Beef Wrap December 23

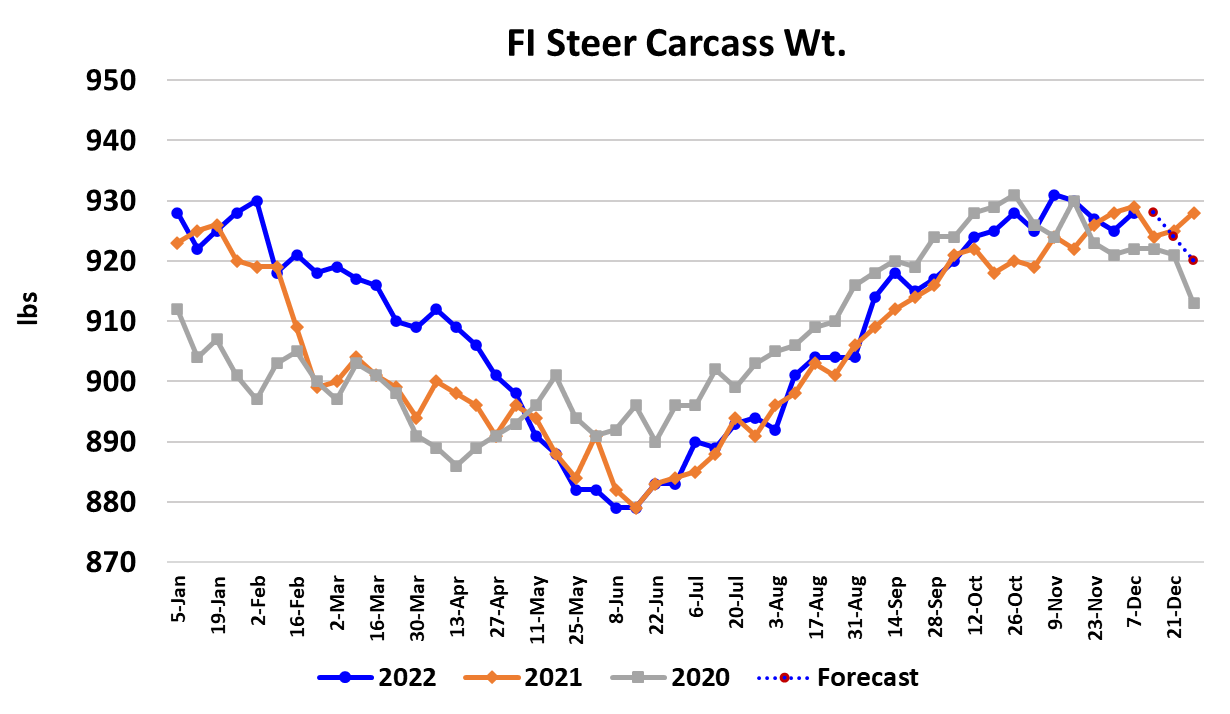

This was a week of disruptions. First, the upcoming Christmas holiday trimmed slaughter schedules and slowed the meat trade. Next, the artic cold penetrated the midsection of the country raising concerns about animals in the feedyards and limiting both buyer and seller interest in moving animals. The end result is that not many cattle were sold, fewer cattle went to slaughter and very light volumes of beef changed hands. For market observers, the main takeaway is that there can’t be many strong takeaways in a week like this. Beef prices shot higher, but that very well could be more a function of surprise shortfall in production than an indicator of strong demand. The Choice and Select cutouts both gained between $10 and $11/cwt. on a weekly average basis. The attached chart on primal contribution to the cutout shows that all of the primals had a hand in lifting the cutout. That is often a sign of a sudden shorting of the market due to smaller-than-expected kills. Of course, packers have been struggling with margin issues for several months and they really needed to cut the kill in order to improve profitability. It was fortuitous for them that the cold snap and the holiday combined in the same week to make that happen in a big way. I calculate that packer margins this week were almost zero. I know that doesn’t sound great, but when you consider that last week they were -$94/head, it is a pretty strong improvement. The cash cattle market was steady to very slightly higher this week averaging around $156/cwt (last week’s average was $155.69). However, packers didn’t buy very many cattle in the negotiated market because they will lose a complete slaughter day on Monday for Christmas and thus their cattle supply needs are not big. It looks like packers might have only bought about half of what they bought the week before. The fed kill this week was only 425k and next week it may be even a little smaller than that. That is almost 100k below what the kill was running near the end of November. Clearly, there must still be some cattle standing in the feedyards that their owners had hoped would be marketed by now. The flow model tells us that there should have been enough cattle to fuel fed kills slightly over 500k per week in December and I estimate that the fed kill during the last 3 weeks on the month will average 440k per week—a deficit of 60k per week or 180k in total. That won’t be helpful in keeping feedyards current. That should help the packers to get cattle bought a little cheaper during January unless more winter weather suppresses weight gains substantially. USDA reported FI carcass weights up three pounds this week when the normal seasonal would be for weights to decline. Of course, this week’s frigid weather has the potential to turn weights sharply lower in the near future, so that is something to keep an eye on.

The polar vortex was very cold, but it held minimal precipitation and was very fast moving, so my guess is that it won’t affect weights in a huge way. On the demand side, perhaps the biggest surprise was that the ribs failed to break lower this week. On a weekly average basis, the rib primal was up about $25/cwt. I can’t believe that ribs are going to stay elevated at that level into January, so I’ve still got a substantial price break built into the forecast. The end meats also posted big gains, but its not that unusual for end meats to get a lot of feature activity in January and so perhaps some retail buyers were spooked by the short production and decided to buy now rather than risk even higher pricing later. It will be interesting to see if they made the right call. One thing that this week’s sharply higher beef prices did was to help turn the combined margin sharply higher. Even if the cutouts don’t hold all of this week’s gains, it is likely that the combined margin is now going to trend higher for a while. However, the chart makes it clear that the recent low was the softest in over five years. That should serve as a caution on beef demand moving into 2023. It’s reasonable to ask whether or not next week will give us a better read on the fundamentals, but I suspect not because the holiday influence will still be there. USDA provided its monthly Cattle on Feed report today and it showed November feedyard placements down 2.1% YOY. That was about 2.5% bigger than what analysts were expecting. As of Dec 1, total US feedyard inventories are 2.6% below last year. It definitely seems like the cattle and beef complex is a bit out of balance currently. Cattle feeders are insisting on higher cattle prices in order to help cover their higher costs of production, but packers have had trouble getting beef prices high enough to cover those higher cattle costs. If they now constrain the kill, that will very likely help their margins, but it will raise the cutouts and thus squeeze retail margins. The retailer will respond by raising prices to the consumer and thus slowing movement through the system. The whole system needs to be made smaller—fewer cattle, fewer feedyards, less packer capacity, and ultimately less beef eaten by the consumer at higher prices. That is the long-run trajectory that the industry is on, but we are just in the initial stages of the downsizing and right now players in each segment are reluctant to give any ground. Eventually those with the higher cost structure will succumb and exit the industry, but it is likely to be a messy process. For the past couple of years, very strong consumer demand has limited the need for this industry downsizing, but now that demand recalibrated lower, the process takes on a stronger sense of urgency. Next week watch for middle meat price erosion and possibly some further strength in the end cuts. The holiday disruptions will still be there, but at least it looks like the weather won’t cause further problems.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}