Beef Wrap August 19

Cash cattle prices advanced again this week, gaining $2.37 to

average $146.76. As usual, prices in the North were reported

several dollars over the South, which traded in the $141-142

range. While packers’ cattle cost was rising, the price they got

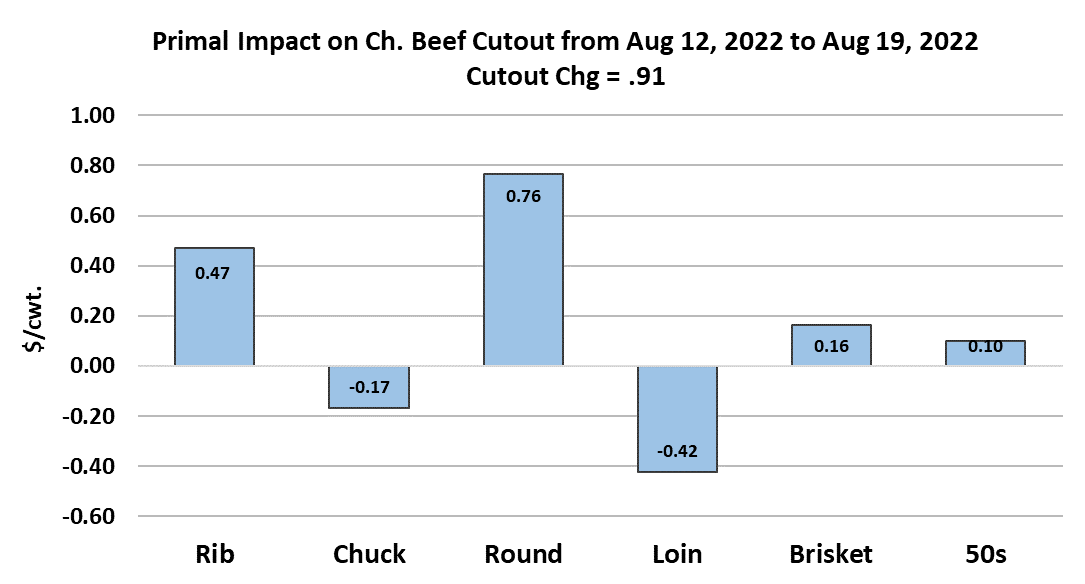

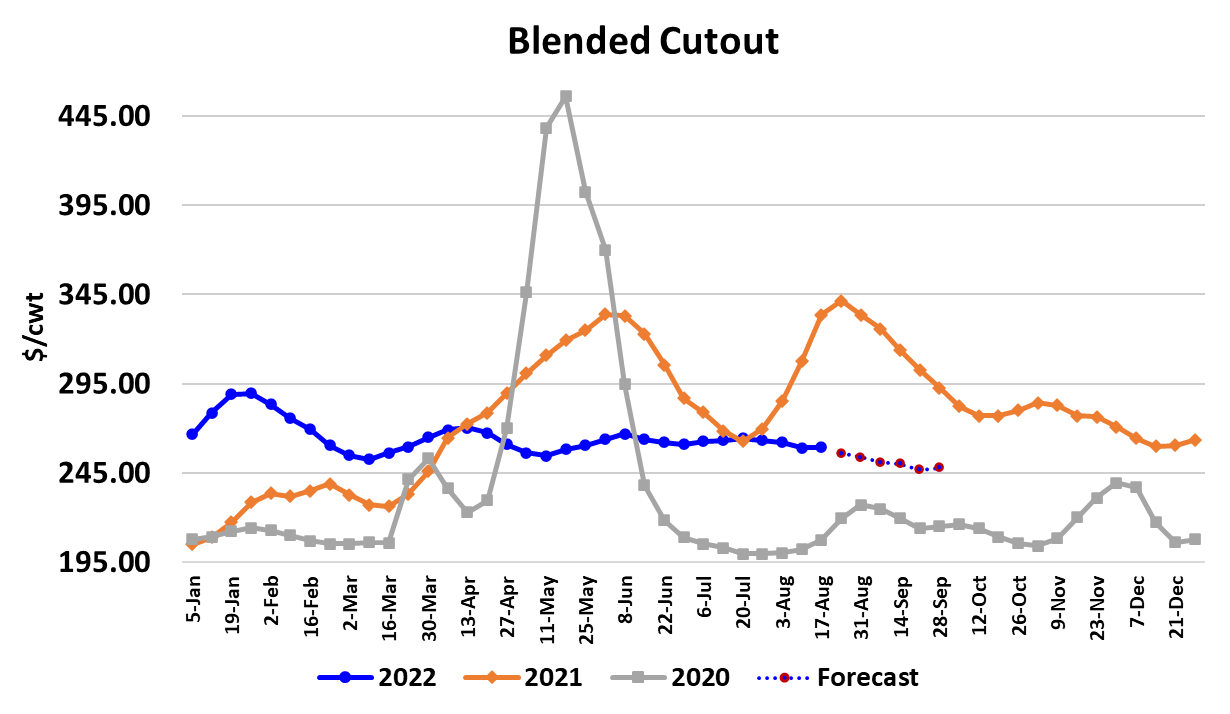

for their beef was not. The Choice cutout gained a paltry $0.45/

cwt and the Select cutout was up only $0.30/cwt. That means

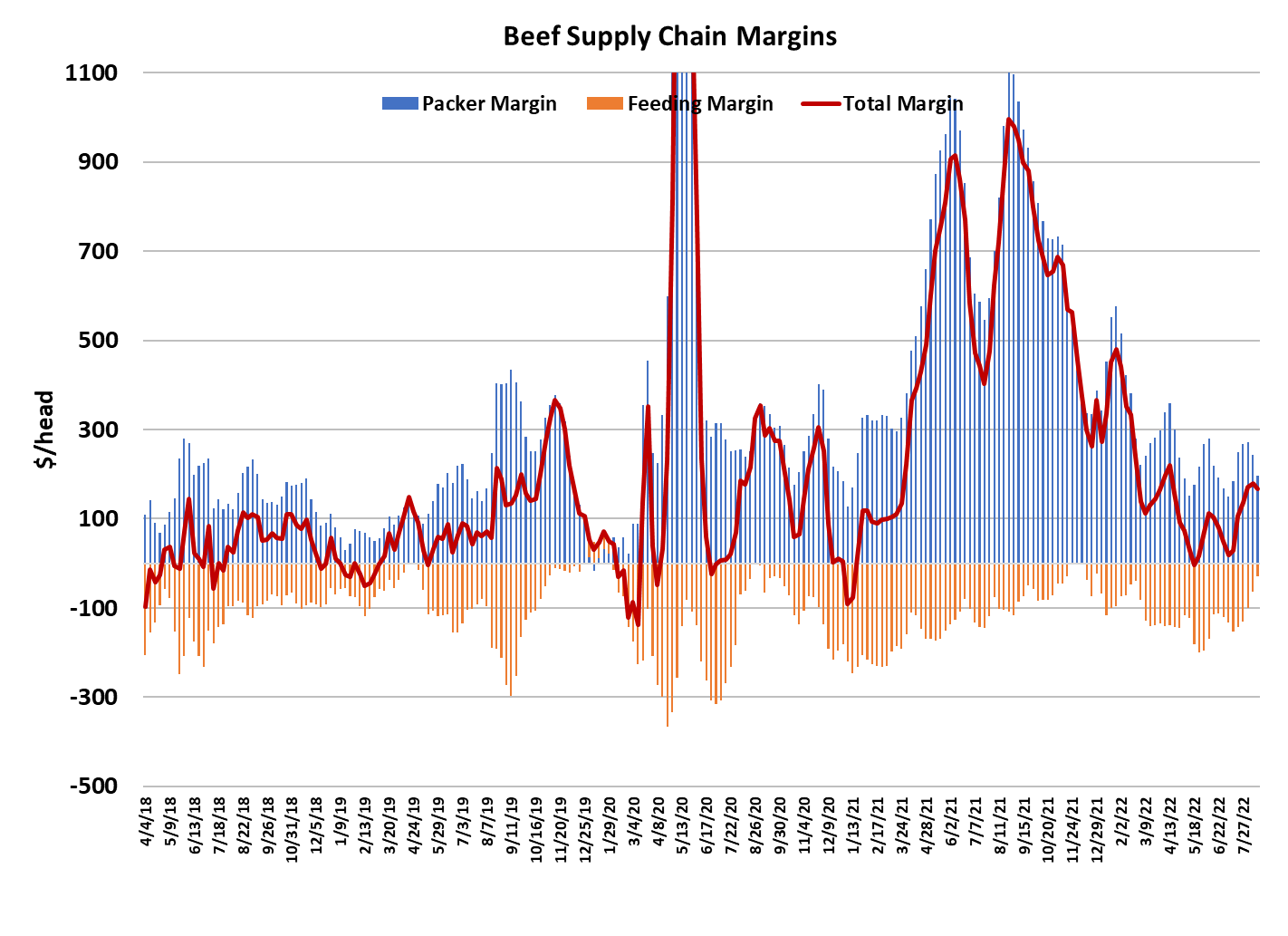

packer margins compressed further, now estimated near $197/

head. When this week’s more expensive cattle show up at the

packing plant, margins are likely to fall below $150/head. There

have been some rumblings about packers cutting the kill in order

to protect their margins, but so far we haven’t seen a concerted

effort to do that.

This week’s fed steer and heifer slaughter registered 517k, up 12k

from last week, but still below the 525-530k that the flow model

suggests. The biggest surprise in this week’s production data

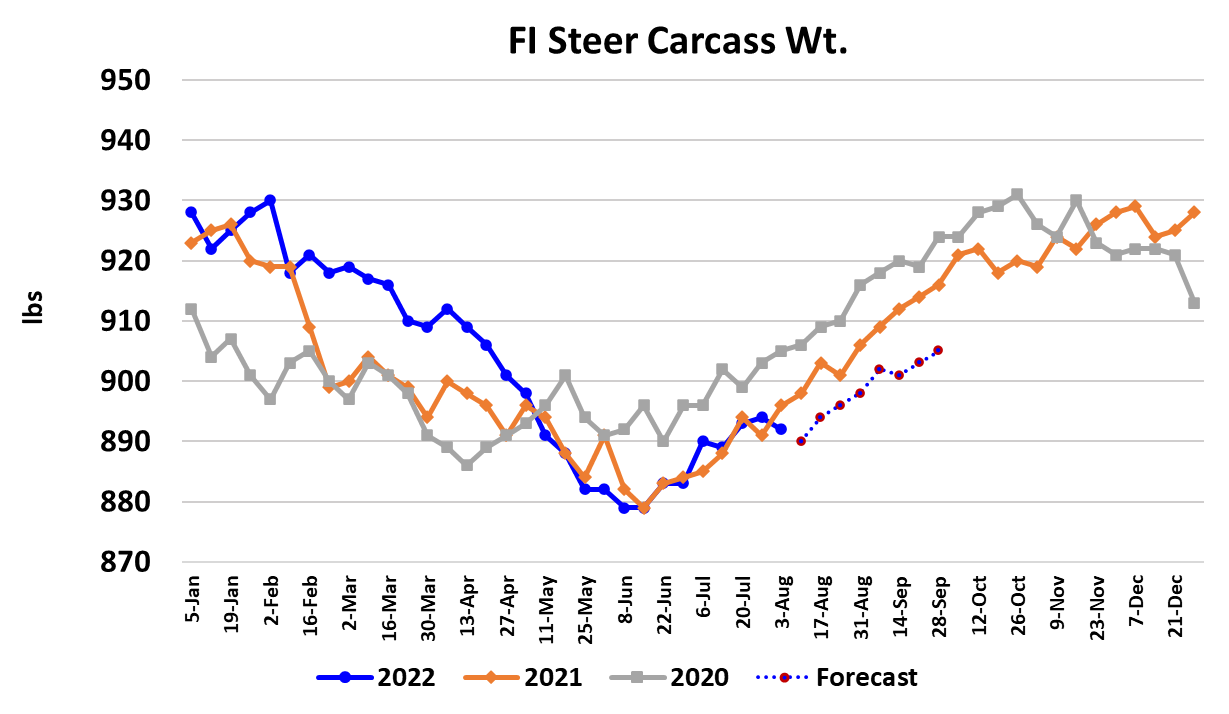

was carcass weights, where steer weights came in 2 pounds

lower than the week before. The normal seasonal pattern in

carcass weights would have them increasing about 3 pounds per

week at this time of year, yet we saw weights actually decline.

The DTDS weights, which were already at very low levels, moved

even lower. This information makes a strong case that feedyards

are very current and thus in no hurry to market cattle. Packers

will be busy delivering on Labor Day orders over the next couple

of weeks and thus I think that cutting the kill is not something they

would do in a big way until after those orders have been satisfied.

Thus, cattle feeders seem to have packers over a barrel right now

and are extracting higher cattle prices as a result. Cattle feeding

margins have improved a lot lately, going from -154/head in the

middle of July to -38/head this week. It seems to me that, with

feedyards very current and packers reluctant to cut kills as they

are delivering on Labor Day orders, there is a good chance that

cattle prices will rise for at least a couple more weeks. After that

however, Labor Day week will be upon us and that provides

packers with a natural excuse to scale back the kill. The

presence of the holiday on a Monday is likely to cause the kill to

be suppressed in 2 consecutive weeks since packers will likely

give workers the Saturday heading into Labor Day off. My guess

is the steer and heifer slaughter for the 2 weeks around Labor

Day will average close to 480k each.

When packers get back to full kills in September, the flow model

suggest that they should be able to find enough cattle to kill

530k each week through the balance of September and into

October. It is that post-Labor Day timeframe when the best

opportunity will exist for packers to pull back hard on the kill and

thus increase the odds that they can stop the rising cash cattle

market. In the beef market, after Labor Day we should see

better interest in end meats as the weather cools down some in

the northern tier states and by the end of September buyers

should be actively working on packages for the end-of-year

holidays that will focus on the middle meats.

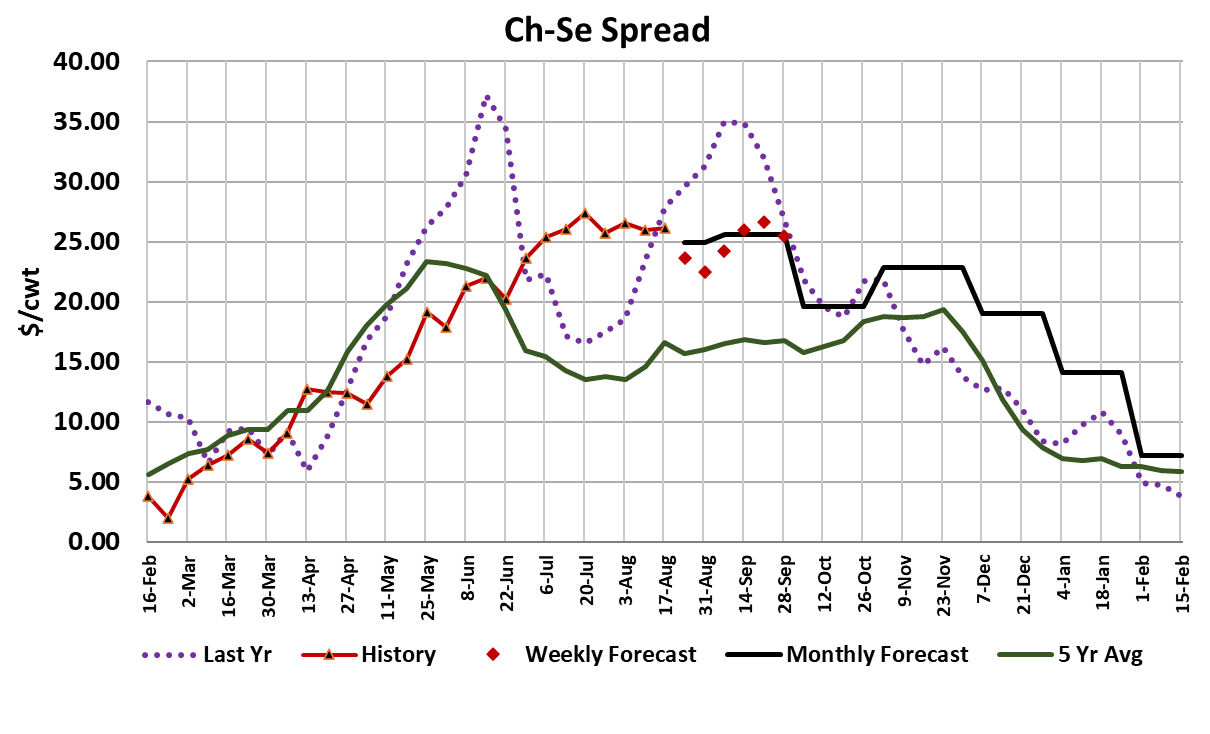

They will want Choice of better product to fill that need and that

is something that is pretty tight right now. This week the ChoiceSelect spread averaged over $26/cwt and packers were paying

an average of $20/cwt over that for cattle that will grade Prime.

Clearly, the supply of high quality beef is low relative to demand

right now. Look for the Choice-Select spread to remain wider

than normal for the next several months until all of the holiday

business is wrapped up. The combined margin worked lower

again this week, but the decline was small. There just isn’t much

movement in the cutouts lately and that seems to be keeping

prices in other areas of the beef complex from moving very

much. About the only place that we are seeing significant price

movement is in the cash cattle market. There wasn’t much

notable in the export data that was released this week.

China continues to be the number 3 destination for US beef,

behind Japan and S. Korea. Domestic beef demand appears to

be in a very slow moving downcycle while international beef

demand appears to be holding steady. Today’s Cattle on Feed

report pegged placements during July up 1.8% from last year.

That was larger than the average trade guess and fourth month

in a row now where placements have been larger than

expected. We now have a pretty good handle on the feedyard

inventories that will fuel beef production through the end of 2022

and it looks like there is a strong chance that 2022 beef

production will be almost equal to 2021. Next week, expect the

cutouts to trade steady to slightly lower on some slippage in end

meat prices. Cash cattle are likely stronger again next week as

the upward momentum continues.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}