Beef Wrap December 10

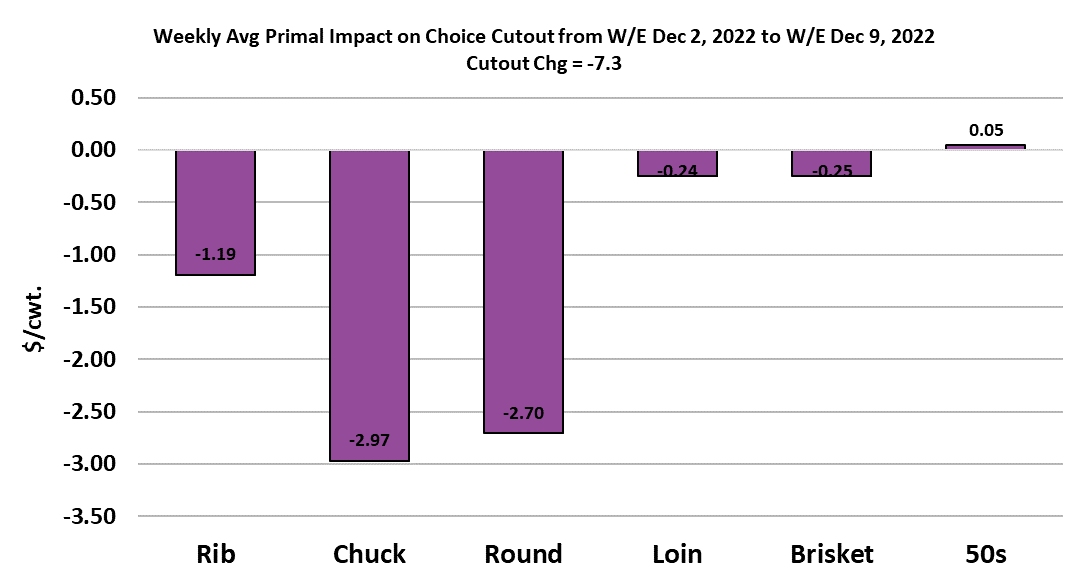

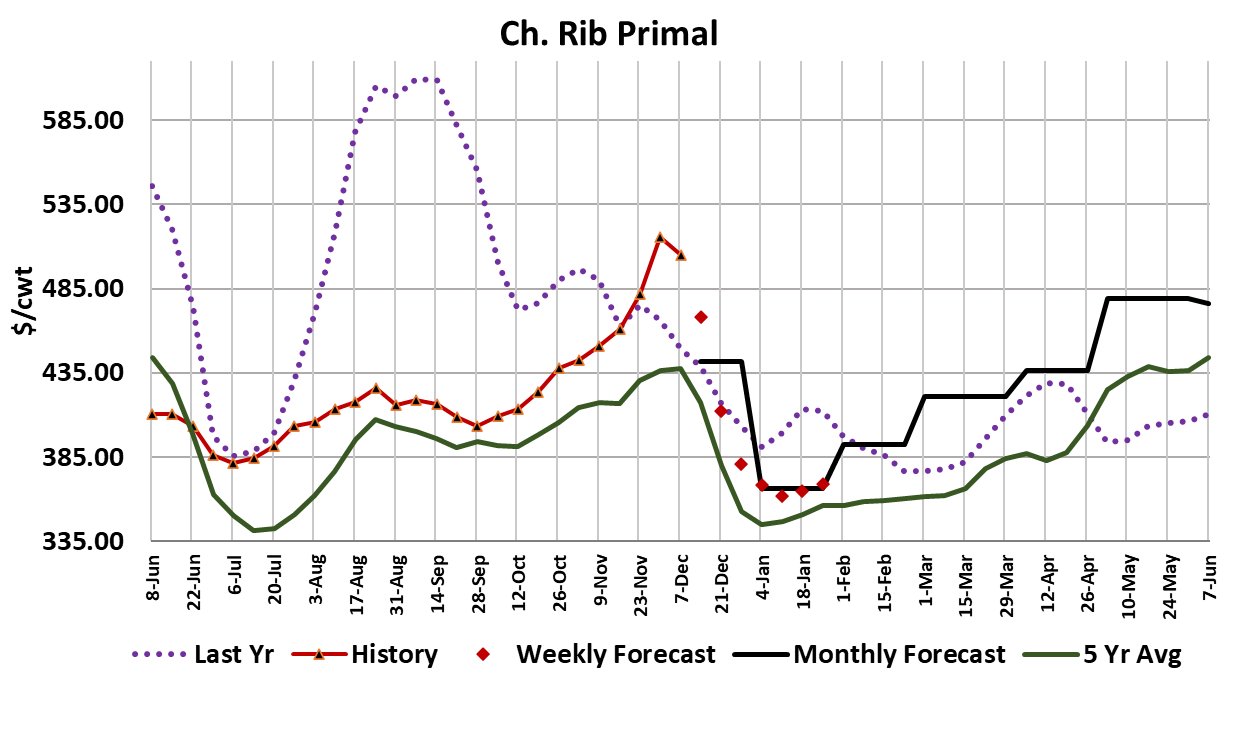

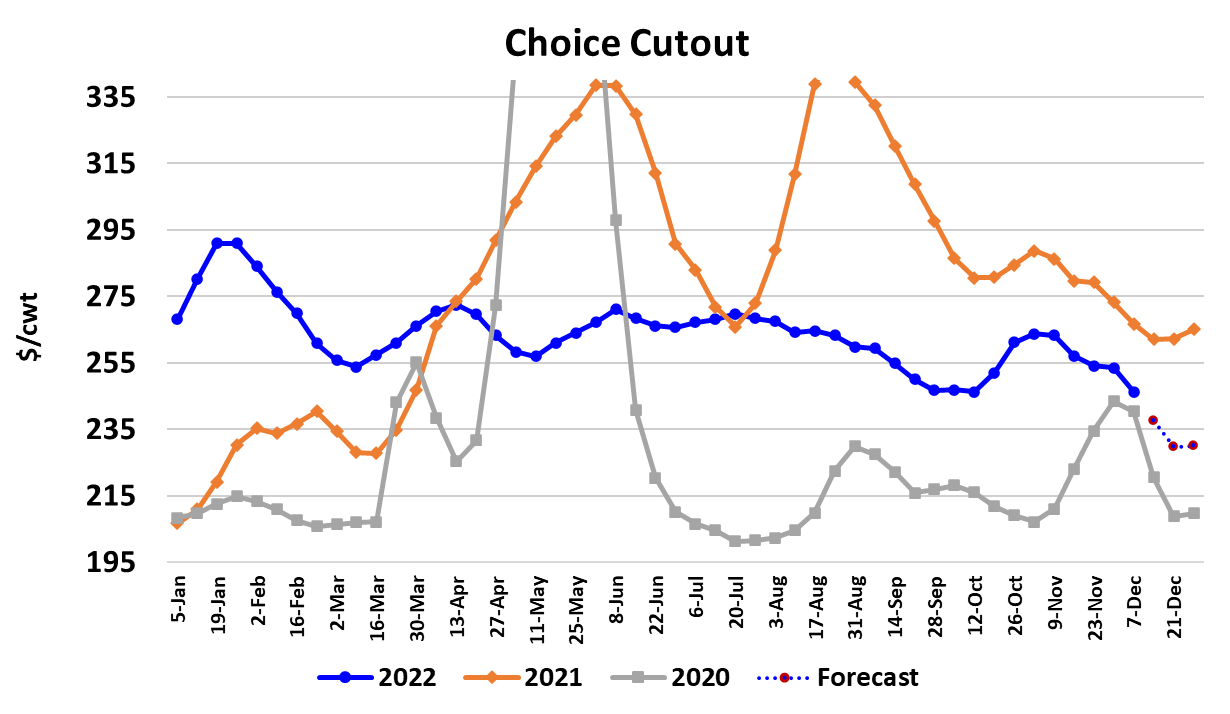

Packers scored a minor victory this week as they were able to purchase cash cattle at about $1 below last week. USDA is reporting the weekly average price near $155.60, but the volume traded was only about half of what they purchase in the negotiated market in a normal week. Obviously, some cattle feeders weren’t interested in taking steady or lower money and those cattle will sit in the yards until next week. Packers can use some formula and contract cattle to try and plug the gap next week, but my guess is that they will need to be back in the market a little earlier than normal. The light volume might also be a signal that they intend on scaling back the kill next week. This week’s fed kill dropped to only 501k, with a very light Saturday kill. The reason: packers are bleeding red ink. I calculate this week’s margin at -$132/head. The last time packer margins were that bad was in April, 2015. Packer margins were pressured by further declines in the cutouts as the Choice lost $7.30/cwt. and the Select was down $5.42/cwt. Those cutout losses happened in a week when the rib primal was only down slightly from the week before. What will happen to the cutout when the rib primal starts dropping $30-40 per week? That could start as early as the middle of next week. The end meats continue to be the biggest drag on the cutout as the attached chart indicates. The chuck primal averaged $188.43/cwt this week and that is very close to where it was in the same week of 2019, prior to the pandemic. Are beef prices going all the way back to pre-pandemic levels? If so, that means we will be looking at a Choice cutout in the $220-225 range soon. That would be a disaster for packers since cattle prices are about $35/cwt. over pre-pandemic levels. To be fair, it isn’t uncommon for packer margins to run for long periods in the red when cattle supplies are the tightest.

Back in 2014-15, packer margins averaged -$64/head over that two year period and there were very few positive margin weeks. But cattle supplies are not nearly as tight as they were in those years. If beef prices are going to reset back to pre-pandemic levels, then it seems there should be some reset in cash cattle prices also. Maybe not all the way back to 2019 levels, but some reset seems in order and it is on the packers to make that happen. It is time for them to cut some shifts and let some of those newly-hired workers go. That will lower cattle prices and raise beef prices. Or, maybe they will need to run deep red margins for several months before they finally take that action. At least this week’s slaughter makes it look like they are trying to dial back the kill some.

Part of the difficulty in reducing cash cattle prices is that cattle feeders have signed up for some very high breakevens by paying exorbitant prices for feeder cattle. The breakeven on cattle leaving the yards today is around $160/cwt., so cattle feeders are still losing money at this week’s $155 cash price. Even worse, that breakeven will escalate to near $170 within a few weeks. You can see why cattle feeders don’t want to take lower money.

The basic problem here is that input costs have risen tremendously over the past couple of years and now that consumer demand has fallen back to pre-pandemic levels, there isn’t enough margin in the system for either packers or feeders to make money. Look at the combined margin chart. That tells the story. Another facet to this situation is that retailers are grabbing up most of the margin that is available by keeping retail prices high even though wholesale prices have come way down. Eventually, retailers will start to compete with each other more aggressively and retail prices should come down, but that could take months to play out. In the meantime, we are about to go through the worst demand months of the year in January and February. There is going to be a lot of margin stress placed on both packers and feeders over the next couple of months, I suspect. And what will cattle feeders do if their margins tank further in Q1? They will pressure feeder cattle prices and send some of this margin pain back down to cow-calf producers. That should encourage further liquidation of the breeding herd. So there are some interesting dynamics that will need to play out in the first half of next year. The beef supply chain is not well balanced at the moment and some corrective action is needed.

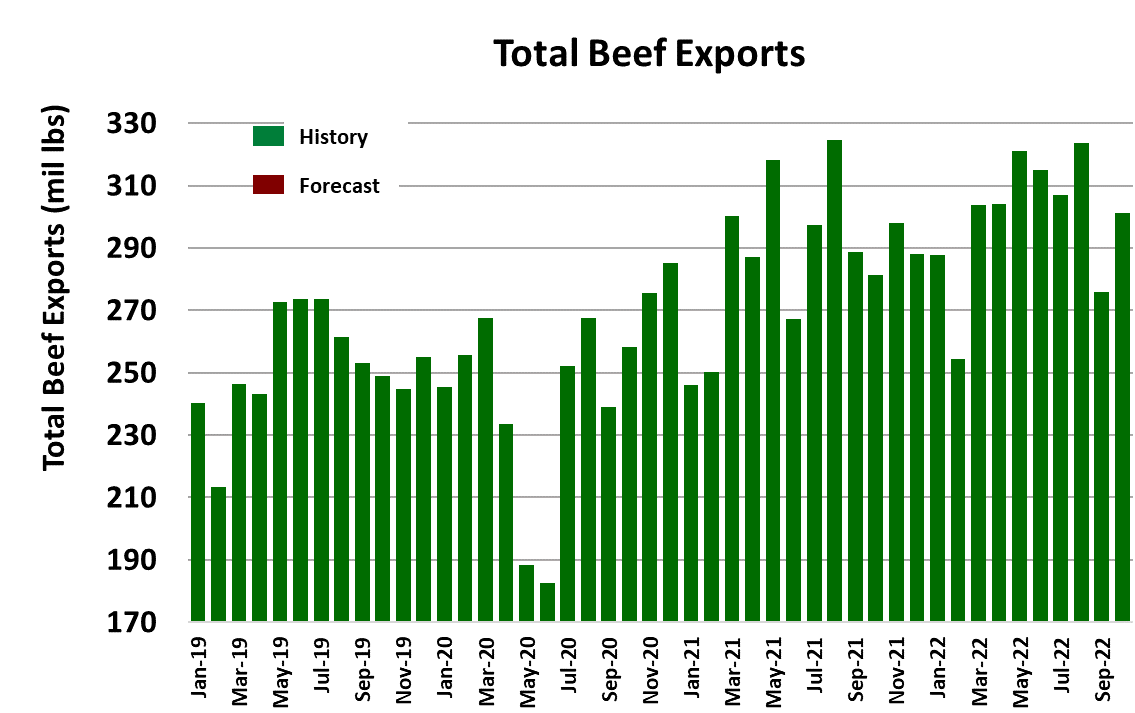

By the way, beef isn’t the only protein that faces this problem. Pork and poultry are also seeing the same thing. This week ERS provided the trade data for the month of October and that indicated beef exports were up 7% YOY. Movement to China was 30% higher than a year ago. YTD, China is now the third largest buyer of US beef. Prior to 2021, China hardly bought any beef from the US. So the growth in demand out of China has been instrumental in boosting the value of US beef in the last couple of years. What happens if that goes away, or at least gets tempered? That would be more bad news for beef and it looks as though China is really starting to struggle economically now. Protesters in China are pressing for relaxation of covid restrictions and it seems like the authorities are ready to relent. The result could be a huge wave of covid over a country that doesn’t have near the medical resources that other countries have. If that happens, it’s not likely that consuming US beef will be a high priority for the Chinese. October beef imports were down 11% YOY, so that kept the US as a small net exporter. Next week, the big story is likely to be the collapse of middle meat prices as the holiday business is completed. That should drive the cutouts down hard again. Packer margins are likely to move deeper into the red and the talk of kill reductions will grow louder.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}