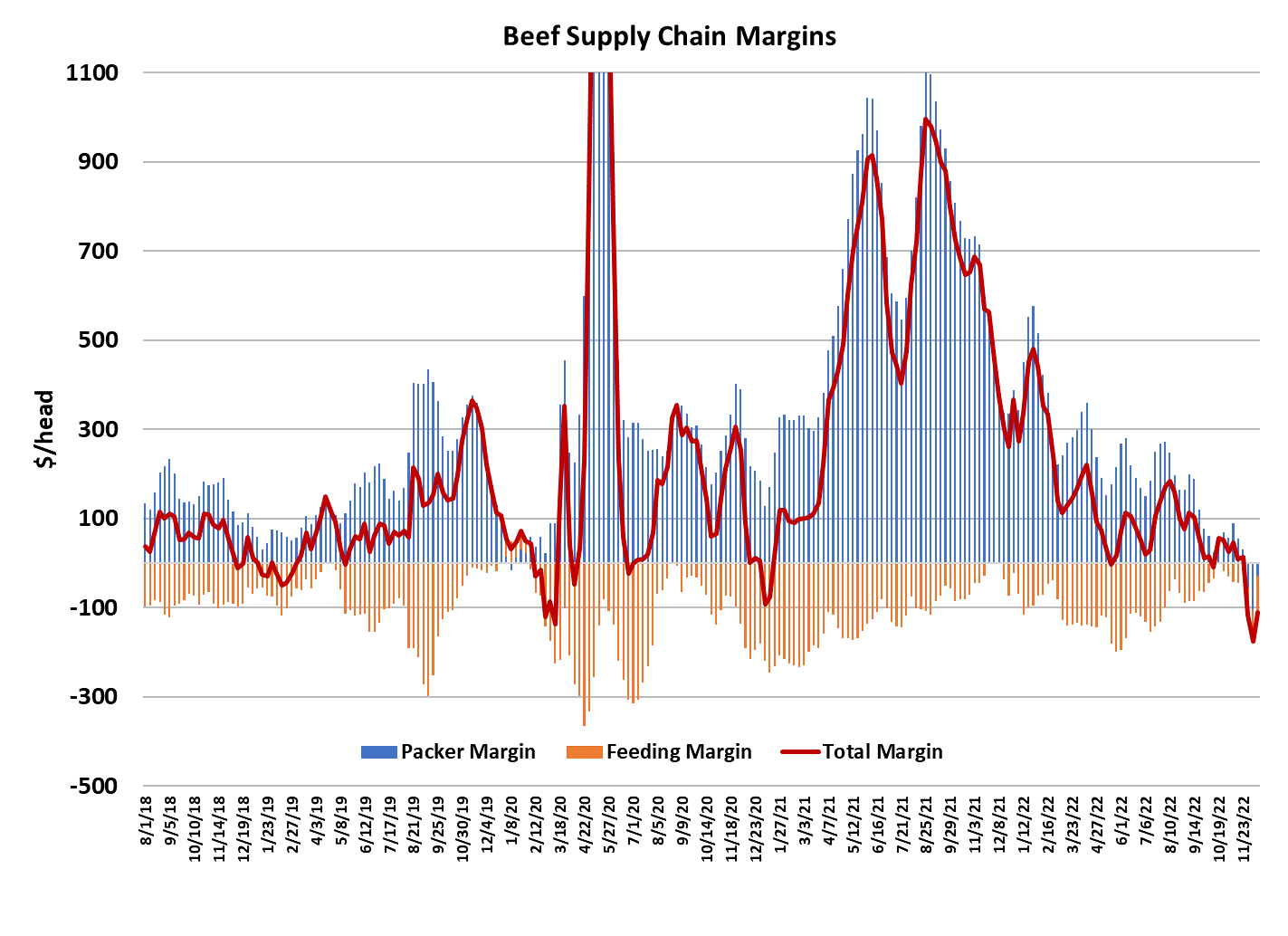

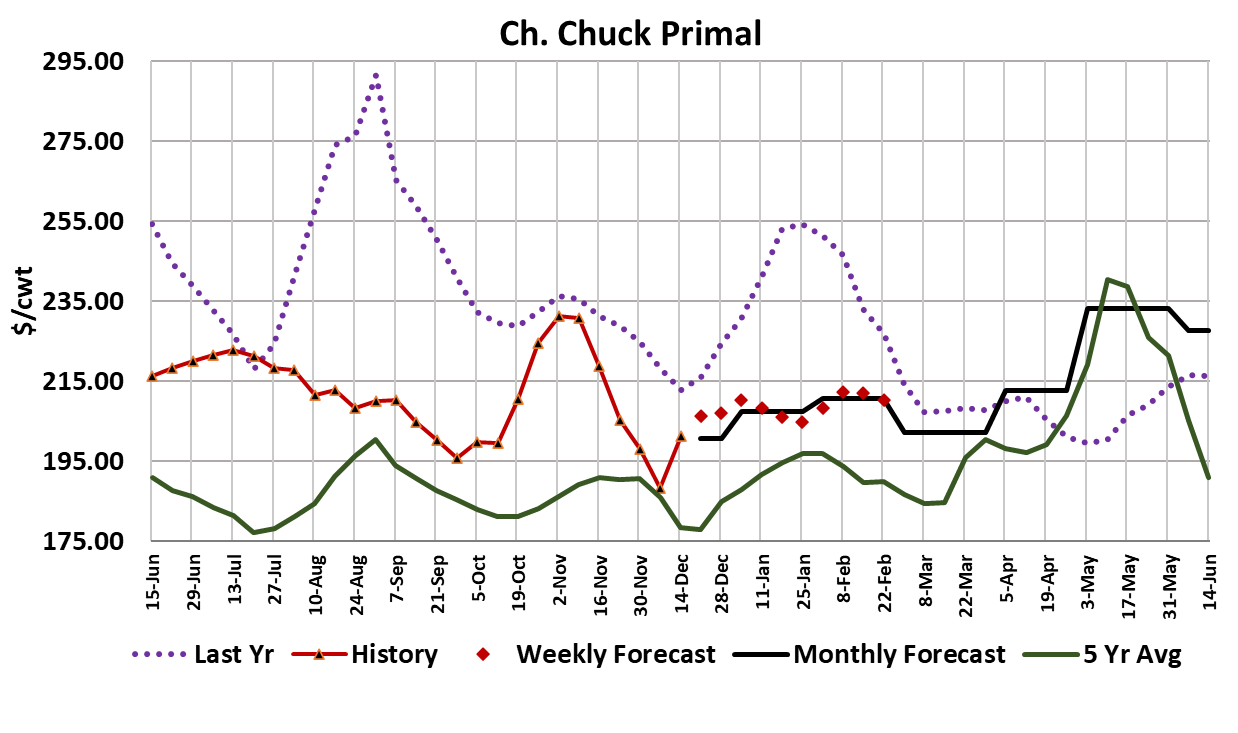

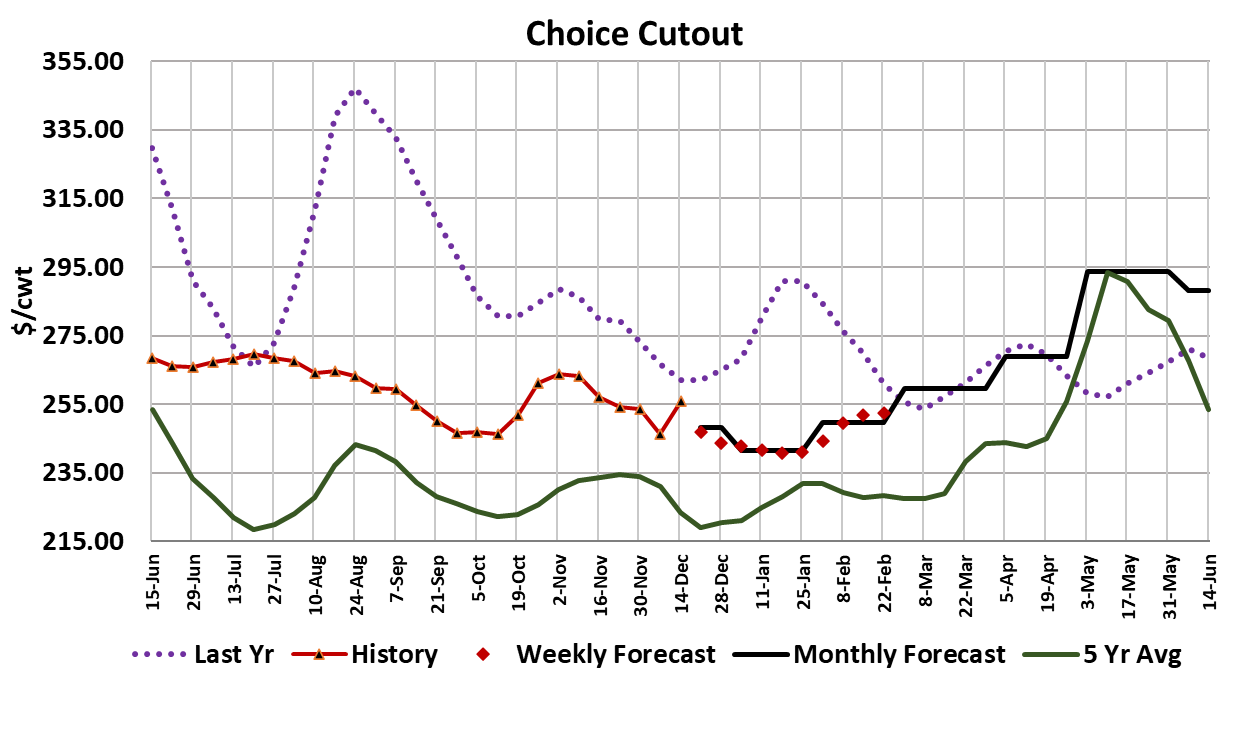

The beef market was volatile this week as buyers wrapped up last minute purchasing ahead of the holidays. The rib primal traded in an almost $100/cwt. range from $457 on the low side to $546 on the high side. That was to be expected as buyers with immediate ship needs moved in and out of the market, but what wasn’t expected was a sharp surge in end meat pricing. The chuck primal alone added almost $13/cwt. on a weekly average basis and the round primal was up a little over $8/cwt. It is hard to call that last minute holiday buying because the end cuts generally are not “must haves” during the holiday season. It is more likely that it was buyers positioning themselves for early January features that will focus on the end cuts. Because the end meat market has been trending lower since early November, there could have been some buyers that waited as long as they could to do their early January shopping and were caught in a bad spot as packers have reduced production in the last couple of weeks. When it was all said and done, the Choice cutout added $9.61/cwt. on a weekly average basis and the Select was up $7.99/cwt. Of course, the next question is “Will it last?” I think that the cutouts are more likely to decline next week than to keep moving higher, simply because the drag of falling middle meat prices should more than outweigh any additional increases in the end cuts. The rib primal only averaged about $8/cwt. lower this week and that doesn’t even come close to the normal seasonal break that is typical for ribs. That is likely to be the main feature in the market next week. I think we can expect about a $5-7/cwt. drop in the blended cutout next week and then maybe a couple more dollars down the following week. Most of the middle meat damage should be done by the first week in January, so then we might start to see some upward pressure on the cutouts. This week’s surge in the cutout did help packer margins considerably and now they are only about $15/head underwater. Packers managed to get cash cattle bought this week at prices that averaged very close to the week before ($155.60). The sharp reversal in packer profitability also helped the combined margin which has now turned decidedly higher. It was probably due for an upturn after trending lower through most of the fall, but I suspect that it will do some stutter-stepping over the next few weeks as we move through the holidays and then resume its uptrend in January.

It was another week of limited price changes in the cash hog and pork markets. The WCB negotiated market dropped $1.44/cwt. on a weekly average basis and the NDD market was down $1.35. The cutout managed to eek out a $0.20/cwt. gain. Dec LH futures expired on Wednesday and were cash-settled to the LHI at $81.88/cwt. That expiration didn’t happen without some drama however as someone paid $184/cwt. for about ten loads of 13/17 lb. bellies on Tuesday morning and that jacked Tuesday’s cutout up to $91. On Tuesday afternoon, the 13/17 bellies were back to trading $100/cwt., where they have been for the better part of the last two weeks. The timing was very curious given the futures expiration on the following day. Outside of that little bit of excitement, it was mostly a bland week in the hog and pork complex. The Feb futures did post a huge rally of more than $4/cwt. on Friday, but a surge in the next nearby isn’t all that unusual following an expiration. It looks like the LHI will print $80.50/cwt. early next week, so the Feb futures at near $86 is pointing to about a $6/cwt. increase in the LHI over the next eight weeks. That is entirely do-able and $86 is not too far off of my estimate of fair value for Feb. However, the market might have to navigate further softness in both the hog and pork markets before those gains take hold. The biggest risk at the moment is posed by the ham primal, which was down a little over $3 this week and could easily shed another $10 between now and the end of the year. The belly primal only gained $1.81/cwt. this week, even with the help of that abnormally high belly trade on Tuesday. Bellies are likely to stay soft for another couple of weeks before gaining some upward traction in January. So, with bellies sideways and hams potentially dropping hard in the near-term, we could see the cutout push down into the lower $80s to finish up the year. The LHI is likely to go with the cutout and could print in the high $70s for a few weeks unless packer margins narrow even more. This week’s packer margin was close to $10/head, up about $1.80 from the week before, but still way below what is considered normal at this time of year. It’s the same old problem of too much capacity chasing too few hogs and I don’t expect that to change in Q1, so I’ve kept my packer margin forecast unusually tight heading into next year. Actually, there is good reason to believe that the hog supply situation will only get tighter next year and so packer margins could be well below normal for all of 2023. Right now, I have packer margins forecast to average only about $9/head in 2023, down from $10 this year and $21 in 2021. Next Friday, USDA will release it’s next installment of the Hogs and Pigs report and I’m expecting it to show the hog herd down 1.4% YOY and the breeding herd down 0.2%. I’m looking for the Sep/Nov pig crop to be down 1% YOY. I haven’t seen the consensus estimates yet, but it is quite probable that those will be smaller than what I have dialed in. No one I’ve talked to can find a reason why the hog herd should expand, so if USDA does show any YOY gains on this upcoming report, it would be a real shocker. The reasons to expect further contraction are many: Prop 12 uncertainty, persistent high feed prices, high energy prices, cost of labor increases, China’s exit as a major importer of US pork, etc. The Jun/Aug pig crop, which the industry is currently slaughtering, was reported down 1.1% YOY, so if I’m correct about the Sep/Nov pig crop being down 1% and the breeding herd also being down, that will pretty much guarantee YOY declines in hog slaughter through the first three quarters of next year. I’m looking for per capita pork availability to be down about 1.7% in 2023, but that could be offset by softer demand next year and thus I have the cutout averaging about $98.50 in 2023 compared to a $103.30 average this year. This week’s kill came in at just a hair under 2.6 million head, so packers should have strong inventories heading into the holiday weeks. I see next week’s kill somewhere close to 2.34 million head and the following week we could see the kill drop below 2 million head. I don’t really expect the smaller kills to put much upward pressure on the cutout however. Some of the retail items might see modest gains (loins for example), but if the hams soften as expected that will probably be enough to keep the cutout on a slight downward trajectory until the bellies wake up after New Year’s. Hog carcass weights are still slowly rising in normal seasonal fashion, but don’t really pose much risk to prices in the near term. A very cold blast of winter weather is projected for the Northern Plains next week and that might temporarily pause further weight increases. However, negotiated hog prices are likely to continue to track lower since packers won’t be aggressively seeking extra hogs during the holiday weeks. When we emerge from the holiday period, look for weekly slaughter to bounce back over 2.5 million head per week for most of January. Next week, watch for further slippage in the hams to put some modest downward pressure on the cutout and expect negotiated hog prices to soften further as well.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}