Beef Wrap December 15

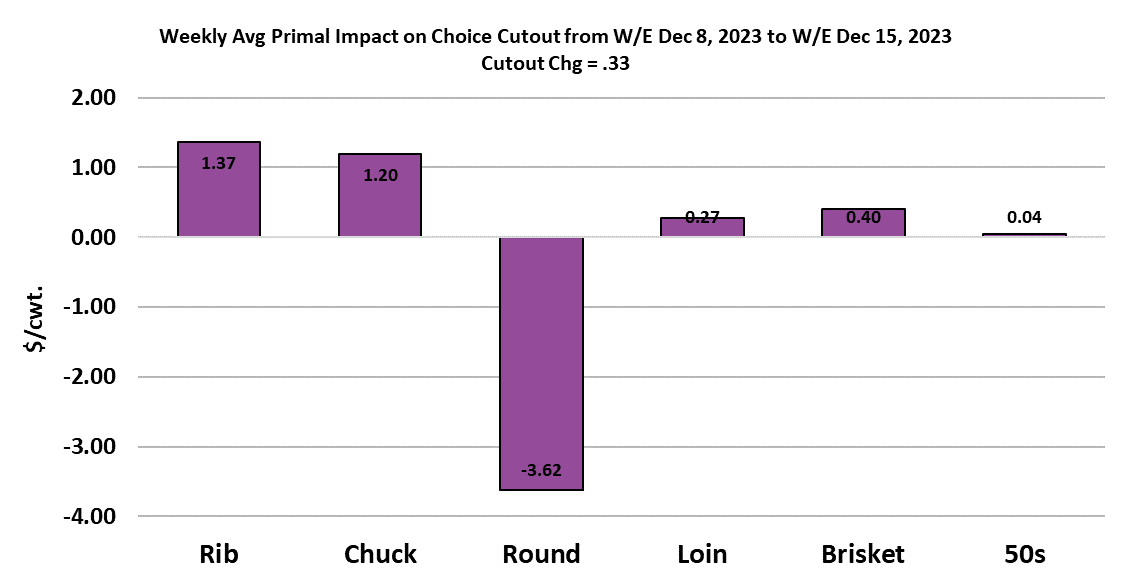

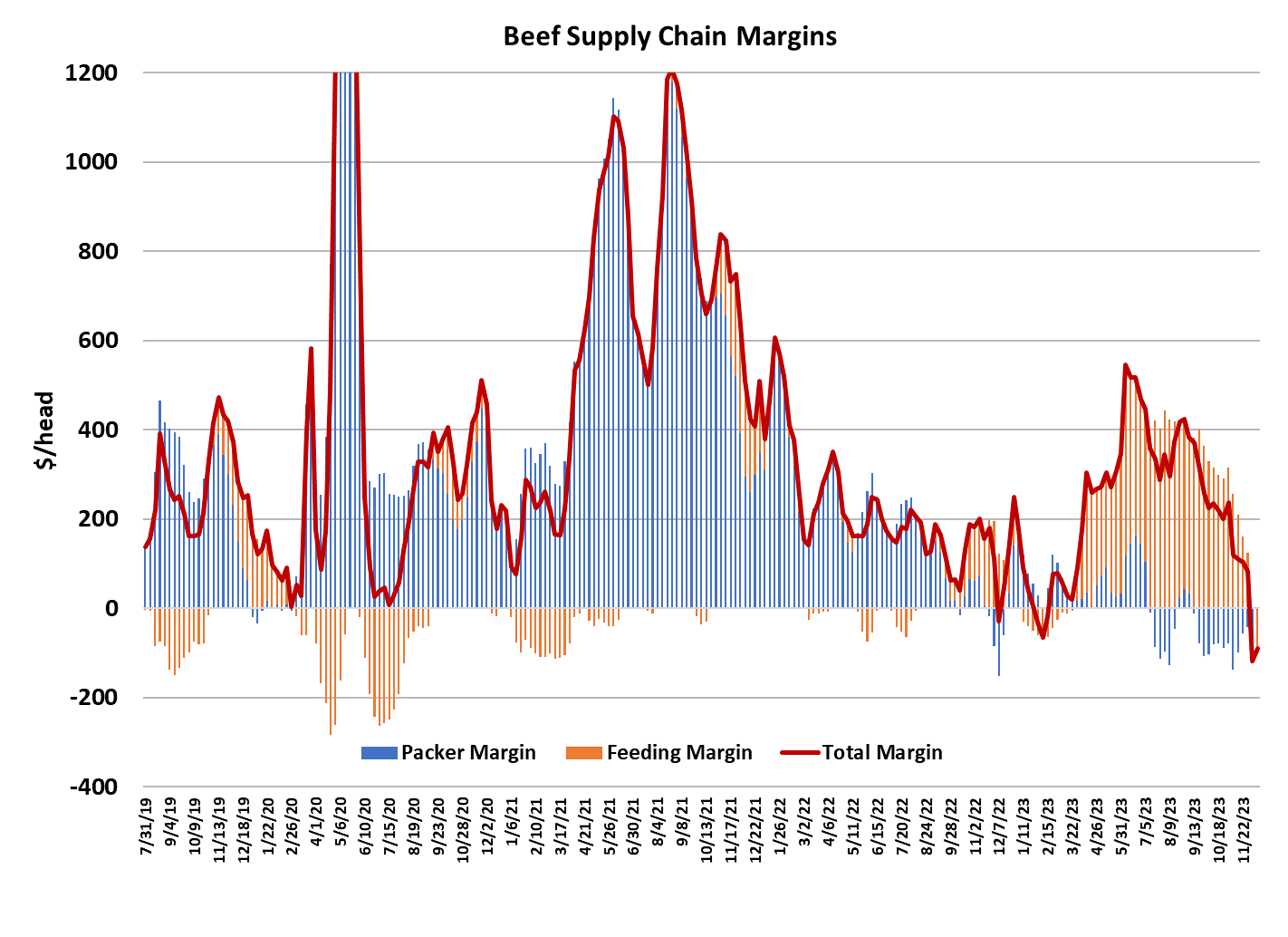

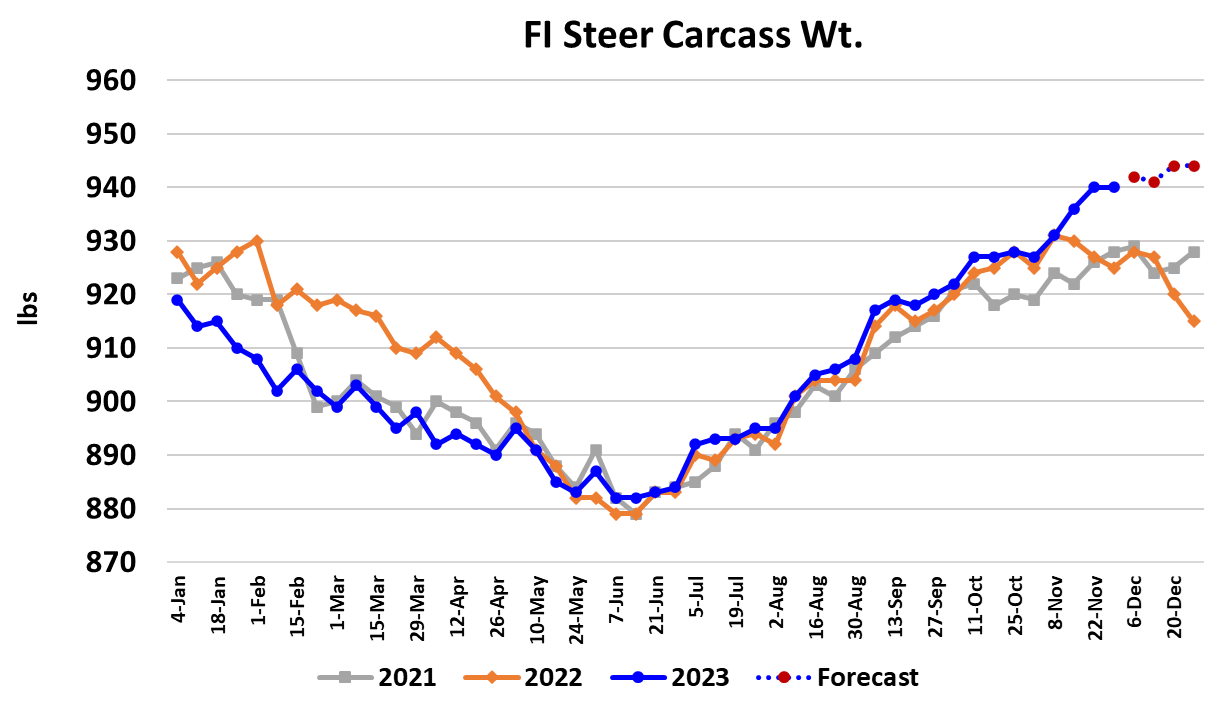

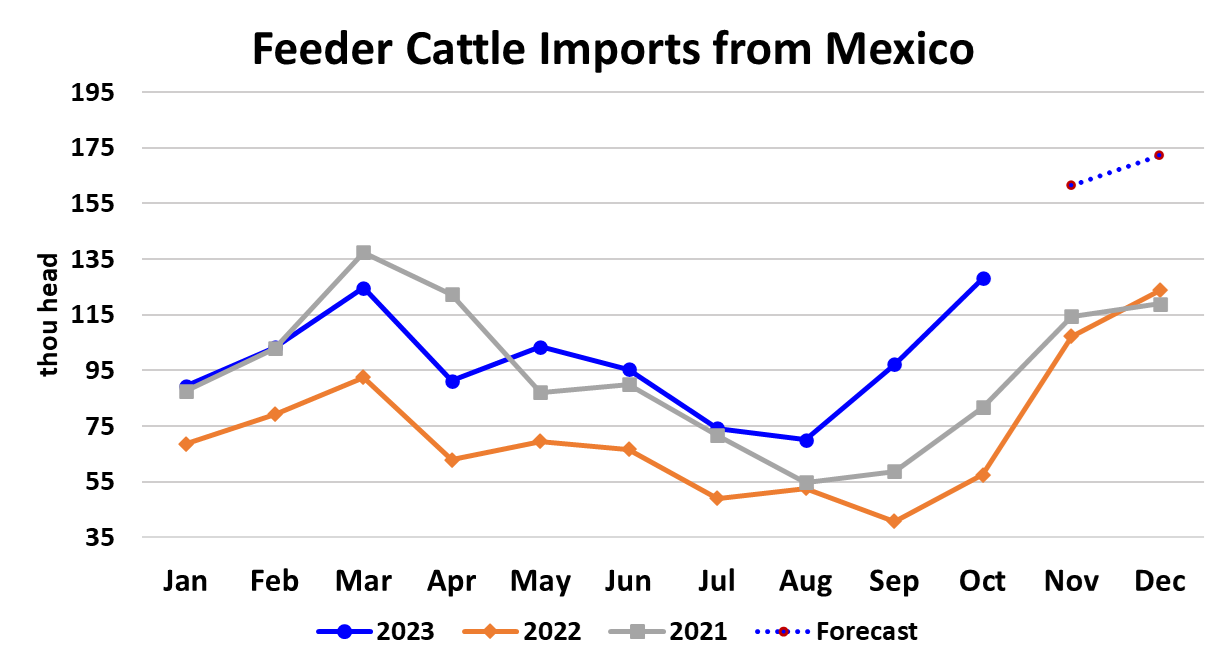

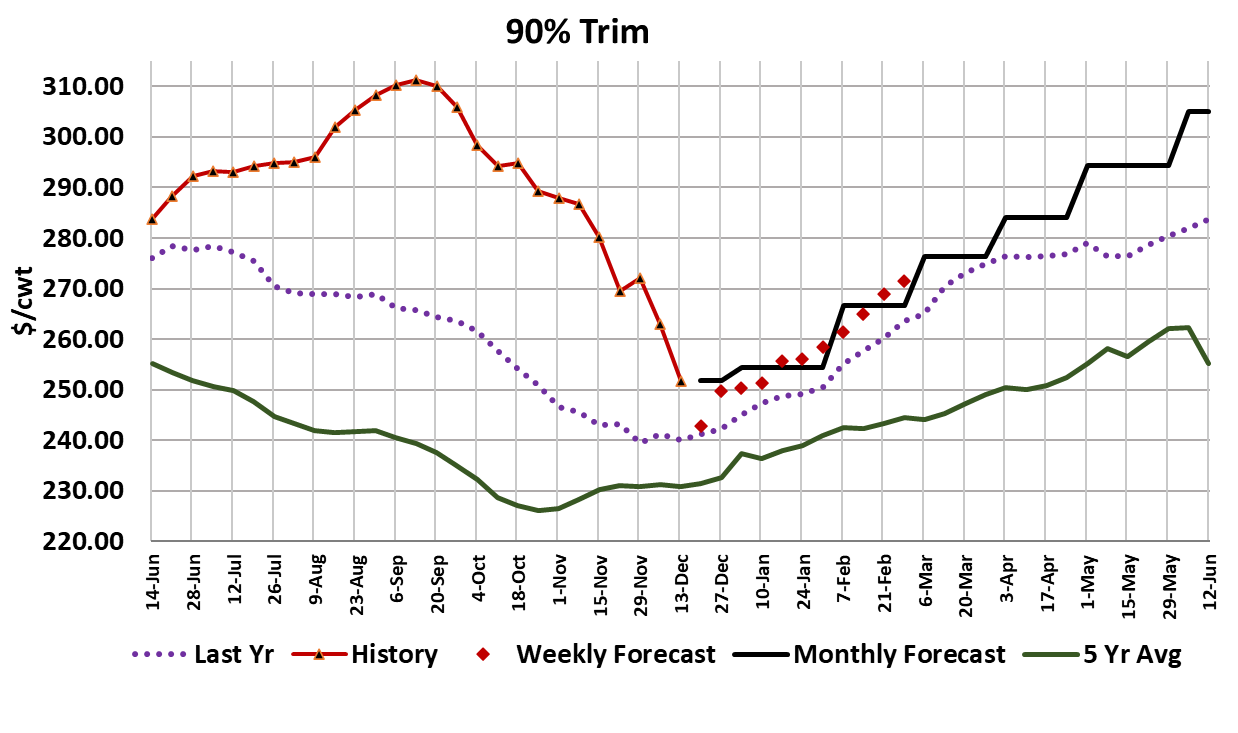

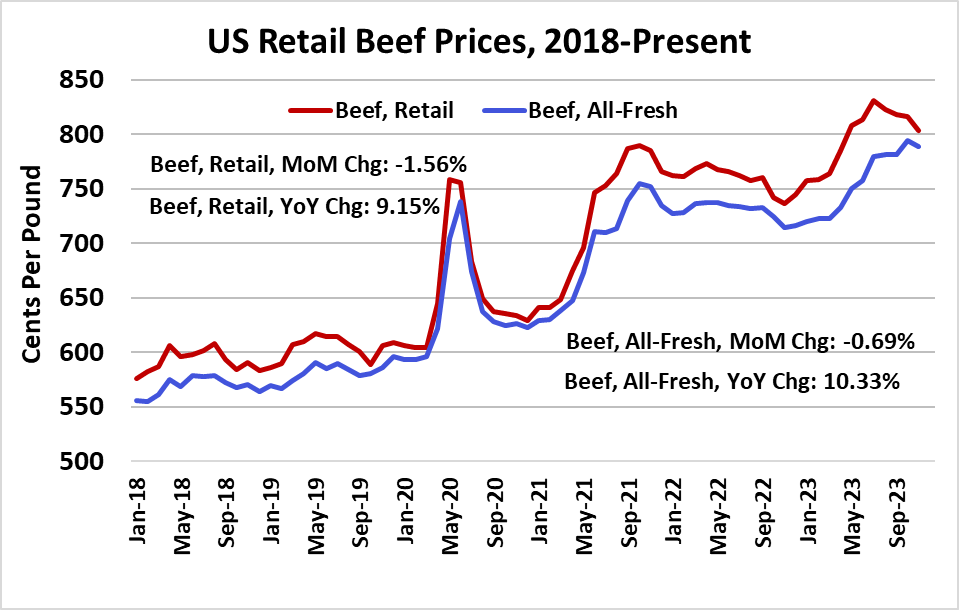

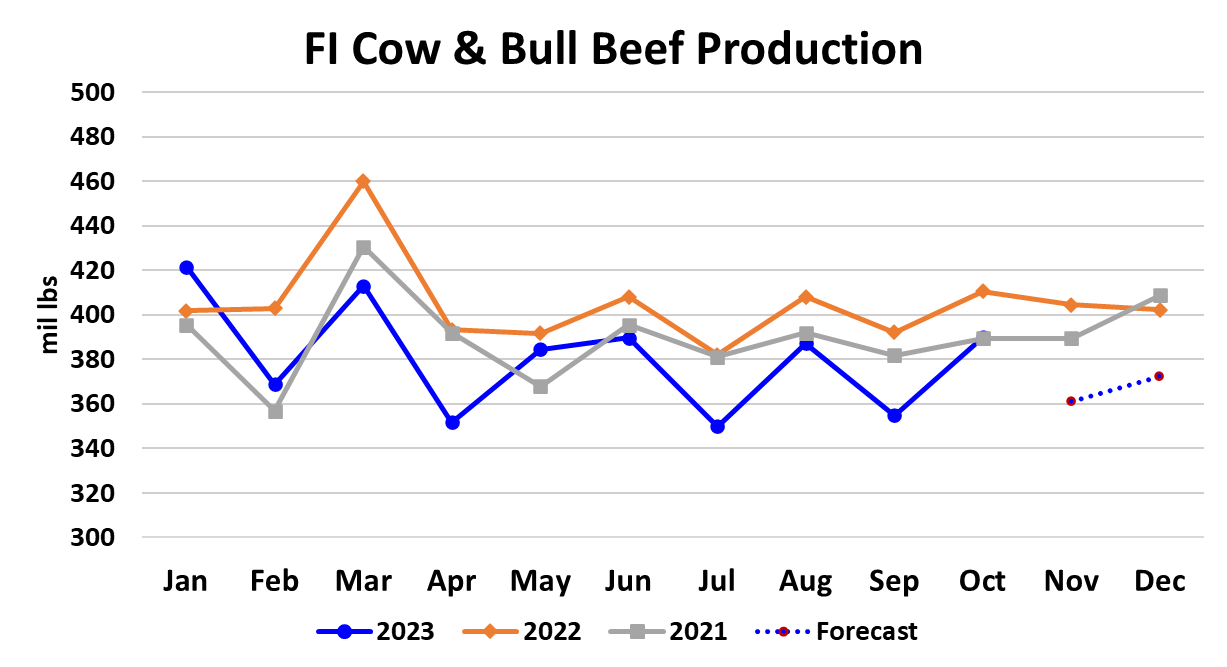

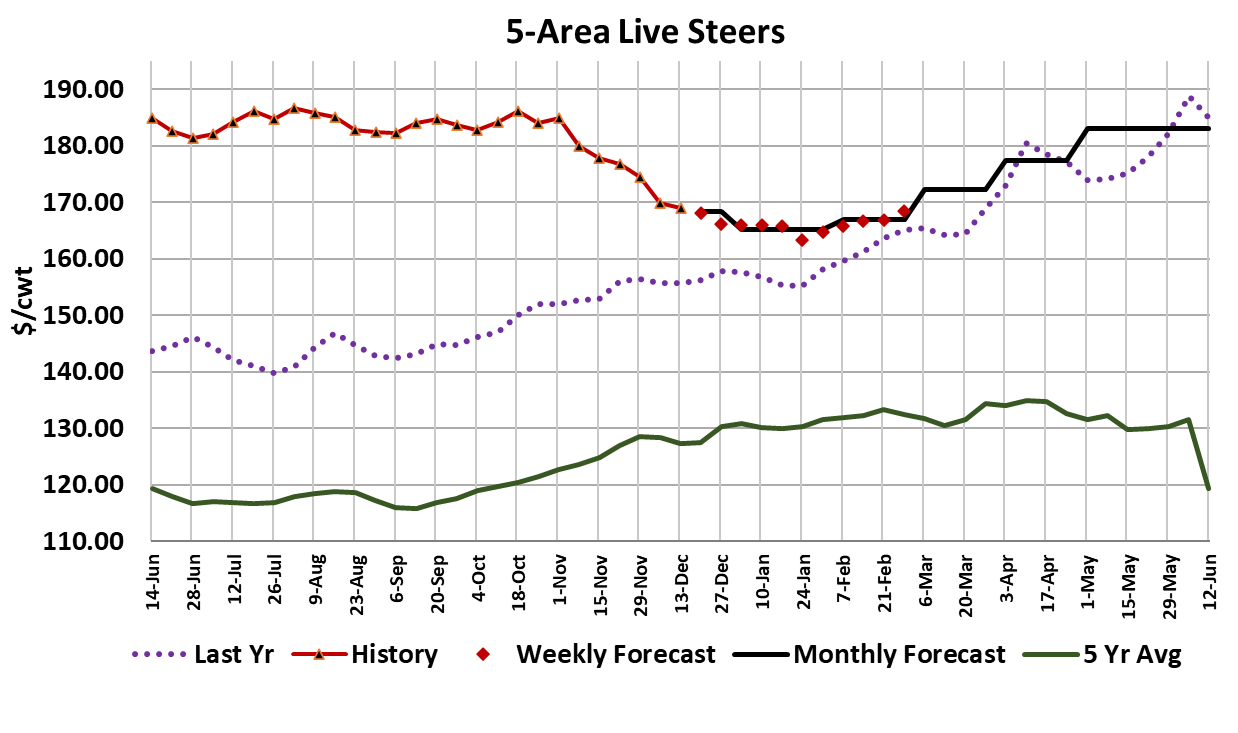

The cash cattle market traded lower again this week, with transactions in the Southern Plains at mostly $170, down $1 from the week before, while trades in the North were from $167-170, with more activity located at the lower end of that range. For the week, it looks like the average 5-area live steer price will be just a little over $169. The beef market was mostly steady in aggregate, with the Choice cutout gaining a mere $0.33/cwt. on a weekly average basis and the Select cutout losing $0.42/cwt. Packer margins improved considerably because the cattle that showed up for slaughter were purchased last week, when price levels dropped $4/cwt. I calculate this week’s packer margin to be very close to zero. Packer margins have been solidly in the red since mid-September, so this is a clear sign that packers have finally wrestled some leverage back from feeders. The packer’s leverage should improve even more in coming weeks as they will need to purchase fewer cattle in the next two weeks as they prepare for short kills due to Christmas and New Year’s. At the same, we have seen a lot of warmer-than-normal weather through the Plains States and that is forecast to continue through December, thus producing better-than-average cattle performance in feedyards. Carcass weights are the highest they have ever been in history and the latest FI steer weights were 15 pounds over last year. Cattle feeders want to behave as though there is no problem with cattle backing up, but the data suggests otherwise. There seems to be a feeling that just because the futures stopped going down for a week, that the worst of their pricing problems is over. But the futures are different from cash market fundamentals and those don’t look so good at the moment. Next Friday, USDA will deliver another Cattle on Feed report and my model is pointing to November placements that are down only a fraction of a percent from last year. If that comes true, then the number of cattle standing in feedyards as of Dec 1 would be up close to 2.8% YOY. Futures traders haven’t taken kindly to bearish COF numbers in recent months and they may very well get another set of them next week. One thing driving strong feedyard placements is a big increase in the number of feeder cattle coming into the US from Mexico (chart attached). This week’s fed kill came in at 505k, up 9k from the week before. That kill was a little bigger than expected and probably reflects packer’s desire to build some beef inventory ahead of Christmas week, especially since slaughter on the Saturday before Christmas is likely to be pretty light. For the holiday weeks themselves, I’m forecasting the fed kill to average around 425k in the first week and 435k in the second week. One supply side variable that we always need to watch closely in the winter is weather. Snow and rain can cause muddy feedyards that hurt weight gains and cause cattle prices to soar. However, there is no evidence of that this year. In fact, recent weather forecasts point to temperatures in the Northern Plains during Christmas week that could be as much as 20 degrees warmer than normal. Of course, a weather market could still develop, but right now it looks like just the opposite is occurring. The demand side of the market is strong in a historical context, but appears to be easing from the red-hot levels seen earlier this fall. This week, the rib and chuck provided support to the cutout that helped to offset a big drop in round prices. The rib primal is probably just days away from collapsing and that should take several dollars off of the cutouts. Pork demand is awful right now and chicken demand is also soft. It is probably just a matter of time before beef demand buckles. January is a prime candidate for that. Beef 90s have been falling hard in the last few weeks and are now back very near to last year’s levels. It’s not a coincidence that prices for end cuts from fed cattle have also been coming down rapidly. Those two markets are closely related. Cow kills have been running below last year for all of 2023 and are currently about 5-7% lower YOY. So, if cow beef production is down substantially from last year, yet 90s price levels are getting very close to last year, that tells me that the demand side of the lean beef market is softening. That could pose a problem for the end cuts in the near term. Once piece of good news that came out this week is that USDA reported the all-fresh beef retail price down 0.7% in November. That’s not a huge drop, but it will help. YOY, that all-fresh price is still up more than 10%. I think that high retail beef prices are going to constrain consumption in the next couple of months, right when the bulge in fed cattle supplies needs to be marketed. Export demand still looks soft, judging from the weekly volumes that FAS reports. Maybe if beef prices reset lower in Jan/Feb, then we might see some improvement in overseas movement. Next week, we could get a trifecta of lower cattle prices, lower cutouts and a lower futures market in response.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}