Beef Wrap December 08

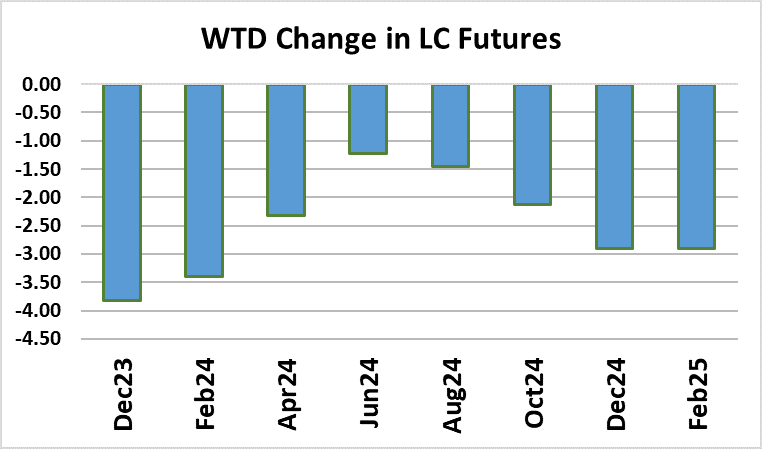

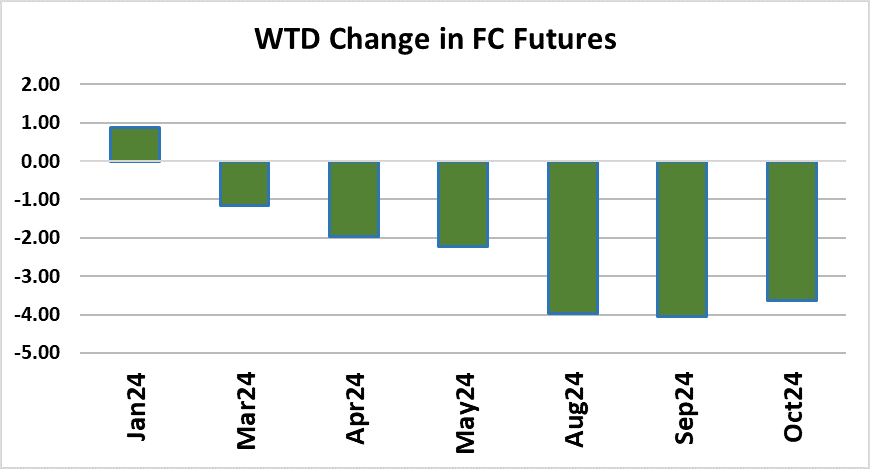

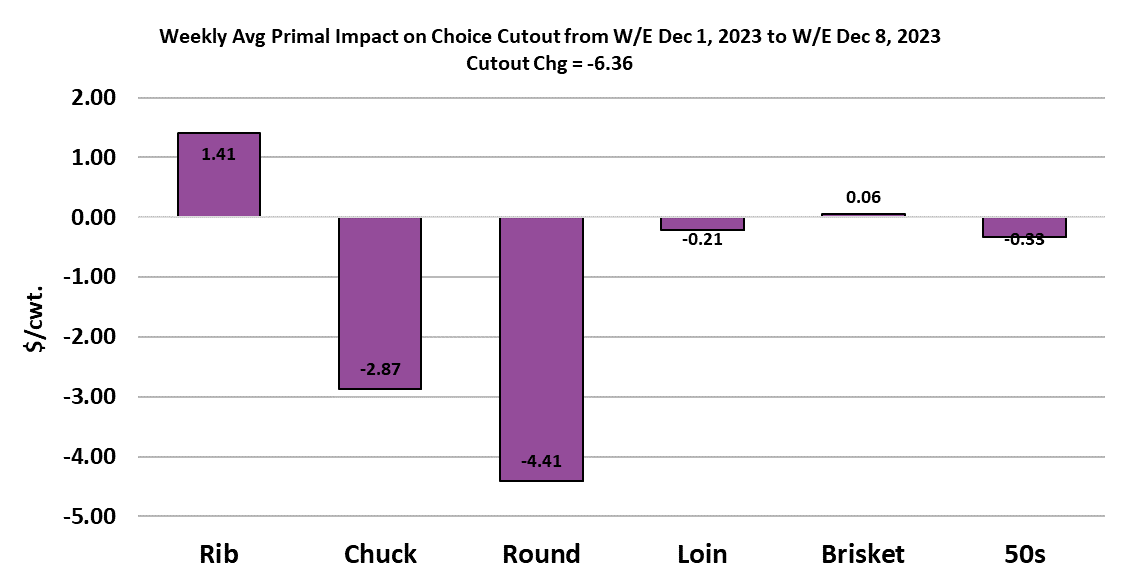

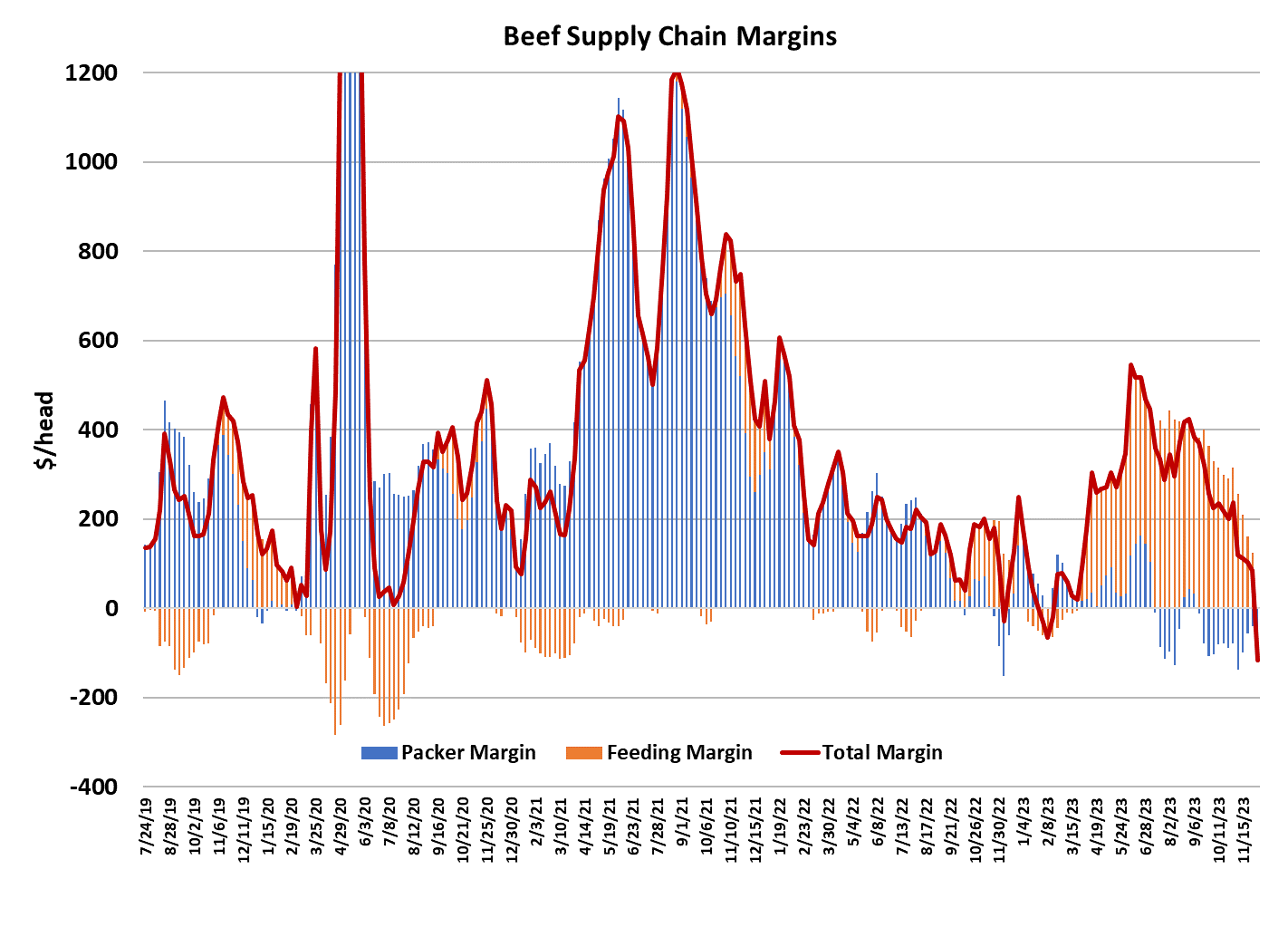

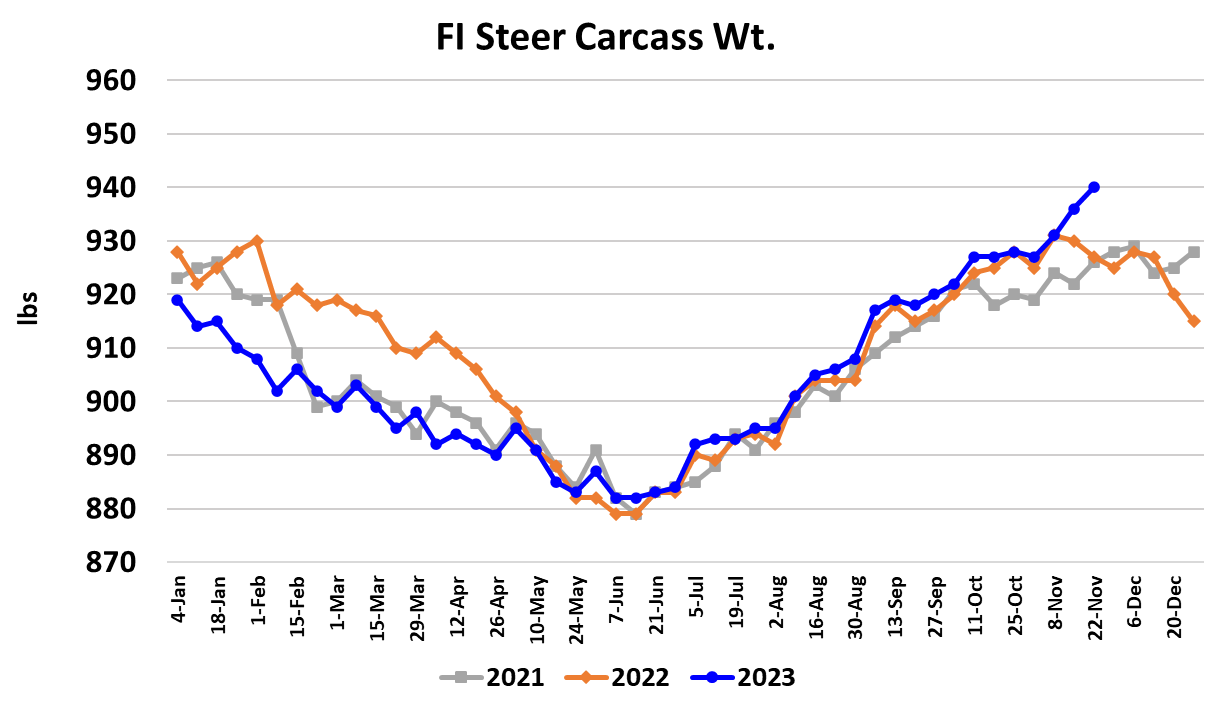

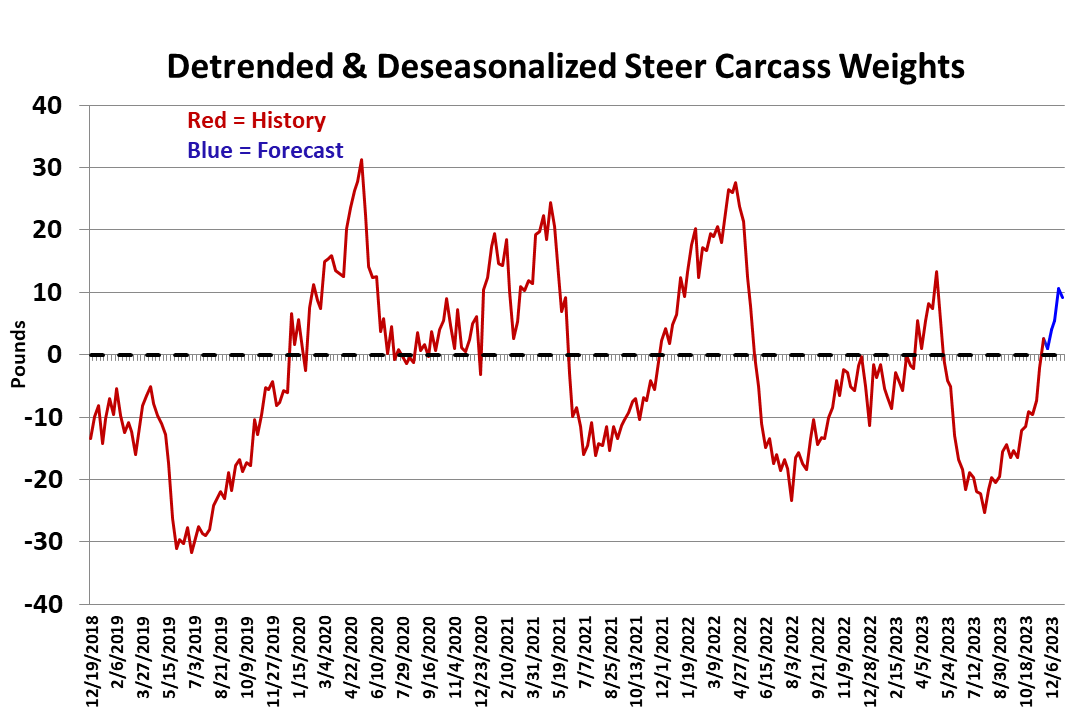

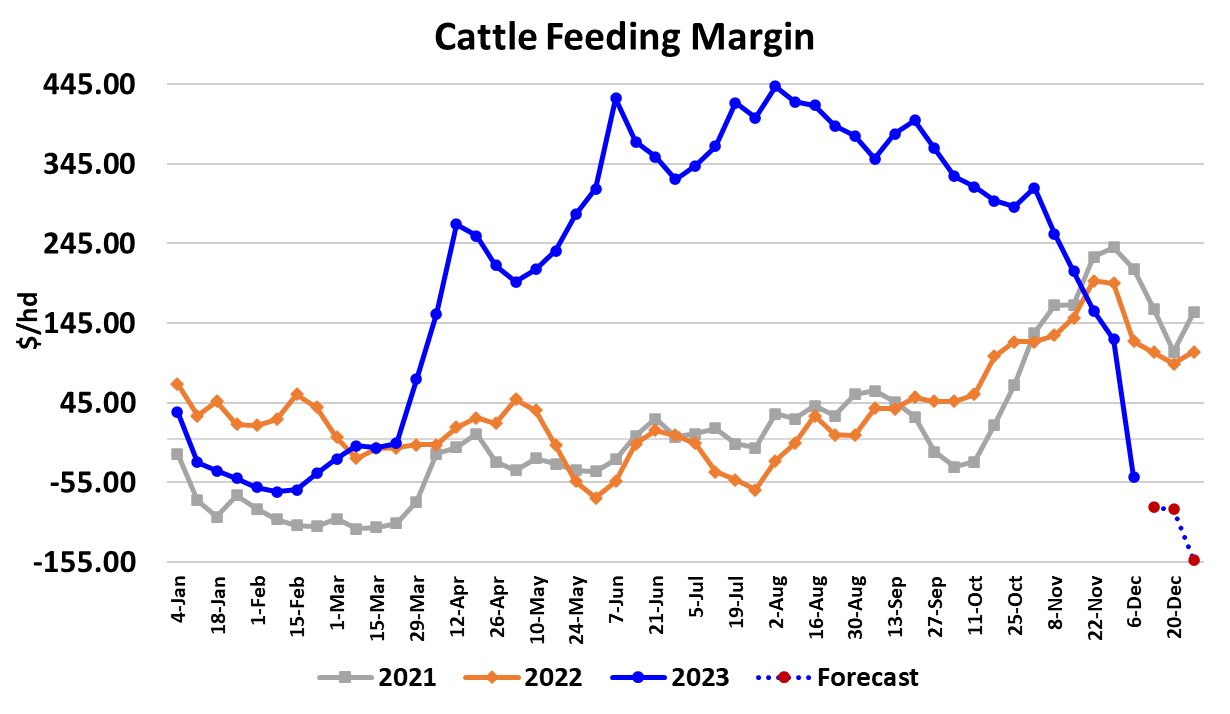

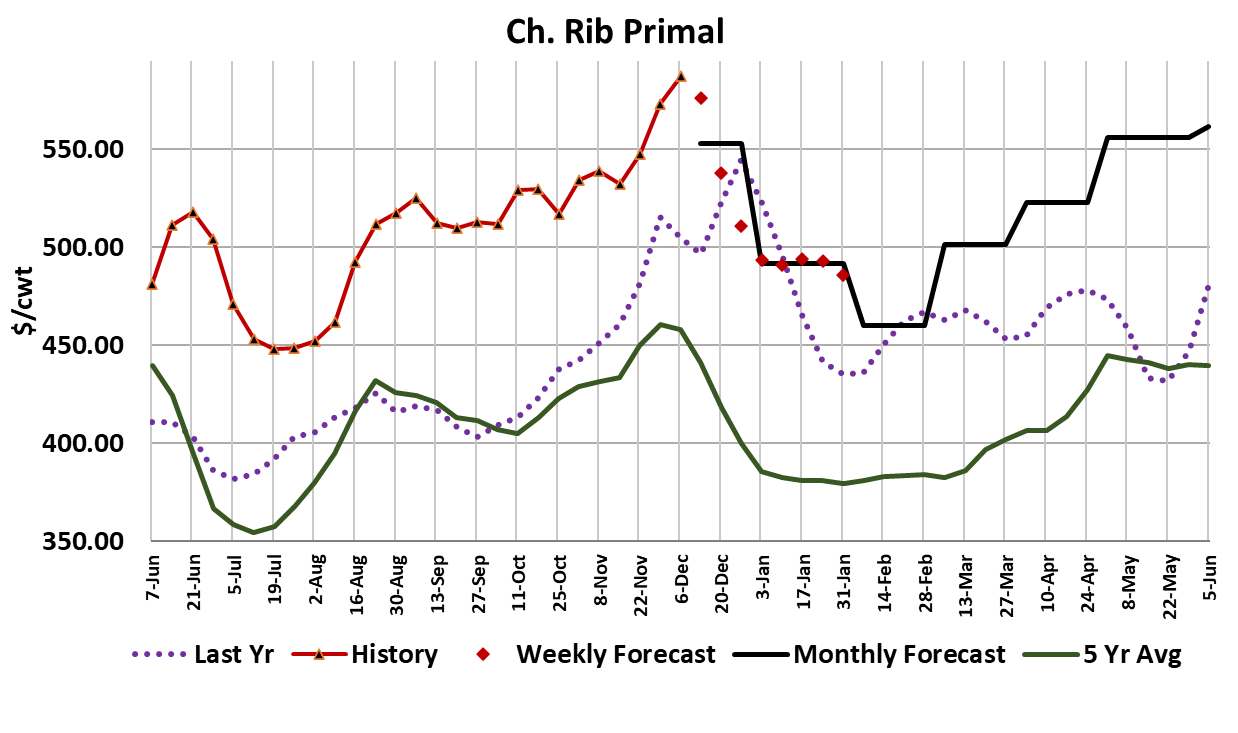

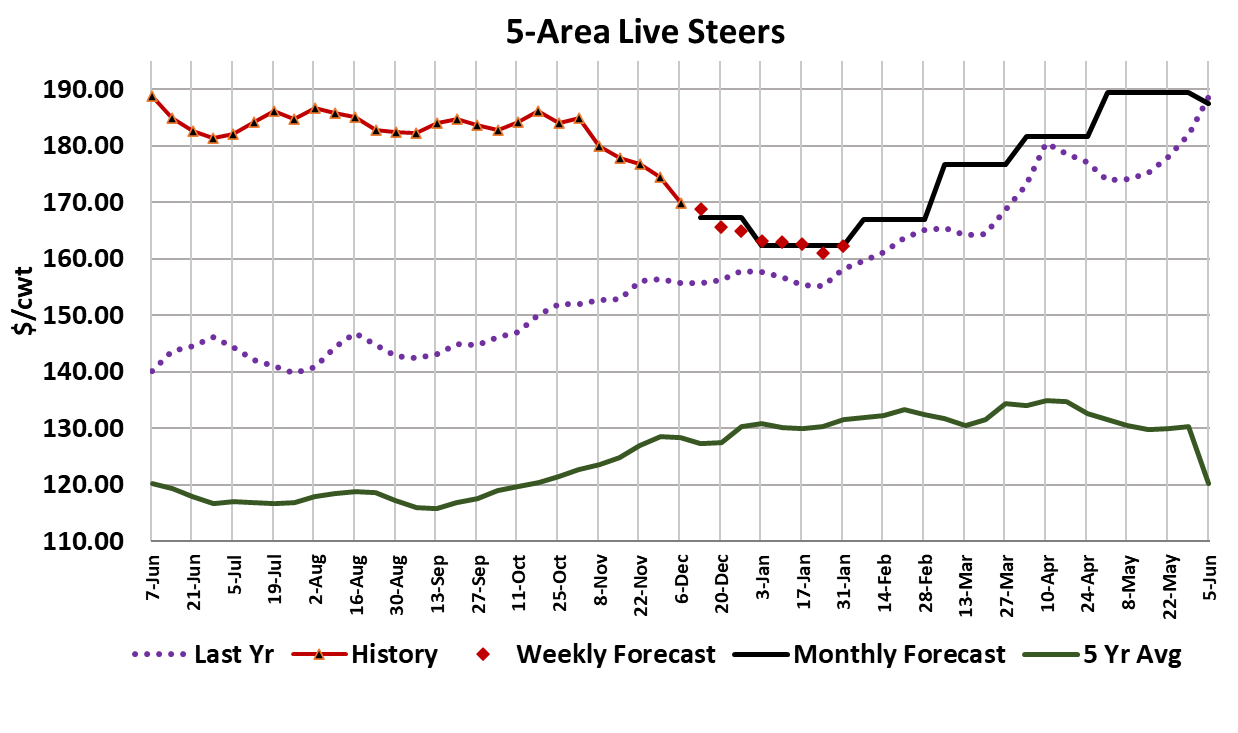

It was another tough week in the cattle and beef markets. The nearby Dec LC contract lost nearly $4/cwt., finishing up at $165.45. On Thursday, it settled three dollars lower than that. Why were traders so pessimistic? Well, there wasn’t much good news in either the cash cattle market or the beef market. Softening demand for end meats continued to drag the cutouts lower, with the Choice cutout losing $6.36/cwt. and the Select cutout dropping $5.98/cwt. on a weekly average basis. Cash cattle traded sharply lower in response, and when all of the numbers are released on Monday, I’d expect the five-area steer price to be close to $169.95/cwt. That would be down almost $4.50/cwt. from the previous week. There was some trade late in the week even lower than that, in the area of $168. So, yeah, very bearish. The futures moved higher on Friday as some traders must believe that the bottom has been made, but I would argue that it could still be a long way off. In the last three months, every time the futures has rallied following a sharp drop it has been a bull trap. That happens because the computers that are buying after the dip based on technical indicators are not paying attention to the fundamentals, and the fundamentals look very dark indeed. Let’s start with the demand side. A quick look at the attached combined margin chart would indicate that something is very amiss in the market right now. This week the combined margin fell to its lowest level since the summer of 2019. Often when one segment of the supply chain gives up margin, the other segment will gain margin and so we don’t often see huge weekly moves. In the current case, cattle feeder margins have evaporated rapidly and packer margins have not improved any. A month ago cattle feeders were making close to $250/head. This week I estimate that their margin fell to -$55/head. A month ago, packer margins were -$78/head and this week I have them at -$67/head, so I guess technically they have improved a little, but they certainly didn’t inherit the $300/head that feeders lost over that time period. A good question to ask at this point is, “If packers didn’t gain the $300 in margin that feeders lost, where did it go?” Certainly not to cow-calf producers, because feeder cattle prices have been coming down rapidly. The lion’s share of it went to retailers. A month ago retailers were facing a $305 Choice cutout when they needed to restock their beef case and this week they faced a $291 average cutout. I’m pretty sure that retailers didn’t lower their retail prices over that period (they may have even raised them), so their already fat margins got even fatter. As the cutout continues lower, retailers will likely lower consumer prices some, but that process evolves slowly and it could take months to get a meaningful price reduction. Until then, these super-high retail prices will limit consumer off-take and that is a real problem because there is a supply bulge coming down the cattle pipeline that is likely to require strong off-take by consumers in Jan/Feb. Now, we all recognize that seasonally, the Jan/Feb period typically has some of the softest demand of the year so it is easy to see how there could be a serious problem in the post-holiday period. One more note on the demand side is that the cutout we are seeing today is somewhat artificial in that it is getting a lot of support from very high pricing in the rib primal due to last minute buying for the holidays. When that goes away, we could see the Choice cutout lose $10 or more in short order. So how will packer margins improve in that environment? The short answer is that they won’t improve unless they can push cash cattle prices substantially lower. Packers will use the only tool available to them and reduce the fed kill. They will get some help from the two holiday-shortened weeks at the end of December. How will that help cattle feeders market the bulge of cattle that is coming? It won’t help at all, it will make it worse. Some might argue that cattle feeders will just refuse to accept any further reductions in cash cattle prices. That is possible, but if they do that they will just be setting themselves up for a bigger backlog of cattle and a bigger train wreck down the road. Cattle weights are still moving higher and that is a sign of a backlog building. The weather across cattle feeding country has been excellent this fall and the weight gains have been strong. Note the de-trended and de-seasonalized carcass weights moved above the zero line this week and probably have further to go. This week’s fed kill registered 492k, but packers would probably have killed less than that if they weren’t chasing Choice middle meats to fulfill previously-booked holiday orders. One of the things that was instrumental in turning the futures market sharply lower over the past few months was large feedyard placements in both September and October. In two weeks we will get the placement numbers for November and my model points to about a 1-2% YOY reduction. First of all, that’s not a very big reduction in placements and second of all, the marketing rate has been so slow that even if my placement estimate is correct, the Dec 1 feedyard inventory will grow to about 2.7% over last year from 1.7% over on Nov 1. I suspect that futures traders won’t like that news at all. Some of the futures contracts on the board have now lost everything they gained in 2023. Some will wonder how it could go any lower from here, but make no mistake, it certainly can go lower. In some ways, 2023 was the perfect storm of very strong demand meeting cyclically tighter cattle supplies, but now it seems the air is coming out of the demand side rapidly and we are faced with a near-term abundance of cattle. Longer-term, the outlook is still bullish because cattle numbers are likely to continue to shrink for at least another couple of years. It’s even bullish in the second half of 2024 because if we have a backlog-induced train wreck in the cattle market early in 2024, cattle feeders are likely to slam the brakes on placements and that would result in tighter cattle and beef supplies later in the year. Near-term however, things don’t look very good and it feels like we are closer the beginning of this problem than to the end of it.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}