Beef Wrap August 25

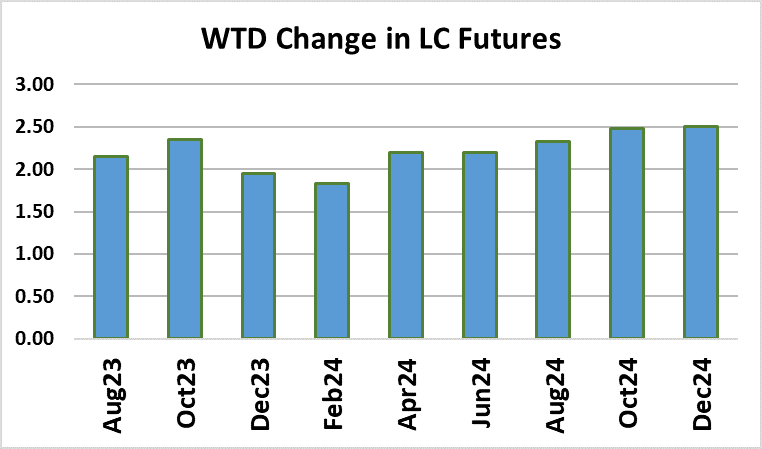

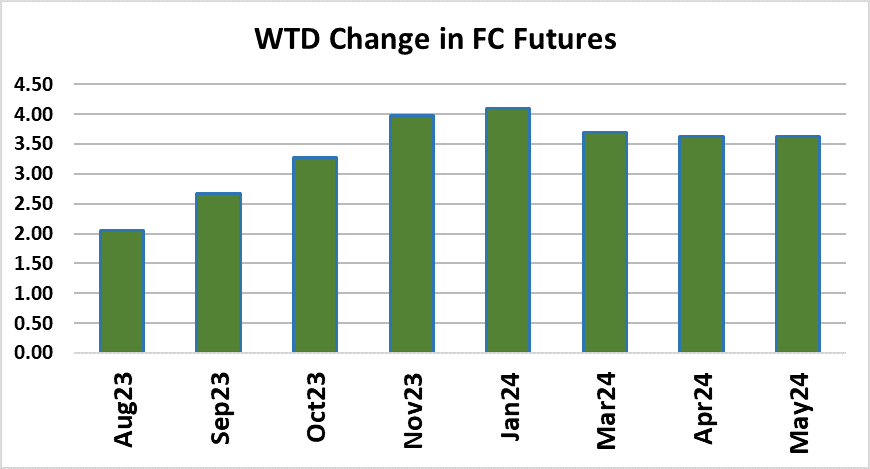

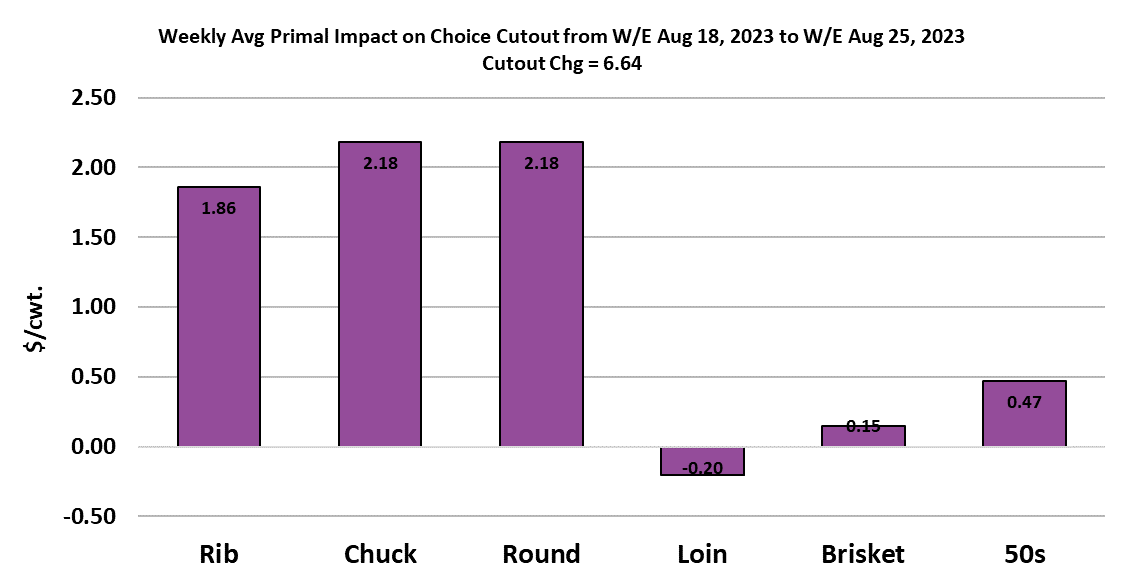

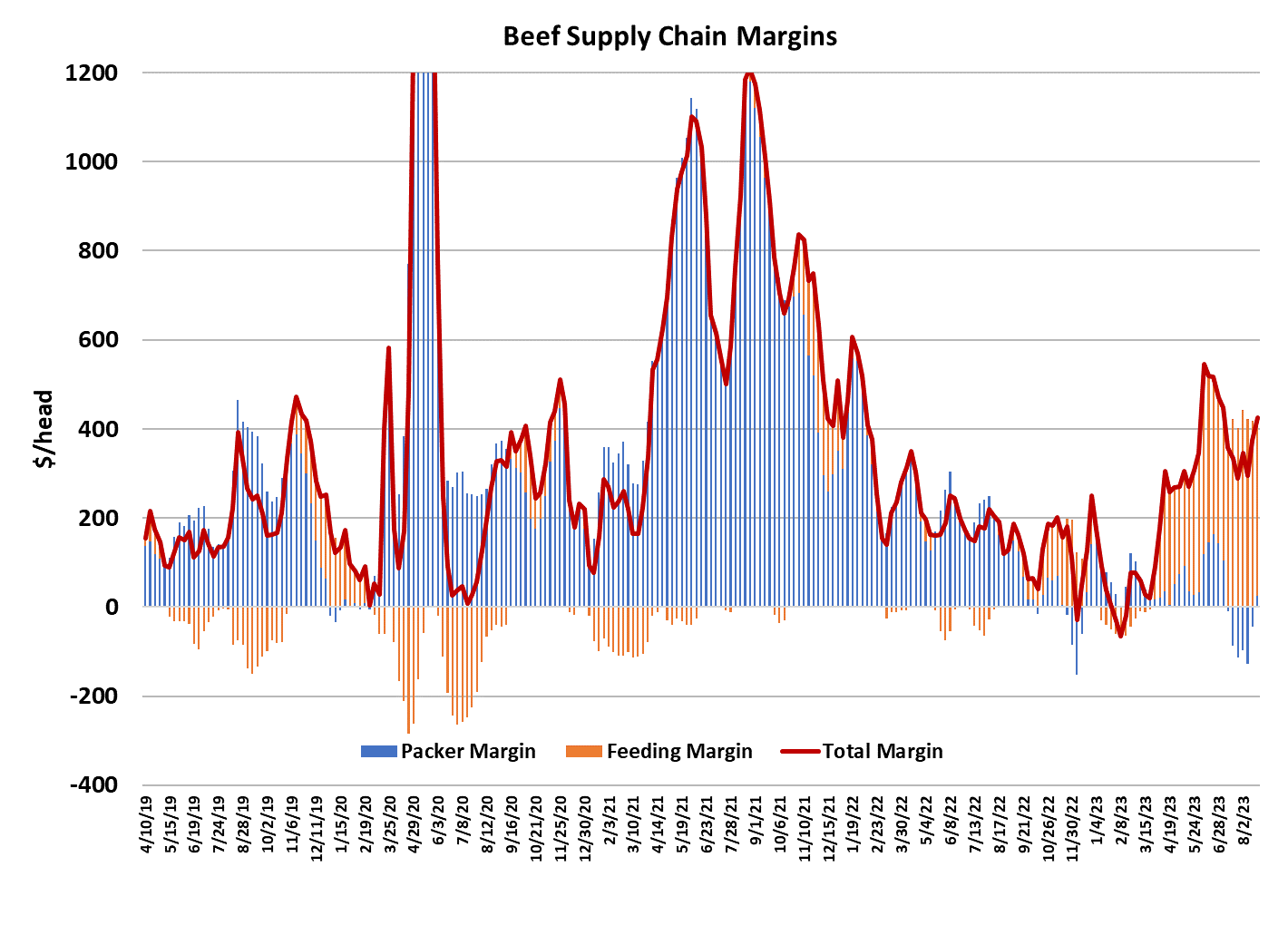

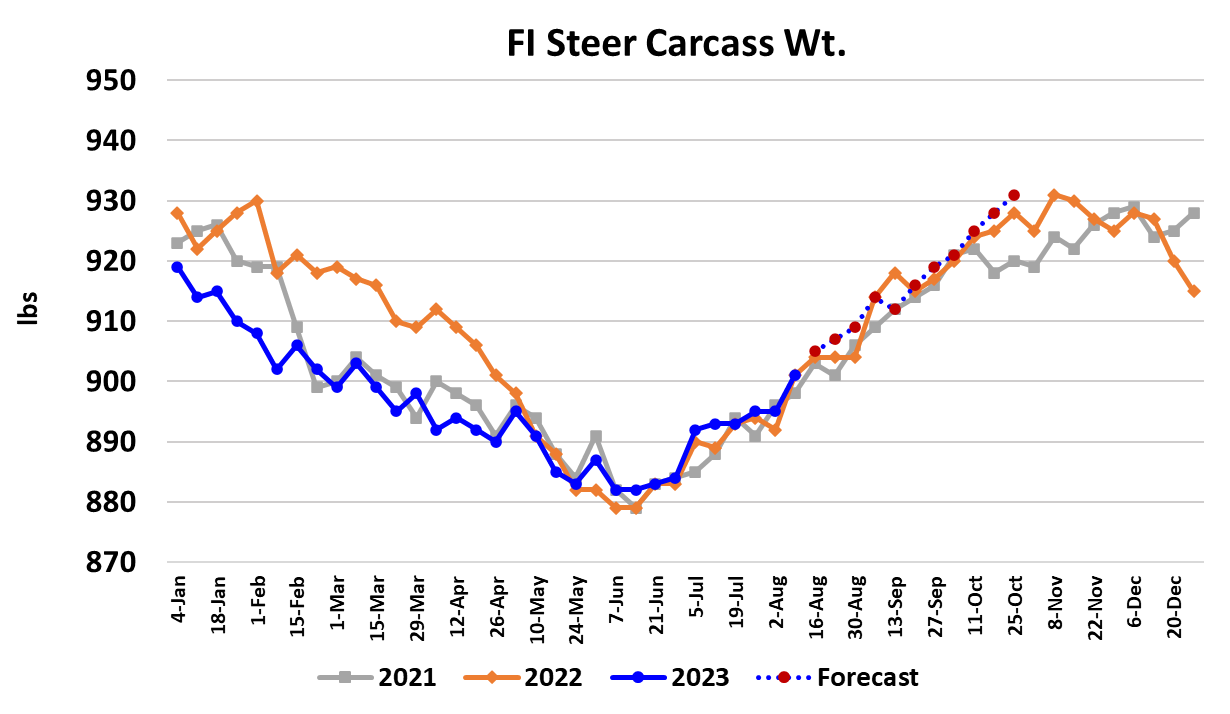

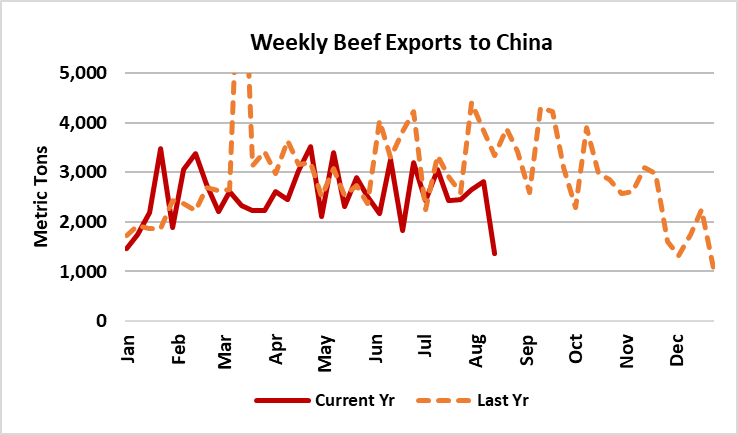

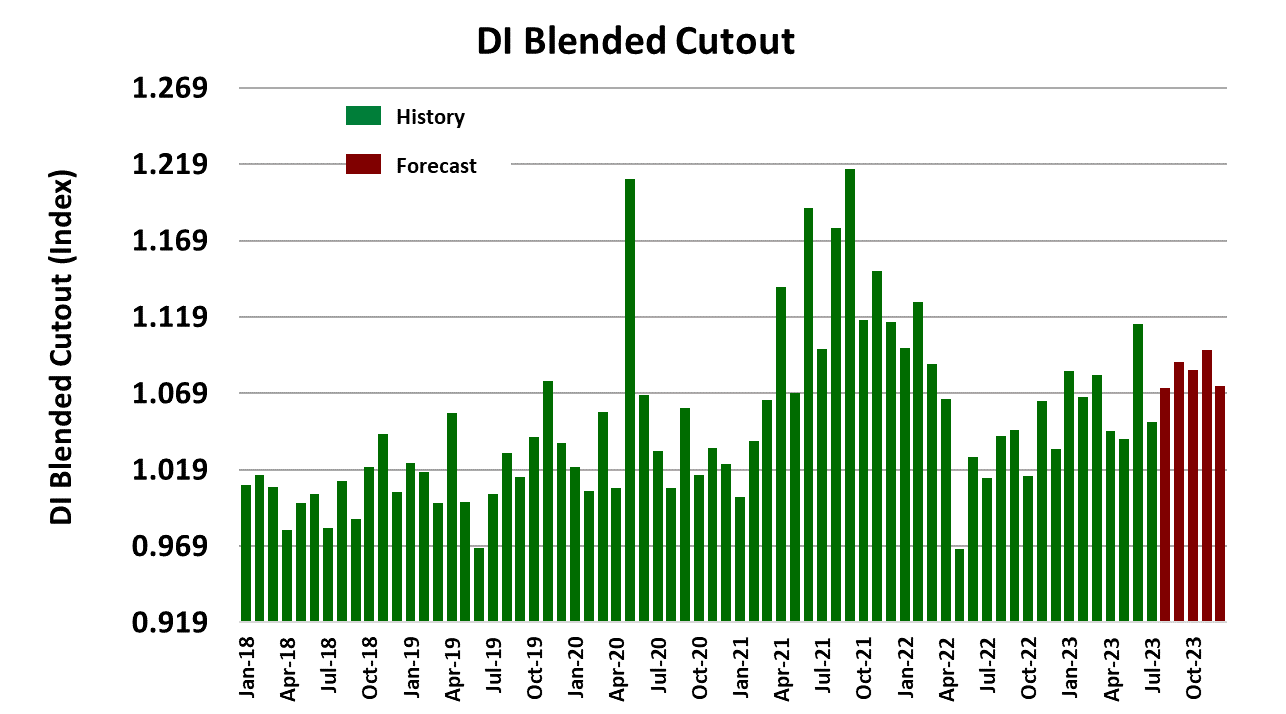

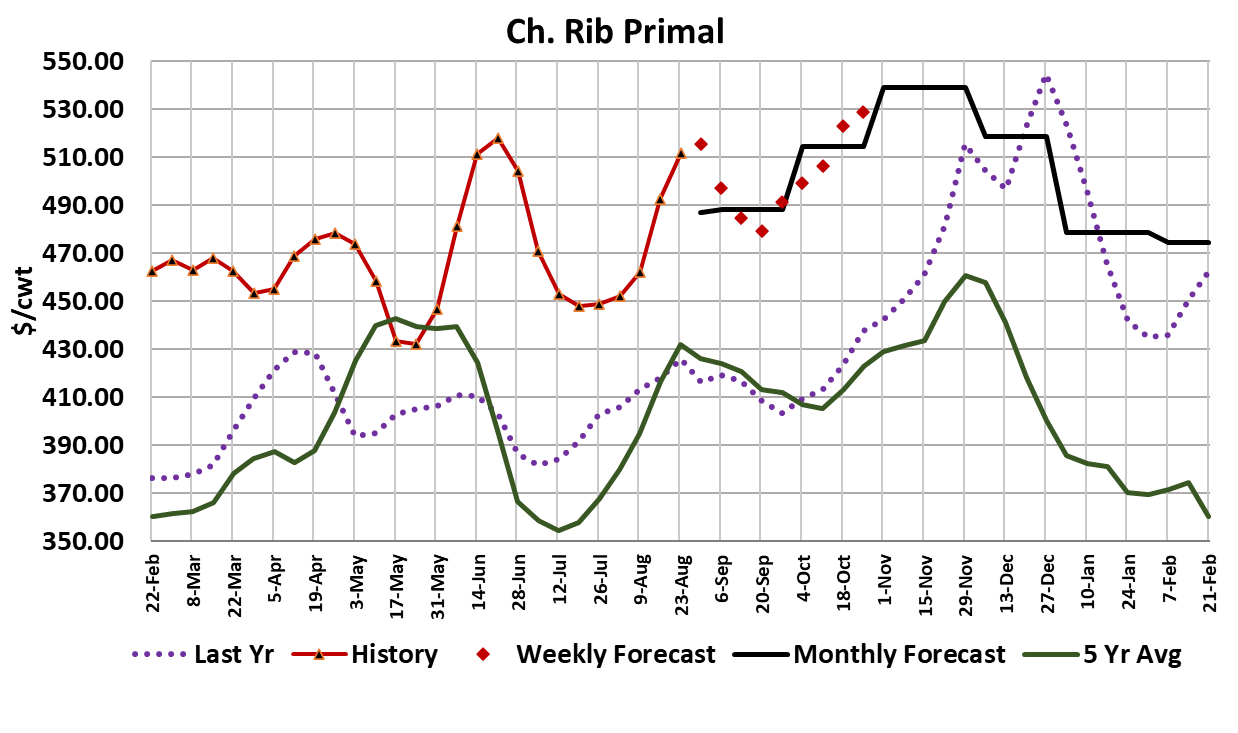

It was another good week for the beef cutouts, with the Choice gaining $6.64/cwt. on a weekly average basis and the Select adding $6.03/cwt. That helped packer margins considerably and, on top of that, packers managed to buy cattle at an average price that was about $2 below last week’s average. Trade in the South was mostly steady at $179/cwt., while trade in the North was $2-3/cwt. softer than last week. I calculate this week’s packer margin at about +$26/head, which is about $125/head stronger than it was just a couple of weeks ago. The packer’s willingness to adhere to reduced slaughter schedules is finally paying off. However, now that margins are back in the black, there will be a temptation to expand the kill where they can. This week’s fed kill came in close to 492k, up 11k from the week before. So, it looks like some kill expansion has already started, but the next two weeks will see small kills due to the Labor Day holiday. Packers will probably run a light Friday and Saturday kill next week to allow workers to enjoy the full weekend and that may mean that the fed kill doesn’t do much better than about 480k. The following week, there will be no kill on Monday (the holiday), but packers will run a huge Saturday to partially compensate. The fed kill could drop to 460k during Labor Day week. While it looked like the gains in the cutouts were slowing near the end of the week, they may not drop a whole lot over the next couple of weeks due to tighter availability. There was a lot of talk this week about the heat dome that developed over the central part of the country and how it might be detrimental to cattle performance, thus further limiting beef availability. It is unclear just how much of an effect the heat had on feedyard cattle, but the fact that we saw lower pricing out of the northern region, where the heat was most severe, tells me that it probably wasn’t a huge problem. The heat will relent next week, but the forecast says it might return during Labor Day week, so that is something to keep an eye on. USDA reported steer carcass weights up six pounds this week and I suspect they will go up another 4-5 pounds in next week’s data. If the heat affected carcass weights, it wouldn’t show up in the FI carcass weight data until data for the current week is released two weeks from now. The gains in the cutouts this week were driven by the rib, round and chuck primals. Stronger pricing on the ribs is likely due to last minute orders ahead of Labor Day and the gains in the end meats could be due to retailers preparing for post-holiday features that tend to favor end cuts as fall approaches. Trim markets were firm this week, with the 50s adding about $12/cwt. on a weekly average basis and the 90s up about $4/cwt. Reduced kills probably helped the 50s, while the 90s should be nearing a near-term peak and will likely trade lower after Labor Day. Domestic beef demand appears to be pretty good at present. The JSF Demand Index for August should come in around 1.072, up from 1.05 in July and 1.04 last year in August. I have relatively strong beef demand imbedded in the forecast for the remainder of 2023 and leads me to a Q4 Choice cutout projection very near $300/cwt. There are risks to demand however, the biggest of which is the restart of student loan payments in October. It also looks like the macroeconomy is starting to cool a bit here at the end of summer, so it isn’t a given that domestic beef demand will remain strong. International demand is weak to all destinations except Mexico. The FAS data on exports released this week looked absolutely awful with big drops in shipments to most of our Asian trading partners. Hopefully, that was just a data anomaly that will get ironed out next week, but we know that there are other countries where the macro picture is far worse than what we’ve seen here in the US. China is the biggest example that comes to mind. China has been a major destination for US beef ever since the Phase One agreement, but high unemployment and sluggish GDP in China may be tempering demand for expensive beef out of the US. The one bright spot is Mexico, which saw beef shipments last week running nearly 28% stronger than last year. Futures traders have been reluctant to build much of a premium over current cash into the futures curve. Dec futures settled today only $4 higher than the expiring Aug contract, and the Aug24 futures are only $4 premium to Aug23. That seems insanely small in an environment where the herd is shrinking rapidly and there are no signs of herd rebuilding. Maybe futures traders expect much softer beef demand next year, but it would take a huge drop in demand to offset the tightening in beef supplies that is already dialed in for 2024. My forecast has cash cattle exceeding the $200 mark sometime next summer, so clearly the futures are seeing things differently than I do. Next week, look for the ribs to ease lower as holiday buying dries up. Packers will be buying for a short kill week, so they might be able to shave a little off of cash cattle prices also. It is time to bring summer to a close and get geared up for the fall market and the challenges it may entail.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}